STZ - Constellation Brands: Beer Segment Shows Strong Performance

2023-10-13 06:06:35 ET

Summary

- I recommended a buy due to the expectation of resolving near-term challenges, continued growth in the beer segment, and improved valuation as the company reduces its debt.

- STZ's beer segment is the largest revenue and profit driver, with consistent organic growth and stable margins.

- Recent financial results show strong performance in the beer category, with increased net sales and share gains, and management's commitment to deleveraging supports a positive outlook.

Overview

My recommendation for Constellation Brands (STZ) is a buy rating as I expect near-term headwinds to resolve themselves overtime, the beer segment to continue its traction, and valuation to improve as STZ deleverages its balance sheet.

Business

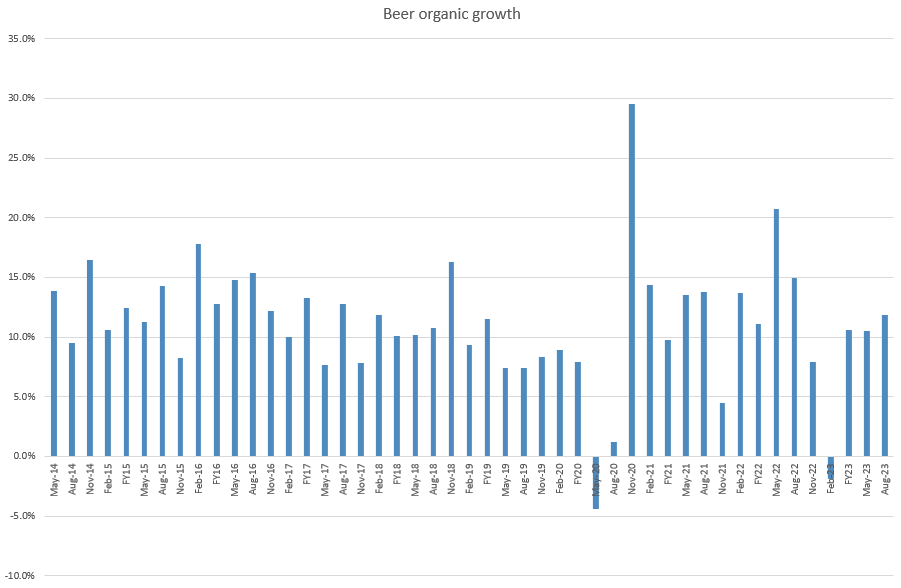

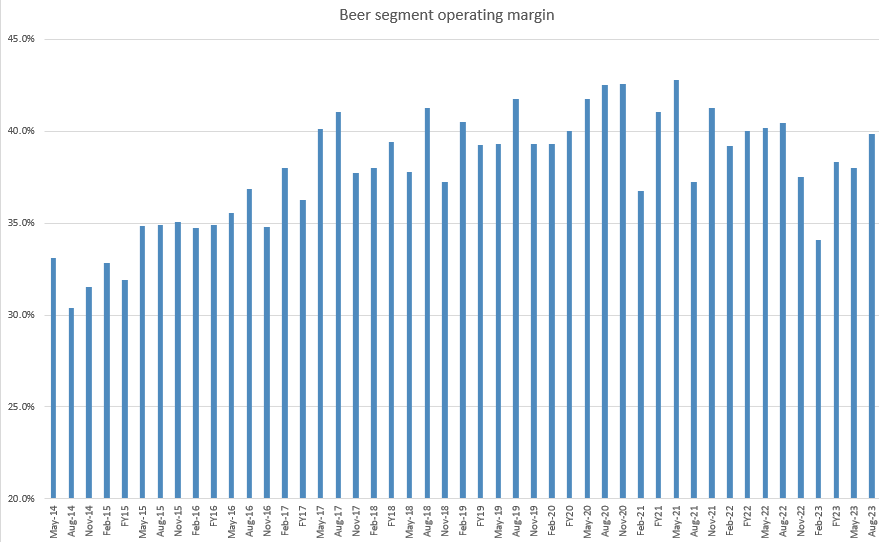

STZ manufactures alcoholic beverages. The company portfolio includes categories in beer, wine, and spirits. In each of these categories, STZ owns multiple brands that enable them to tap into a wide array of customer preferences in the United States (97% of revenue from the US). Of the three categories, beer is the largest revenue and profit driver, representing 84% of revenue and 92% of segment operating profit. Over the years, STZ has done a remarkable job of growing the beer segment organically, as it has only seen two negative growth periods over the past ~10 years. Similarly, margin also increased over the years and stabilized at ~high 30+% range.

Author's valuation model Author's valuation model

{kind=link}

{kind=link}

Recent results & updates

On October 5th, STZ announced 2Q24 EPS of $3.70, which was significantly higher than the consensus estimate of $3.39. Net sales growth of 6.8%, which beat consensus estimates by 400 bps, was largely responsible for this. Beer sales growth of 11.8% was partially offset by a 13.9% decline in wine and spirits sales. Given the composition of total sales, however, the rapid growth of the Beers division stands out. Increases in both volume shipped and price/mix contributed to growth in the beer category, which grew by 8.7 percent. While the beer segment gross margins contracted 229 bps to 51.4%, the segment was slightly more operating cost-efficient, cushioning the decline in gross margin (segment operating profit fell by 60 bps to 39.9%).

In light of the strong performance in the Beer segment, management has revised its guidance positively. They now anticipate beer net sales growth to range between 8% and 9%, which represents a 100 bps increase at the midpoint compared to the previous range of 7% to 9%. Additionally, the beer operating profit growth is expected to be in the range of 6% to 7%, with a 100 bps increase at the midpoint, as opposed to the prior range of 5% to 7%. While it's worth noting that the updated guidance suggests no alteration to the beer operating profit margin of 38% for FY24, management has effectively communicated the forthcoming challenges for the Beer segment in the second half of the year. This transparency should help align market expectations, making it unlikely for STZ to fall short of consensus estimates. There are four primary headwinds that will impact STZ in the short term:

- Seasonality and the potential impact of brewery maintenance in 3Q24 will cause STZ shipments to decrease sequentially in the second half of the year;

- The effect of the price increase implemented by STZ in October 2022 and the subsequent retail pre-buying cycle will be lapped by the company by the beginning of 3Q24;

- STZ will experience operating deleverage due to increased fixed cost absorption and marketing expenditures;

- STZ will be negatively impacted by foreign exchange rate fluctuations due to a stronger peso and offsetting lower inflationary pressures.

At a glance, these headwinds might seem a lot to digest and are worrisome. However, the way I see it, these headwinds are not as bad as they seem. Importantly, they are mostly non-structural to the business and should resolve themselves over time.

- For points 1 and 2, it is a matter of timing and should not repeat

- For point 3, it can be argued to be a matter of timing, as STZ needs to reinvest in the business to capture more volume, which will drive margins upward. I point readers to the Beer segment operating margin chart above, where it shows periods of margins moving up and down intraquarters, indicating that this type of volatility is not uncharted territory.

- For point 4, there is nothing STZ can do about this but bite the bullet. That said, it is not a structural weakness.

In contrast, qualitative comments provided by management give confidence that the beer segment growth momentum is on the right track. Specifically, management is seeing share gains continue for its beer brands into 3Q24.

Not only did we remain the top share gainer over the entire critical summer season, we also extended our leading position from Cinco de Mayo to become the number one share gainer in tracked channels during the 4th of July holiday. And although it falls slightly after our second quarter end, I'm also pleased to report that we further accelerated our share gains during Labor Day.

Modelo Especial remained the key driver of our strong performance, achieving double-digit volume growth in tracked channels and an 8.6% increase in depletions, ultimately strengthening its position as the top brand across the entire U.S. beer market and dollar sales fiscal year-to-date. The broader Modelo brand family also delivered phenomenal results, with Cheladas achieving 50% volume growth in tracked channels and an increase in depletions of over 40%, while Oro continues to build on a solid launch, increasing its share gains in the overall beer category and performing in line with our plans for the fiscal year.

Beyond Modelo, our Corona Extra and Pacifico core beer brands also continued to perform strongly. Corona Extra delivered solid low single-digit growth in depletions and tracked channel volumes and was the number six share gainer in the category, while Pacifico achieved 15% depletion growth, tracked channel volume growth of approximately 27%, and was the number 11 top share gainer in tracked channels. from: 2Q2024 earnings call

On the balance sheet front, I expect management to continue keeping their foot on their accelerator to deleverage the business, thereby contributing to EPS growth. This was well reflected in management guidance, where they raised their comparable EPS outlook for FY24 and now expect EPS of $12 to $12.20 vs. the prior $11.70 to $12.00, reflecting tighter interest expense management. As of 2Q24, STZ has a net debt position of nearly $12 billion, or a 3.2x net debt to EBITDA ratio (management is targeting 3x). Given the cash flow generation capacity of STZ (FCF has been positive for 10 straight years), I don't see an issue with STZ reaching its 3x target.

Overall, I think the results were great, and I was surprised to see the poor share price action. I believe the market might be overly focused on the near-term headwinds, which should resolve themselves over time. As such, we continue to see any weakness in the stock as an attractive entry point for investors.

Valuation and risk

Author's valuation model

According to my model, STZ is valued at $267 in FY24, representing a 12% increase. This target price is based on my growth forecast of 5% in FY24, a deceleration from FY23 of 7% due to the headwinds mentioned above, and an acceleration back to 7% as the headwinds resolve themselves over time. For net income, I use management EPS guidance as a benchmark for FY24 and expect FY25 margins to improve modestly due to operating leverage as the beer segment continues to see volume growth. While margin might see some headwind from reinvestments into the business (fixed cost absorption), I believe the savings from deleveraging the business (lower interest expense) should negate these headwinds.

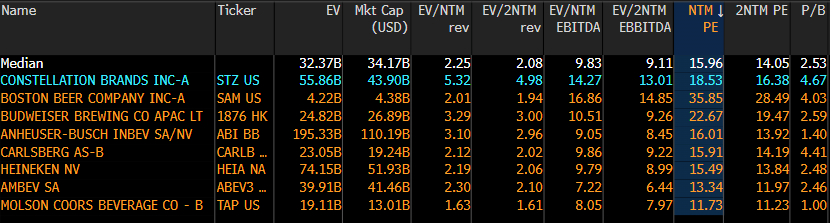

STZ is now trading at 18.5x forward PE, which I believe will rise gradually as I believe STZ should trade at the higher end of the group, closer to Budweiser, given they have similar revenue size, growth profile, and margin.

- Both of have similar revenue size range, with Budweiser at $7 billion and STZ at $9 billion.

- Budweiser is expected to grow 8 to 9% over the next two years, which is relatively close to STZ expected growth of 7%

- Both have similar EBITDA margin profile of 30+%

The difference is that Budweiser has a stronger balance sheet and a net cash position. Hence, I see the path for STZ to close its valuation gap against Budweiser is by deleveraging its balance sheet, and management is keen on doing so.

{kind=link}

The inherent risk with STZ is that it sells an unhealthy drink that will continue to face pressure as consumers become more health-conscious. While it is unlikely that everyone will stop drinking alcohol in the near term, if more and more consumers switch to non-alcoholic drinks, it will definitely impact the long-term growth of the business. Moreover, it would be almost impossible for STZ to transition any of its alcoholic brands to a non-alcoholic brand, as consumers associate the brand with alcohol. STZ would have to create a new brand to compete in the large non-alcoholic beverage industry that is dominated by several large players.

Summary

In conclusion, I recommend a buy rating for STZ, as I anticipate that the short-term challenges will gradually resolve themselves, the robust performance of the beer segment will persist, and valuation will improve as STZ continues to reduce its debt. STZ operates in the alcoholic beverages industry, with a strong focus on beer, which constitutes the majority of its revenue and profit. Recent financial results have been promising, particularly in the beer category, with notable growth in net sales and share gains. Although there are near-term headwinds to contend with, these challenges are largely temporary and not indicative of structural issues in the business. Management's commitment to deleveraging and improved guidance for EPS further support the positive outlook. Despite short-term concerns, STZ's prospects appear strong, and any market weakness presents an attractive entry point for investors.

From a valuation perspective, I project a target price of $267 for FY24, reflecting anticipated growth of 5% for the year and a gradual return to 7% growth as headwinds dissipate. STZ's forward PE ratio of 18.5x is expected to rise as it aligns more closely with peers like Budweiser due to similar revenue size, growth potential, and margin profile. The key to narrowing this valuation gap lies in STZ's ongoing deleveraging efforts.

For further details see:

Constellation Brands: Beer Segment Shows Strong Performance