CA - Constellation Software Q1: The Wings Of Its Dual Growth

2023-05-23 15:50:28 ET

Summary

- Constellation Software Inc. reported a great Q1 2023.

- Highlights could be found in organic growth and capital deployed, the company's double growth engine.

- The new focus on organic growth eases the fears caused by Constellation's main bear arguments. We discuss how.

- The Altera acquisition is performing well, showing a promising future for Constellation Software's larger capital deployment efforts.

- Large acquisitions bring lower hurdle rates, but a higher probability of meeting or surpassing them.

Introduction

Constellation Software Inc. ( CSU:CA , CNSWF ) reported its Q1 earnings last week. The results were very strong, with positive signs on the organic growth front and related to Altera, the company's largest acquisition to date.

We have seen a lot of discussion regarding Constellation lately. The company has always had skeptics who typically end up in the "it's too good to be true" argument. This is not unexpected for a company that has achieved a 36% compounded annual growth rate since going public in 2006. That adds up to a total return of almost +16,000%. On top of that, Constellation Software stock is close to its all-time highs again.

Performance has indeed been great, but it was great news to see management retain the usual humility during the company's latest Annual General Meeting. Constellation's management team is constantly learning and thinking forward, which is essential to mitigate the most significant risk for any successful company: complacency.

Without further ado, let's dig directly into the numbers.

The numbers

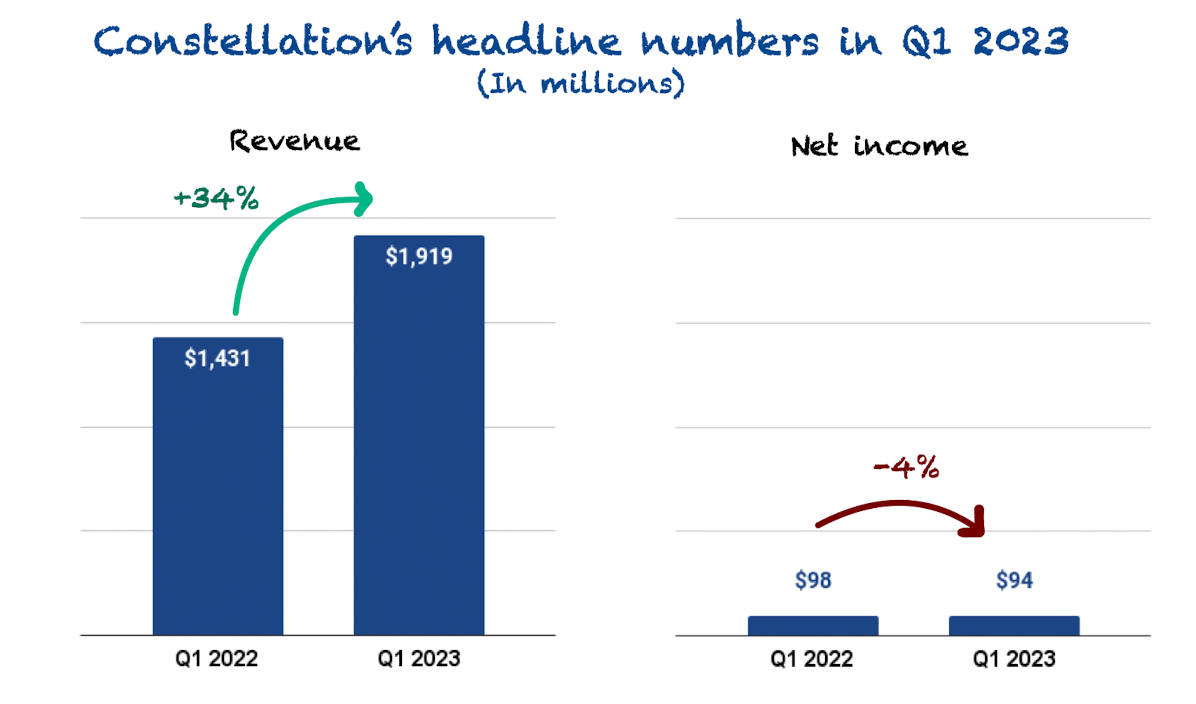

Constellation reported great numbers in Q1. Revenue grew 34% year-over-year to $1.9 billion. Net income attributable to CSI shareholders decreased 4% to $94 million:

{kind=link}

For yet another quarter, Altera, the company's largest acquisition to date, played a significant role in the company's growth rate. Revenue growth would've been 20% excluding its impact, which is still high but not 34%. Note, though, that Constellation Software is in the business of deploying capital into acquisitions, so it's somewhat strange to exclude an acquisition from the numbers.

We think it's important to understand how Altera might impact the numbers. Constellation closed the acquisition of Altera from Allscripts in Q2 last year, so Q3 will bring us a more apples-to-apples comparison. Altera's revenue has declined year-over-year in every quarter since Constellation acquired it; before the acquisition, too, if you were wondering. That's why we might start to see Altera contribute negatively to revenue growth starting next quarter. The landscape in cash flows is a different story, and cash is king for Constellation. More on this later in this article.

Digging deeper into revenue

Constellation has two sources of revenue growth: acquisitions and organic growth . As in almost all quarters, acquisitions were responsible for most of the growth again, but organic growth continued to show some very positive signs.

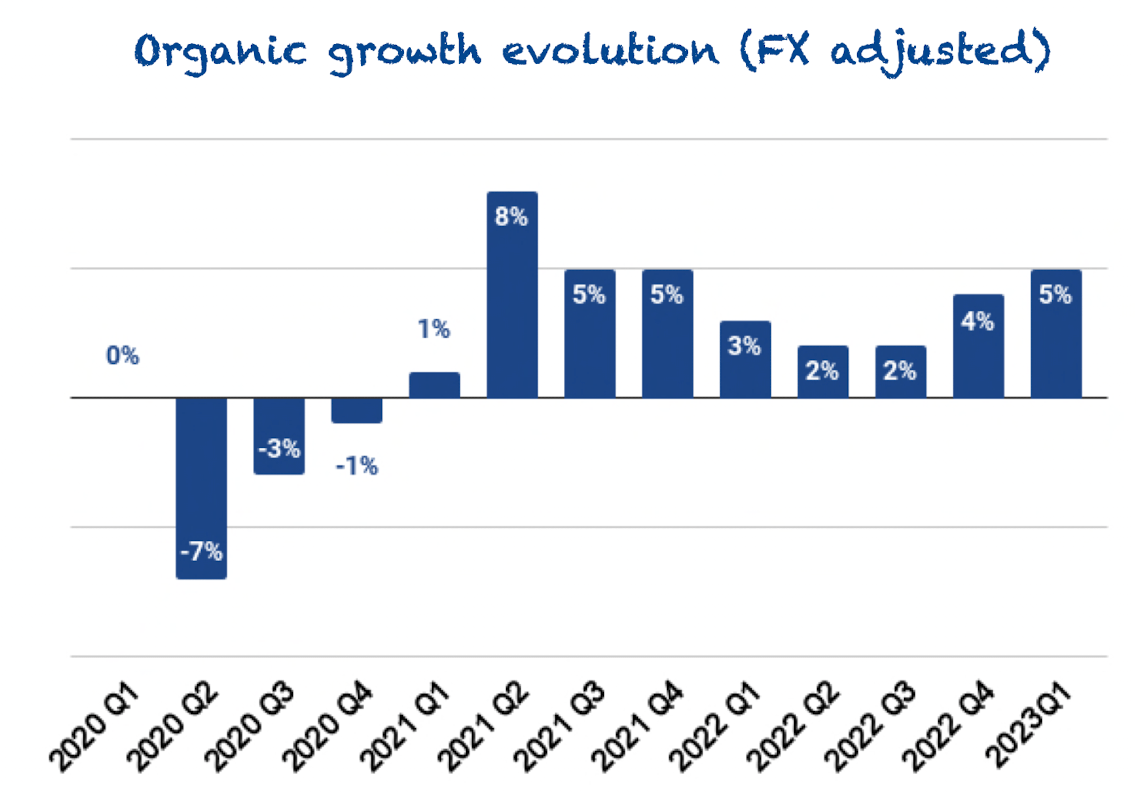

Organic growth was impacted by currency exchange rates. Adjusted for these impacts, revenue grew organically by 5% year-over-year . This was the highest organic revenue growth the company has posted since 2021 . That's extra impressive if you know that the 2021 numbers faced easy comps due to the pandemic period:

{kind=link}

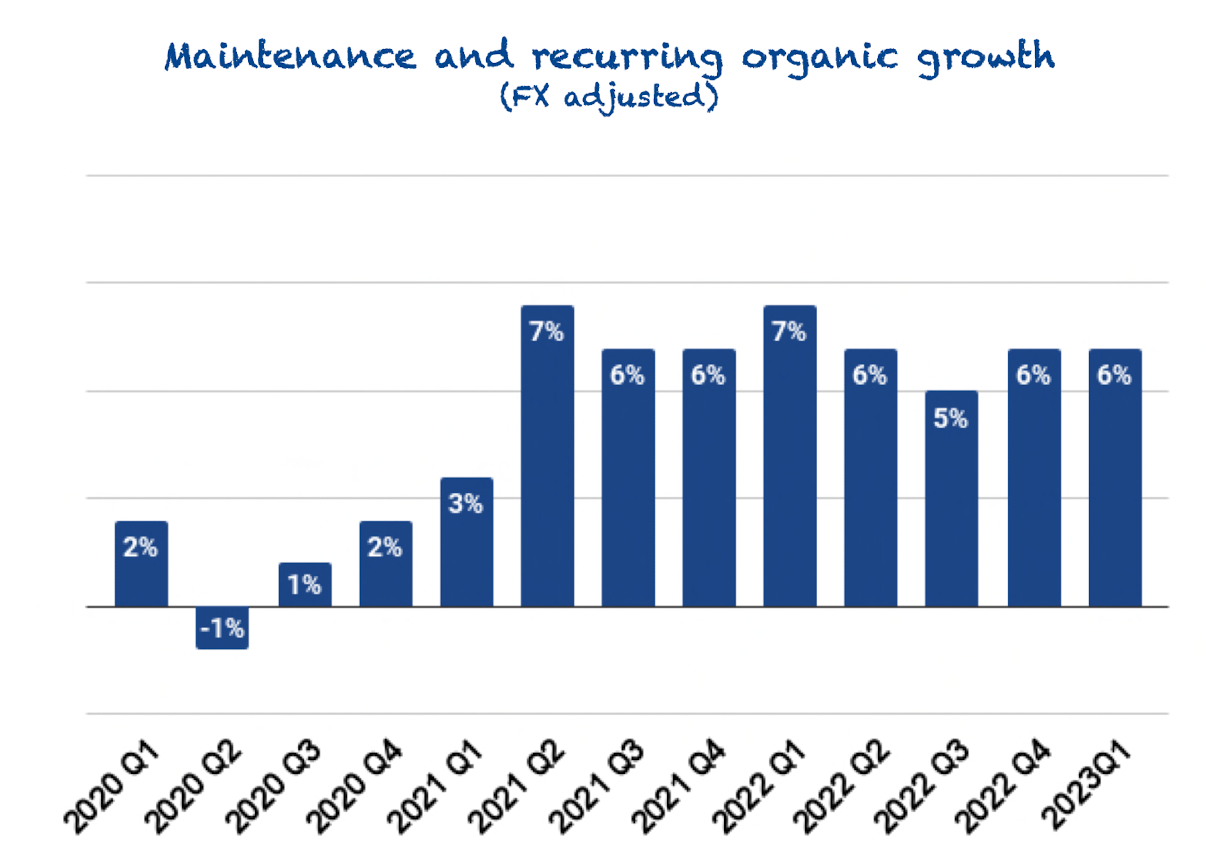

Management has openly discussed efforts to improve organic growth. While these are not evident entirely in overall organic growth, they seem to be surfacing in maintenance and other recurring revenue organic growth. This was the bright spot again of the release, with maintenance and other recurring organic revenue growth steady at 6% . 2021 seemed like the consequence of "easy" comps due to a weak 2020, but the strength is persisting, and Constellation seems to now have a better hold of this metric:

{kind=link}

Organic growth is not the central aspect of Constellation's investment thesis. However, it's a nice upside to the base case, mainly because it mitigates the main bear case: Constellation running out of runway to deploy capital.

Historically, Constellation had deployed most of its capital into acquisitions, so inorganic initiatives generate most of its growth. This meant a runway of prospective acquisitions was necessary to keep the flywheel going. I don't anticipate this to be any different in the foreseeable future.

However, if the focus on organic growth is successful, Constellation will have two growth engines , inorganic and organic, and two capital deployment targets acquisitions and business development. This eventually means that the company would not only rely on a large runway of companies to acquire to generate growth. And don't get us wrong, we think the runway for acquisitions is still long because the pipeline is large; it's just that good organic growth can relieve the pressure on M&A, which becomes arguably more challenging as the company scales.

Three large companies impacted Constellation's organic growth: Altera, Topicus , and Lumine . There was little surprise this quarter directionally. Altera (-9% year-over-year) and Lumine (+1% year-over-year) were headwinds to the company's organic growth rate, whereas Topicus (+8% year-over-year) was a tailwind.

Needless to say here that the investment thesis behind Altera is not high organic growth ; it's better cash conversion and stabilizing this growth. On the other hand, the thesis behind Topicus is indeed faster-than-company-average organic growth , so there was not much of a surprise in these numbers. As per Lumine, it's still a bit early to understand how organic growth can trend there, especially since there's a bit of noise in the numbers. This said, Constellation reports 100% of Lumine as non-controlling interest ("NCI"), so it's not really that relevant for the bottom line.

All in all, Constellation's top line growth was great for yet another quarter. Altera might soon impact the company's top line numbers negatively. However, growth might still be good considering the amounts Constellation is deploying into M&A and the good news in organic growth.

Looking at the expense side - More noise from a new spinout

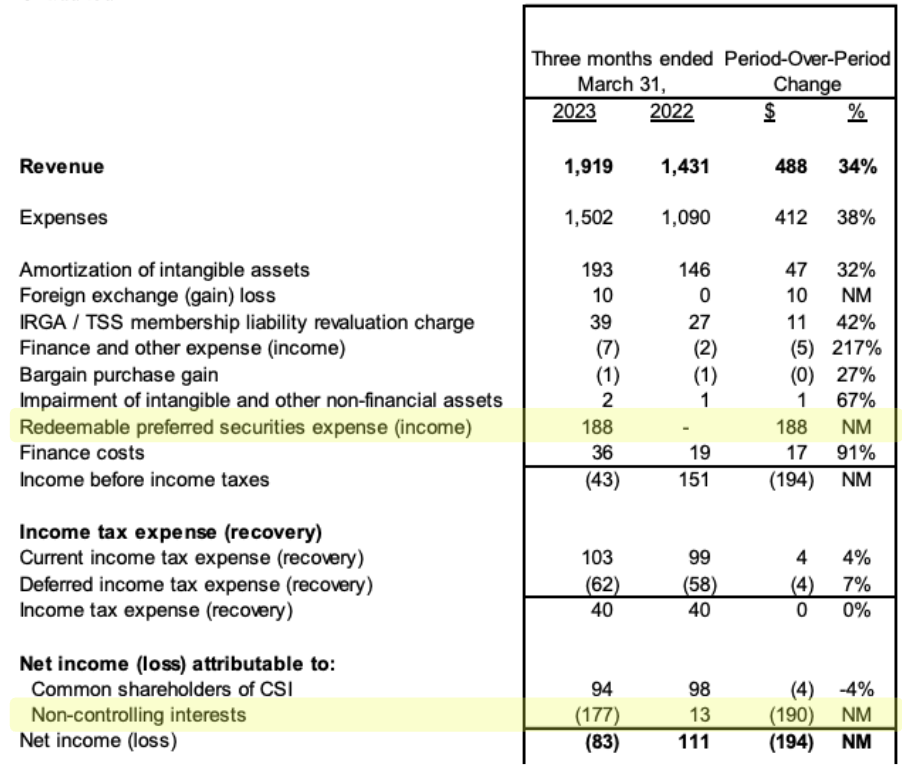

Constellation spun out Lumine Group Inc. ( LMN:CA , LMGIF ) this quarter, and this event has created more noise (yes, more) in the income statement . As with Topicus last year, Lumine incurs a redeemable preferred securities expense due to its share structure. The good news is this expense is not recurring and it's non-cash, but it undoubtedly introduces noise in the income statement.

Constellation Software recognized $188 million for this expense which is not included in net income attributable to CSI shareholders. As discussed before, Constellation consolidates Lumine because it owns a super-voting share that entitles it to 50.1% of the voting power. Still, the company owns almost 0% of Lumine, so it's deducted later in NCI. The discrepancy between this expense and what is deducted in NCI comes from the fact that there's more than Lumine there:

{kind=link}

With this expense behind us, we can now focus on the rest of the income statement.

There was margin contraction at the operating and net income levels even if we ignore this expense. The operating margin contracted due to a faster rise in expenses than revenue. These grew 38% year-over-year, 400 basis points faster than revenue:

Constellation's MD&A

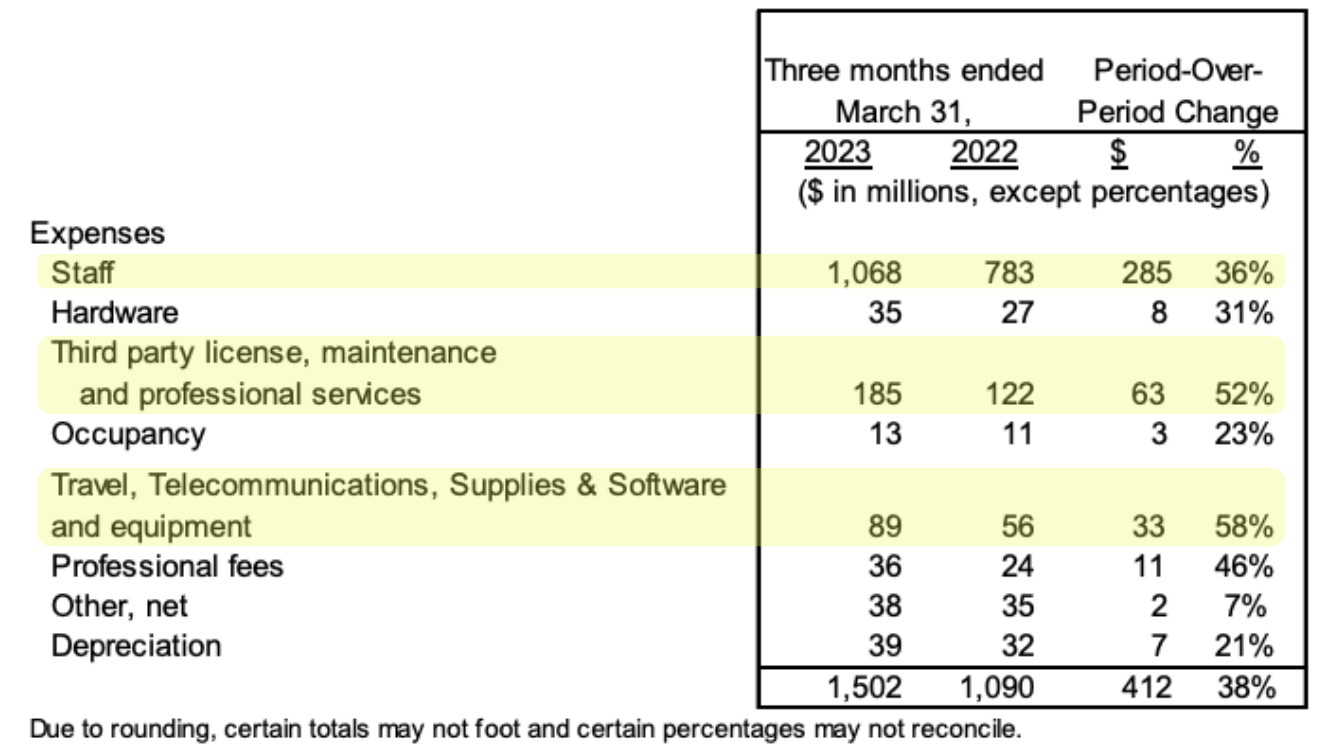

This difference comes mainly from the company's acquisitions, which typically have different cost structures to those of Constellation. Expenses that added the highest absolute cost were: staff; third-party license, maintenance and professional services; and travel:

{kind=link}

The increase in staff and travel are straightforward to understand. First, increases in staff expenses come from acquisitions. When the company acquires other companies, it also "acquires" its staff, and it's fair to assume that these companies usually don't have an ideal labor structure. If they had, Constellation would not be able to buy them cheap. Increased travel costs result from returning to a more normal travel environment after COVID.

As for the increase in third-party license, maintenance, and professional services , management attributed these to acquired businesses.

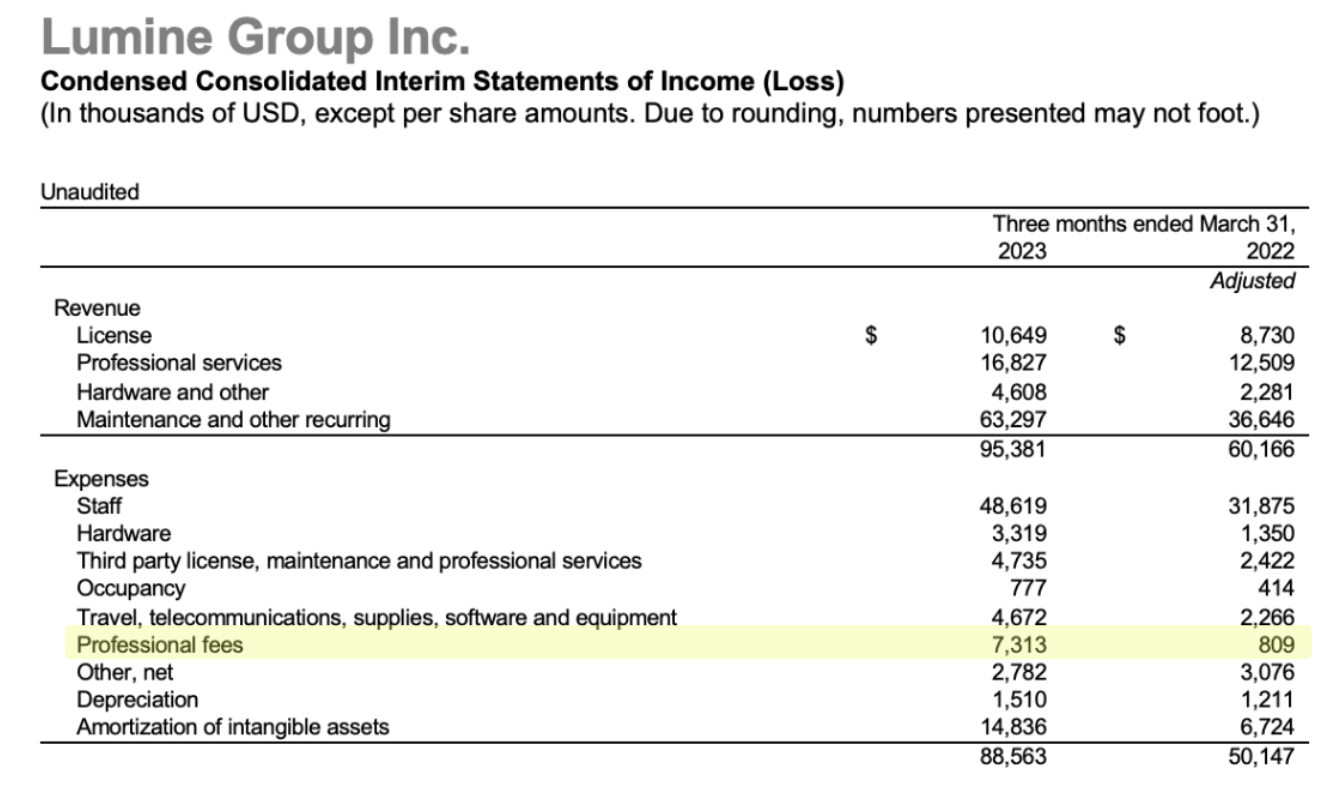

Another relevant expense increase came from professional fees , although it was not as important in absolute terms. It's hard to tell if some of these professional fees are still attributable to Lumine's spinout. Lumine saw a pretty substantial increase in professional fees in Q1, although we don't really know if these were related to the spinout because management has yet to upload the MD&A:

{kind=link}

Other, net was not a protagonist this quarter, but there are always several interesting things in this group. For example contingent consideration:

Constellation's MD&A

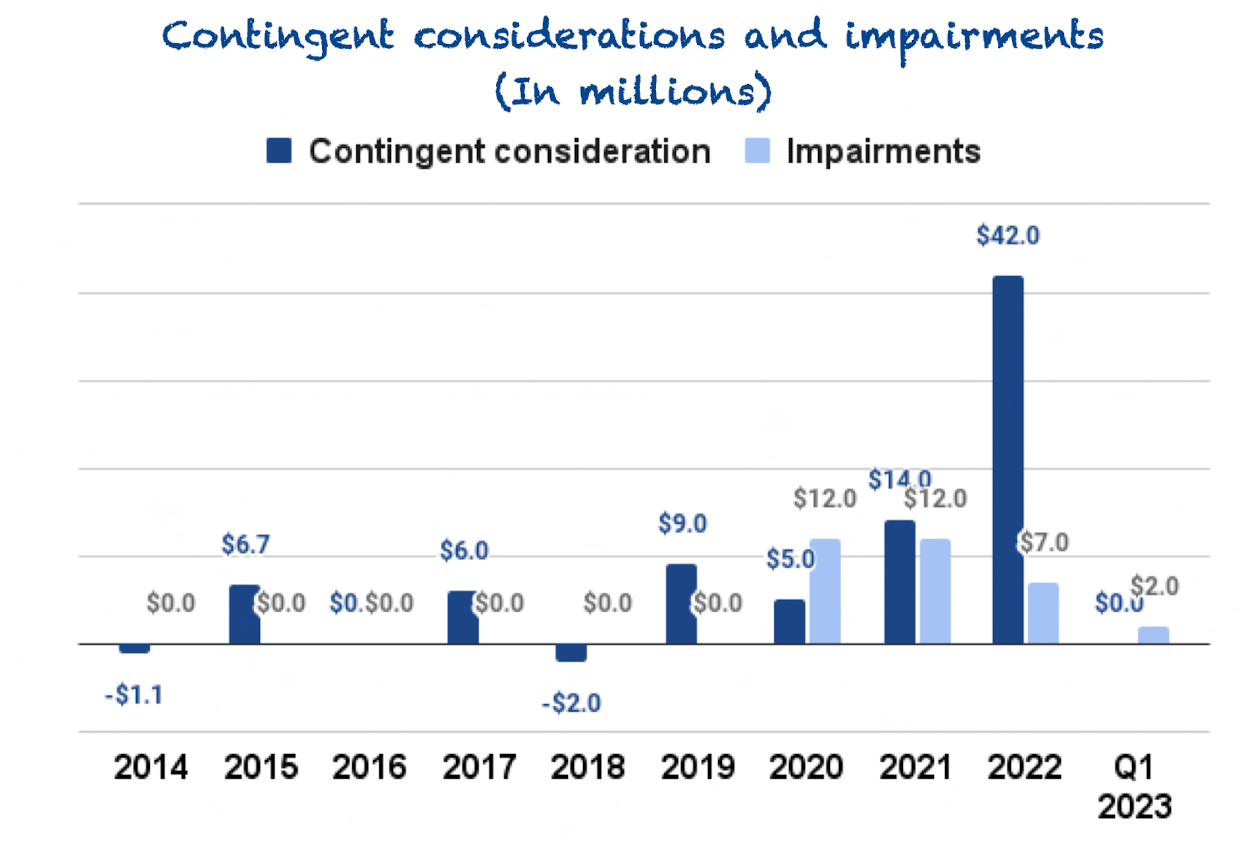

Contingent consideration decreased by almost 100%. In previous articles, we explained a few times already why contingent consideration is a "good" expense. The bottom line is that it measures the payments the company has to make when acquisitions go better than expected, which is great, of course. It allows us to have at least an idea of how acquisitions (those with contingent considerations) are doing. No contingent consideration expense is good for margins, but this means that acquisitions with contingent considerations included in them are not doing better than average.

The counterparty to contingent considerations is impairments , which slightly increased in absolute terms in Q1 to $2 million. If we plot both together, we can see there's no reason to worry about the performance of acquisitions right now. 2020 and 2021 brought significant impairments which might have been caused by COVID-related issues which were impossible to foresee.

{kind=link}

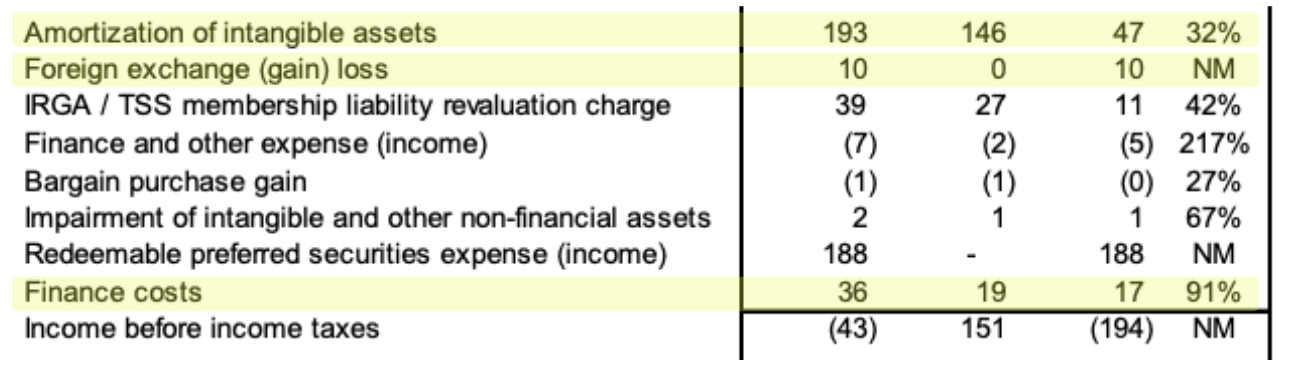

These increased costs, however, are not enough to explain the 4% drop in net income attributable to CSI shareholders. The fact expenses grew faster than revenue did create margin contraction, but several non-operating expenses augmented this :

{kind=link}

The most important of these were redeemable preferred securities expenses which we already discussed. Others were foreign exchange loss, and finance costs. Amortization of intangibles also added quite a bit of expense, but those grow due to acquired companies.

As for finance costs , these are increasing because management now runs a more leveraged balance sheet and interest rates are higher.

All in all, it was not the best quarter from a net income standpoint, but as we've seen, a portion of these increased expenses came from non-operational activities, some of which are out of management's control. But for Constellation, cash flows matter more than net income.

Looking at cash flows

A good deal of the increase in non-operating expenses came from non-cash sources, so Constellation grew cash flow nicely in the quarter and more in line with revenue.

Operating cash flow grew 27% year-over-year and FCFA2S (free cash flow available to shareholders) grew 40% year-over-year:

Constellation's MD&A

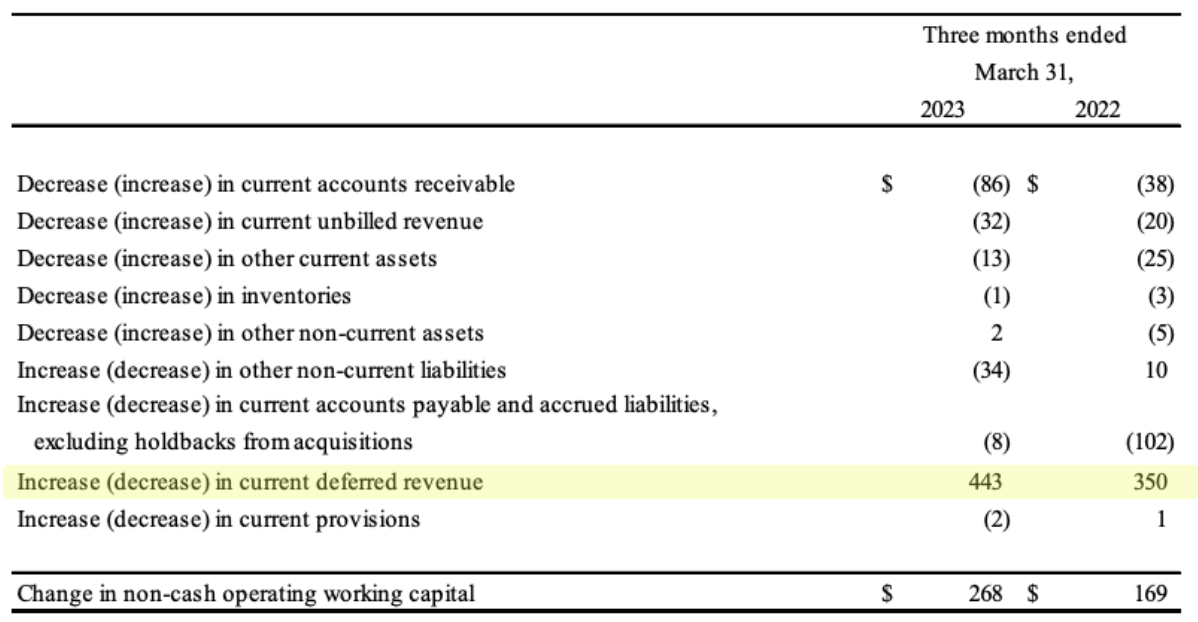

Improvements in operating cash flow came from the non-cash adjustments mentioned above and better cash conversion, primarily from an increase in deferred revenue. Increasing deferred revenue means customers made more cash payments to pay in advance for services but this revenue still has to be recognized later. "Current" deferred revenue means the revenue will be recognized over the next 12 months.

Deferred revenue is also the reason why the company's Q1 brings the highest cash flow and it operates with negative working capital:

{kind=link}

The growth in free cash flow was similar, but less was attributed to non-controlling interests, making Constellation's portion of this free cash flow advance faster than operating cash flow.

Acquisitions

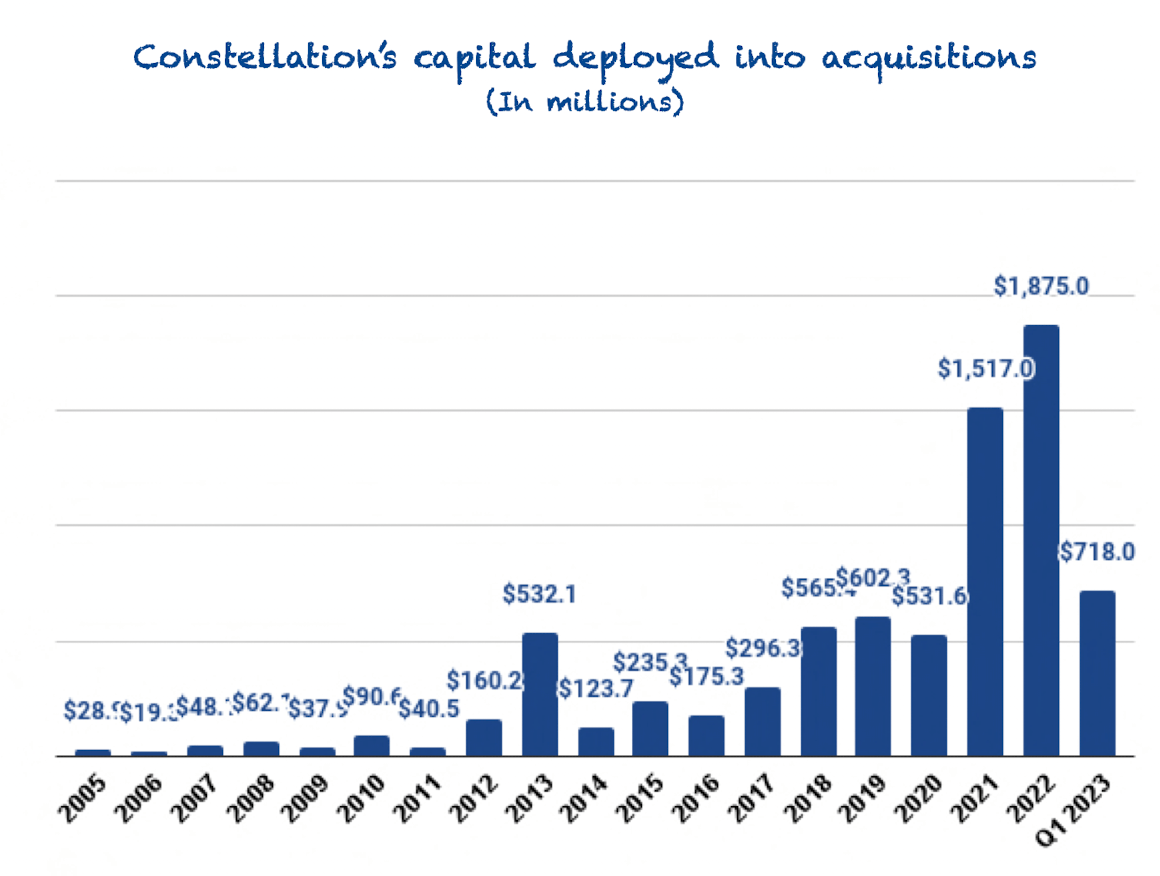

Constellation had a great quarter in terms of capital deployment. The company acquired companies for an aggregate cash consideration of $718 million . To put this into context, $718 million is higher than any year before 2021 in terms of capital deployment:

{kind=link}

$222 million of this total consideration was attributable to Lumine's WideOrbit acquisition. If we exclude this, we still get to a total amount of more than $450 million. It always seems as if Constellation has reached a limit, but management continues to find ways to deploy more money . Of course, as we have said several times, it's increasingly likely that more capital will have to be deployed in larger acquisitions, where hurdle rates are lower.

The good news here is that Altera, the company's largest acquisition, seems to be doing quite well. Let's look at it in a bit more detail.

Altera's performance is a good sign for future large acquisitions

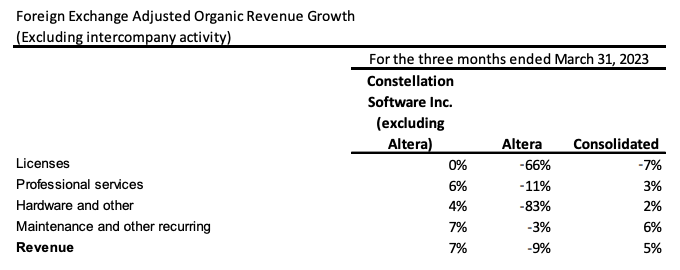

Organic growth is normalizing at Altera. It's still decreasing, but it's going down slower than last quarter and certainly showing some interesting signs.

{kind=link}

Note how most revenue sources are falling significantly, but maintenance and other recurring revenue remain fairly resilient . This is probably the result of a conscious and typical effort by Constellation's management to make this revenue source the most important revenue source for Altera, which will most likely help the company's growth remain more resilient going forward.

It takes some time to turn such a large ship, but the words from Jeff Bender during the Annual General Meeting indicated that results from the implemented changes are starting to surface.

So I mean, basically, we inherited one sort of Goliath business, we call it Altera, the carve-out from Allscripts. We now have turned it into 11 very focused business units , right, with their own, again, focus on your product and customers and employees. So I think that, to me, has been -- it's been a huge effort, but I think it was the right thing to do, and I think we're now starting to see the benefits of having done that. The other positive is when you acquire an organization with 5,000 employees, there was just some amazing, amazing talented employees in that organization. And I think helping them look at how to run a vertical market software business differently has been, again, very positive.

So again, they're embracing our best practices. They're engaging and again, trying to do things differently. So I think those have all been the positives. I think some of the negatives, I think, are trying to change a globally-based 5,000-person organization, like it just takes time. It's just -- it's slow.

Source: Jeff Bender, Harris Group's CEO, during the Annual General Meeting (emphasis added).

These changes can also be seen in the numbers. While revenue decreased year-over-year, both revenue and profitability increased compared to Q4 2022. Operating cash flow and free cash flow have improved markedly since Constellation's acquisition, but they worsened sequentially:

Made by Best Anchor Stocks

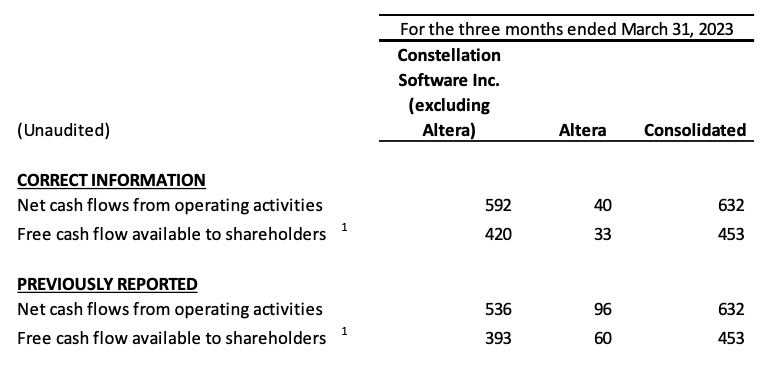

There was a mistake in the initial filing regarding Altera's cash flows, which has now been restated:

{kind=link}

If the numbers prior to the restatement were true, then the picture would be even better, but even with the restated numbers, Altera has generated $104 million in Free Cash Flow ("FCF") for Constellation in under a year . The company effectively paid less than a 9x FCF multiple for this asset. With an ongoing stabilization in growth and improvements in profitability, we might see this turn out to be a great investment for Constellation.

Success here goes beyond the numbers as it would effectively mean the company can successfully deploy cash into large acquisitions. This will be necessary to sustain high levels of reinvestment going forward. Hurdle rates for large acquisitions are lower, but according to management, there's a lower probability of missing these hurdle rates because there's more operational flexibility:

Yes, I think when it comes to larger sort of not speaking to Altera specifically, although it would fit into the same category. I just think the larger of the businesses are, the more opportunities there are to do things. So to Mark's point, whether there's more opportunities to leverage our best practices or they're just more levers to pull within the operations to help us get to or exceed the hurdle rates that we model in smaller businesses, you have a couple. And if they don't work out exactly as you had intended, it can be a little bit more challenging to find other ways to get there.

If I want to the larger ones, so it's just -- there's a lot more. And then the magnitude of what you can do when you put the best practice through tends to be -- tends to give you a lot more return as well on the larger transactions.

Source: Jeff Bender, Harris Group's CEO, during the Annual General Meeting (emphasis added).

Conclusion

Constellation Software Inc. reported another great quarter, as shareholder have become accustomed to. Revenue growth was excellent. Margins contracted due primarily to expenses the company can't really control. Cash flow growth was impressive, aided by better cash conversion, and the company pushed the boundaries of capital allocation yet again.

When it comes to the highest-quality companies, the best thing to do is to hold for a long time and don't do much, except adding to your position every now and then. Constellation Software Inc. is one such company, in our opinion.

In the meantime, keep growing!

For further details see:

Constellation Software Q1: The Wings Of Its Dual Growth