CA - Copper Mountain Mining Having A Very Bad Year

Summary

- Copper Mountain Mining is a Canadian small cap miner with one mine in operation (Copper Mountain) and another under development (Eva).

- The stock is down big on the year for a variety of reasons and with upcoming tax loss selling is unlikely to get better any time soon.

- The long-term thesis for both copper and Copper Mountain Mining looks very promising, but the remainder of the year will likely be challenging.

Hi everyone,

I'm writing about Copper Mountain Mining ( CCMC:CA ) & ( CPPMF ), which is a small holding of mine that definitely hasn't worked out this year!

Copper Mountain Mining is a junior small cap copper miner with one mine in operation, Copper Mountain in British Columbia, and one mine in development, Eva in Australia.

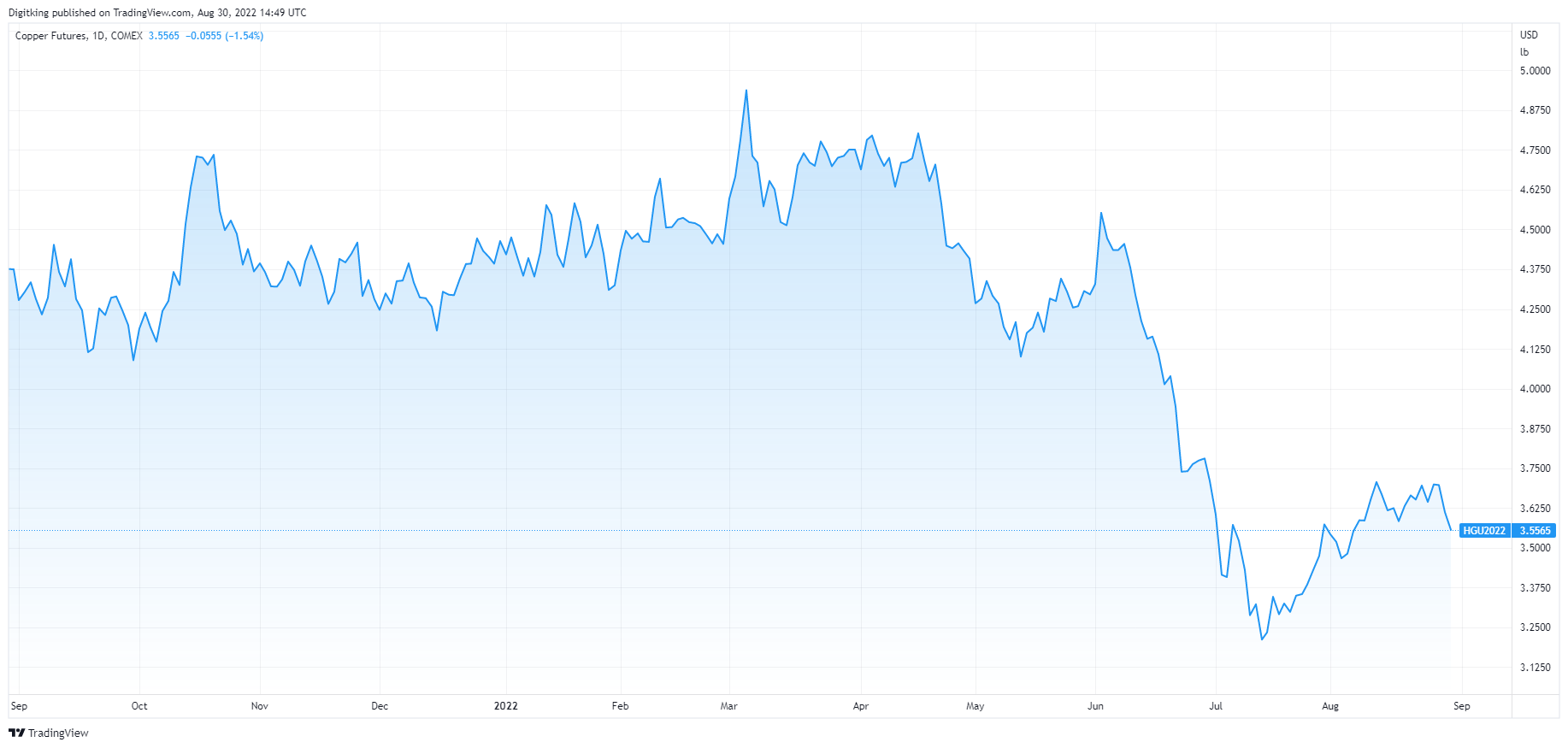

After having a strong bounce back from COVID in 2020 & 2021, 2022 has been a disastrous year for the company on many fronts. Starting with the share price which has taken quite the beating this year:

The stock is now down ~65% from its 2021 highs and ~55% YTD. Copper Mountain's shares have also dramatically underperformed the base metals miners index:

So why has the company underperformed so much this year? Well, it's been one problem after the other. Let's dive into them.

Dark Macro Clouds on the Horizon

It should come as no surprise to anyone that the fear of recession; whether that's from central bank tightening or the global energy crisis has rattled investors. "Dr. Copper" has also taken these global economic fears on the chin:

{kind=link}

Copper prices are now down ~25% from the highs set earlier this year (could've been a lot worse without the rally from July to August). Smaller mining companies like Copper Mountain have been hit harder by this decline and overall economic uncertainty.

Small-cap miners (orange line) have underperformed the broader mining indexes which are heavily weighted towards mega-cap and large-cap miners (purple line) by ~1500bps this year.

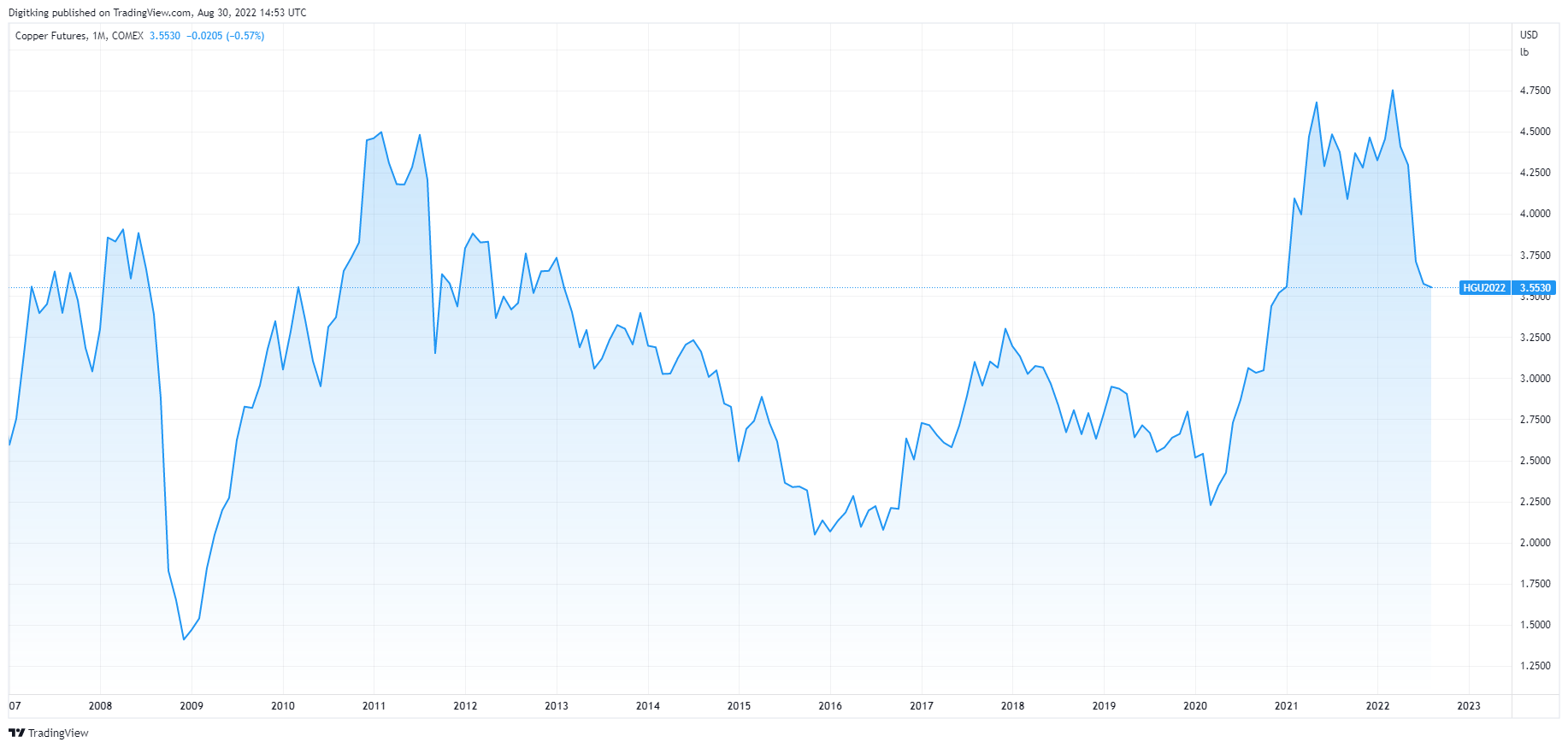

Lost in the shuffle and looking back a little further is that copper prices, even at ~$3.55/lb, is still pretty good when compared to the last 5-6 years.

{kind=link}

Given the unfolding energy crisis across the world (not just in Europe). It seems like the most likely trend short-term in copper is down.

Longer-term, the future is still looking very bright for copper. S&P Global, Wood Mackenzie, Goldman Sachs, IHS, and many others are very bullish long-term on copper.

The reason is pretty simple. A "green transition" is going to require an awful lot of copper and there's been very limited capital spending over the last decade to meet that demand.

One of my favorite articles of the last year was Issues' "The Hard Math of Minerals" which summarized the copper situation (well really all base metals and minerals) as such:

It has long been known that building solar and wind systems requires roughly a tenfold increase in the total tonnage of common materials-concrete, steel, glass, etc.-to deliver the same quantity of energy compared to building a natural gas or other hydrocarbon-fueled power plant. Beyond that, supplying the same quantity of energy as conventional sources with solar and wind equipment, along with other aspects of the energy transition such as using electric vehicles (EVs), entails an enormous increase in the use of specialty minerals and metals like copper, nickel, chromium, zinc, cobalt: in many instances, it's far more than a tenfold increase. As one World Bank study noted, the "technologies assumed to populate the clean energy shift … are in fact significantly MORE material intensive in their composition than current traditional fossil-fuel-based energy supply systems."

I recommend everyone read the entire article (if you have time), but safe to say that the long-term demand for copper itself is looking very good. It's just that you'll have to stomach the volatility in the short term.

Bad Time For Operations To Hit A Road-Bump

Declining price of copper has been tough for all mining companies. But for Copper Mountain, this has been compounded by operational problems that really hit the company hard in the first half of this year.

On the company's Q4 2020 report and conference call (in February 2021), the company alerted investors that the company's mine had suffered extensive damage.

A small piece of steel had gotten into the secondary crusher and did some serious damage to the crusher. This meant that the company had to stop using the crusher which dramatically reduced mine throughput.

At the same time, they were mining an area called Phase 2 which was expected to have much lower grades.

So in summary, copper prices were declining, meanwhile mine throughput grades would be substantially lower. Q1 and Q2 were shaping up to be very bad quarters! The stock quickly dropped from ~CAD$4.20/share to CAD$3.40/share on the news.

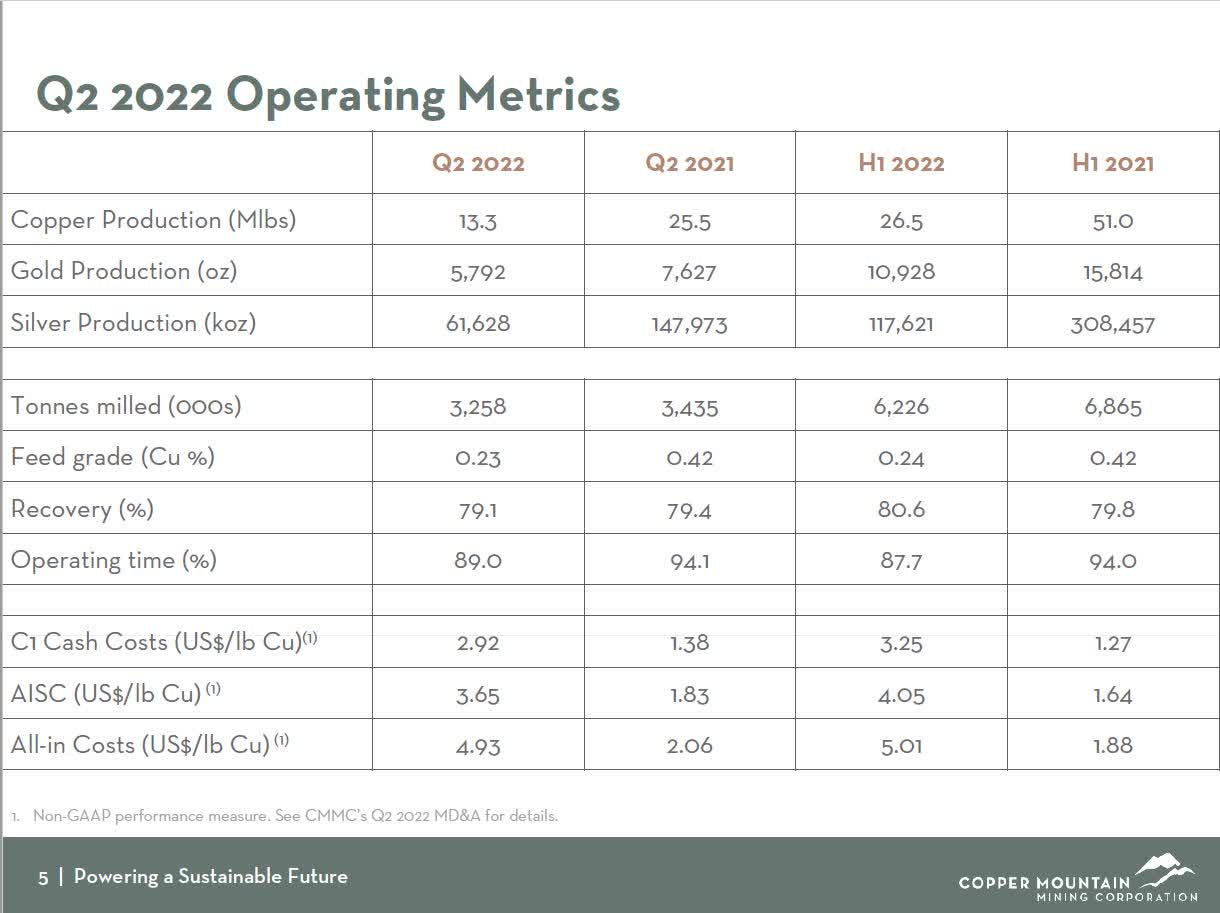

We then get to the Q1 and Q2 results which were bad (as expected), but it caught the markets off-guard just how bad they were given share price declined both times. As we can see from the slide below, production is down almost 50%, grades are down ~40% while cash costs/AISC are way up when compared with H1 2021 (due to lower mine throughput).

CMMC Q2 Conference Call Presentation

{kind=link}

Management is now guiding that the second half of the year and 2023 will see a significant turnaround in production as the crusher has been fully repaired and significant upgrades to the Copper Mountain mine have been completed in the meantime.

While these kinds of things do happen in mining all the time, they still hurt management credibility. It'll be up to management to rebuild their credibility through solid execution and no more "surprises". Which leads me to the latest setback...

The Hits Keep Coming

Last week, Copper Mountain announced that their CFO had been terminated and that their VP of Finance would be promoted to CFO on an interim basis. This was a pretty shocking announcement and the company didn't provide any reason or rationale for the termination.

The following day Mining Journal (among many others) reported that the (now fired) CFO, Rodney Shier, had sold ~1/2 of his CMMC shares between November 2021 and March 2022 without disclosing it or filing any of the proper paperwork. Once the company and Board of Directors became aware of the situation, they promptly fired him for this serious breach of laws and regulations.

This was (hopefully) a one-off and none of the other executives at Copper Mountain have done anything similar. But again, it further hurts their credibility at a time their credibility wasn't great to begin with. The net result is that most investors will have Copper Mountain in the "penalty box" for the remainder of the year (or longer).

Management really needs to execute and "keep their noses clean" now to rebuild credibility. But it's going to be a real upwards battle.

The Coast Isn't All Clear

Copper prices have tanked and are now appearing to be on the mend (or at least stabilized). Management has indicated that the production issues are behind them and going forward, it should be all clear to "buy the dip" right?

Wrong.

Unfortunately, this has been a tough year for most investors (stating the obvious). After the last couple of years of big market gains, I expect that we'll see significant tax-loss selling in Copper Mountain along with many other names.

Tax loss selling can often have a huge impact on Canadian shares, especially smaller and less liquid names such as Copper Mountain.

I think there's a very good chance we could see a scenario like this:

- Copper prices have bottomed and are slowly rising.

- Management reports Q3 results sometime in October showing a rebound in operations along with positive updates on Copper Mountain LoM and the Eva project.

- Share price sinks going into year-end(i.e. drops under CAD$1/share), as investor look to realize tax losses in November & December.

For this reason, I can't recommend buying now. Even if the fundamentals started to improve, I think it would be drowned out by tax loss selling. I've already started to put together a shopping list of tax-loss candidates to "buy the dip" for late November and December. Barring any more surprises, Copper Mountain will be one of them.

Longer-Term Thesis

The medium to long-term thesis on Copper Mountain Mining still looks very enticing, despite the short-term setbacks.

Copper is going to be in short supply for the rest of the decade, and given that it now takes on average 12-17 years to build a new mine, it's highly unlikely that additional supply will be brought on fast enough to meet the expected demand.

Copper Mountain's mine is in a low-risk jurisdiction (British Columbia) with its copper project under development, Eva, also in a low-risk jurisdiction (Australia).

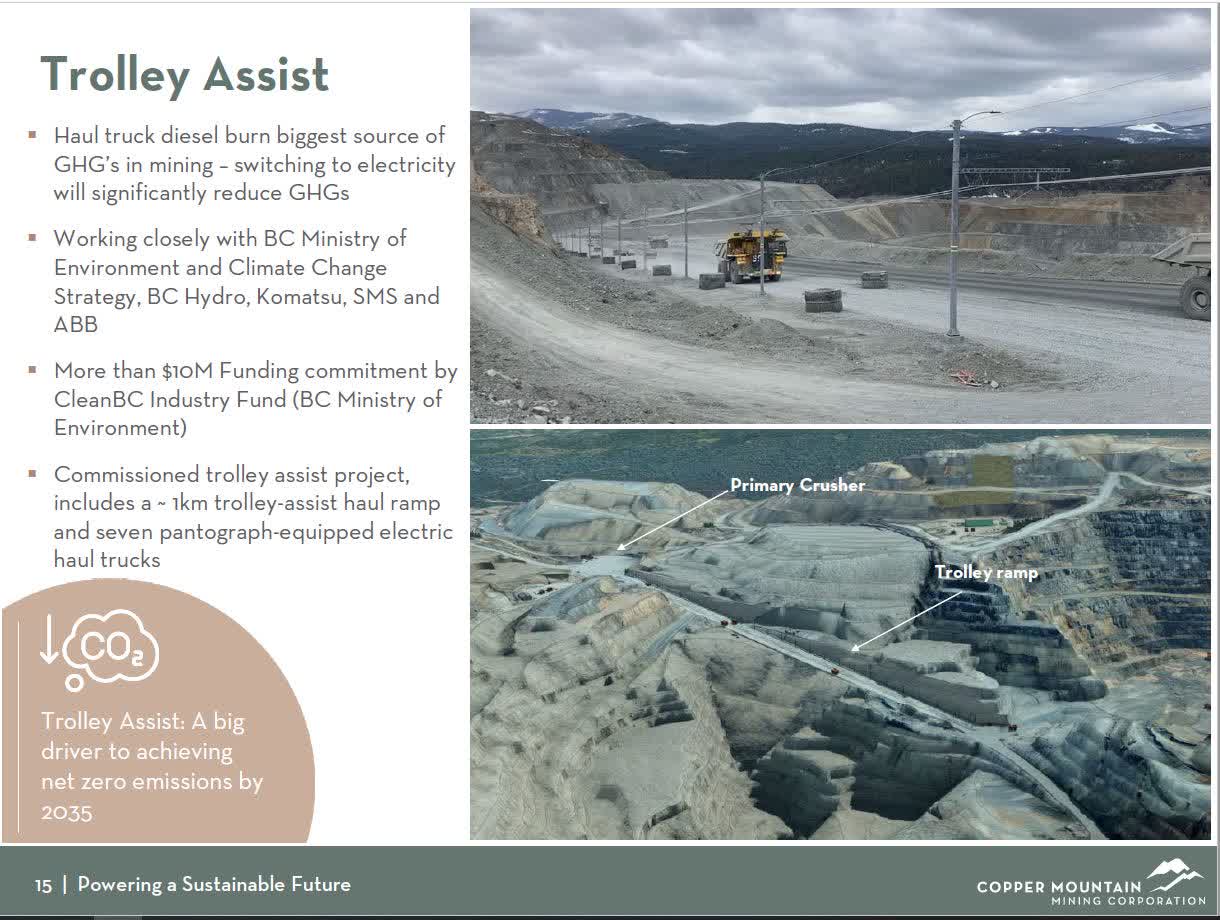

The company is also busy making interesting improvements that will both save costs, improve efficiency and improve its environmental record. For example, they recently installed an electric trolley system (the first of its kind in North America) to pull their haul trucks out of the pit. This reduces the energy consumption (saves on diesel), increases the speed of the haul trucks, and reduces the environmental emissions (as the electricity comes from nearby hydropower plants).

CMMC August 2022 Corporate Presentation

{kind=link}

These are the kinds of "win-win" moves I like to see as a long-term investor. But it'll take a lot more of them to get investors back in the name.

Overall the company's shares are very cheap once the operational issues are sorted out. However, you won't know this by looking at the share price over the remainder of the year as it's likely to remain under pressure from tax loss selling.

I think the biggest risk to the thesis (short of bankruptcy) is that a larger mining company swoops in and buys the company while it's cheap. At first glance, a large company such as First Quantum or Freeport stepping in and offering a 25% - 50% premium being a "bad outcome" would seem absurd. But that kind of premium would probably only amount to a share price offer of CAD$2.00-$2.50/share which would leave many investors underwater and a bitter experience.

So in summary, this is a small holding that I have and won't be adding to it in the short term. Hopefully, as we approach Christmas and year-end, we'll have a better understanding of how well (or poorly) the operations are going and have a chance to add to the position from price insensitive (aka tax loss) sellers.

Until then, stay safe and have a good fall.

For further details see:

Copper Mountain Mining Having A Very Bad Year