CA - Corus Entertainment: Macro Headwinds Provide Entry Point

2023-05-01 10:54:00 ET

Summary

- Ad recession woes have hammered Corus' stock price, and brought net debt to segment profit (similar to EBITDA) up to 3.59x. Leverage will likely rise further in the near-term.

- But the stock price pullback is out of proportion with temporary macro headwinds and with the slow secular decline in the core linear business.

- Current free cash flow yield is around 35%, on a normalized basis, it would be in excess of 80%, and the post-cut dividend yield is back over 8%.

- There is enough pessimism baked into the stock that the bar is set extremely low for future business performance.

- I discuss the recent amendment to the credit agreement, the leverage covenant, and prospects for a further dividend cut.

Investment thesis

With Corus Entertainment Inc.'s ( CJREF )( CJR.B:CA ) stock price recently plunging by close to 70% from a year ago, below the lowest point in March 2020, one might think that Corus is in a precarious state of financial distress. But this isn't quite the case, even if the macroeconomic outlook has created temporary headwinds. Corus' y/y decline in consolidated revenue of 6% fiscal year-to-date is the result of an ad recession that has affected the media sector in general, and is largely not reflective of company-specific problems.

Subscriber revenues are declining at a slow pace, they continue to be free cash-flow positive, debt is moderate even relative to the depressed current business performance, they should be able to navigate through any potential issues with their leverage covenant, and they have close to C$300M in liquidity, as of F2023Q2.

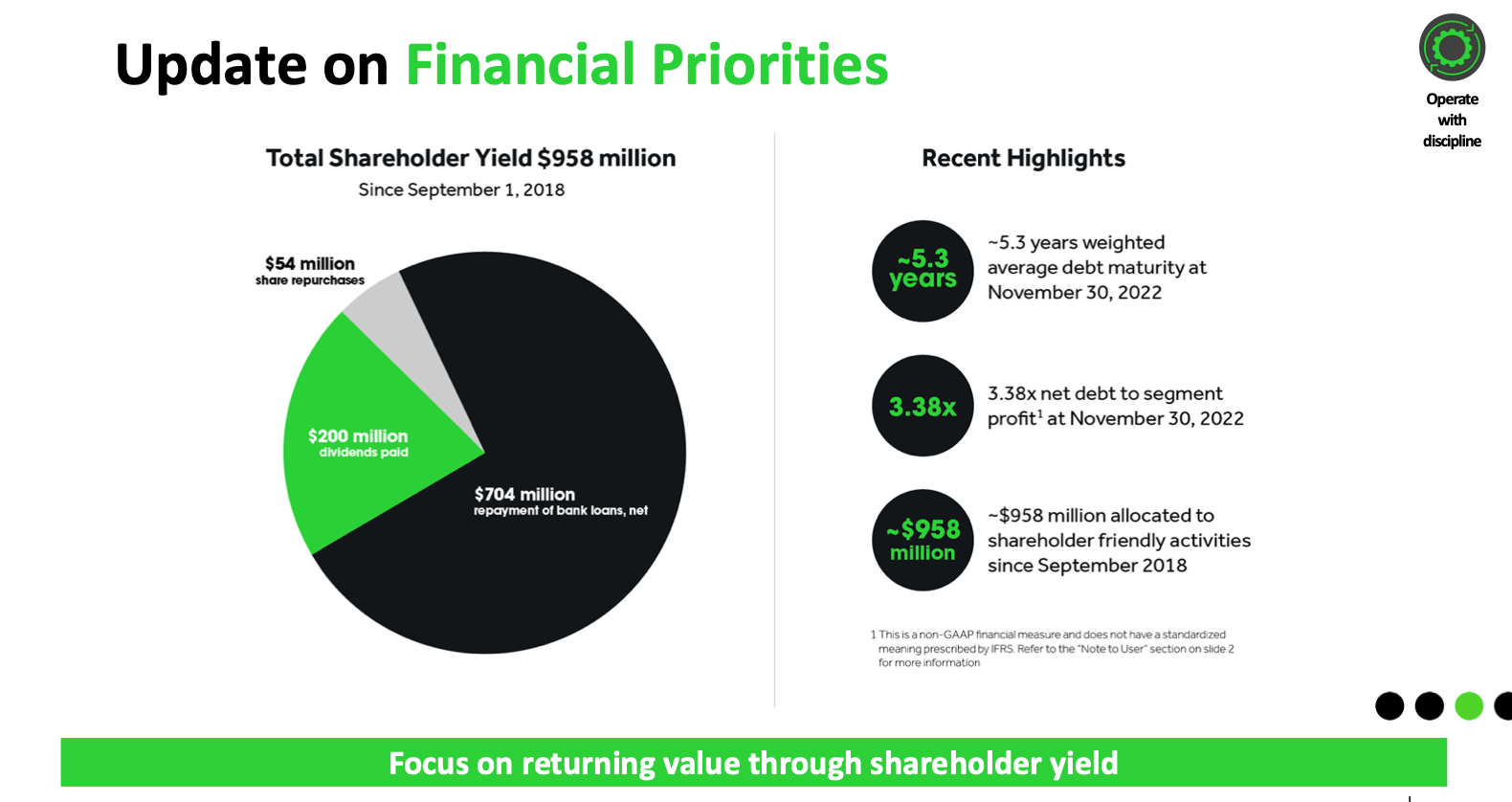

With so much pessimism baked into the stock, the bullish thesis is that expectations are too low. Corus has allocated C$958M in shareholder-friendly ways since September 2018, in the form of debt reduction, stock buybacks, and dividends, relative to the current market cap of ~C$285M. Temporary macro headwinds will eventually recede, and Corus will get back on track with deleveraging.

Background

I previously wrote about Corus two years ago, and the stock price fluctuated for a while before taking a sharper turn for the worse particularly starting in mid-2022. To give a quick business overview, Corus is a Canadian media/entertainment company that operates 33 specialty cable channels, 15 television stations, and 39 radio stations, produces content, and has a streaming service, StackTV, which includes a bunch of their content offerings live and on-demand.

A few highlights that might motivate some interest in a bullish case:

- Even with the weaker macro conditions, Corus has still generated C$49M in free cash flow in the past two quarters.

- Free cash flow in 2021 and 2022 was C$252M and C$241M, respectively, relative to a current market cap of ~C$285M. Free cash flow prior to the pandemic was also strong.

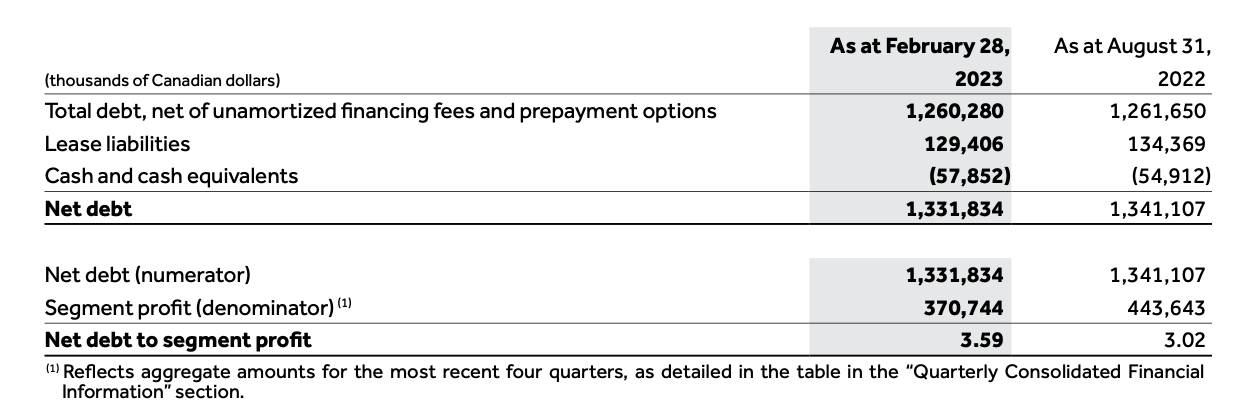

- As of February 28, 2023, the Company had $57.9M of cash and cash equivalents and around $241.6M that could be drawn on its Revolving Facility.

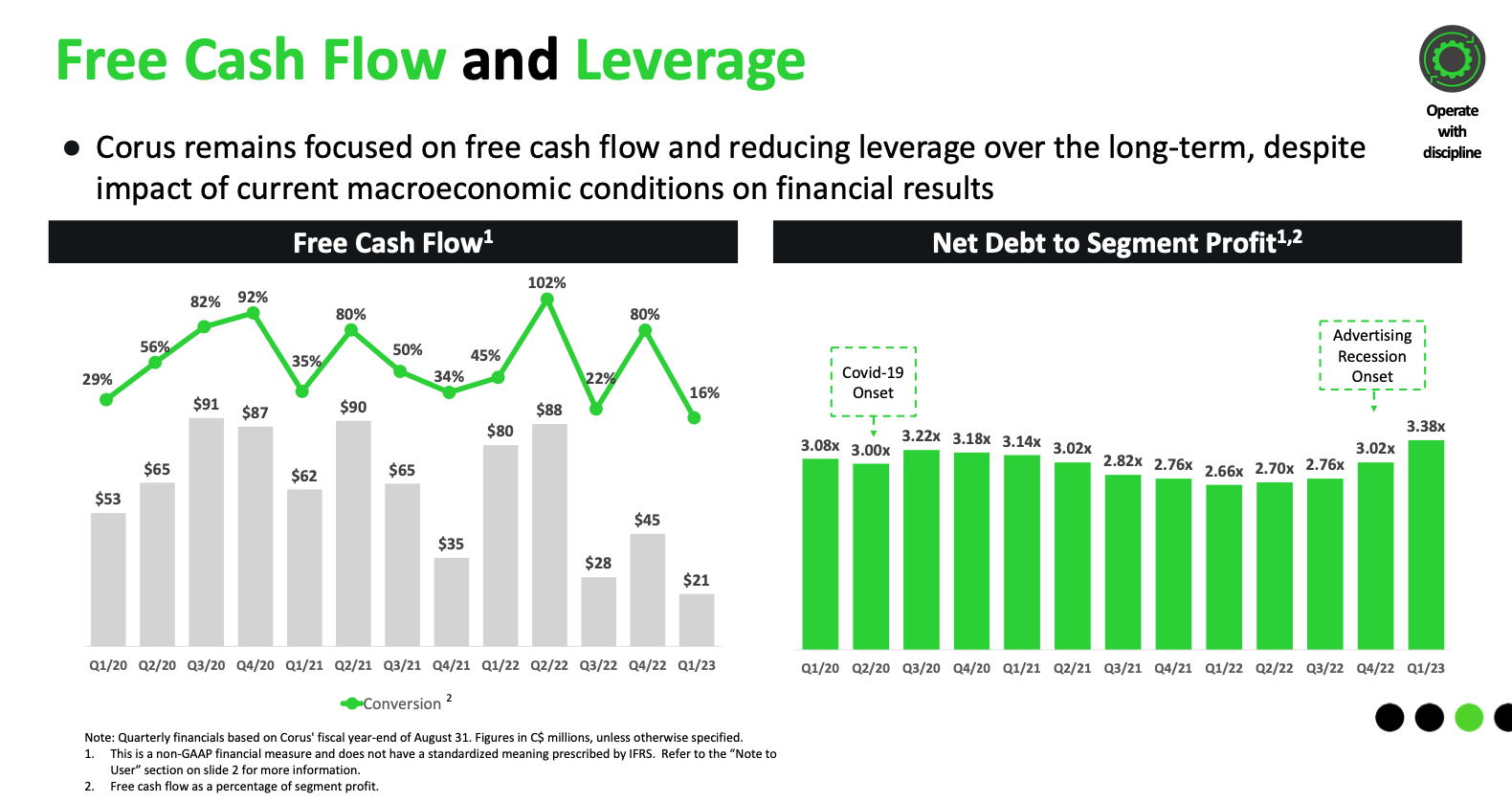

- They have reduced bank loans by C$704M since September 2018, and brought net debt down from ~C$1.89B to C$1.33B in the most recent quarter. Given their liquidity position, current FCF, normalized FCF, segment profit, and ~5 years weighted average debt maturity (as of F2023Q2), debt looks manageable.

- After the recent dividend cut to C$0.12/year, the yield is back over 8%.

- Although it's not clear when macroeconomic headwinds will abate, it's too early to discount the earnings strength of the business in normalized economic conditions.

https://assets.corusent.com/wp-content/uploads/2023/02/Corus-Investor-Presentation-Feb-723fw.pdf (Corus Investor Presentation, Feb 7, 2023) Corus Investor Presentation, Feb 7, 2023

{kind=link}

{kind=link}

Competitive Threats

Competition is a fact of any sector -- media/entertainment is clearly no exception. Undoubtedly, the streaming wars and proliferation of U.S.-based streaming services, are a concern for some investors in terms of the potential impact on Corus. But a few observations come to mind:

- U.S. players have often found it advantageous to partner with local companies in the Canadian market, with Pluto TV being the latest example, where Corus is the advertising representative .

- Corus is also the marketing partner for Discovery+, in Canada.

- This can be partly explained by the advantages of tapping into Corus' local ad salesforce, and regulatory context, including broadcast/cable regulations, which had led U.S. companies to strike licensing deals with Canadian cable providers, as well as minimum requirements for Canadian content.

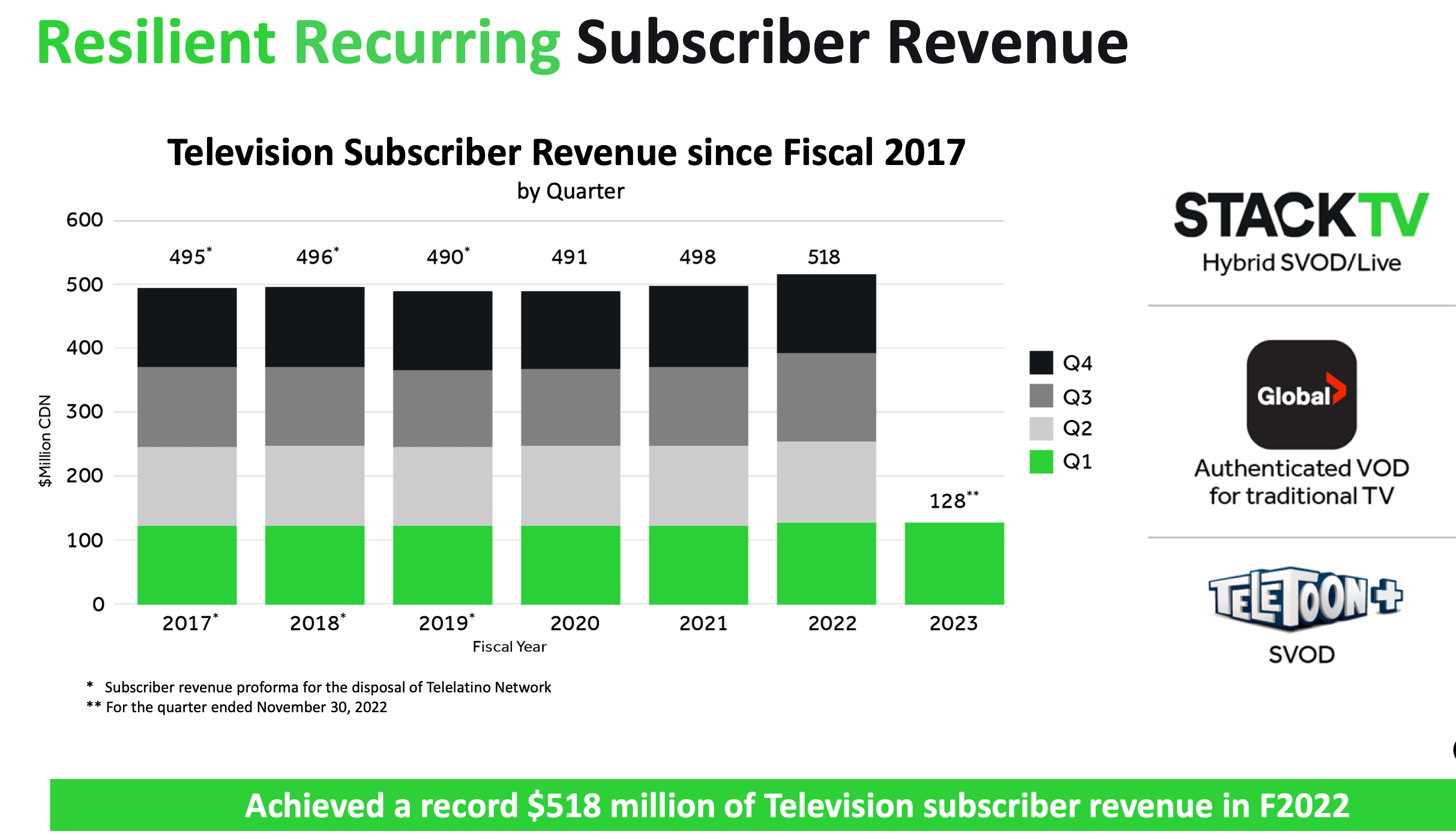

- Skinny basic cable TV bundles in Canada have provided a relatively affordable option for several years, now. As a result, the secular decline in Canada's cable business is occurring at a slower rate than what is seen in the United States.

- In that respect, subscriber revenue has held somewhat steady at Corus over the past few years (see figure below). In the most recent quarter, the y/y decline was 2%, after the " retroactive adjustment from renewal of distribution agreements ".

- Growth for Corus' StackTV and other streaming options has flattened out, but is still up to 750,000 subscribers versus 725,000 a year ago. Along with other digital initiatives, this has helped to offset the slow secular decline in cable.

Corus Investor Presentation, Feb 7, 2023

{kind=link}

I've written about a number of streaming companies including Warner Bros. Discovery ( WBD ) and Netflix ( NFLX ). The industry has been entering a new phase , with a focus on profitability leading to consolidation, price increases for streaming services, and potentially a slow-down in growth on content spend. This points to a retreat from the scorched-earth pursuit of subscriber growth, which characterized Netflix's disruptive entry into the sector.

In this respect, Crave (which includes HBO and other content) costs C$20/month in Canada , while Netflix ranges from C$10-21/month. These prices will almost definitely go up over time. Meanwhile, PlutoTV and other FAST services are, in economic terms, " inferior goods ", which households would typically not rely on exclusively, if they have enough disposable income to do otherwise.

But the combination of streaming and more traditional media remains complementary and fairly affordable in Canada, as shown by the slow decline in linear subscribers. Overall, competitive threats should be put in perspective of the depressed stock price.

The Leverage Covenant and Other Risks

While the depressed stock price should help to partly offset risks, nevertheless, risks remain. Some of these include:

- Prolonged macroeconomic headwinds.

- Failure by Corus to grow its streaming services.

- An acceleration in subscriber declines in the cable business.

- In general, a worsening in business performance that could lead to a breach of covenant and require an additional cut to the dividend.

- Any number of other unforeseen company-specific or other issues.

Leverage will no doubt increase, as results for the most recent four-quarter moving window get weaker because of the ad recession. As a result, Corus proactively amended its credit agreement to increase the threshold for the "Total Debt to Cash Flow Ratio" to 4.75x until August 31, 2023.

As explained on the F2023Q1 call , the Total Debt to Cash Flow Ratio is about 1/4 to 1/3 of a turn higher than the "net debt to segment profit" that the company regularly reports. The difference is driven by using gross debt for the covenant, with some adjustments for minority interest. Given the current state of leverage and the covenant, it seems odd that they don't report both, even if net debt would ordinarily be more relevant for investors, and the spread isn't moving around much.

{kind=link}

Ultimately, I expect that Corus can manage through the macro headwinds and the leverage covenant issue through some combination of the following:

- Avoiding a breach of covenant, with the help of cost cuts and the recent higher prioritization of debt repayment.

- Proactively obtaining amendments to the credit agreement, if needed.

- Proactively obtaining waivers, if needed.

- Cutting the dividend.

- Refinancing debt by finding other lenders.

A breach of covenant would put the ball in the court of the bank creditors, and give them the right to demand immediate payment of debt. My expectation is that a breach of covenant would most likely lead to a further cut or elimination of the dividend -- the amendment to the credit agreement basically sets the stage for that. Under a breach of covenant, a dividend can't be paid out if it exceeds the last 12 months of free cash flow. Bank creditors would generally not have any interest in taking over a media/entertainment company or bringing about a bankruptcy that would reduce their prospects of being fully repaid, particularly when the headwinds are temporary.

However, even in the case that a waiver is obtained, it's certainly plausible that the stock price could drop even further, e.g. to less than C$1/share. It might get there anyways, until leverage peaks and starts to decline again. My guess is that net debt to segment profit could reach about 4.2x, if F2023Q3 and F2023Q4 segment profit are down by a similar amount as Q1 and Q2. It's tricky to gauge what the market is already anticipating.

Also, despite the shareholder-friendly allocation of capital over the years, Corus has clearly had a hard time shaking off the stigma against having a core business in secular decline. Every time there are macro headwinds, these will get conflated with fears around sectoral issues. This is something to keep in mind when thinking about a price target and holding period.

Final Words

Although the situation with leverage and the covenant warrants caution, periods of temporary macro headwinds and heightened pessimism have often turned out to be fortuitous entry points for future returns. Keeping in mind that a recovery might take several quarters, the pullback of Corus' stock price to a level previously only seen in the March 2020 onset of the pandemic arguably looks like such an occasion.

Corus' situation does not look as precarious as the stock price performance would imply. A significant deterioration in the macroeconomic scenario could, of course, further impact business conditions, but there is a lot of fear that's already priced in. Meanwhile, supply chain woes and inflation have been easing, which should eventually benefit the macroeconomic outlook, more broadly.

Let me know your comments and feedback on Corus.

For further details see:

Corus Entertainment: Macro Headwinds Provide Entry Point