CCEP - Coca-Cola Europacific Partners: Brand Strength On Display

2023-10-18 13:56:26 ET

Summary

- Staples companies are finally seeing some resistance to price hikes, but Coca-Cola Europacific Partners' exposure to some of the strongest consumer brands in the world is serving it well.

- The proposed acquisition of Coca-Cola Beverages Philippines would add another higher growth market to its stable.

- At around 15x EPS, these shares continue to look reasonably valued given double-digit annualized EPS growth potential over the next few years.

Being economically subordinate to the Coca-Cola Company ( KO )("TCCC") has its downsides, but on the plus side it does give anchor bottler Coca-Cola Europacific Partners ( CCEP ) access to one of the strongest fast-moving consumer goods ("FMCG") brands on the planet. That has served investors well recently, with volume performance looking resilient in its core European business.

Turning to the stock, I thought it looked reasonably valued when I last covered it with a Buy rating in Q4 2022. The shares have done well in the interim, returning a little over 12.5% in around 11 months (including dividends) amid notable outperformance versus the broader global staples space.

Looking ahead, CCEP's hitherto resilient operating performance has seen it raise guidance for the full-year 2023, while it has also announced its intention to acquire a majority interest in Coca-Cola Beverages Philippines ("CCBPI") – an acquisition which should nicely supplement its growth outlook. With these shares still trading on a circa 15x EPS multiple, I continue to view CCEP as being reasonable value for the long-term investor.

Brand Strength Evident

Household savings built up by government stimulus and lockdowns may have provided a soft environment for staples firms to raise prices last year, but with inflation elevated and consumer finances increasingly stretched, this is increasingly no longer the case, with many firms now seeing pushback in terms of softer volume comps. Although this makes for a more difficult trading environment, it does also serve to identify the stronger brands in the FMCG space. Few are stronger than those owned by TCCC – a fact that was again demonstrated in CCEP's H1 2023:

Most importantly, our customers continue to share and support our success as we once again created more value in the retail channel for our customers within FMCG in Europe and within NARTD in Australia and New Zealand than our peers.

Damian Gammell, CEO CCEP, 1H 2023 Earnings Call

Volume has held up better at CCEP versus various other European staples I cover. In H1, company-wide comparable volume grew 1% year-on-year, with the away-from-home and home channels recording positive comps on both a year-on-year and pre-COVID 2019 basis. Revenue per unit case increased 10% year-on-year on price hikes and pack/brand mix, with overall revenue up 10.5% on a currency-neutral basis. Full-year guidance for revenue (up 8-9% versus 6-8% previously) and operating profit (up 12-13% versus 6-7% previously) were both raised.

Europe (~80% of company-wide volume and 75% of EBIT) has been particularly strong, with H1 volume up 2.5% (0.5% in Q2). Encouragingly, Q2 year-on-year volume comps were still positive in Great Britain, Germany and France, which are three of CCEP's top five markets. Volume was weaker in Asia, the Pacific and Indonesia ("API"), falling 5.5% in H1 (-11% in Q2), though some context is required here, as SKU rationalization in Indonesia drove much of that decline. API FX-neutral revenue growth was nonetheless still positive in both H1 (7%) and Q2 (0.5%).

Fig 1. (Data Source: CCEP Earnings Releases)

Fig 2. (Data Source: CCEP Earnings Releases)

Fig 3. (Data Source: CCEP Results Releases)

Fig 4. (Data Source: CCEP Earnings Release)

Comps versus pre-COVID levels aren't the cleanest here given the API segment was acquired through the Amatil deal , but looking at CCEP's two geographic segments discretely would indicate the company has done a good job managing the current bout of high inflation. In Europe, H1 2023 EBIT margin (~13%) was within around 30bps of the same-period 2019 mark (Fig 1), with unit case volume (~7% higher)(Fig 2), revenue (~22% higher)(Fig 3) and EBIT (~20% higher)(Fig 4) all advancing in line with my benchmark CAGR. API EBIT margin (~12.8%) is around 80bps higher than comparable-period 2019, with revenue and EBIT growth landing at a circa 6.5% and 8.5% CAGR respectively.

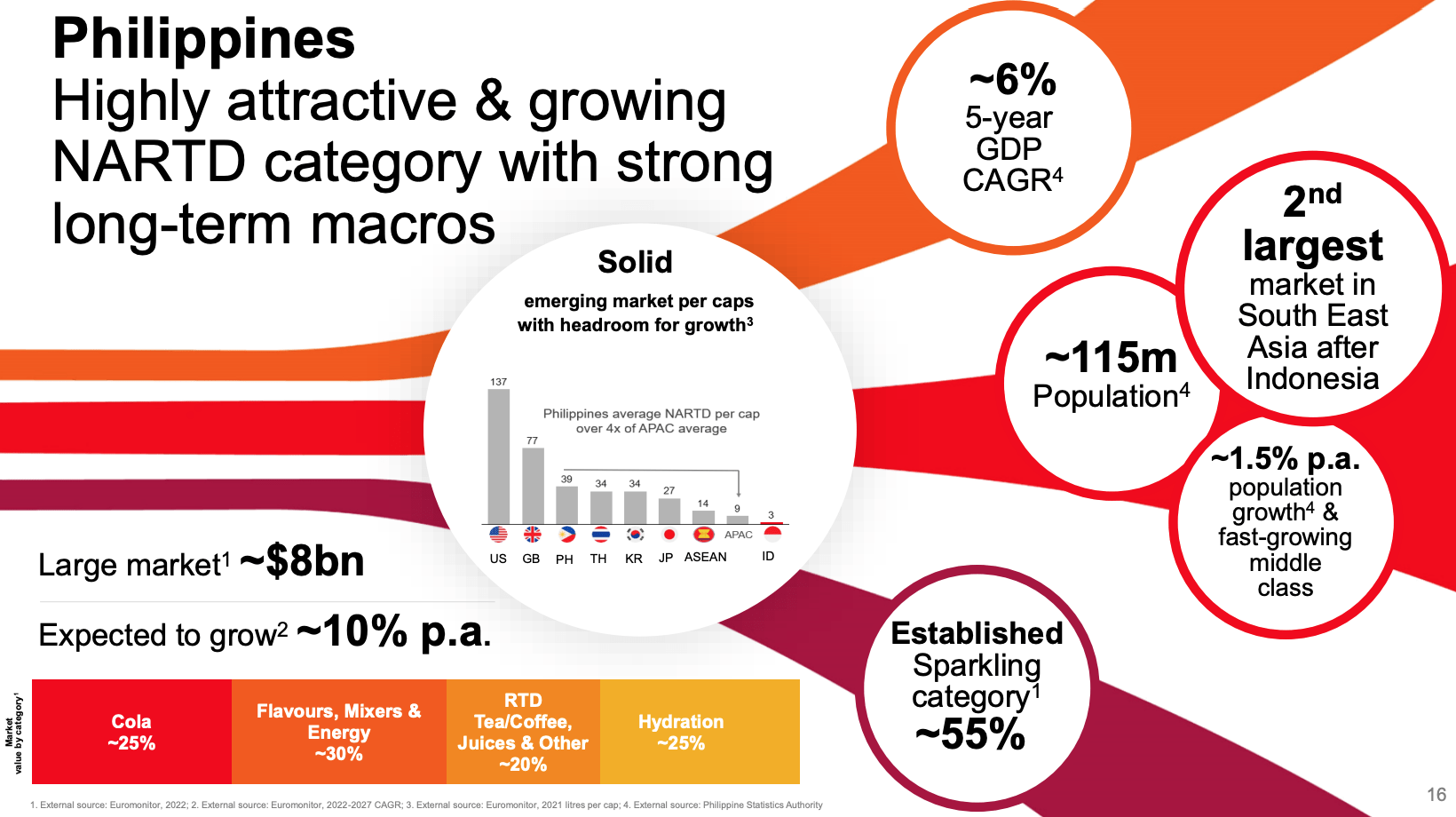

CCBPI Acquisition Can Support Growth

Alongside its Q2 results, CCEP announced its intention to acquire Coca-Cola Beverages Philippines in a 60:40 JV with Aboitiz Equity Ventures ( ABTZY )( ABOIF ). This would be a meaningful transaction for CCEP, doubling its API business in terms of volume and being immediately accretive to EPS.

{kind=link}

Source: CCEP 1H 2023 Results Presentation

At ~$1.8 billion (~$1.1 billion for CCEP's share), an implied multiple of ~10x EBITDA looks about fair given its better-than-average growth prospects. Per-capita consumption is quite high in the Philippines since it is actually TCCC's oldest foreign bottler, but it still trails developed international markets like Great Britain by a factor of two. Furthermore, demographics are still a positive tailwind in this part of the world (~1-2% CAGR), with strong GDP growth, a rising middle class, and ongoing urbanization all positives for beverage market growth. Management has that growing at ~ 10% CAGR, and although a challenging market in some respects (e.g. logistically), I do wonder whether management has some levers it can pull on operating leverage (e.g. integrating CCBPI into CCEP's current digital systems).

Still Reasonable Value

Given how defensive the business is I don't see much risk in the medium-term. Markets like Indonesia are a bit more macro sensitive and could surprise to the downside, but this remains a relatively small part of CCEP's business (~5% of revenue) – albeit one with good long-term growth potential. Inflation also seems to be moderating now. Higher energy prices maybe something to look out for, though CCEP has a fair amount of hedging in place through FY 2024 and again this is not something I would be too concerned about.

With that, these shares continue to look like a reasonable value for the long-term investor. The current price - $58.74 at time of writing - equates to around 15x my FY 2023 EPS estimate (~$3.91 at the current USD/EUR exchange rate), while CCEP's medium-term growth formula remains in place from last time out. That means low single-digit contributions from both volume and revenue per unit case from FY 2024 onwards, with around 40-50bps per annum of EBIT margin expansion on top. That maps to an FY 2025 EPS target of circa $4.60 – roughly in line with Seeking Alpha's consensus estimate. Management further aims to pay out 50% of EPS by way of the dividend, which by my count would imply around $4.35 per share cumulative over the next couple of years. On a flat 15x FY 2025 EPS multiple, investors would therefore be looking at a total return price of $73.35 per share in two years' time, equal to ~ 11.7% CAGR from the current share price. With that, I reiterate my Buy rating.

For further details see:

Coca-Cola Europacific Partners: Brand Strength On Display