CSGKF - Credit Suisse's Earnings Weren't Brilliant But It's Unlikely To Go Under

Summary

- Credit Suisse Group AG reported a huge net loss for 3Q2022.

- The bank announced a full-scale restructuring program.

- The Swiss bank's stock plunged to muti-year lows after the results were announced.

- It is highly there will be a recession soon enough.

- The bank is in a risky situation. But it seems to me the market is far too pessimistic about Credit Suisse stock.

Credit Suisse Group AG ( CS ) reported an enormous net loss and announced a restructuring plan . It sounds really scary on the surface. But let us dig somewhat deeper. As I mentioned before in my previous article on Credit Suisse , restructuring does not mean liquidation. The company also announced its quarterly earnings results, and these were not as horrible as they looked.

Do not get me wrong. I understand Credit Suisse is not going through its best days, but the whole situation still does not look like the Lehman Brothers crash. Let me explain this in some more detail.

Credit Suisse's 3Q earnings

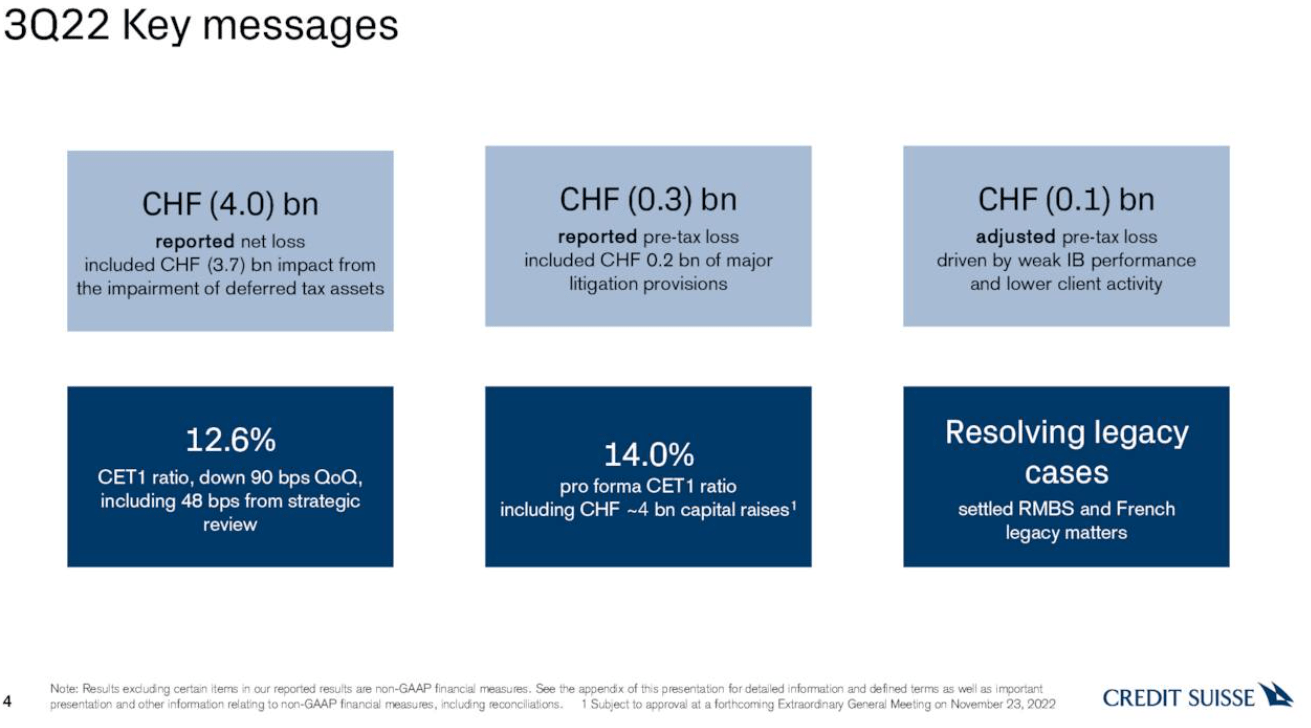

It could be said that Credit Suisse's reported net loss of CHF 4 bn was much worse than many analysts had expected. At the same time, CHF 3.7 bn of the net loss was due to the impact of the impairment of deferred tax assets. These were all due to the bank's strategic review. The rest of the loss was partly due to the litigation expenses (CHF 0.2 bn) and the poor performance of the investment bank (CHF 0.1 bn). Here I would also like to note the bank's litigation expenses were very moderate, compared to the ones reported in the previous quarters.

Another interesting highlight of the reported earnings was the CET1 ratio. Before the CHF 4 bn capital raise, it used to be just 12.6%. But after the capital raise, it totaled 14.0%, a very good result, indeed. However, in order to get CHF 4 bn, the bank had to issue more shares, thus diluting its existing stockholders. But this allowed the bank to boost its liquidity position, an important step, given the situation.

{kind=link}

Source: Credit Suisse's earnings presentation , slide 4

Also noteworthy was the bank's performance if we see the breakdown of its results according to Credit Suisse's divisions.

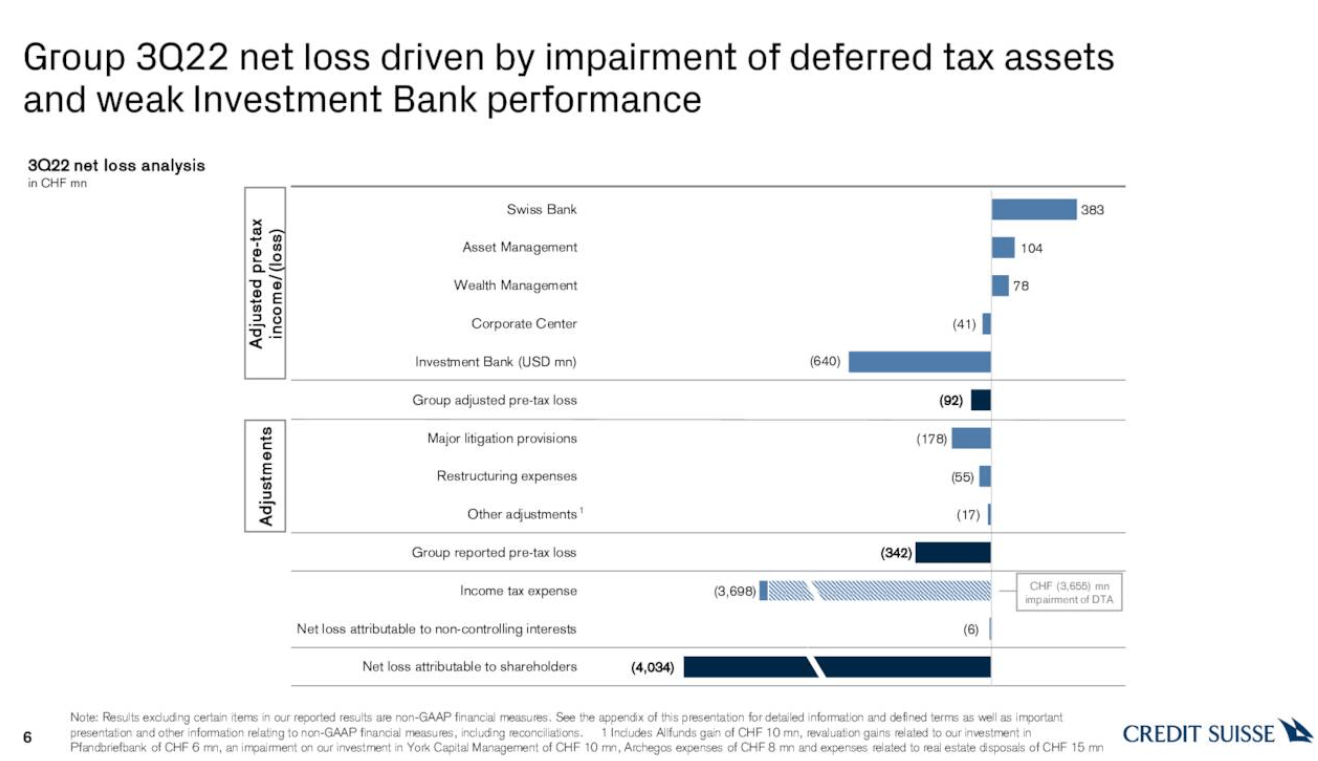

The excerpt from the presentation below shows Credit Suisse's adjusted pre-tax income/loss. The most successful department was the Swiss bank. It has been traditionally the best-performing division of Credit Suisse for many years. The asset management and the wealth management departments also demonstrated sound performance results. The outsider was, obviously, the investment bank division that reported $640 mln in losses. The good news is that Credit Suisse is transforming and selling this division to focus on better-performing businesses. It was due to the investment bank that Credit Suisse reported a pre-tax loss of CHF 342 mln. In fact, without the investment bank, the bank's pre-tax profit would have been a positive CHF 298 mln.

{kind=link}

Source: Credit Suisse's earnings presentation, slide 6

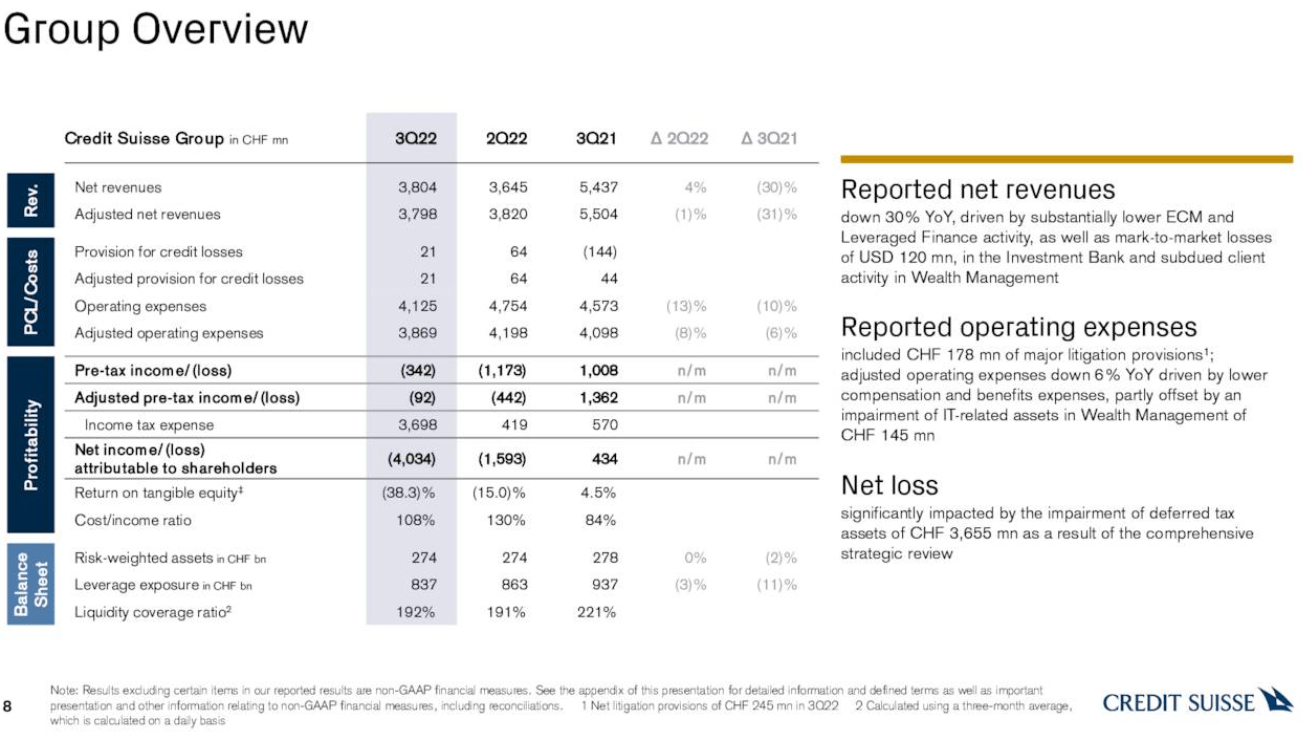

If we look at the earnings overview and compare the recently reported results to the ones reported for 2Q 2022, we will see Credit Suisse's operating indicators did not get much worse, indeed. This is especially true of the operating expenses reported for 3Q 2022. Due to the low revenues, the management decided to cut its pay and other financial benefits to the bank's employees. This was the main reason for the lower costs.

{kind=link}

Source: Credit Suisse's earnings presentation, slide 8

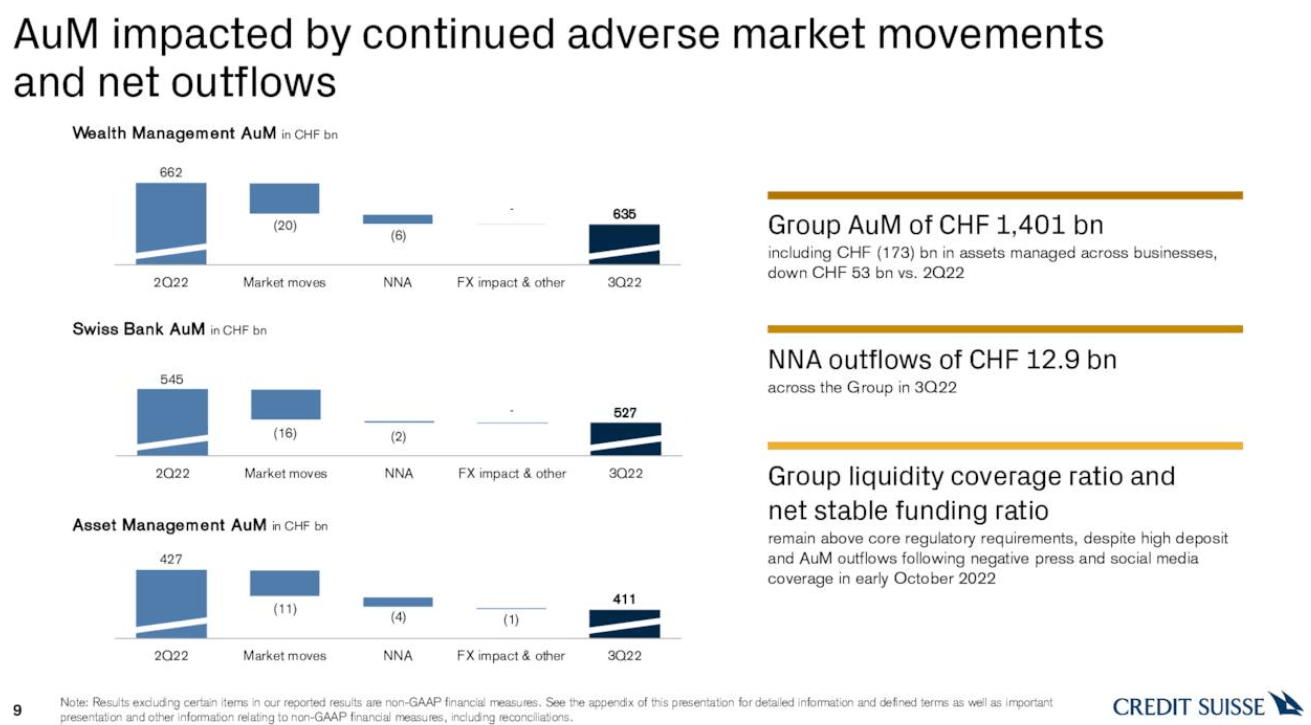

The recent several quarters were also problematic in terms of money outflows. But the negative coverage in the press about Credit Suisse in the recent month or so also made some investors panic.

So, the Group's assets under management ("AuM") totaled CHF 1,401 bn for the 3Q 2022. These decreased by CHF 53 bn compared to 2Q 2022. The outflows, meanwhile, totaled CHF 12.9 bn. So, we can assume the bank's AuM fell mostly due to investors' unwillingness to open new accounts at Credit Suisse. But not many people started panicking whilst taking money out of the bank, which is also a positive given the situation. As I have mentioned before, the liquidity level also remained tolerable and even improved after the bank's capital raise.

{kind=link}

Source: Credit Suisse's earnings presentation, slide 9

The restructuring plan

I would also like to say a couple of words about the bank's restructuring plan. It seems the process will be long, but it leaves investors some hope. After all, the bank has already boosted its liquidity by issuing shares and is going to cut costs by 15% in the long run.

By issuing more shares, the bank will obviously dilute its existing shareholders, which is bearish for the stock price. However, the good news is that a very serious investor, namely Saudi National Bank, is going to invest CHF 1.5 bn in the newly issued shares.

Overall, the bank expects its restructuring charges to total CHF 2.9B from Q4 2022 to 2024. It might sound expensive, but this is the total amount of money CS will pay for reforming its businesses. Credit Suisse's cost base is expected to decrease by around CHF 2.5 bn to total CHF 14.5 bn per year in 2025.

In order to achieve that, the bank will cut 2,700 full-time jobs, or 5% of its employees, in Q4 2022. By the end of 2025, CS expects to cut its jobs by 6,500. So, the bank's workforce would fall to around 43,000, down from 52,000 at the end of Q3 2022.

There were also some important steps really aimed at de-risking Credit Suisse's business. Amongst them was the bank's decision to transfer a majority of the Securitized Products Group to an investor group led by Apollo Global Management (NYSE: APO ). This is good for CS, since trading securitized products is very risky during the recession. And there will highly likely be one soon. So, the more conservative the bank's business is, the better it is.

The management also decided to split the investment bank into three units, namely, the markets, the CS First Boston (centered around capital markets and advisory activities), as well as a capital release unit.

The markets business will be about trading equities, foreign currencies, and other assets. It will also closely cooperate with Credit Suisse's wealth management and Swiss bank franchises.

CS First Boston will be responsible for attracting third-party capital.

The capital release unit will comprise of securitized products group and a non-core unit.

There are also rumors CS First Boston will merge with M Klein & Company, which, if it happens, will be a positive for Credit Suisse since this will allow the bank to raise cash.

Risks

Credit Suisse has been recording losses for a while. What is more, it operates in an industry that is highly cyclical. The recent economic news also inspires fear. Central banks all over the world are hiking interest rates in order to fight inflation. The Fed is particularly hawkish here. At the same time, regions around the world are experiencing their own pains. This can be said about the U.S., China, and Europe. But particularly worrying seems to be the situation with the Bank of England. It had to substantially intervene in the bond market in order to prevent the financial market collapse and therefore a very serious recession.

Apart from the problems the bank itself is experiencing, there are more than enough external threats. However, Credit Suisse is the second-largest Swiss bank that seems to be " too big to fail. " In other words, if a major crisis happens, the Swiss government will highly likely intervene in order to save CS.

Valuations

Credit Suisse's valuations are astonishingly low. Straight after the publication of the results, the bank's stock lost almost 20% over one trading session.

What is more, the stock price is near its all-time low. It looks like the stock market expects the bank's liquidation. But for the reasons, I have mentioned before, and also based on what S&P Global is saying , this is unlikely to happen.

In order to judge how undervalued Credit Suisse is, I decided not to use the P/E (price-to-earnings) ratio since the bank is loss-making at the moment. That is why I limited Credit Suisse's valuation to the P/B (price-to-book) measure.

According to the P/B indicator, CS stock is extremely cheap. A reasonable P/B ratio for a bank is 1 . But 0.23, the indicator given by Y-Charts as of the time of writing, is extremely low.

So, we can say the valuations fully take all the risks into account.

Conclusion

Credit Suisse is a problematic bank that has been facing serious pressure since 2021. It is still not entirely clear how successful the restructuring process will be. And yet, in my view, the pain the bank is experiencing is somewhat exaggerated by the financial media. It is highly unlikely the bank will be allowed to go bankrupt thanks to its significance for the Swiss economy. At the same time, the record-low valuations fully reflect the bank is not going through the best of times.

For further details see:

Credit Suisse's Earnings Weren't Brilliant But It's Unlikely To Go Under