WFC - Commercial Real Estate Could Add To U.S. Regional Banking Troubles

2023-04-26 16:06:14 ET

Summary

- At first glance, it may seem that the current commercial real estate lending sector has less excessive risk-taking than in the Global Financial Crisis.

- However, as a result of structural issues in the office market due to the increasing trend of working from home, office assets have seen increasing vacancies, underutilization and shadow vacancies.

- On top of that, $1.5 trillion in commercial real estate debt is due to be refinanced in the next three years at a higher interest rate and lower loan-to-value ratio.

- The worst-performing office assets today are the older and lower quality assets. Office assets developed before 2015 have seen negative absorptions since Covid-19.

- When everyone is rushing for the exit, regional banks that hold considerable amounts of commercial real estate debt may find themselves in trouble.

This article was first posted in Outperforming the Market on April 25, 2023.

Having been exposed to both private and public real estate, I think that there is a general view that the commercial real estate sector could be hit hard from the effects of what has happened to the smaller and mid-sized banks.

Commercial real estate could be the next domino to fall and this article explains just why that is so.

First look suggests excesses in commercial real estate not as bad as prior cycles

It can be said that in the current cycle, it seems that the excesses in commercial real estate are not nearly as bad as in prior cycles.

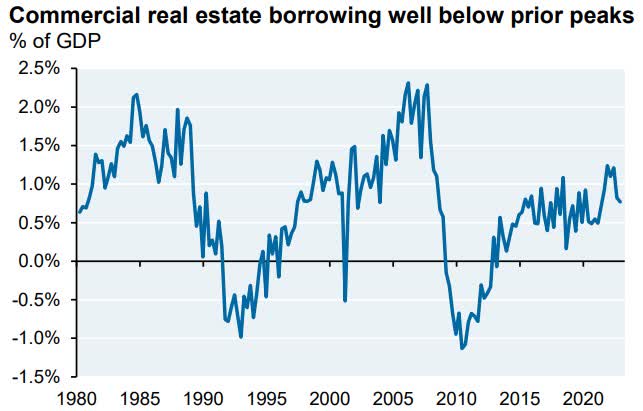

Commercial real estate lending is well below its prior two peaks in the 1980s and the 2000s.

Commercial real estate borrowing well below prior peaks (Federal Reserve Board, BEA, JPMAM)

{kind=link}

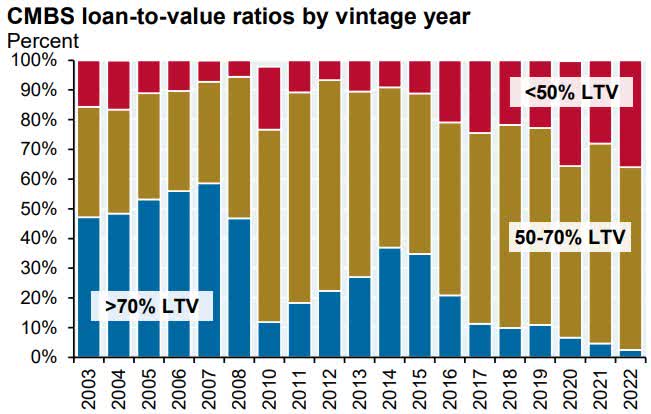

Furthermore, we have seen significant improvements in the underwriting standards in the Commercial Mortgage-Backed Securities ("CMBS") markets since the Great Financial Crisis. It has resulted in the weighted average loan-to-value falling from its peak of 70% in 2007 to around 55% today. Thus, the lower loan-to-value ratio we see today is definitely a positive sign that the risk taking we are seeing in the commercial real estate market remains relatively subdued.

CMBS weighted average loan-to-value by vintage year ( JPMAM)

Lastly, I have segregated the loan-to-value ratios by categories, separating those with less than 50% loan-to-value ratios, those with more than 70% loan-to-value ratios and those with between 50% to 70% loan-to-value ratios. As can be seen, the percentage of CMBS that has less than 50% loan-to-value ratios have increased over the years, while those with more than 70% loan-to-value ratios have decreased significantly over the years.

CMBS loan-to-value ratios by vintage year (JPMAM)

{kind=link}

The first problem: Regional banks

While we have covered the CMBS market earlier, since the Great Financial Crisis, the CMBS markets make up a relatively small share of the lending in commercial real estate.

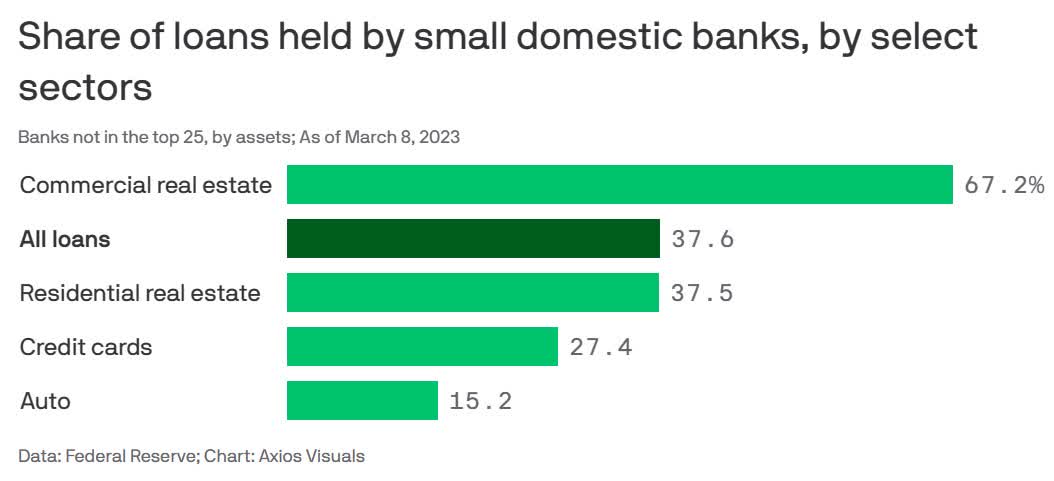

In fact, 90% of the increase in bank commercial real estate loans since 2015 was contributed by regional banks.

As stated by UBS, banks with less than $250 billion in assets actually account for 80% of commercial real estate lending.

The data varies, but the vast majority of the data points to around 60% to 80% of commercial real estate lending comes from banks with less than $250 billion in assets.

Share of loans held by small domestic banks, by select sectors (Axios)

{kind=link}

Needless to say, with the stress the regional banks have been seeing in the past few weeks, it is expected that we could see stress in the commercial real estate lending sector as well.

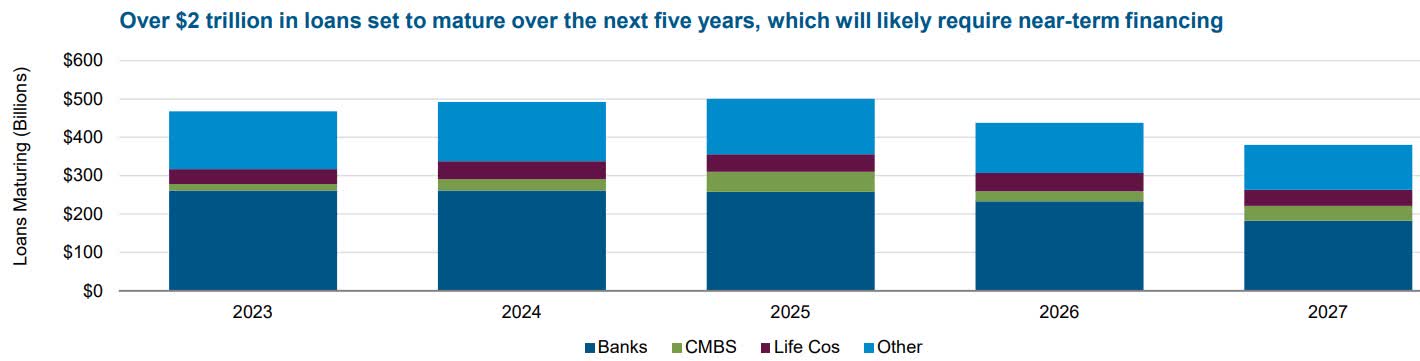

PIMCO estimates that more than $2 trillion in loans in the commercial real estate sector are expected to mature over the next five years and these will require near-term financing.

Over $2 trillion in loans set to mature over the next five years, which will likely require near-term financing (PIMCO)

{kind=link}

Other sources state that $1.5 trillion in commercial real estate debt is coming due in the next three years. As these need to be refinanced and the regional banks will now increase their lending standards, this could mean lower loan-to-value ratios and higher interest rates than when all these commercial real estate debts were initially financed.

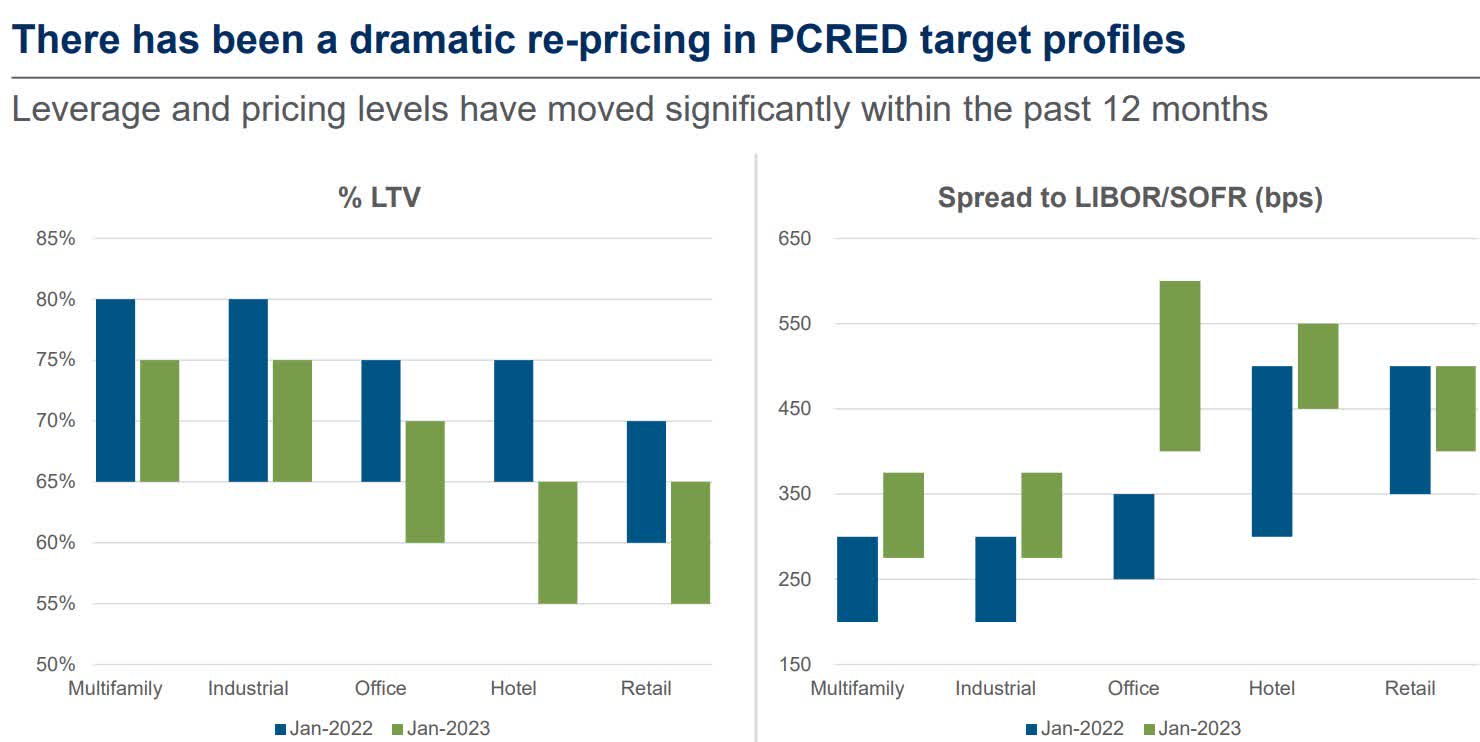

PIMCO's commercial real estate debt fund has seen loan-to-value ratios and spreads reprice dramatically in the last 12 months as a result of what has happened, with the most significant repricing happening in the office space.

Leverage and pricing levels have moved significantly within the past 12 months (PIMCO)

{kind=link}

I do think that the office sector may be the most vulnerable as fundamentals of the sector have been rather weak as a result of structural shifts in the sector due to the work from home trend since the pandemic.

The second problem: Structural issues

As a result of the Covid-19 pandemic, workers all over the world, including in the US, had to work from home. This proved that working from home was indeed possible and that work could be done from home rather than in the office.

As a result, in the US in particular, there has been a structural shift away from the office and towards working from home. The appeal for working from home includes saving on the travel time which could be used more productively.

As a result, the office market faced a structural decline in the US after the Covid-19 pandemic as occupancy for the office market faced problems, particularly so for the lower quality offices.

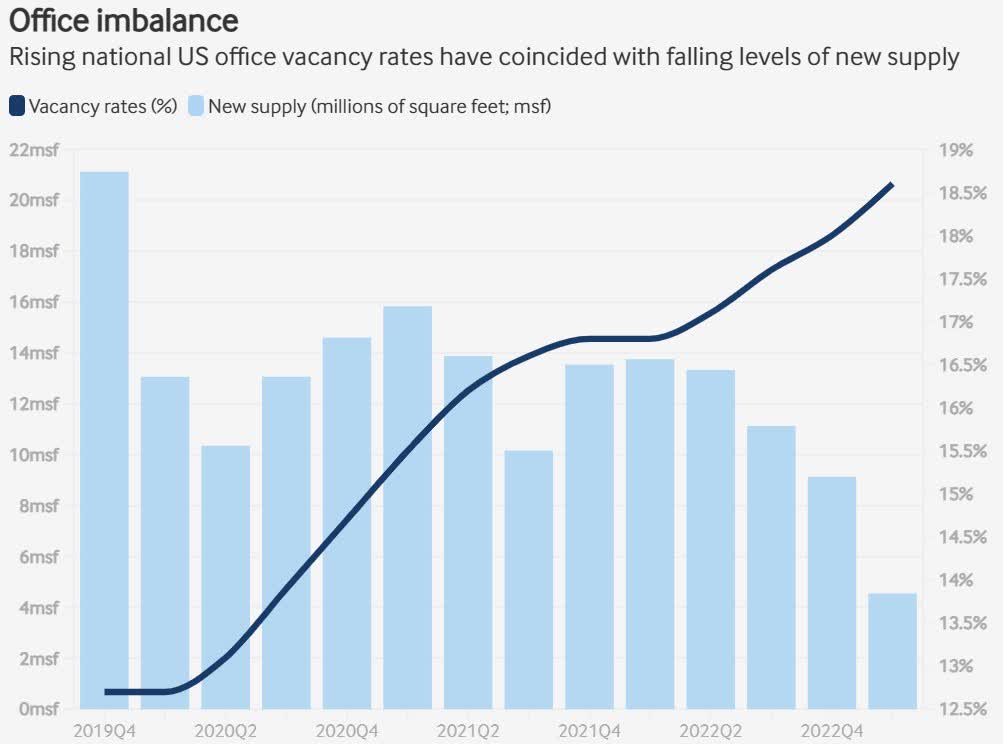

In the US office market, vacancy rates have reached all-time highs at close to 19% despite new supply coming off.

US office vacancy rates ( Cushman & Wakefield)

{kind=link}

While vacancy rates and occupancy rates are the most apparent metrics that are most publicly released, the amount of underutilized space and shadow vacancy is also important to understand exactly how much stress the office market is facing.

As can be seen below, based on the different states, we can see the amount of underutilized space, and the shadow vacancy. Austin has one of the least stressed office markets while San Jose, Philadelphia and Washington are one of the most stressed office markets.

Office stress measures by market (Kastle Systems, CoStar, First American, JPMAM)

Despite Covid-19 largely behind us and NYC transit even staging a decent recovery, there has been a gap between the improvements in the utilization of office compared to the improvement in the NYC transit use.

NYC transit use vs office utilization (Kastle, MTA, JPMAM)

JLL reported that Manhattan office vacancy reached an all-time high of 16% and about two thirds of all leasing activity is renewals rather than new leases.

Furthermore, with all the headcount reductions we have seen in the big technology companies like Microsoft ( MSFT ), Meta Platforms ( META ) and Amazon ( AMZN ), this will lead to downward pressure on office spaces and demand in the near-term.

Green Street estimates that at a national level, office appraisal values have fallen by 25% in the past year alone, which is the largest decline of any property type.

Since the pandemic, Costar found that the US office market rent growth has even underperformed the retail market rental growth.

Rent growth by property type (Costar)

Where will the pressure be the most in the office markets?

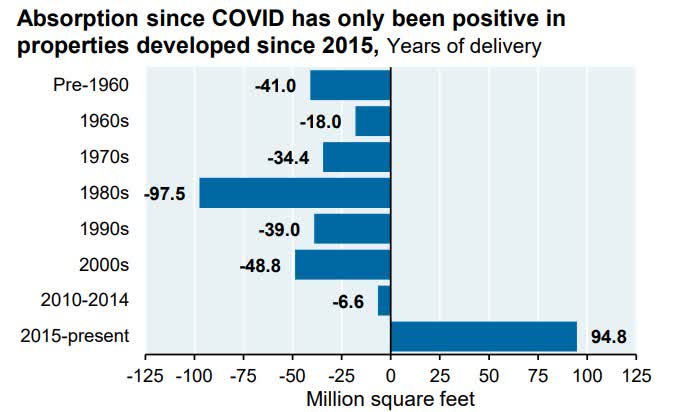

Undoubtedly, older properties and lower quality properties are likely to be hit the most. As evident in the chart below, absorption since Covid-19 has only been positive for properties that were developed since 2015. As a result, companies are looking at their office real estate, refocusing their remaining office leases on the newer and higher quality office assets while the older and lower quality ones have performed poorly since the pandemic.

Absorption since COVID has only been positive in properties developed since 2015 (JPMAM, Trepp)

{kind=link}

How will all this affect office properties? As shown below, if I assume a modest change in cap rates, loan-to-value falling 10 percentage points from 70% to 60% and net operating income sliding 8%, this implies that 30% of the original property value has to be raised in expensive mezzanine financing when the loans need to be refinanced in the current environment.

Property value as a function of cap rate, NOI and LTV (JPMAM)

Its relatively easy for equity investors to exit and reduce office exposure but lenders of commercial real estate may find it harder to reduce and exit their exposure to the US office market, particularly those with office assets that are lower quality and older.

For US banks, about 20% of their total commercial real estate lending is in the office market and it might be more challenging for these players to be offloading any of their loans that they deem higher risk in the current environment.

Again, this is a highly correlated market with linkages across markets. With the values of office assets declining and fundamentals worsening, banks with substantial exposure to commercial real estate loans, particularly office loans, are definitely at a higher risk.

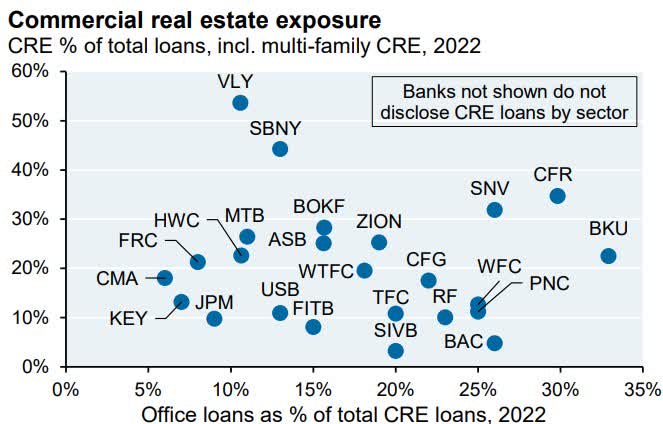

As can be seen in the graph below, Valley National Bancorp ( VLY ), Signature Bank (SBNY), Cullen/Frost Bankers and Synovus Financial ( SNV ) have higher commercial real estate loans in their loan book as a percentage of their total loan book. On the other hand, players with more than 25% of their commercial real estate loan book in office loans include PNC ( PNC ), BankUnited ( BKU ), Wells Fargo ( WFC ), Cullen/Frost Bankers and Synovus Financial

Bank's commercial real estate exposure ( Bloomberg, GS, JPMAM)

{kind=link}

JP Morgan did a bank stress test assuming that there will be a 21% delinquency rate for office assets, 15% for retail and with a recovery rate of 60% for both while the losses are assumed to be incurred over three to five years. It found that this will lead to about 30 to 40 basis points of reduction in Tier 1 capital at some smaller regional banks. That said, it assumes that 2022 pre-provision income will be sustained over the three to five year period when the pre-provision income is actually probably going to fall as a result of a likely recession as well as higher cost of customer deposits. As a result, I do think that the impact to Tier 1 capital could be larger than expected.

Conclusion

All in all, I think the fact that the banking and the real estate sector are highly interlinked is re-emphasized here.

On the surface, it seems that there is less excessive risk taking in the commercial real estate market today. That said, because of the weakened regional banking sector as a result of what has happened to customer deposits and increased scrutiny on their unrealized losses on securities, these regional banks are likely to increase lending standards substantially.

Given that a large majority of commercial real estate lending comes from these regional banks, there is a refinancing risk for the commercial real estate sector. We discussed that within the commercial real estate sector, the office sector has seen a structural decline as a result of the working from home trend and this has decimated the office market, especially for older and lower quality office assets.

Once again, these regional banks also hold commercial real estate loans and office loans, which are difficult to exit or reduce exposure to as a result of the weak office markets. This then increases the risks for these regional banks that have a larger exposure to the office market and the commercial real estate market.

I would avoid stocks with office exposures, be it REITs or financials for the time being to avoid catching a falling knife, until the current commercial real estate lending and office market stabilizes. These includes REITs like Alexandria Real Estate Equities ( ARE ) or Boston Properties ( BXP ), which have fallen 47% and 65% from their peaks.

For further details see:

Commercial Real Estate Could Add To U.S. Regional Banking Troubles