CA - Constellation Software: A Buffet-Like Compounder

2023-08-08 23:02:49 ET

Summary

- Constellation Software is a great compounder and has a similar business model as Berkshire Hathaway or Markel.

- Due to its reputation, the high switching costs and operating in a niche, Constellation Software has a wide economic moat around its business.

- Although the company is trading for rather high valuation multiples, the stock might be undervalued at this point.

- However, we should be careful as setbacks and larger declines during a potential recession are possible, and Constellation Software is facing the risk of growth rates declining over time.

(Note: If not otherwise specified, amounts are in U.S. dollar as the business is also reporting in USD despite being a Canadian business)

In the past, when I have written about Canadian businesses it was usually about the “Big Five” Canadian banks. And without much doubt, Canadian banks are great businesses – especially compared to banks in many other countries – but Canada also has to offer other great businesses worth looking at.

In the following article, I will cover Constellation Software Inc. ( CNSWF ) for the first time. The software company is among the top 20 companies in Canada (by market capitalization) and is often seen as one of the great capital allocators and often compared to businesses like Markel Group Inc. ( MKL ) or Berkshire Hathaway Inc. ( BRK.A ) ( BRK.B ). And although these businesses are operating in very different sectors and market segments – Berkshire for example has little exposure to software companies or technology businesses – the investing philosophy is very similar. And that’s making Constellation Software interesting as an investment.

Company Description

Constellation Software is a Canadian diversified software company that was founded in 1995 by Mark Leonard – a former venture capitalist – and has the headquarter in Toronto, Canada. In the following years, the company began to assemble a portfolio of vertical market software companies and is now operating mostly in Canada, the United States, the United Kingdom, and several other European countries. In 2006, the company had its initial public offering and continued to grow to over 25,000 employees.

In fiscal 2022, the company generated $6,622 million in revenue and compared to $5,106 million in the previous year, the business could grow its top line 29.7% year-over-year. Income before income taxes could almost double from $374 million in fiscal 2021 to $725 million in fiscal 2022 (94% year-over-year growth). And diluted net income per share increased 65.1% year-over-year from $14.65 in fiscal 2021 to $24.18 in fiscal 2022. While Constellation Software could report high growth rates in its income statement, free cash flow available to shareholders declined slightly from $883 million in fiscal 2021 to $853 million in fiscal 2023 – resulting in 3.4% year-over-year decline.

In total, Constellation Software is owning over 600 different businesses, which can be split up in six operating segments: Volaris, Harris, Topicus, Vela, Jonas and Perseus.

Constellation Software Investor Relations

{kind=link}

Aside from splitting up the business in six different segments by the sector these are operating in, we can also look at four different sources of revenue. The biggest part of revenue ($4,688 million in fiscal 2022) was generated by “Maintenance and other recurring” followed by revenue from “Professional Services”, which was $1,381 million in fiscal 2022. “Hardware and other” ($233 million in fiscal 2022) and “Licenses” ($320 million in fiscal 2022) contributed only a small part to overall revenue.

Wide Economic Moat

When analyzing a new business, an important aspect I always pay attention to is the wide economic moat every long-term investment should have.

To find out if a company has a wide economic moat, we can start by looking at several metrics that usually indicate a competitive advantage that leads to outperformance. A first hint can be the outperformance of a stock over a very long timeframe. Constellation Software had its IPO in 2006 and although 17 years might not be long enough, the outperformance during that time was impressive. While the S&P 500 ( SPY ) gained “only” 248% during that timeframe, the return of Constellation Software was 14,640%.

But we all know that stocks can be severely over- or undervalued and this is disturbing the picture. And as we will see, Constellation Software is trading for a rather high valuation multiple that might have contributed to the outperformance. Hence, we should also look at fundamental numbers. A good starting point are the margins of a company – and while we are also searching for businesses with high margins (as high margins are always good), it is especially consistency we should pay attention to. A high-quality business with a wide economic moat around the business should be able to report stable margins (or improving margins) over time.

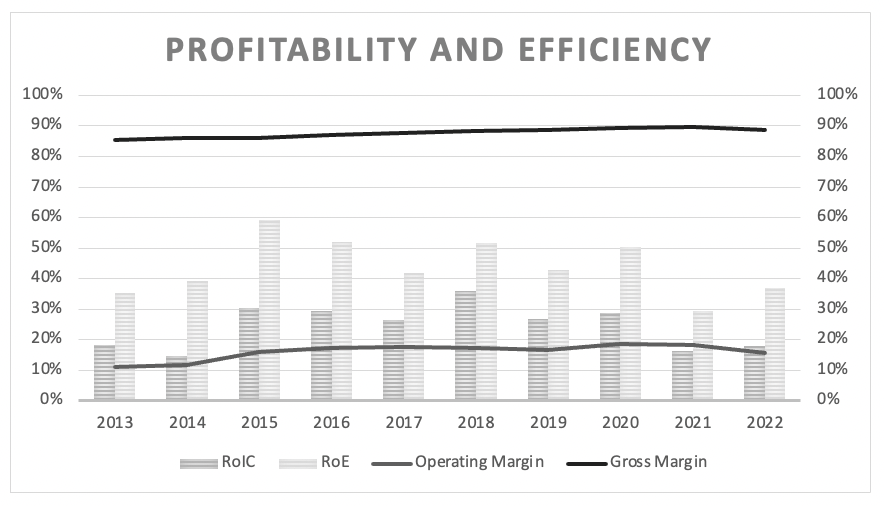

Constellation Software: Margins and return on invested capital (Author's work)

{kind=link}

And although operating margins declined a bit in 2022, Constellation Software could report an increasing operating margin during the last ten years and gross margin is stable at a very high level – this is a strong indication for pricing power. Aside from margins we especially pay attention to return on invested capital as a strong hint for a wide economic moat. In the last ten years, the company could report an average RoIC of 24.54%, which is an impressive number.

Switching Costs and Niche

Not only numbers are indicating a wide economic moat – we should also be able to identify a clear source for an economic moat. And when looking at the different sources of an economic moat, Constellation Software is operating in a niche and the customers are usually facing high switching costs.

The vertical market software is often mission-critical for the customers and the software solutions are designed to meet the specific needs of the customers. Additionally, the costs for the software account only for a fraction of a company’s overall costs. These are perfect conditions for high switching costs: A company can save only a few bucks by switching to a cheaper competitor but is facing high risks when switching as the competitor’s products might not meet the specific needs and during the switching process a lot can go wrong. This is making the incentives to switch to a competitor very small and enabling Constellation Software to raise prices without losing customers.

And Constellation Software (or the different companies operating under the holding company) is usually serving small niche markets with small addressable markets. This is making the markets unattractive for competitors and is keeping the major corporations away. Often the costs to develop the software are rather high and with a small addressable total market these high upfront costs are a huge disincentive – especially when having to compete with an established competitor like Constellation Software. Hence, Constellation Software (or its subsidiaries) are the only player or one of very few players in a niche market giving the company pricing power again.

Reputation

Additionally, the reputation (or the brand name) of Constellation Software is also important. Usually, brand names are rather important for businesses that sell to end consumers. But in case of Constellation Software, the brand name and reputation are important for a different reason. The company’s reputation as leading vertical market software acquirer is important and is most likely leading to Constellation Software being able to make better deals. The deals could be better as Constellation Software might be able to acquire high-quality companies with a better business model – and it might also be able to acquire them for a cheaper price. And Constellation Software is often acquiring family-businesses or small businesses run by the owner and they might appreciate the management style of Constellation Software more than getting the highest amount possible for the business.

It is also important to point out, that Constellation Software is never selling a business. It is often reported that Mark Leonard once sold a business in the early days of Constellation Software, and he is still regretting it. And for family-run businesses it is also important not to be sold to a different owner every few years or being optimized for a high selling price by drastic cost reduction strategies.

Mark Leonard is following a similar strategy as Warren Buffett and Charlie Munger: acquired businesses will remain as independent as possible. And we must assume that most founders and leaders appreciate being able to remain in control of their own business. Constellation Software writes on its homepage:

CSI will not take over the day-to-day management of its businesses. We continue to rely on the managers and employees of our subsidiaries to run their businesses well. Managers who are excited at the prospect of creating an Exceptional company and who are willing to embrace new ideas tend to flourish at CSI.

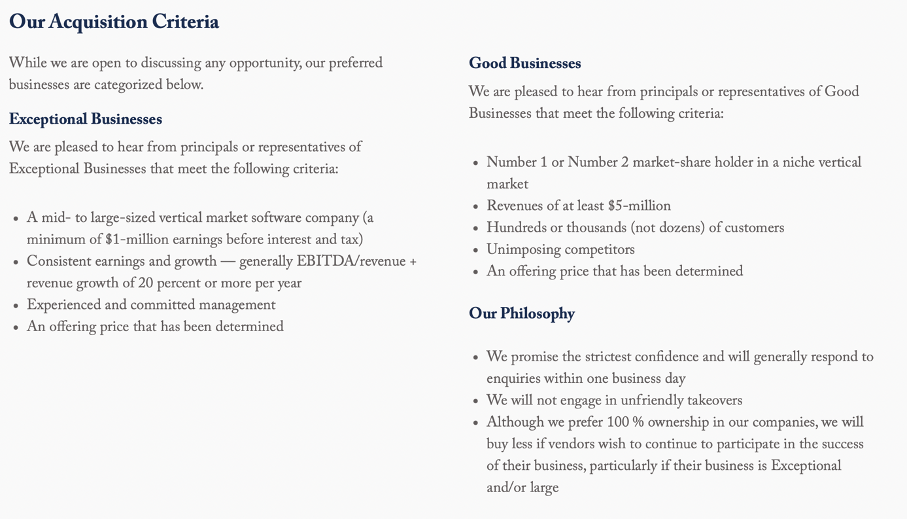

On the homepage we also find the acquisition criteria the company has for good or exceptional businesses.

Constellation Software Investor Relations

{kind=link}

And as long as we are talking about positive aspects of the business, we can also mention that Mark asked the board of directors about 10 years ago to reduce his salary to zero. Therefore, the CEO has high incentives for the business to performance great over the long term.

Summing up, Constellation Software has a great setting and structures put in place to outperform over a long period – and past numbers are proof for an exceptional business model.

Recession

Aside from a wide economic moat around a business, the performance during a recession is also important – not only because I still see a recession on the horizon. In case of Constellation Software, we have data since 2006 and can look at two different recessions – the Great Financial Crisis and the recession in 2020 during the COVID-19 crisis.

And although the data from only two recessions is not enough for solid conclusions, we have hints that Constellation Software will perform quite well during recessions. For earnings per share, we see some fluctuations during the years – but we do not necessarily see a correlation between recessions and declining earnings per share. And when looking at revenue, we never saw a decline since 2006. I don’t want to call Constellation Software recession-proof, but we can be confident the business will perform quite well during the next recession.

It is also worth pointing out that the stock never declined more than 26% since 2006.

Intrinsic Value Calculation

So far, we can summarize that Constellation Software is a great business that did not only perform well during the last two recessions but also seems to have a wide economic moat around the business. And in the past, the company could report high growth rates with high levels of consistency and therefore is it not surprising that the stock is trading for rather high valuation multiples.

In the last ten years, Constellation Software was trading for an average P/E ratio of 63 and right now, the stock is trading for 83.6 times earnings. It doesn’t really matter how great a business is and what growth rates it can report – a high double digit valuation multiple is seldom justified.

Instead of the P/E ratio, we can also look at the price-free-cash-flow ratio, which can often be seen as the better and more accurate metric. In case of Constellation Software, it is also painting a different picture: Not only was the average P/FCF ratio 24.82 in the last ten years, right now, Constellation Software is trading “only” for 30.6 times free cash flow.

At this point, we can make the argument that Constellation Software is neither cheap nor expensive and to determine an intrinsic value (and come closer to a decision if the stock can be purchased at this price) we use a discount cash flow calculation. As always, we are calculating with a 10% discount rate and the company has 21.2 million outstanding shares. When using the reported free cash flow available to shareholders from fiscal 2022 (which was $853 million), the business must grow 16% annually for the next ten years followed by 6% growth till perpetuity to be fairly valued right now.

When looking at the growth rates in the past, Constellation Software could grow revenue 22.21% during the last ten years, operating income even with a CAGR of 25.40% and earnings per share grew 18.66% annually. From this point of view, 16% growth annually for the next ten years seem reasonable and achievable (in theory) but Constellation Software is not a bargain and not cheap.

Of course, Constellation Software has a track record of growing with a high pace for a long time and one could bet on Constellation Software growing in the double digits in 10, 15 or 20 years from now. But as I have mentioned several times in the past, it is impossible to know what will happen in 5 years, 10 years, or 20 years from now. And making extremely optimistic assumptions is leading to a high risk of overpaying. One can also make an argument for the reversion to the mean and it could get more and more difficult for Constellation Brands to keep up the high performance over decades to come.

On the other hand, we can also make the argument that we can take a free cash flow of $1,388 million as basis in our calculation. We get this number when using the cash from operating activities of the last four quarters and subtract capital expenditures. When using this amount, the business must grow only 9% annually in the next ten years followed by 6% growth till perpetuity to be fairly valued right now. And this is painting a very different picture of the business and 9% growth for the next ten years definitely seem achievable and we can make the argument for Constellation Software being undervalued.

Conclusion

Without much doubt, Constellation Software is a great business, and we can also make the case for the stock being undervalued at this point. The argument is often made that Constellation Software is a similar business as Berkshire Hathaway but at a much earlier stage – buying Constellation Software today could therefore be like buying Berkshire Hathaway in the 1980s and when seeing Constellation Software as a long-term investment, potential setbacks in the next few years can be ignored. Only if Constellation Software would not be able to report at least high-single digit growth rates anymore, an investment might be a mistake.

For further details see:

Constellation Software: A Buffet-Like Compounder