CA - Constellation Software: Is Bigger Better?

2023-10-26 10:00:00 ET

Summary

- Constellation Software has been a long-term market outperformer.

- The big question is the scalability of its acquisition model.

- Recent carve-outs from Black Knight indicate that the model is evolving, but keeps on working.

- Constellation looks to be reasonably priced at these levels.

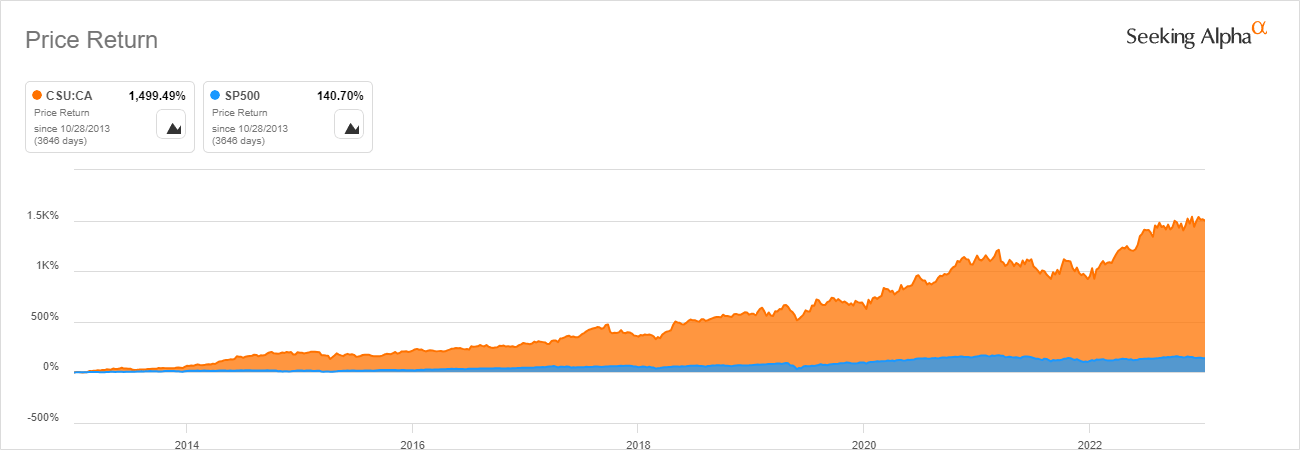

Constellation Software ([[CNSWF]], [[CSU:CA]]) has become one of the largest Canadian corporations after decades of steady high growth by acquisition. It outperformed the S&P 500 by 10x since 2013. I detailed my investment thesis for Constellation Software in an article early last year. I'll check back on the company in this article and see how it developed.

Throughout this article, I often refer to Constellation Software Inc. as CSI.

{kind=link}

Recap: Business model

CSI primarily grows through acquisitions: The 10-year revenue CAGR is at 21.88%, even though organic growth is in the low single digits. Over the same period, EBITDA grew by 23.44%, operating profit by 26.27%, and free cash flow by 25.25%.

To achieve these numbers, CSI is a serial acquirer of small Vertical Market Software companies. These companies are focused on small niches without much competition. This makes the business sticky and allows for predictable and relatively safe cash flows; reinvestment needs are limited and allow for high margins. Many of these companies operate in markets with just a few million dollars in size.

The big question mark behind the sustainability of this model is the scalability. To achieve this, CSI has a decentralized model with many subsidiaries deploying the capital generated by the operating companies. The company has tens of thousands of targets in its database and has been in contact with many targets for a decade, so if they eventually want to sell, they know who to contact.

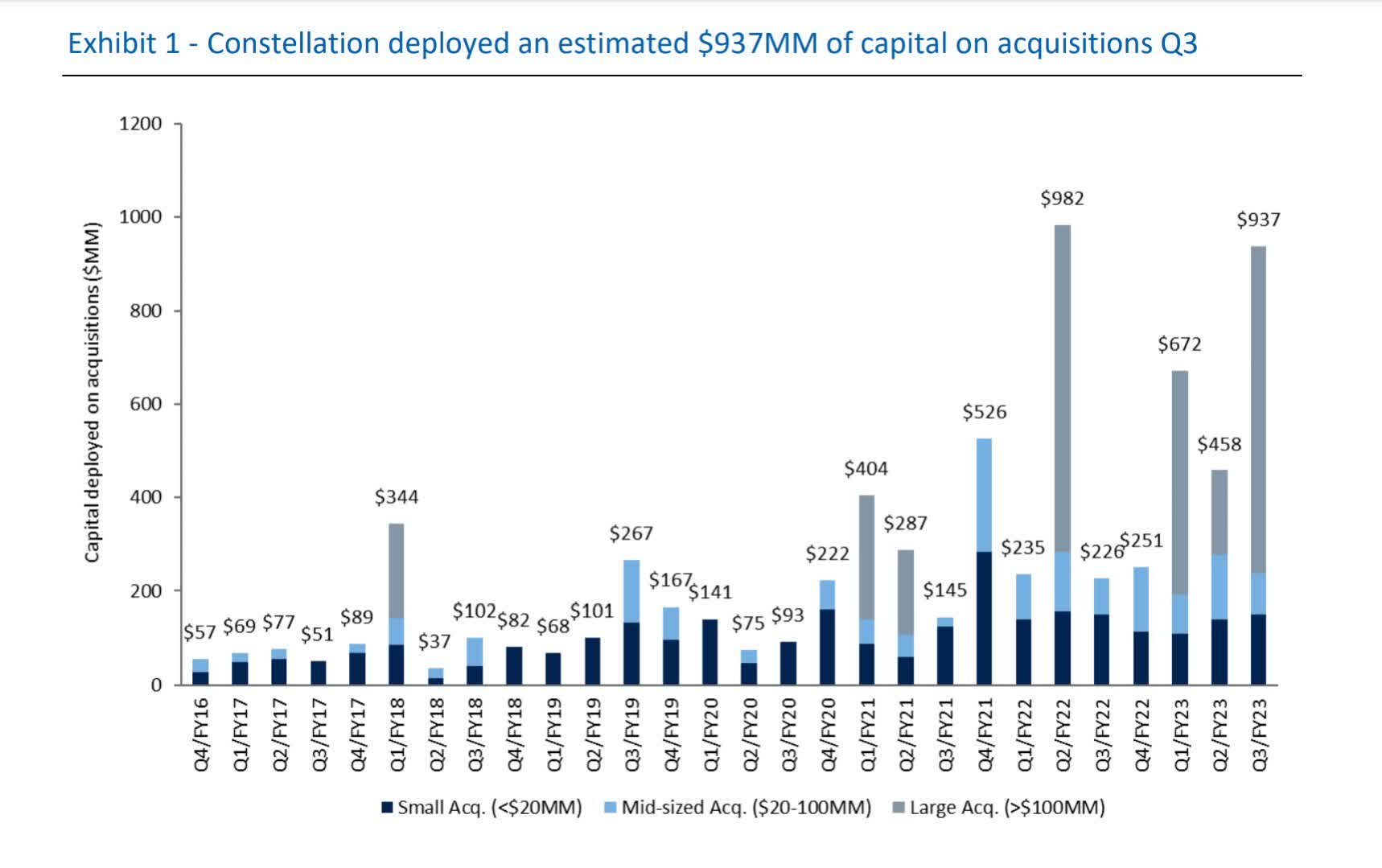

Bigger Deals

In my prior article, I highlighted that bigger deals could be a way for CSI to continue deploying 100% or more of its cash flow into acquisitions. This is integral to the investment case; lots of capital has to be deployed at high rates of return to continue compounding. CSI has a stringent rule to stick to its high hurdle rate in making deals: If the projected return isn't good enough, the deal will fall through. Bigger deals, on the other hand, offer an opportunity to deploy much more capital, but potentially at a lower hurdle rate. Shortly before my prior article, CSI did its most significant acquisition at that point, acquiring assets from Allscripts Healthcare Solutions for $700 million. Since then, CSI has managed to do two more large carve-outs, which I already covered in my Intercontinental Exchange (ICE) article . Last year, ICE announced a merger with Black Knight (BKI) to create a complete life-of-the-loan platform at a $16 billion valuation. After regulators scrutinized the deal, ICE agreed to sell off two of Black Knight's crown jewel assets, in my opinion, a vital part of the whole life-of-the-loan plan, to Constellation Software:

- Empower (together with Black Knight's Exchange, LendingSpace, and AIVA solutions) is estimated to generate $75 million adjusted EBITDA. The purchase price isn't confirmed, but there are estimates of around $190 million , under three times AEBITDA.

- Black Knight recently acquired Optimal Blue in early 2022 at a $3 billion valuation. CSI now paid $700 million, consisting of $200 million cash and $500 million in a 40-year promissory note at 7% interest to Black Knight.

Both of these carve-outs look to be exceptional deals and show that CSI is a good address for companies to carve out deals. These carve-outs are especially interesting because, often, they are the result of a large merger, where smaller segments need to be spun off to get the big deal done. The incentive, most of the time, lies on the big deal, allowing for excellent conditions on the small carve-outs. Speed and flexibility are key components to secure these deals and CSI is ready to make any deal work as long as the hurdle rate is met and the assets are good.

In the chart below, we can see that CSI managed to scale capital deployment well and I believe that these carve-out deals won't be the last either.

{kind=link}

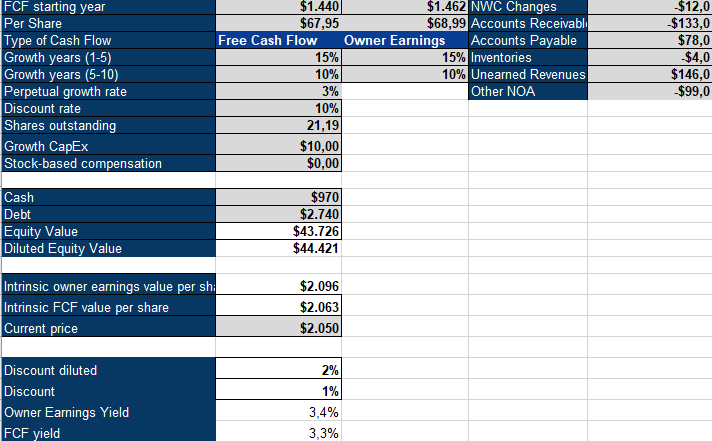

CSI looks cheap

To value CSI, I'll use an inverse DCF Model. The model here is pretty uncomplicated, as there aren't any stock-based compensation, minimal capital expenditures, and net working capital changes present. Based on current cash flows, CSI would need to grow at 15% for the next five years, followed by five years at 10% growth. This is significantly below the historical revenue and profit growth of the company. I believe that CSI will continue close to its historical growth rate, as the scalability of the acquisition model seems to work, as the two ICE carve-outs would indicate. This is a new opportunity for CSI and makes me feel confident in owning shares.

{kind=link}

For further details see:

Constellation Software: Is Bigger Better?