STZ - Constellation Brands: Too Hefty Of A Price

2023-09-05 09:09:39 ET

Summary

- Constellation Brands has a history of stable growth and high margins, that seems to be continuing into at least the current year, despite a challenging macroeconomic climate.

- The company owns popular brands such as Modelo Especial and Corona Extra, with a large focus on been brands.

- Although a good company, Constellation Brands' current valuation is concerning; my DCF model estimates a significant downside for the stock.

Constellation Brands (STZ) produces and sells alcoholic drinks in locations such as the United States, Canada, and Mexico. Although the company has a history of stable growth and high margins, I have a sell-rating for the stock as the market already seems to price in these factors in a too big manner.

The Company

Constellation Brands owns brands such as Modelo Especial, Fresca, Corona Extra, Pacifico, Casa Noble, as well as multiple other brands producing wine and spirits:

Constellation's Brands (globalbrandcenter.cbrands.com)

The company's stock has seen a good increase on the stock market, as Constellation Brands has had a CAGR of 16.2% in the past ten years:

{kind=link}

On top of the price increase, investors have received a small dividend yield from 2015 forward ; although not a very significant amount, I believe the estimated forward yield of 1.37% should be mentioned.

The company's at an interesting point, as Elliott Investment Manager has pushed for seats in the company's governance - although the capital manager's favored direction for the company is not clear, the move could push for a more favorable direction for the company concerning investors.

Financials

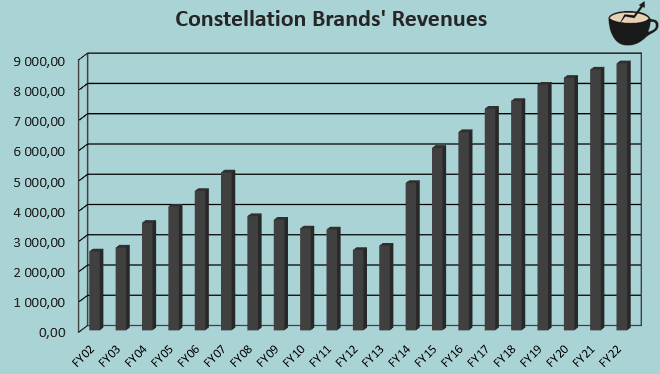

The company has had a very good history of growth, as from FY02 to FY22 the company's compounded annual growth has been 6.3%, well above the industry as a whole:

{kind=link}

As seen in the chart, the growth was disrupted by decreasing revenues from FY08 to FY12 - as I believe, the decreases were largely due to the company's divestures during the period - from FY07 to FY11, the company had almost a billion dollars in divestures. After the decreases, the company has been able to grow its revenues very well - although the growth is partly caused by large acquisitions in FY14, FY16 and FY17, the company has been able to keep up a good rate of growth even without significant acquisitions.

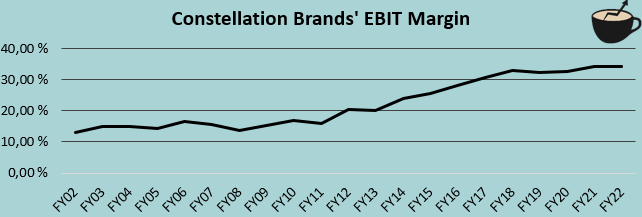

The rising revenues are coupled with a very good cost control - Constellation Brands has been able to grow its EBIT margin from FY02's 13.1% to a margin of 30.8% in FY23 with stable increases:

{kind=link}

Although the margin has increased very significantly in the past twenty years, I don't believe the margin can go a lot further - the current margin is already above the global beverage leader Coca-Cola's margin ; as Constellation owns leading brands in many categories, they should already have realized most benefits of scale.

Constellation Brands leverages debt, as the company has around $11.5 billion in long-term debt as well as $819 million in short-term borrowings. Of the long-term debt, $549 million is in current portions - the company has almost $1.4 billion in short-term interest-bearing debts. As the company is expected to bring in free cash flows of $1.3 billion in the current fiscal year, I don't believe that the debts pose too much of a threat for the company. The company does also have cash reserves of $193 million.

Valuation

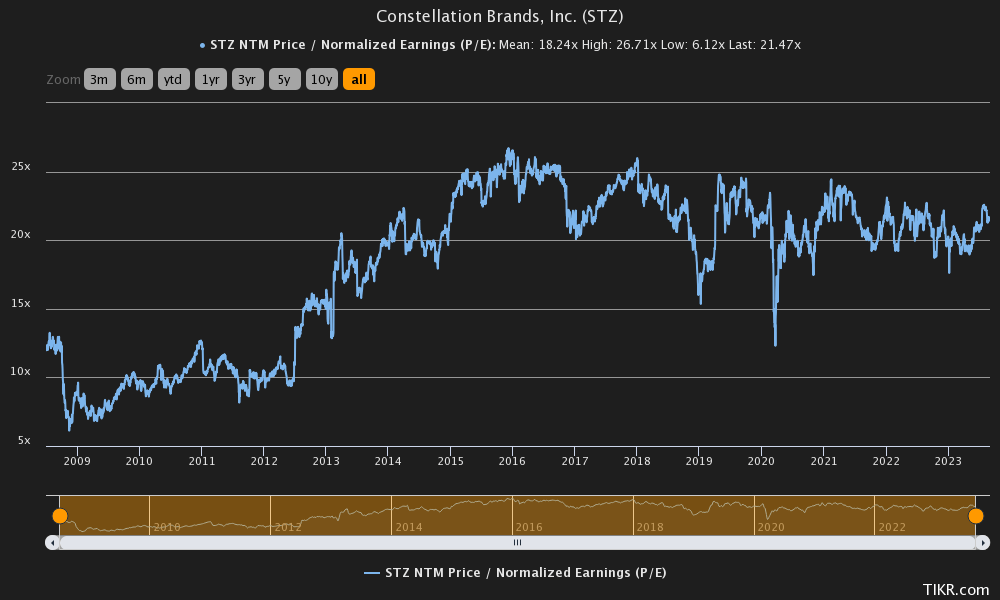

Currently, Constellation Brands trades at a forward price-to-earnings ratio of 21.5 - the rate is above the stock's mean figure of 18.2:

{kind=link}

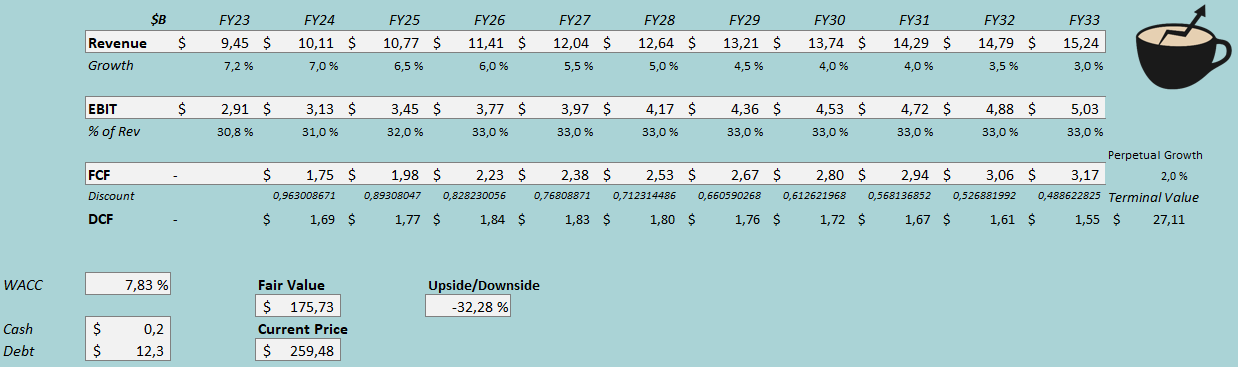

The ratio being above Constellation's mean is a bit concerning, as interest rates have gone higher and as I believe that the company's further operating leverage potential is significantly lower than in its history. To further contextualize the valuation, I constructed a discounted cash flow model. In the model, I estimate Constellation to hit its current year's revenue guidance. Going forward from FY24, I expect the company's growth to slow down in small steps into a perpetual growth rate of 2%.

For Constellation's margin, I expect the company to keep its margin quite stable going forward - in the DCF model, I have an EBIT margin of 31% for FY24, which further rises into 32% in FY25 and into 33% in FY26 and forward. Converting the company's earnings into free cash flow, the company's capital expenditures seem to exceed depreciation and amortization by a moderate amount, which I consider in the model.

These expectations along with a cost of capital of 7.83% put the stock's estimated fair value at $175.73, around 32% below the current price:

{kind=link}

The used cost of capital is derived from a capital asset pricing model:

CAPM of Constellation (Author's Calculation)

Constellation had interest expenses of $118 million in Q1 of FY24 - annualized, this makes the company's interest rate 3.83% with the current amount of interest-bearing debt. The company seems to leverage debt quite well to its advantage - I believe Constellation Brands' long-term debt-to-equity ratio will be around 25%.

On the cost of equity side, I use the United States' 10-year bond yield of 4.17% as the risk-free rate. For the equity risk premium, I use Professor Aswath Damodaran's estimate of 5.91% for the United States. Tikr estimates the company's beta to be 1.03 - I believe that the estimate is too high, as alcoholic drink manufacturers are historically very stable throughout different economic states. In fact, so has Constellation Brands - the company kept a mostly stable margin throughout the 2008 financial crisis and seems to perform up to the company's standards in the current economic climate.

As I believe that Tikr's beta estimate is too high for Constellation Brands, I instead use an average of other alcoholic companies' betas - Tikr estimates Diageo's beta at 0.38, Heineken's beta at 0.64, Carlsberg's beta at 0.60, and Ambev's beta at 0.62. Taking an average of these figures, the beta becomes 0.56, which is much fairer for Constellation Brands in my opinion - although this method varies from my usual, I believe it's more accurate.

Finally, I add a liquidity premium of 0.5% and an ESG-addon of 1.5% into the cost of equity to address the factors. With these assumptions, the cost of equity ends up at 9.48% and the WACC at 7.83%, used in the DCF model.

Takeaway

Although a fantastic company with a likely stable future, I believe Constellation Brands is currently priced too steeply. With the DCF model estimating a downside of 32% with assumptions that I see as reasonable, I have a sell-rating for the stock.

For further details see:

Constellation Brands: Too Hefty Of A Price