CA - Crescent Point Energy: Built For The Long Run

Summary

- CPG is paying 50% of Excess Cash to shareholders, and that's growing.

- CPG has cleaned up its balance sheet and has made smart acquisitions which are already paying dividends.

- CPG has a strong hedge book to lock in profits.

Crescent Point Energy (CPG) is returning cash to shareholders at an increasing rate, and it's only going to get better in my view. The company has started to make acquisitions the right way, in areas that are likely only going to increase the returns going forward. I fully expect Crescent Point to ride the wave of the oil & gas curve going forward. I remain bullish on the industry and it appears we are about to enter a period of strength. If you are looking for some exposure, I think Crescent Point is a safe spot to park some cash for the long run.

What's Driving Crescent Point?

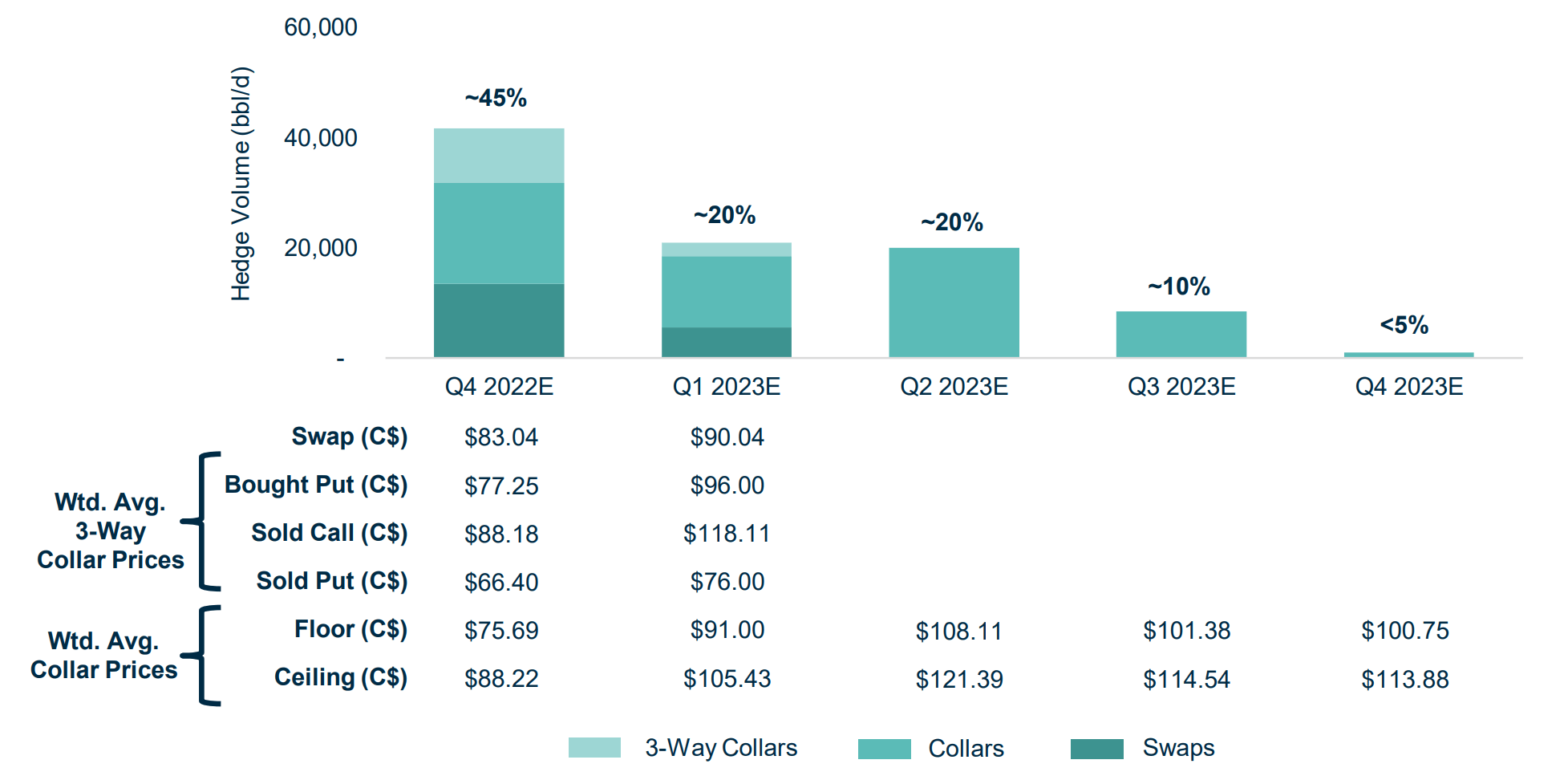

Like all oil & gas companies, right now it's cash flow. Crescent Point has always been a high point of debate given some of their acquisition history and how they go about said acquisitions. But I have to give them credit now for building a solid business with a great cash base that is likely only going to grow. The company has focused on improving its balance sheet and sustainability. Part of that locked-in plan is a strong hedge book. While others are as my Grandma would say "Flying by the seat of their pants" and riding this wave mostly unhedged, Crescent Point is still hedging a good chunk of their production. While I don't love seeing hedges as high as this, it's hard to argue with the results.

{kind=link}

While we will get an update in early March on what the outlook for 2023 is, the most recent update was that they are expecting 138,000 - 142,000 barrels per day with an Excess Cash Flow of $1.25 billion at $80 WTI. But all in all, it's looking to be another fantastic year. The Kaybob Duvernay play has been a major focus for them, and they are continuing to add to their asset base there. The cash flow generation has been massive. The initial investment in 2021 is about to be fully paid off at some point in Q1 2023. Since then, they have made two other investments in the area:

- Q3 2022 acquisition for ~$87MM

- Q4 2022 acquisition for ~$375MM

Both of those were paid for in cash (bonus!) and there's an expectation to grow production to >55,000 barrels per day within 5 years, from ~35,000 barrels per day in 2022 . All in all, there is a lot to like about what is coming down the pipe concerning growth in sustainable plays.

How's That Dividend?

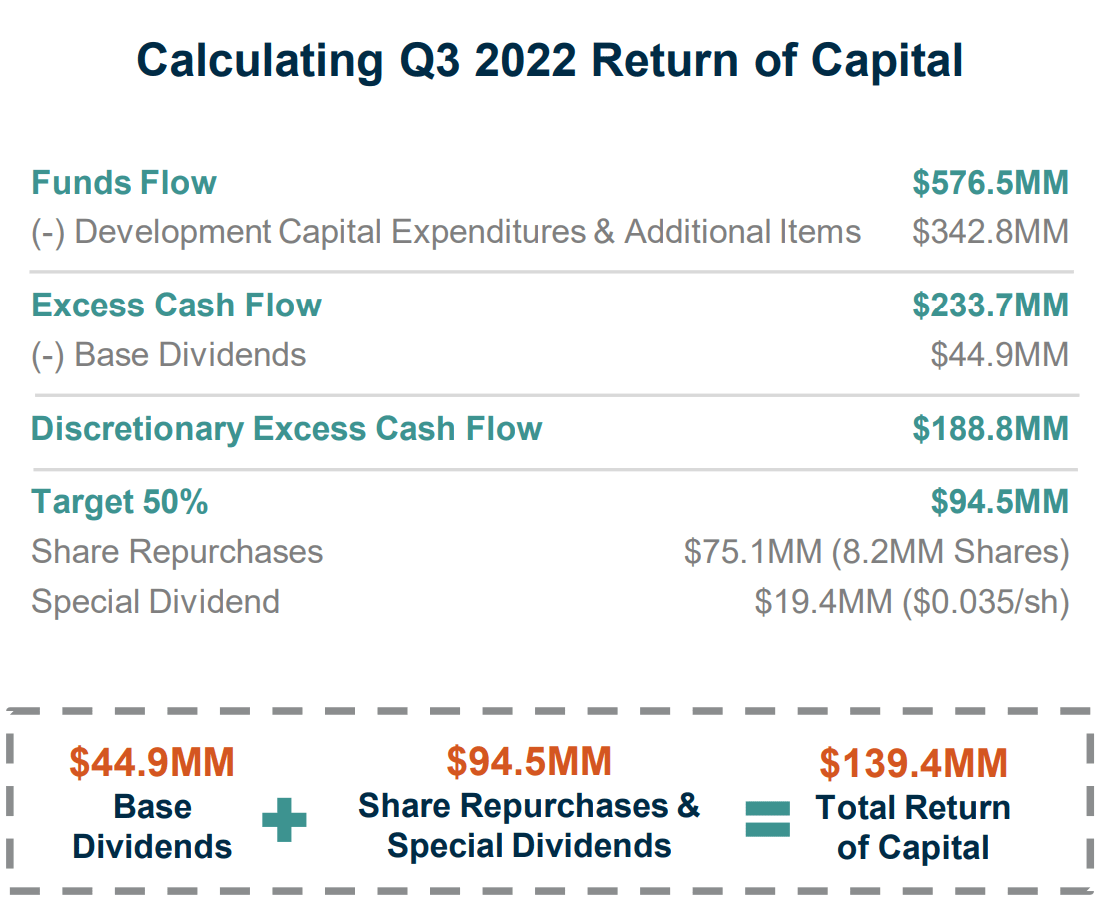

If you like seeing 50%+ of free cash flow being returned to shareholders, then you're loving life... so long as you aren't sitting on shares you bought before 2018 that is. Just so everyone understands where the 50% is coming from, it's 50% of Discretionary Excess Cash Flow. Which is, Funds Flow less Development Capital Expenditures & Additional Items and the Base Dividend. The breakdown of what was paid in Q3 can be seen below. Essentially, for the quarter shareholders are benefiting from $94.5 million, of which $75 million went towards buybacks, and the rest went towards the special dividend. Add that in with the base, and the company returned $139.4 million to shareholders. Not bad!

{kind=link}

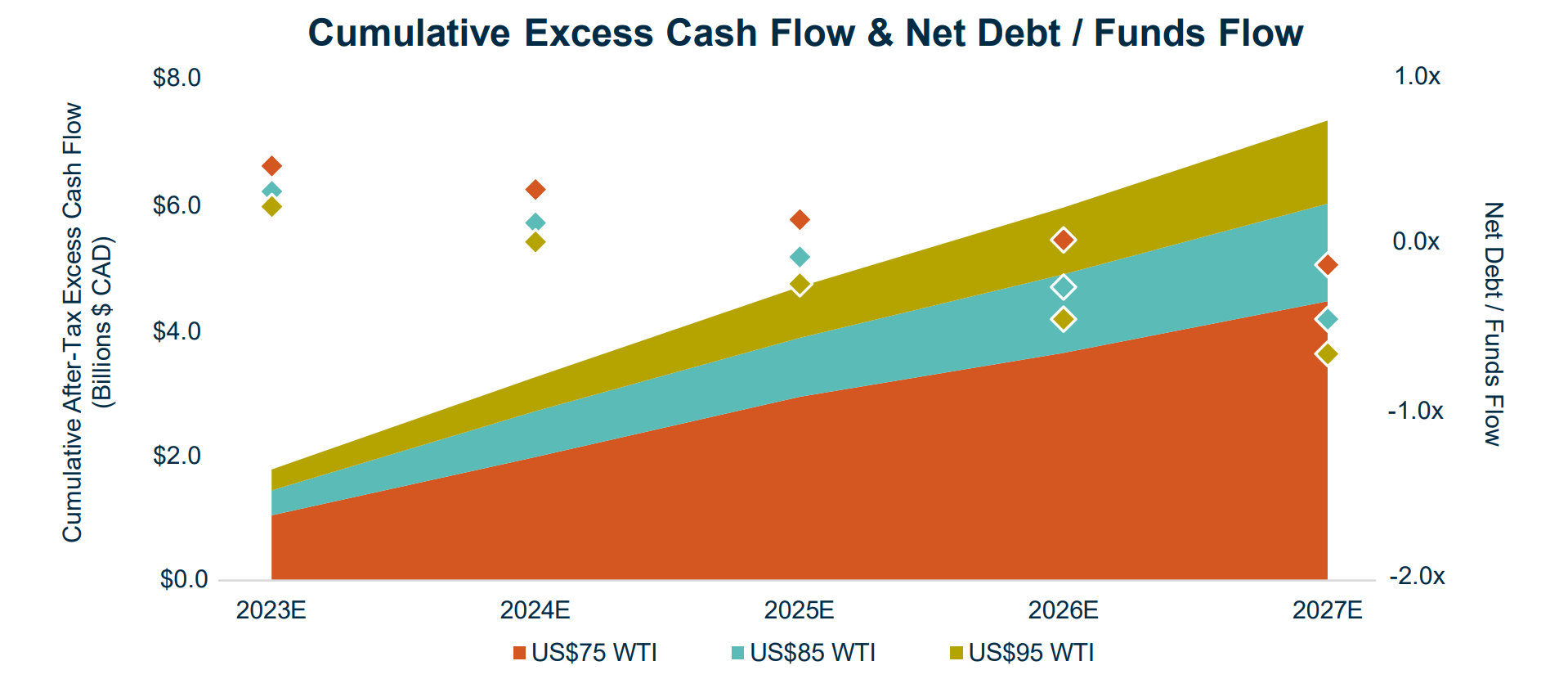

What does this mean for future returns? It means that the returns are only going to grow so long as the price of oil remains stable. Looking below, we can see the growth in Excess Cash Flow over the next few years relative to the price of oil. We can see their expected leverage ratio charted as well. While it's not as easy to read, the important part is that the company, on its current path, will be debt free in 2024 or 2025. But, we all know they will continue to acquire assets and take advantage of the situation they have put themselves in. Let's just hope they keep using cash and don't fall into habits of old and issue stock.

{kind=link}

As for what exactly we can expect for dividends in 2023, estimates are coming in at around $0.43 per share after seeing $0.28 per share in 2022. It's hard to argue with much when the stock is yielding over 4.5%. Crescent Point has always been heavily owned by "retail" and that usually means the stock offers something that appeals to most people. A quality dividend, and exposure to an industry they may not have exposure to otherwise. Looking below, you can see that almost 65% of the float is owned by the general public. There's a good chance that a large number of those shareholders are long-term, and are still quite underwater from the days this stock was worth over $30. Never hurts to understand who might be on your side of a given trade.

{kind=link}

What Does The Price Say?

Crescent Point has been undervalued for years, and that theme remains true today. As I've mentioned, one of the issues is the trust in management to not issue stock in any acquisition which has hampered the stock in the past. The rest is solely due to the industry in which they play in.... but if you know me, I am a huge oil bull, so I think there's definitely money to be made here.

Looking below, we see that this should be a $10 stock based on future cash flows. This is more true than ever with the cash that Crescent Point is pulling in, and returning to shareholders. Getting to $10 would lead us to about a 50% return from current levels, which isn't so bad.

{kind=link}

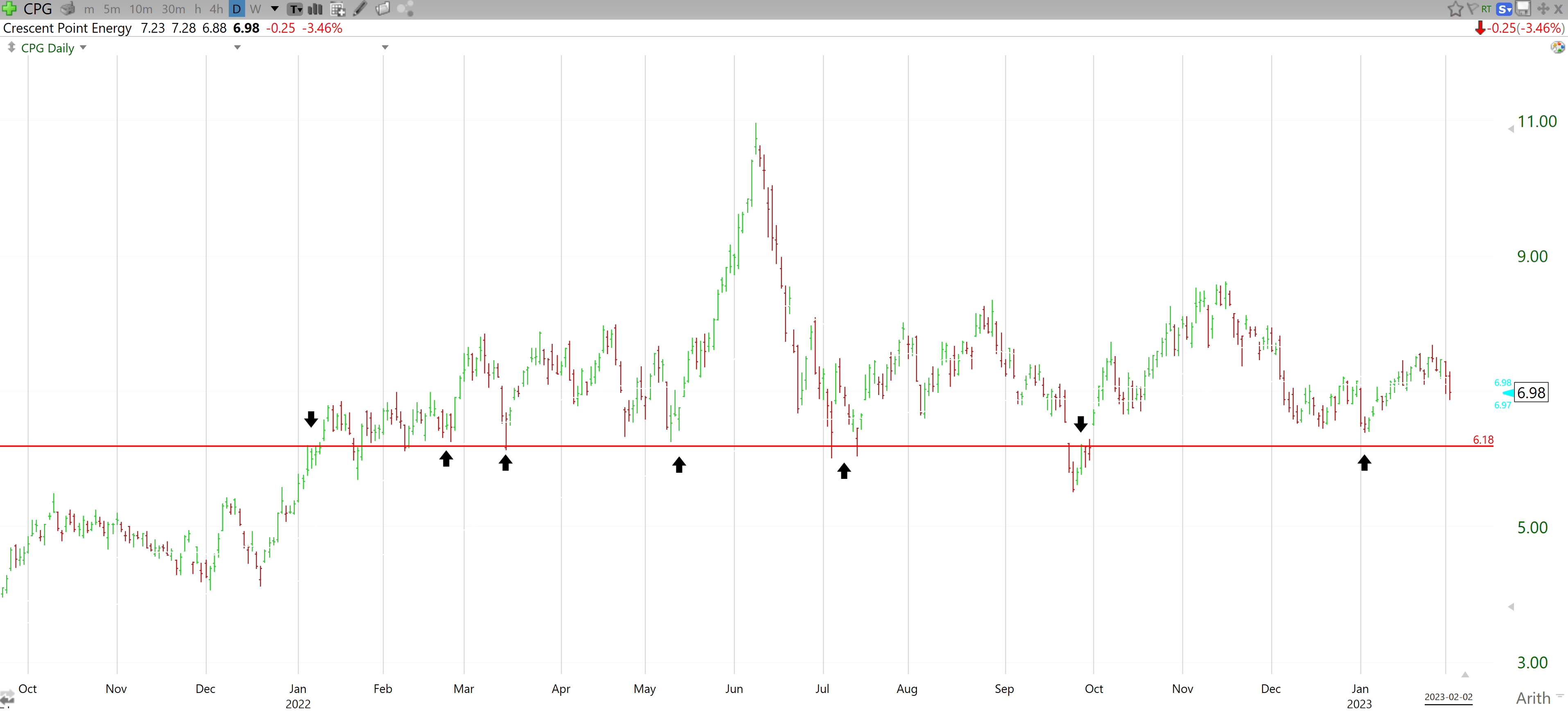

As for the technicals, we are at a point where we can afford to take on some risk. The main reason for this is that the stop would have to be on any current entry. I would have my stop right around $6.18 which is about 11% from current levels. Looking below we can see a pretty firm line in the sand. Owning the stock below $6.18 is risky business and not something I'd be looking to explore in this current market.

{kind=link}

As you can see from the chart, we really have been range bound outside of the pump last summer. This does make it really easy to chart, which means setting goals and targets is a breeze. Below, we can see my first target is $7.75, followed by $8.62. The importance here is cracking through recent highs. If we fail at either of these, it would be a sign that we could be stuck in the current range for a bit longer. Which isn't great, but given the dividend and the planned cash return, there are worse spaces to be.

{kind=link}

The last chart I will leave with you here is one that supports this range theory. Looking at the industry as a whole, we are nearing the end of the down-to-flat season as we enter February. Turnaround season is upon us and historically, oil stocks have done quite well from late February through October. Let the fun begin!

{kind=link}

Wrap-Up

As you can see, there is a lot to like about what Crescent Point is doing. The company is making smarter acquisitions and hedging to ensure shareholders will get the returns they have been promised. The balance sheet is clean, and the company is on pace to be debt free in the next two years. The stock has been range bound, and the clear line in the sand makes this investment an easy one to ride out for the long run. I am bullish on oil and bullish on Crescent Point Energy.

For further details see:

Crescent Point Energy: Built For The Long Run