GIS - Conagra Brands Q2 Earnings: Positive Volume Trends Despite Top Line Pressure

2024-01-04 10:15:27 ET

Summary

- Consumer packaged goods company Conagra Brands just reported its fiscal second quarter results.

- The company’s mixed showing, with a beat on earnings and a miss on sales, sent shares lower by approximately 3% immediately following the release.

- The results follow significant share price underperformance relative to both the sector and the broader markets.

- At current trading levels, I view Conagra Brands stock as an attractive addition for investors seeking defensive positioning in the new calendar year.

Conagra Brands ( CAG ), the maker of a variety of consumer staples and foods including Hunt’s Tomato Sauce and Slim Jim meat sticks, is fresh off its fiscal Q2 earnings release . Ahead of the release, the stock has lagged over the past year, with losses of approximately 25%.

While current results likely didn’t inspire the most significant change in sentiment, Conagra appears to be heading in the right direction. Importantly, volume trends are exhibiting signs of significant improvement, particularly in their frozen foods division. Looking ahead, I am expecting continued recovery in this metric. At current trading valuations, I view CAG as attractive for those seeking a more defensive posture in the new calendar year.

CAG Stock Key Metrics

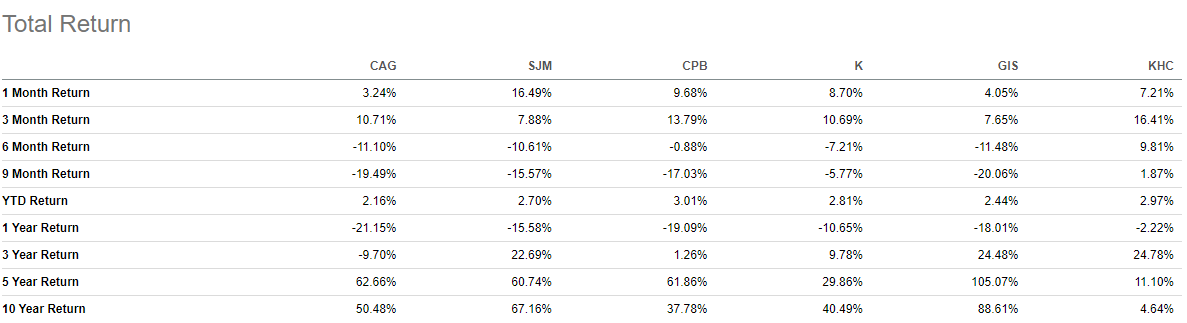

Though CAG’s share price performance over the last year is comparable to others within the sector, the stock has traded more muted in the last month. This compares to a relatively strong start elsewhere. Campbell Soup Company ( CPB ) and The Kraft Heinz Company ( KHC ), for example, have both gained about 3.5% in the last five days. The J. M. Smucker Company ( SJM ), more impressively, is up over 16% in the last month. The gains across the packaged food sector may be indicative of a more defensive posture from some investors returning from the holiday break.

Seeking Alpha - Total Returns Of CAG Stock Compared To Peers

{kind=link}

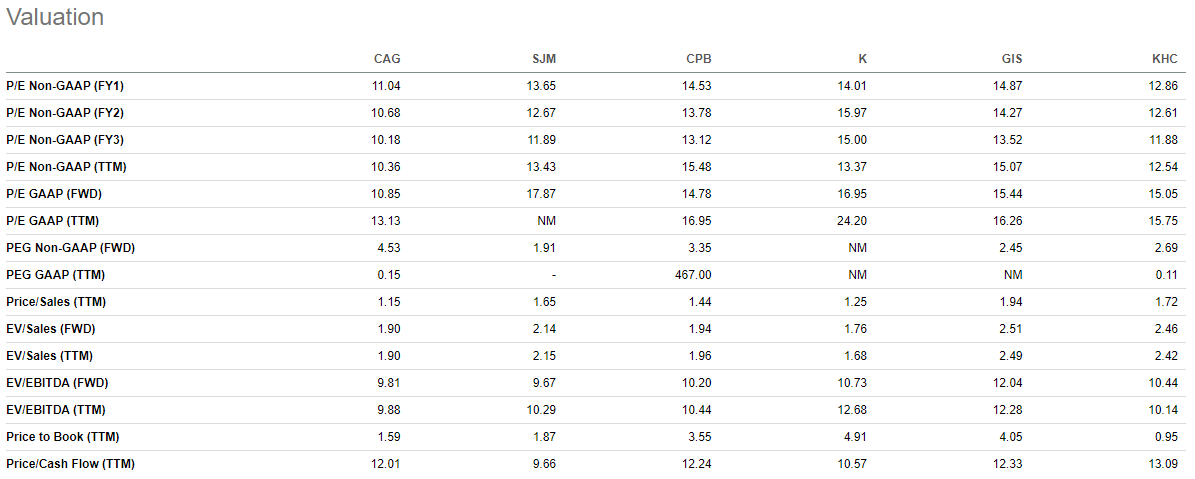

The lagging share price performance in CAG position the stock at a discount to its peers in most regards. On a forward basis, shares command an earnings multiple of approximately 11x. This is about 4 to 5 turns below the multiple held by the peer set. Additionally, its EV/EBITDA multiple of under 10x is well below its five-year average of 15x.

Seeking Alpha - Valuation Metrics Of CAG Stock Compared To Peers

{kind=link}

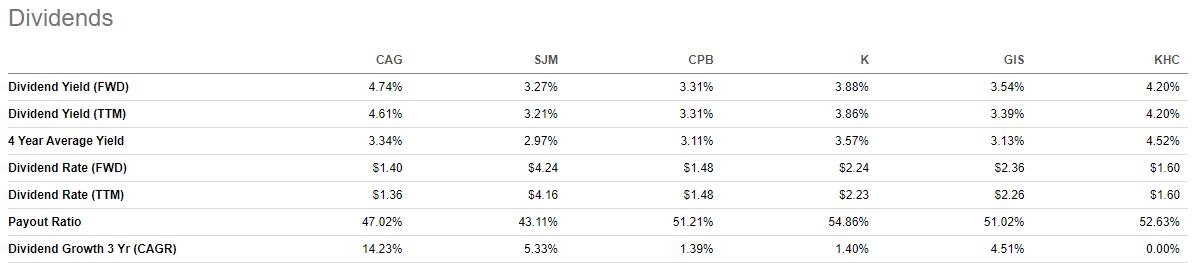

In addition to potential share price upside, the subdued valuation of CAG is also resulting in a peer-leading dividend yield of 4.75%. Also worth mentioning is the attractive dividend growth rate of approximately 5% on a compounded 5-year basis.

Seeking Alpha - Dividend Profile Of CAG Stock Compared To Peers

{kind=link}

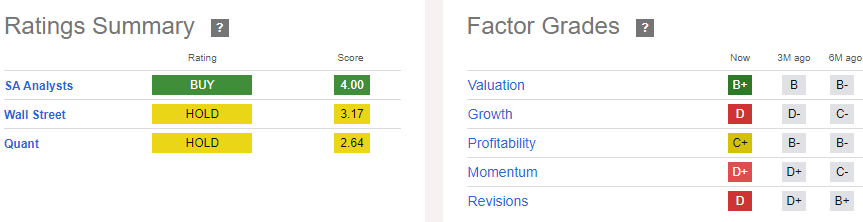

Despite the attractive metrics, analysts on Wall Street remain neutral on the stock, with an average price target of an underwhelming $30/share. Seeking Alpha’s (“SA”) quant ratings are similarly neutral. The broader SA community , meanwhile, is generally more bullish overall.

Seeking Alpha - Ratings Summary Of CAG Stock

{kind=link}

CAG Q2 Financial Recap

CAG reported mixed quarterly results, with a miss on revenues but a beat on the bottom line. During the quarter, organic net sales decreased 3.4% due largely to continuing headwinds in consumer consumption trends. Like the quarter prior, consumers were still reported to be stretching their existing supplies via either more hands-on prep as opposed to convenience or more use of leftovers. This is consistent with the consumer environment experienced by others within the sector.

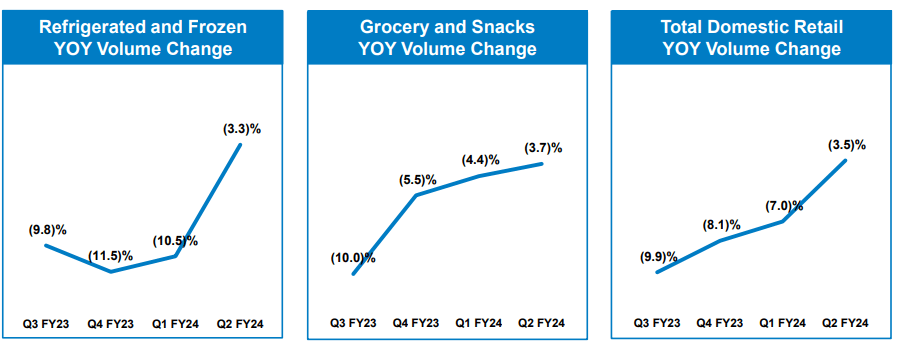

Though overall sales were down, CAG made significant progress on improving volume trends; in particular, within their refrigerated and frozen food businesses. While volume was still negative, the extent was much less so in this segment.

CAG Q2 Earnings Presentation - Graph Showing Volume Recovery Across Frozen Foods and Groceries And Snacks

{kind=link}

Two segments that continue to outperform are CAG’s international and foodservice units. This is notable, as the two combined represent nearly 20% of CAG’s total net sales.

The international segment delivered YOY volume growth of 3.3%, building significantly on last quarter’s 0.3% increase. The segment also benefitted from improved price mix, which ultimately supported strong organic net sales growth of 8.1% during the quarter. Likewise, the foodservice segment delivered organic sales growth of 4.3%, primarily resulting from favorable mix.

Though overall advertising and promotional spend was down, SG&A expenses still increased 6.8% during the quarter due to impairment and legal reserves taken in the reporting period. The higher SG&A combined with continued cost inflation and lower organic net sales ultimately contributed to weaker margins during the quarter.

During the period, adjusted operating margins were 15.9%, representing a 108 basis point decrease over the prior year. Similarly, adjusted gross margins also declined. Compared to 27.6% last quarter, CAG reported a margin rate of 26.9% in Q2. Though lower, this was expected based on prior commentary in Q1.

What Does Conagra Expect For Remainder Of Fiscal Year?

Similar to competitor General Mills ( GIS ), who reported earnings previously, Conagra paired back their full-year guidance following the release of results. CAG now expects full-year net sales to decrease between 1% and 2% compared to a previous estimate of 1% growth. The range is slightly more pessimistic than General Mills, who guided for flat to negative 1% sales growth.

Expectations for operating margins were also tempered. Instead of margins of between 16% and 16.5%, CAG now sees adjusted operating margins at 15.6%. The lowered margin expectations in conjunction with the weaker sales outlook likely contributed to the downward revision in full year EPS. CAG is now guiding for an EPS midpoint of $2.625/share, down ten cents from the prior midpoint of $2.725/share.

Despite the negative revisions, CAG did make positive strides in their frozen food business during the quarter. While the segment still reported negative sales growth, volume performance improved significantly. In the reporting period, volume declined 3.3%, much improved from the 10.5% decrease seen last quarter. This should provide assurance of CAG’s ongoing investments in the business.

Is CAG Stock A Buy, Sell, Or Hold?

Behavioral shifts in consumer spending patterns over the past year have weighed on Conagra and others within the sector. While the current period results indicate these dynamics still exist, I view CAG stock as well positioned for a second half rebound.

For one, Conagra Brands, Inc. should benefit from a more favorable comparable environment. Last year, CAG was impacted by a fire at their Jackson plant in the second half of their fiscal year. This significantly impacted their frozen fish business, a key staple around Lent. Similarly, CAG also operated through a can meat recall through both Q3 and Q4. Barring the negative externalities this fiscal year, I am expecting a significant tailwind in these categories.

More-leveled profitability in the form of stable gross margins also provides CAG greater flexibility in increasing their advertising and promotional activity on their biggest businesses. While this could negate some of their pricing actions, it could also drive volume, which is a more pressing need across the industry in my view.

At a forward trading multiple of approximately 11x, Conagra Brands, Inc. is trading at a discount to both the broader markets and to the peer set. At $35/share, CAG would still trade at a discount to peers yet present upside potential of over 15% to long-term focused investors. For investors seeking defensive positioning in the new calendar year, I can see CAG rising to this target in the months ahead on an improved consumer backdrop and continuing strength in CAG’s international and foodservice segments. Following earnings, I am bullish on CAG and view shares as a “buy.”

For further details see:

Conagra Brands Q2 Earnings: Positive Volume Trends Despite Top Line Pressure