CORT - Corcept Therapeutics: Growth Investment Geared Entirely To Clinical Programs

2023-06-08 08:33:03 ET

Summary

- Corcept Therapeutics' stock is trading back at FY'22 range after a snapback rally leading into Q2 FY'23.

- The company is allocating capital to its clinical programs, but returns on these investments haven't beat the hurdle to date, leading to economic losses for shareholders.

- I suggest a period of flat growth moving forward and reiterate my hold rating for Corcept Therapeutics.

Investment Summary

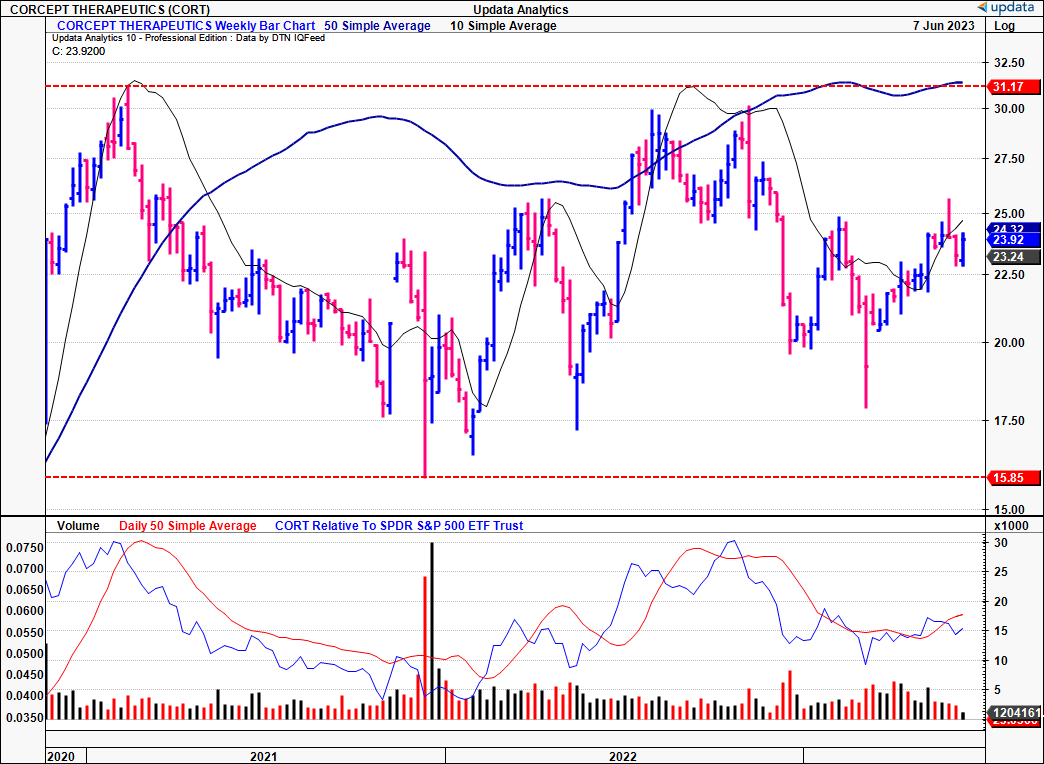

After a snapback rally leading into Q2 FY'23 the equity stock of Corcept Therapeutics ( CORT ) is now trading back at FY'22 range. In my previous CORT publication I urged investors to consider holding off the stock until further clarifications were obtained. The Korlym saga is still ongoing, despite a trial date set this year, but there insufficient data to warrant CORT's revised rating to a buy in my opinion.

In this report I'll delve into the critical facts underpinning the hold thesis, paying close attention to the firm's capital budgeting and investments to future growth. Findings show the company is allocating capital to its clinical programs, but that's about it, and returns on these investments haven't beat the hurdle to date, leading to a series of economic losses for shareholders. It is difficult to see investors paying 36x forward earnings and 25x forward EBIT with these characteristics, let alone paying any upside on this. For the buyer of CORT today, my analysis suggests a period of flat growth moving forward, and this supports a neutral view. Net-net, reiterate hold.

Figure 1. CORT 2-year price evolution

{kind=link}

Critical facts – Q1 Numbers, Capital Productivity, Growth Investments

After 5-years of horizontal equity gains, investors deserve an informed appraisal of the company's investment offering. This is simple enough. I'll anchor against the Q1 numbers and to exhibit the broader fundamental issues in need of discussion.

Q1 desegregation

CORT leaped out of the gate in FY'23 with a 13% YoY growth in Q1 turnover to $105mm. Around 50% of this growth was underscored by new patient starts on its Korlym label. So much so, that it now projected $455mm in top-line revenues for FY'23 after revising the outlook last period. I'd encourage you to check the deep dive performed in my last CORT publication.

You'll also read in that publication of the ongoing lawsuit with Teva Pharmaceutical ( TEVA ) regarding the Korlym label. As a reminder:

- In March 2018, CORT initiated a lawsuit against Teva in a Federal District Court to prevent the unauthorized marketing of a generic version of Korlym. CORT alleges this would infringe on its patents.

- Management noted the court has recently ordered both parties to negotiate a schedule for pretrial activities, and the trial is now scheduled to commence on September 27th this year. Definitely keep a very close eye on this date.

- Very importantly from this result–– Teva can no longer challenge the validity of the 214 patent until then. The patent trial and appeals board upheld the validity of this patent after Teva's post-grant review. Per Charlie Robb on the earnings call, " Teva's only remaining defence is to argue that their proposed product does not infringe on our patent".

This is good news and should provide greater visibility on future cash flows in my view. Still, the price response remains mute. It pulled the $105mm in turnover to $15mm in operating income and $0.15 in quarterly earnings.

Capital productivity, profitability

The financial results, whilst telling of the state of the business operations, do little in the realms of educating us on CORT's business economics. A more thorough look-through at the firm's usage of capital, profitability and value creation is warranted.

The calculus underpinning CORT's rolling valuation are fairly easy to ascertain in my view. It is formed by the contribution of its steady-state operations, plus the contribution from its future growth. Both involve the firm's profitability and ability to grow profits for its shareholders over time.

Growth is obtained as a product of the firm's capital investments and operating margin. On that, CORT is indeed a profitable entity, evidenced by the following record:

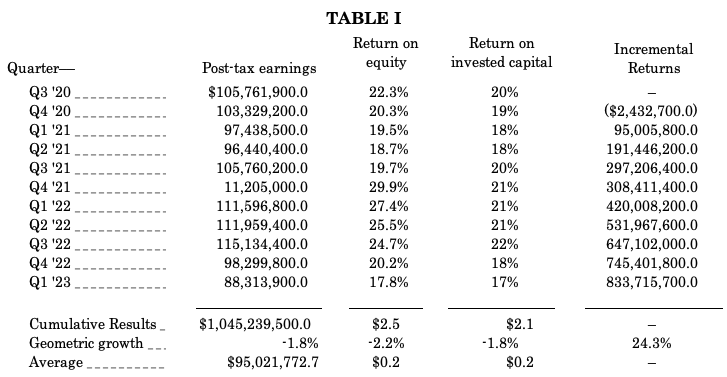

Note: Rolling TTM periods are shown (Data: Author, CORT SEC Filings)

{kind=link}

Table 1 shows the rolling TTM results for the firm's returns on equity and capital, including the incremental post-tax earnings produced since 2020. Over this time, CORT has generated $1.045Bn in cumulative tax-adjusted operating income, equating to a 24% annualized compound rate. The return on existing capital is superb at 17–20% range, but has clipped back by 3 points. Nevertheless, CORT has averaged 20% ROE and ROIC over this period, well above the hurdle rate (12% in this analysis).

Two issues here, however:

- There's been no additional post-tax income generated for shareholders since 2020 – $88.3mm versus $105mm (TTM figures);

- At the same time, CORT has put no additional capital at risk, investing negligible further capital on top of its Q3 FY'20 base [Figure 3].

The ability for a firm to generate above-market returns on investment is a critical feature within my investment criteria. If I can get 10-12% riding the benchmark, I'd look for my companies to be pushing 15%+. You couldn't serve me a more delicious investment cake. Delicious as this is, to find such a sweet offering is incredibly rare. Not in the least due to the fact that highly lucrative investment opportunities aren't always on the table. Imagine you are a highly skilled mathematician. With a small investment of your time and capital, your mathematical edge gets your clients 15–20% faster lead times than any of your competitors. Everyone wants to hire you, and you are able to create immense value for your stakeholders. You are profitable, and gaining new clients quarter-on-quarter. The problem is, at some point, there will be no more new clients to take on. No more new jobs. No new opportunities to invest. It's the same for businesses.

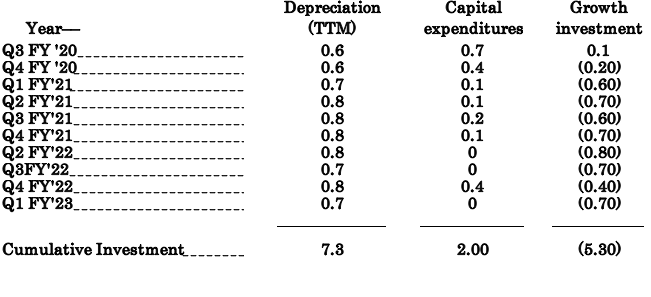

Oftentimes, firms have the capital, but just not the opportunities to deploy it at high rates of return. That is a problem, because this too is an opportunity cost, and therefore, value lost. Earlier I noted the lack of growth CapEx CORT has allocated over the testing period. The firm's agnostic position to investing to growth is exemplified below:

{kind=link}

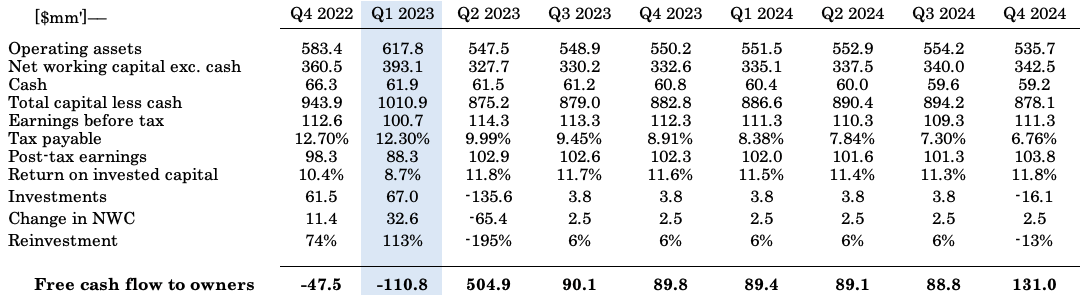

The growth investment is measured as the delta between depreciation charge and CapEx, as it one advocated convention. Notably, the firm has invested a cumulative $2mm over this time, but this is $5.3mm below the 'maintenance' CapEx of $7.8mm.

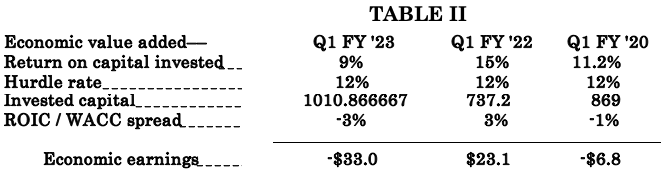

Net-net, the result has been a pullback in economic earnings over the last 2-years to date. Assuming a 12% hurdle rate, the firm generated a negative $33mm in economic loss in Q1, behind the $16mm accounting profit [Table 2]. This is a critical fact that investors must be factoring in at this stage. The firm's lack of economic profitability would be the major driver to its compressed valuation in my opinion, and justifies the low rating should it continue growing the top-line.

{kind=link}

Investments in clinical programs

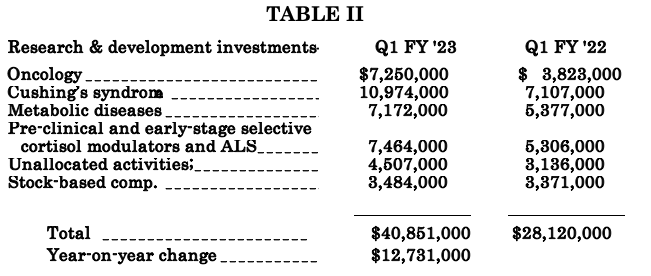

The lack of tangible investment is telling. It me the firm has been allocating the bulk of capital towards its clinical programs, 'investments' that are in actually expensed on the income statement.

This is important, as it did in fact put another $12.73mm towards its R&D pipeline from Q1 last year. That made a $40.8mm quarterly investment over the 12-months to March 31st this year, and thus you're looking directly to the firm's clinical trials as potential catalysts to move its stock price.

{kind=link}

Looking ahead, CORT anticipates several significant milestones in the coming months. To name a few:

- It expects to receive crucial data from our GRACE, Gradient, and NASH Phase Ib studies.

- The Gradient Phase III trial will evaluate relacorilant in patients with Cushing's syndrome caused by adrenal adenoma or adrenal hyperplasia.

- Furthermore, it intends to New Drug Application ("NDA") for relacorilant in Cushing's syndrome in the H1 of FY'24, leveraging the data from the GRACE study as a basis for the submission.

A key point I'd say to investors is to stay active on the readouts of these trials in FY'23. It will be in H2, when most companies do so, and thus keeping a watch on the company's chart and fundamentals until then could be worthwhile.

Nevertheless, the capital charge to R&D is noted, but hasn't rotated back into additional market valuation for CORT. Not surprising, given the asymmetrical payoffs with R&D investments. Collectively, I am reserved on the company's ability to attract investment on this basis.

Valuation and conclusion

Much of the rational investment debate falls off the cliff face when talking about valuation with CORT. The market has it priced at an eye scorching 36x forward earnings and 25x forward EBIT. I simply cannot wrap my investment tentacles around this valuation with the firm's lack of monetized investment, negative economic earnings and thin incremental returns on capital.

CORT's 5-year historical P/E is 19x, in-line with the sector. I believe this is a far more appropriate multiple for the company going forward. Assigning this to my FY'23 estimates on CORT's owner earnings gets me to $19.90 per share valuation, below the current market price, thereby supporting the neutral view [see: Appendix 1 for forward estimates].

Appendix 1. CORT Forward estimates

{kind=link}

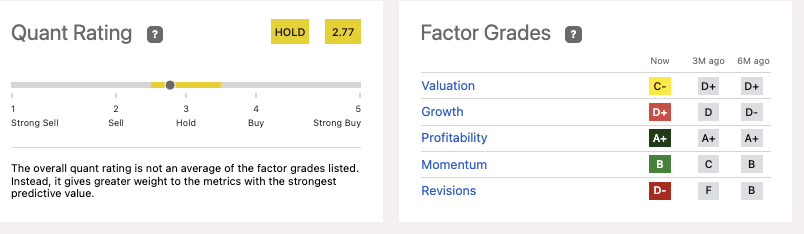

This neutral rating is well supported by objective findings presented in the quant grading system . Critically, it has shown similar results to my own findings, in valuation and growth factors. This must be considered and therefore reiterated a hold view.

Figure 2. CORT quant factor grades

{kind=link}

Net-net, there is insufficient evidence to suggest CORT warrants a revised buy rating in my view. There is still too many unanswered questions on the growth and investment front. CORT has been heavily investing in its clinical programs, but these have yet to pull through to tangible earnings just yet. With numerous selective opportunities available in this space, I am reiterating CORT as a hold.

For further details see:

Corcept Therapeutics: Growth Investment Geared Entirely To Clinical Programs