UNP - CPKC: There Won't Be A Better Railway Opportunity

2023-08-07 14:40:53 ET

Summary

- CPKC's management has revised their growth guidance upwards, indicating a significant opportunity from integrating its network with KC's, despite challenges in gauging the magnitude of the opportunity.

- CPKC's merger with KC was approved under less stringent rules, as both are the smallest Class I railway operators and would remain so after the merger, creating a unique acquisition opportunity.

- CPKC is considered a strong investment due to its understandable performance drivers, all-weather financials, sustainable competitive advantages, clear runway to 10-15%+ EPS growth, and reasonable valuation.

We recently had our first in-depth look at the opportunities ahead of CPKC at the company's investor day presentation.

While it has always been clear that CP would stand to gain from integrating its network with KC's, management itself admitted that gauging the opportunity's magnitude remains difficult, but I expect the upward growth revision they presented for the event not to be the last.

Although more expensive than its peers, I see the premium as justified given the growth forecasts now that CPKC represents the best opportunity in rail.

Why The Opportunity Exists

To obtain regulatory approval, any other acquisition between CPKC's Class I competitors would need to increase the competition in order to satisfy the Surface Transportation Board (regulatory agency).

Instead of this requirement, the STB applied an older and less stringent version of its merger procedure rules to CP/KC; the companies only had to show that competition would not be reduced ( source ).

While I'm not saying that this will be the last acquisition in rail, the pool of non-Class 1 targets for CPKC's competitors is composed of much smaller players such that I don't expect us to see a merger that adds as significant value to the acquirer's network as it will for CP and KCS.

Why CPKC Is A Good Pick

The criteria below both concern CPKC as a company and a security; if satisfied, they establish not only why/how it is a good company, but if those qualities translate into an attractive equity investment opportunity:

- Understandable Performance Drivers

- All Weather Financials

- Clear and Sustainable Competitive Advantage

- Wealth Creator

- Factors enabling 10-15%+ EPS growth

- Reasonable Valuation

Understandable Performance Drivers

It's hard to beat railroad companies in understandability, and while this quality is not exclusive to CPKC among its peers, it doesn't need to be. This criterion is just a starting point; whether or not we should have any confidence in our assessment of CPKC or whether our conclusion is built on shaky ground.

Beyond the short-term visibility of weekly volume data releases, rail operators' quarterly and annual disclosures include a wide range of metrics helpful in evaluating the railroads' efficiency, asset utilization/productivity, profitability, and unit economics.

Below is a non-exhaustive list of KPIs, some provided by the company, others which can be calculated with disclosed data. You'll see them categorized by how I personally used them in my model referenced later.

Company Filings (formatted by author)

All Weather Financials

Beyond the nitty-gritty KPIs, railroads are a GDP-plus industry, such that excluding market share changes, growth is dependent on the economic health of the territory on which they operate. According to the U.S. Department of Transportation , rail accounted for ~29% of the ton miles of shipment in 2020 (approximation including intermodal).

As Warren Buffett commented following Berkshire Hathaway's ( BRK.B ) acquisition of Burlington Northern: "[...] it's an all-in wager on the economic future of the United States."

While CPKC's territory goes beyond only the U.S., the same principle applies. As long as its underlying economies continue to have healthy trade flow, CPKC should perform well on an absolute basis.

Yet in periods of economic deceleration, we also want the top-line to be as resilient as possible. On a relative basis, CP's has been more resilient than its peers, in part due to a shipment mix more heavy on resilient commodities/ products such as grain:

Since there's no absolute protection from earnings fluctuating, to have all weather financials also requires that CPKC would be able to meet financial obligations through downturns.

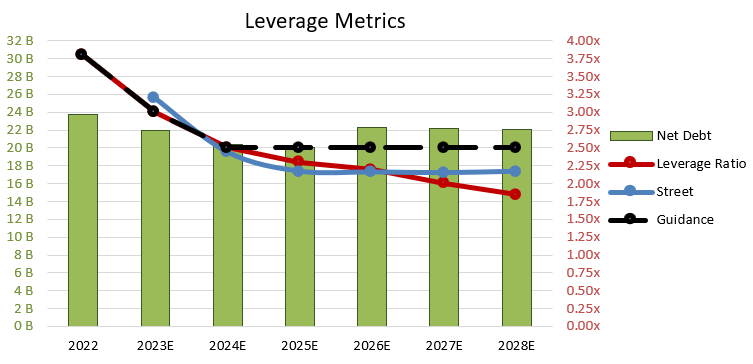

Net Debt to EBITDA (the metric management uses to guide leverage) is historically high for CPKC on both absolute and peer-relative terms, and CPKC's recently-issued 2.5x long-term target would still be at the top of CP's and its peers' historical range:

Given that a 2.5x leverage target in 2028 would imply a significantly rising outstanding debt balance with little reinvestment opportunity, I forecasted flat-ish outstanding debt from '26-'28.

Recalling the historical leverage graph from above, CPKC would still find itself well within it and its peers' historical range. To be clear, the debt and leverage forecasts below are mine:

{kind=link}

Company Filings and Author Estimates

With a clear path to deleveraging, significant cash flow generation, and top-line cyclicality below peers, I consider this criterion satisfied.

While CPKC is undoubtedly exposed to cyclical factors, I don't assume the All Weather criterion to de facto exclude such companies. In fact, it can be hard finding many Industrial companies not exposed to cyclical trends.

Instead, I'm satisfied if its business quality does not risk degradation as a result of cyclical sensitivity (think of CPKC being highly leveraged and, to avoid financial hardship, needing to reduce investments in its network, aggressively cost cut, or reduce important growth programs in a way that would damage their long-term competitive positioning).

Clear and Sustainable Competitive Advantage

This is the criterion most fundamentally altered post-CP/KCS combination. Many relevant aspects were covered during the investor day so I'll attempt to summarize the most relevant points.

GHG Emissions

Management has confirmed the not-surprising fact that the GHG footprint of their service has a material effect on customers' logistics choices. The importance of this factor should only increase going forward.

Compared to trucking, management claims that the GHG emissions are reduced by a factor of 60-75%.

Relative to competing railroad operators, CPKC has been working towards integrating hydrogen-fueled locomotives into its network. While still in its early stages, the program is set to put at least two low-HP locomotives in operation by YE23 (from Investor Day 2023).

CPKC has also solidified this program's promise by partnering with CSX on the development of additional hydrogen-powered locomotives.

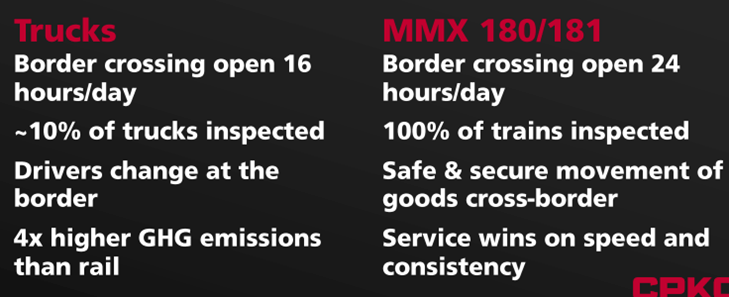

U.S./Mexico Border Crossing

Truck shipments crossing the U.S./Mexico border face many obstacles that are not applicable to CPKC's new MMX 180/181 direct rail line between San Luis Potosi and Chicago (latest investor day) :

{kind=link}

Investor Day 2023

To capitalize on this network advantage, CPKC is in the process of doubling frequency capacity by twinning the Laredo bridge, over which their cross-border rail traffic circulates, and expanding its nearby yard.

We are already seeing concrete signs of the route's value as CPKC has signed logistics operators Knight & Swift and Schneider as the first MMX 180/181 customers on their first day of combined operations. These contracts represent $100mm of incremental revenue.

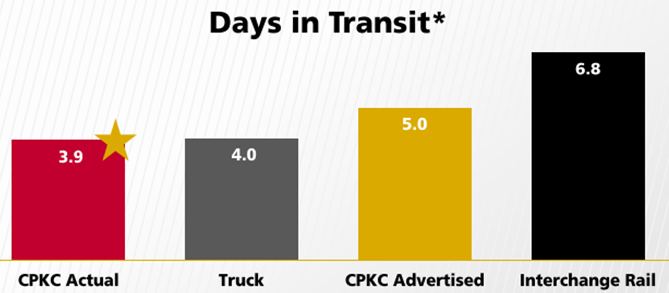

The speed of the MMX 180/181 was also shown relative to trucking and interchange rail (whereby one rail operator would have off the freight to another operator at a connection point to complete the route) all for the same travel between San Luis Potosi and Chicago:

{kind=link}

Investor Day 2023

The bottom-line is that the advantage of their unique cross-border route is clear, but we'll also discuss in a later section how connecting their operations to this new territory creates a lot of incremental investment opportunities at high incremental returns.

Refrigerated Freight

No refrigerated intermodal shipment had ever been transported on rail through the U.S. Mexico border, a clear competitive disruption opportunity for CPKC.

Through a partnership with Americold , the largest publicly traded refrigerated warehousing REIT with more that 20 locations worldwide, CPKC will jointly invest in infrastructure assets increasing their ability to capitalize on an untapped market and make refrigerated freight transport more efficient.

The company claims that trucking transport of refrigerated goods involves a cumbersome border inspection process, trucks possibly stopped for days without warnings and high transportation costs.

The alternative is not only a faster but more reliable service.

During the investor day, management also hinted at the fact that, since Americold is also partnered with DP World which owns many marine terminals in Vancouver and Montreal, a pathway for refrigerated intermodal freight being transported exclusively on CPKC's network exists.

Seaborne Intermodal

Lazaro Cardenas, a port in Mexico, represents a key strategic opportunity for CPKC management. Currently underutilized, they believe that it could represent a solution to the Southwestern U.S. ports being at capacity.

Now connected to their Canada/U.S./Mexico network, shipping goods to this port instead would represent, for example, a 10-14 days shorter alternative than ships going through the Panama Canal to reach Houston.

Management mentioned during their investor day presentation that running a single daily train out of Lazaro Cardenas represented an incremental $200mm revenue opportunity.

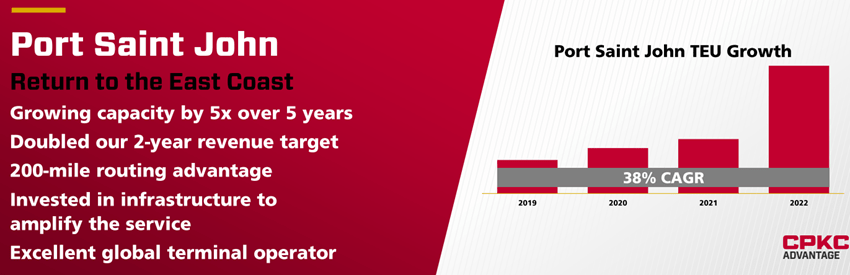

Another investment opportunity exists at the opposite end of their network in Saint-John. Increased investment in capacity would enable more opportunities for market share capture from other modes of transport through direct-to-rail volume but also relative to CN (referenced below as the network compared to which they have a 200-mile shorter route):

{kind=link}

Investor Day 2023

Wealth Creator

This criterion is not only being profitable, it's about also being able to reinvest profits at high incremental returns.

Maintenance CAPEX needs of the industry are low relative to total assets, fueling significant FCF generation, yet structural industry features prevent significant growth plowbacks and make it difficult for rail operators to compound capital fast.

In CPKC's case, I believe the merger has temporarily broken this rule and created significant reinvestment opportunities at high incremental margins.

The first opportunity is bringing KCS's network state up to CP's standard. The comment was made during the investor day that a lack of investment in KCS' network has made it difficult to run Precision Schedule Railroading ("PSR") truly effectively as the maximum train length is limited by the state of its network.

Why does PSR matter? Much of the value created in the rail industry over the past decade has to be credited to its widespread adoption and it enabling asset and personnel productivity increases. You can read more on the operational facets of PSR here .

While most other Class I railroads have maximized PSR efficiencies and are looking to the automation of inspection or crews as the next step in margin expansion, CPKC now has more room to improve through KCS.

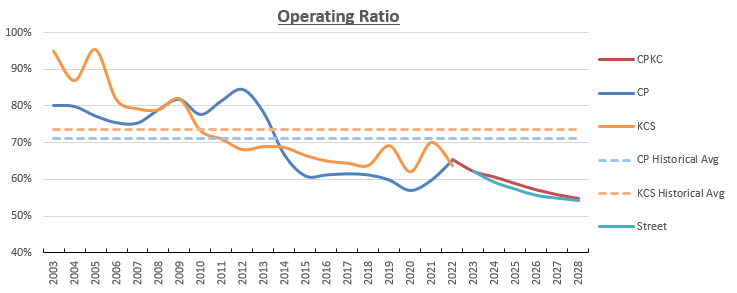

The difference is visible in the progression of their operating ratio, a metric used in railroading that simply represents operating costs as a percentage of revenues:

{kind=link}

Company Filings and Author Forecast

While KCS's ~5% higher ratio may not seem that significant, 5% of CPKC's consolidated 2022 revenue represents 15% of its operating income.

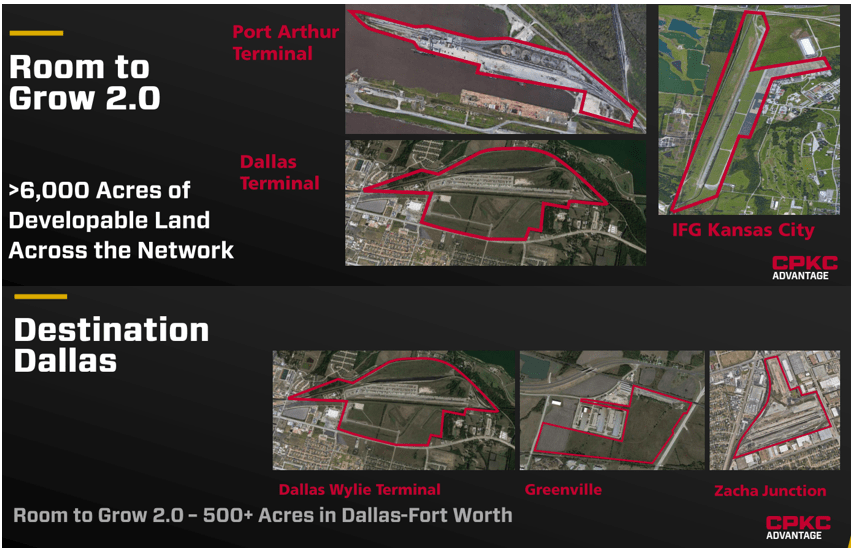

In addition to PSR maximization, CPKC has significant capacity investment opportunities which should generate high incremental returns.

For example, the company showed the following slides during the investor day to highlight possible avenues of investment around its network to meet the demand:

{kind=link}

Incremental Investment Opportunities (Investor Day 2023)

These opportunities also include the Americold facilities discussed above, another point of competitive differentiation for CPKC.

Factors Enabling 10-15%+ EPS Growth

This one is a pretty easy checked box. Given company guidance of doubling EPS from 2023-2028 and double-digit EPS CAGR over the same period, we have clear guidance of 15%+ EPS CAGR over the next 5 years.

My forecast lands at 17.7% CAGR versus analyst expectations I gathered of 17.4%; all very close.

The assumptions I explore below are the main factors driving EPS, but are not the only way to interpret or forecast CPKC's performance. Therefore, I recommend paying more attention to the underlying drivers of these assumptions and not the number themselves in evaluating if you agree with my conclusions or not.

Revenue Growth

- Guide: HSD

- My Forecast: 7.81%

Forecasted through the combination of volume (RTM) and pricing (Rev/RTM) per shipment category, as seen below, along with CP and KCS historical growth for each as reference:

Company Filings and Author Forecasts

The aggregate 5y top-line growth is close to evenly split between volume and pricing.

The source of volume growth is driven by market share gains from both rail and alternative transport modes.

Pricing growth is a GDP-plus-plus that is in line with historical but slightly higher as I attribute a certain premium/unique service pricing lift.

Revenue Forecast Delta vs. Street (Author Forecast)

Relative to analyst forecasts, I am over on pricing and under on volume, and while overall close on total revenue, I front-load more of my growth. As management does not guide long term volume or pricing targets, and I am well within the HSD revenue CAGR guide, I'm confident in this output.

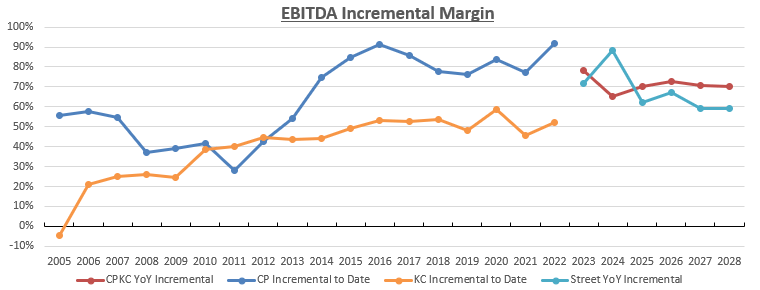

Margins

- Guide: 60-70% EBITDA Incremental Margin

- My Forecast: ~71% Incremental FY23-28 (Cumulative)

This incremental margin is not out of historical norms when looking at the cumulative incremental going back to 2005 (e.g. 2022 data point is Incremental EBITDA/Incremental Revenue from 2005 to 2022):

{kind=link}

Company Filings and Author Forecasts

Repurchases

- Guide: Return to Repurchases

- My Forecast: -4% Shares Outstanding CAGR FY23-28

Repurchases Schedule (Author Forecast)

This was forecasted indirectly given CPKC's guidance for 90% free cash conversion from net income, assuming that all FCF not used for debt repayment goes to repurchases (targeting a leverage ratio presented graphically earlier), and growing the average repurchase price 13% Y/Y from today's price to remain conservative.

Reasonable Valuation

We're concerned here with whether the current valuation entails a relatively low risk of multiple compression that protects the upside to be generated in earnings growth.

If we look below at the forward P/E ratios for CPKC and its peers, it is more expensive than them by a meaningful margin.

To put this multiple in clearer context, the graph below shows that while the relative premium of CP relative to its peers is historically wide, it has on average traded at a premium to them:

Historical Valuation Premium ((Author formatting))

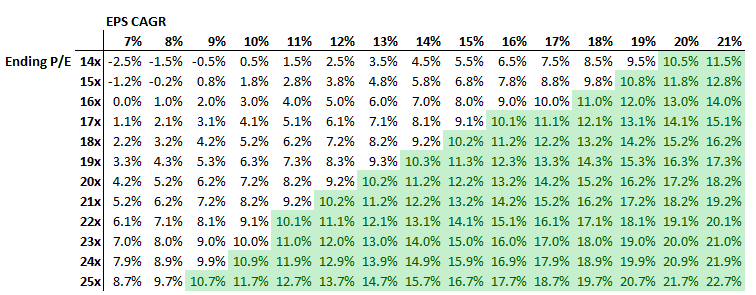

To justify my confidence in the current valuation, I conducted a brief sensitivity analysis below.

Assuming that over a period of 5 years, EPS grows at the rate on the top of the table and converges from a 23x starting point to the multiple on the left of the table, it implies a stock return CAGR at their intersection:

{kind=link}

Analyst sensitivity analysis

For example, assuming that CPKC grows its EPS at 15% over the next 5 years and its forward earnings multiple settles at 17x (close to the S&P 500's historical average), we would have returns of 9.1% annually.

This is a conservative estimate on both inputs. We are assuming a multiple well below its historical average despite better-than-historical market position and growth above its peers'. We are also assuming EPS growth at the low end of guidance.

Therefore, I am confident that CPKC's equity price will be able to grow at an above-market rate of 10%+.

Risks

While management clearly laid out its expectations, they were clear that many new ventures (ex. MMX 180/181 or cross-border refrigerated intermodal transport) are in uncharted territory.

While this could imply upside form current expectations, it could also lead to an overestimation of demand from shippers.

Otherwise, CPKC's Mexico network advantage could be slightly reduced by the STB if it rules that it must engage in reciprocal switching ( as it has been seriously considering ), a process already in place in Canada but know as interswitching.

Under such regulation, routes now solely served by CPKC (such as many coming from Mexico) would face serious competition as they would be forced to hand-off freight to nearby rail operators at interchanges, limiting the benefits to be drawn from CPKC's unique continuous network.

While all Class I operators came out against this proposition, CPKC CEO Keith Creel commented on the matter during the investor day:

I think a lot of customers, especially over the last several years have learned, sometimes the lowest rate is not the best decision

He implies that CPKC's superior service relative to potential switching partners would limit business loss and protect some pricing upside.

Nonetheless, this forced switching would, all else equal, be a drag on CPKC's growth.

For more on reciprocal switching, I suggest reading this informative primer .

Conclusion

CPKC is creating a one-of-a-kind integrated network which I expect to create incremental value not nearly replicable by its peers.

Despite a pricey valuation relative to historical levels and its peers, CPKC's operational advantage in many areas over its peers should command a premium that provides a certain cushion to investors as it contracts over the next years and the company begins to deliver to top-line and cost opportunities.

As such, I believe CPKC presents a resilient and attractive opportunity with solid idiosyncratic growth drivers.

For further details see:

CPKC: There Won't Be A Better Railway Opportunity