STZ - Constellation Brands: Too Expensive Right Now Waiting For A Pullback

2023-12-19 00:43:13 ET

Summary

- Constellation Brands' share price went nowhere all year, prompting me to look into it further.

- The company's financials are recovering and should continue to trend up.

- The beer segment is showing a lot of promise, and I wouldn't rule out international expansion after such a success in the US.

- However, the company at this price is still a bit too expensive for me, therefore, I will be waiting for a pullback or further improvements in earnings.

Investment Thesis

Constellation Brands ( STZ ) has gone nowhere in the last year, which prompted me to look into the company 's finances more in-depth to see why that may be. The company 's debt pile is manageable, and it exhibits respectable top-line growth while gaining market share, however, there are a few uncertainties that keep me away from recommending a buy at this time, like the wine and spirits segment underperformance and the baffling investment into cannabis business which is hurting the company 's bottom line. With conservative assumptions, the company is too expensive right now and would like to see a good pullback or a dramatic improvement in earnings going forward.

Briefly on the Company

STZ is a major American producer of beer, wine, and spirits. The major importer in the US and sells alcohol under brands like Modelo, Corona, and Pacifico. In the Wines and Spirits segments, under the names Robert Mondavi, Kim Crawford, and SVEDKA Vodka.

Financials

As of Q2 '24, the company had around $83m in cash and equivalents, against $10.6B in long-term debt. That is a decent amount of leverage the company has taken on, which will put off a lot of investors who are more debt-averse. There is nothing wrong with leverage if the management knows how to use it properly and manage it correctly. There are a few ways I like to look at it to see if the debt is going to be too risky and will affect my valuation of the company. Firstly, the company 's Debt-to-Assets ratio has been hovering around the range of 0.4-0.51 over the last 5 years, which is very acceptable. Up to 0.6 I believe is a great ratio, so it looks so far that the debt is not overwhelming.

The company 's Debt-to-Equity ratio has been growing recently because of extra debt on the books, however, anything under 1.5 I consider to be not overleveraged, and in the most recent quarter, that number went down to around 1.2 from 1.4 at the end of FY23, which is a slight improvement. So far, so good. Lastly, to check if the company can pay off its annual debt obligations in terms of interest expenses, I look for an interest coverage ratio of above 5. As of Q2 '24, the company 's interest coverage ratio was at around 7.6x, which means EBIT was able to cover annual interest expense almost 8 times. That is more than safe in my opinion. Furthermore, many analysts consider a 2x ratio to be safe, I just like to be even more conservative.

So, it looks like the debt is not a problem in my opinion, which means the company is at no risk of insolvency any time soon.

{kind=link}

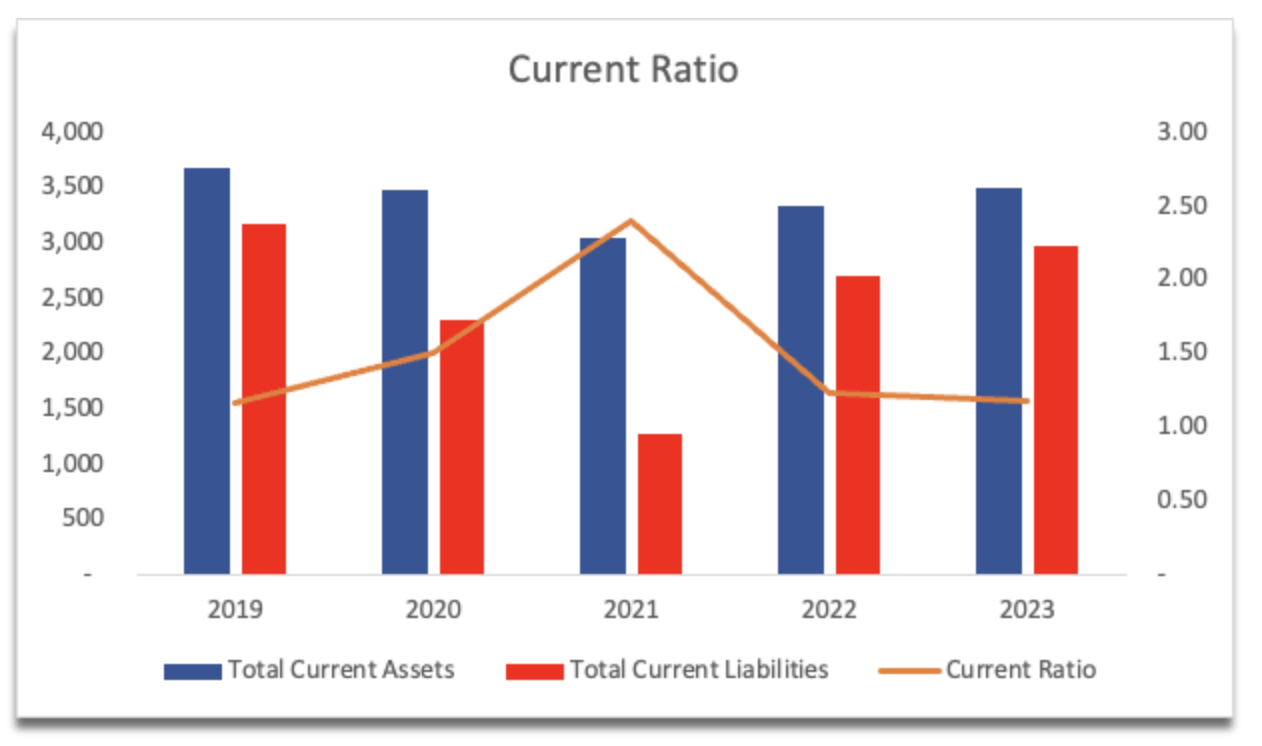

The company 's current ratio has been quite volatile over the last 5 years or so, however, it never dipped under 1, which means the company has no problem paying off its short-term obligations. I would have liked to see at least a 1.5 ratio, but as long as it’s over 1, it 's not an issue. STZ has no liquidity issues.

{kind=link}

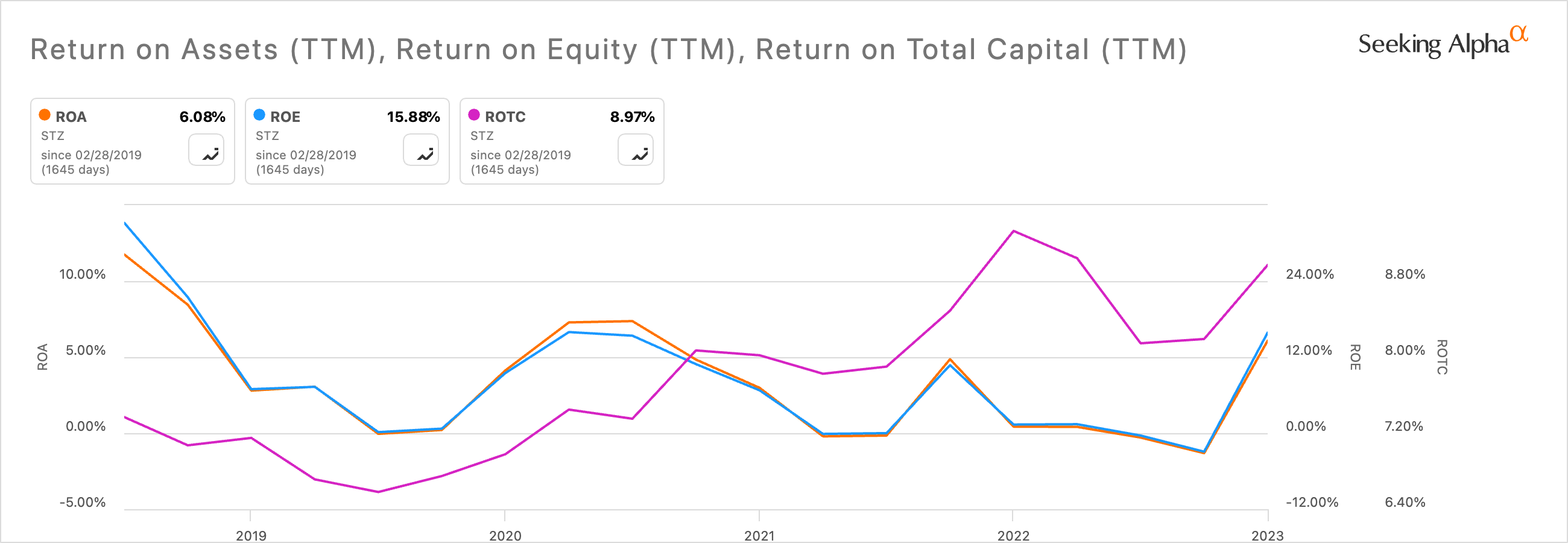

Looking at the company 's efficiency and profitability, recent years have not been the best in terms of performance, however, in the latest quarter, the company has regained its profitability that hasn’t been seen for quite a while, which is a good sign that the management is utilizing company 's assets and shareholder capital efficiently once again. The bottom line has improved dramatically since an year before, which was brought down considerably by a loss from unconsolidated investments of almost $2B.

The same is seen in the company 's ROTC or return on total capital. The company has become more efficient in recent times and is creating shareholder value. The company 's WACC of around 7.4% is lower than its ROIC and ROTC of around 11% and 9%, respectively, which means the company is creating value. Furthermore, what this also tells us is that STZ 's competitive advantage is returning.

{kind=link}

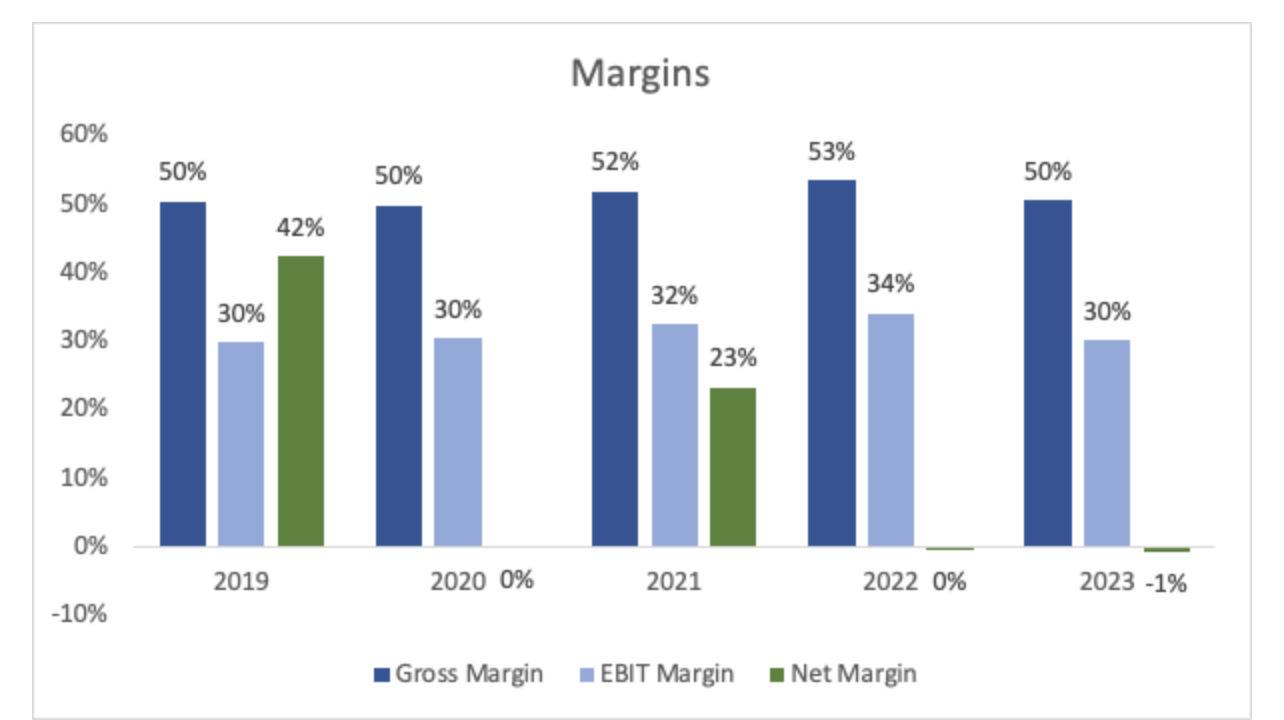

The company 's GAAP margins were affected in recent years by the mentioned losses on investments, mainly from the Canopy cannabis operations, which have not been doing well at all. The ownership has been decreasing, and the company is looking to take on a more passive role when it comes to Canopy operations as the company holds around 21% of outstanding shares as of November down from around 38%, which still means it has a financial interest in it, however, it won 't be affecting the company as much as it did before. So, the margins will improve going forward.

{kind=link}

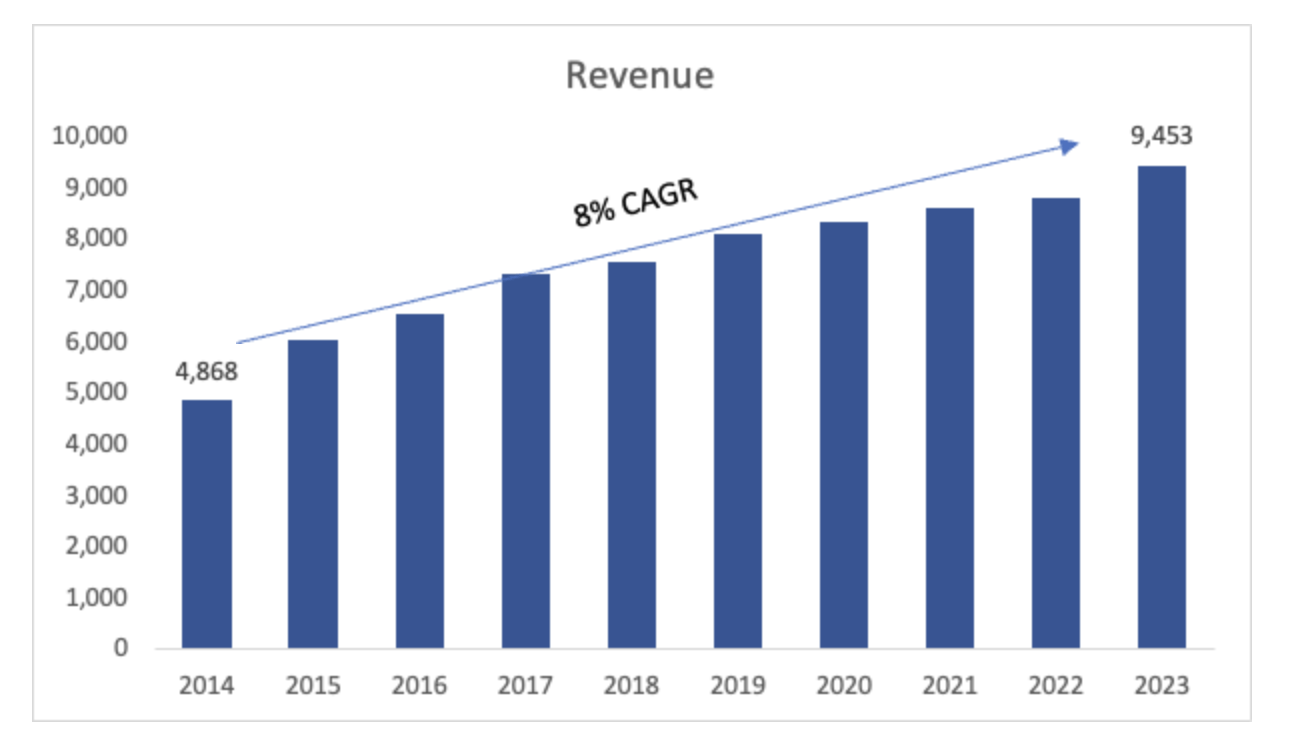

In terms of revenues, the company has been growing very steadily over the last decade with a respectable 8% CAGR. The growth has slowed down slightly due to the Wine and Spirits segments underperforming, while the Beer segment saw 11% growth y/y in Q2 '24. The estimates for FY24 in terms of sales average around 6.5%, which is still good. I will take this number for my valuations too, however, it is impossible to predict the years after, as there could be a lot of uncertainties.

{kind=link}

Overall, I see a company that can handle a bit of leverage quite easily, and if the management can use it smartly, there 's nothing wrong with it. Margins will return and the company will be more profitable in the future as we can already see in the most recent quarter. A lot of the company 's success will depend on top-line growth, which has slowed down a little due to the company 's efforts to reshape its wine and spirits business. This will come with some pains in the short run; however, it will pass, and I don’t doubt we will see revenue increases in the next year or so.

Comments on the Outlook

With the recent dethroning of Bud Light ( BUD ) by Modelo to become the number -one-selling beer in the US , the company 's future looks more promising than ever. This could have been because of all the controversy surrounding Bud; however, it is not to be taken lightly such an achievement by Grupo Modelo to gain widespread popularity in the US. Overall, Budweiser is still one of the tops globally, but this may open some doors to get Modelo and associated beers to more countries of the world, which could be a massive boost to the company 's top line. There is a significant market in Europe that the company should look into, and I’m sure it will through some sort of agreement with AbInBev, distribute beers like Modelo, Pacifico, and others in Europe, however, the European market would be quite difficult to gain a lot of market share due to the many established beer brands.

In terms of the Wine and Spirits segment, I foresee further pain until the company figures out what works and what doesn't. The reshaping of the sector is going to be very positive, however, seeing that the company 's total sales of the segment account for around 20%, it shouldn 't affect the company 's bottom line too much, while the management figures out all the necessary logistics and cost-cutting initiatives. Once they do, the segment will start to contribute positively to the top-line growth once again.

On the Canopy Growth ( CGC ) side of things, I think the company should continue to lower its financial interest in the company and just focus on what is making them money, beer and other alcohol. I don't see potential synergies in entering into such a risky business sector and the continual depreciation in its investment into it just takes away from finding more ways of expanding the market share of its main revenue generators. Maybe I 'm wrong but the cannabis hype train left years ago. There 's probably not much left of the initial investment into the company since it lost 98% of its value in the last 5 years. Let 's just move on.

Valuation

I like to approach valuations with a conservative mindset, to give myself a much higher margin of safety and a better risk/reward outcome in the end. So, for revenue growth, I went with around 7% CAGR over the next decade for the base case scenario, as I believe the company will continue to enjoy an increased market share in the beer segment and will reshape its wine and spirit segment to achieve positive growth. To cover all my bases, I also modeled a conservative and an optimistic case. Below are those assumptions.

{kind=link}

For margins and EPS, I decided to include the company 's horrible investment in Canopy decreased its EPS by around $2 a share, and went with around the guidance the company provided for FY24 . This way I’m getting even more downside protection in terms of a larger margin of safety. Below are those assumptions.

{kind=link}

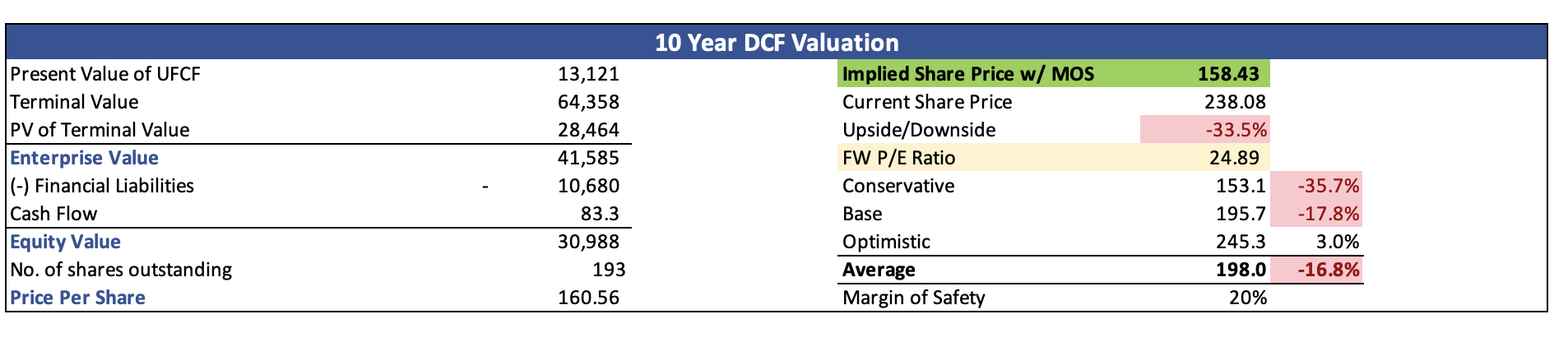

On top of these estimates, I decided to use 8.5% as my discount rate instead of the company 's WACC of around 7.4%, just to give myself even more room for error. Furthermore, I decided to add another 20% MoS to the intrinsic value just so I could get a good night 's sleep knowing that I didn't overpay for the company if I did buy it. With that said, STZ 's intrinsic value, and what I would be willing to pay for it is around $158 a share, which means the company is very expensive right now and is not a good time to commit some capital.

{kind=link}

Closing Comments

The valuation may seem a little harsh, but things happen, and companies do sometimes reverse heavily, and my conservative PTs are breached. Nevertheless, the company is a strong contender for a long-term hold, but only if it comes down in price considerably, or if the company 's EPS improves significantly over the next while, which can happen.

I would like to see the company continue to pay down its debt pile and maintain or increase market share in the beer segment going forward. The wine and spirits segment will return to growth in the future; however, it is hard to tell when, but when it does, it will play a decent role in the company 's bottom line. Nevertheless, the company is slightly too expensive for me right now, so I will set a price alert at around $180 and see how it develops over the next while. I will tune in to the company 's earnings calls to see how the segments are developing.

For further details see:

Constellation Brands: Too Expensive Right Now, Waiting For A Pullback