CA - Crescent Point Energy: Management Found Another Bargain With Hammerhead Acquisition

2023-11-08 19:09:56 ET

Summary

- Crescent Point Energy management completed the Hammerhead acquisition to improve company finances and grow more cheaply than organic growth. The value of 2P reserves comes for free.

- Crescent Point Energy faced financial stress due to debt and drop in cash flow when oil prices dropped back in 2015. It's now a far better company.

- Management is prioritizing debt payment and making accretive acquisitions like the Hammerhead acquisition to improve the company's financial situation and future prospects.

- A management that successfully turns around a financially stressed company heading toward the hereafter (fast) is a very rare management.

- Investors should expect the superior results to continue. Technology improvements should make the acquisition an even better deal.

Crescent Point Energy ( CPG ) management is still finding bargains that can improve the company finances and grow the company more cheaply than is the case of organic growth. The Hammerhead acquisition exceeds that goal as management presents this as the acquisition of premium acreage. If management is right, then improvements will continue by simply drilling new wells with better results when cheap acquisitions are no longer available. This differs from companies that buy cheap merchandise while crimping on the quality. It also enhances the original strategy of management focusing on identified core areas.

Why Hammerhead?

Management is obviously focusing upon what they believe to be the best acreage in a known very profitable basin that has made companies money for years.

The bolt-on aspect is "icing on the cake" because it's likely acreage that management knows (which reduces the risk of failure) while the premium aspect should provide superior cash flow during cyclical downcycles. That would lead to a superior stock price as an above average profitable company is more valuable.

{kind=link}

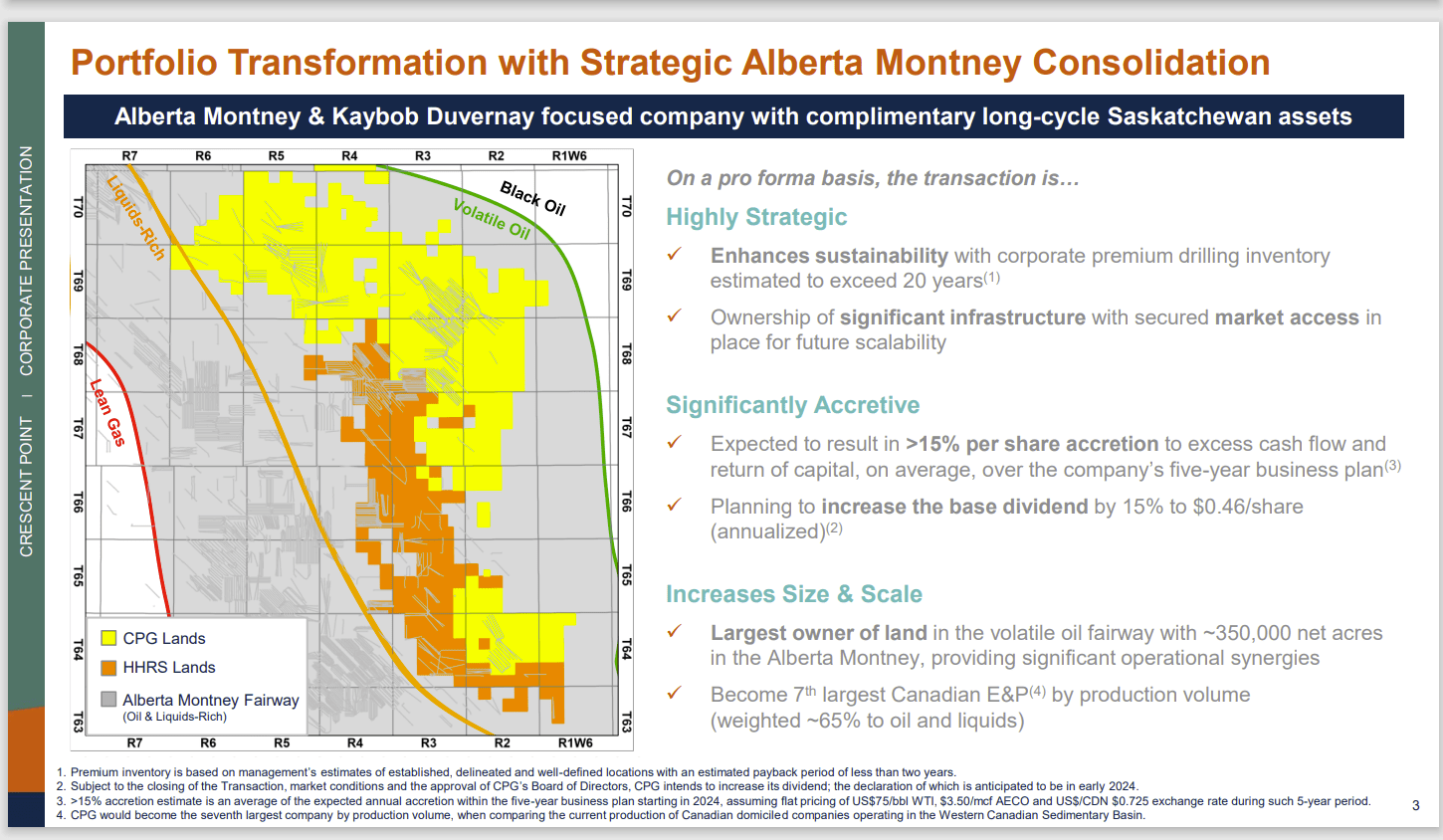

Crescent Point Energy Map Of Proposed Acreage To Be Acquired (Crescent Point Energy November 2023, Acquisition Presentation)

This is a giant bolt-on acquisition (as shown above) that is likely to have similar sized cost-savings opportunities. Combining operations in a situation where the property acquired is "mostly next door" is much easier than running a bunch of detached holdings.

A proposed holding as shown above is going to be far more valuable if marketed at any time because longer more profitable wells can be drilled on the combined property than is the case with two separate owners. This would apply to the boundary areas before the combination. But as shown above, that's a lot of area.

Then there's optimization due to the size of the operation. This type of acquisition in Canada often involves midstream operations that are easily optimized when the properties border on each other. There's also the likelihood of more connections to long haul pipelines that give management more options to get the product to better priced markets.

There's also the bargaining power in transporting and selling more volumes that can help with increasing sales prices while decreasing long-haul midstream costs.

The acquisition also could mean that management anticipates relatively strong commodity prices for some time to come. In this low visibility industry, that view is always a risk. But it's worth noting that this acquisition is a view on the future of oil and natural gas pricing.

It's always hard to tell what any management can do with an acquisition in the future. But this management has long reported well performance improvements along with the capital savings noted (to follow) in the article.

All of this points to a detail oriented, value driven, and very energetic management. None of that is to take away the risks noted before or the price volatility of oil.

It makes the story that management found "premium acreage" believable while not paying much for that "premium." Therefore, some premium location sales proceeds go to the seller. But this is a buyers' market still by most accounts. Therefore, there's likely a lot of value for shareholders in the future if management is correct (which is also a risk of the transaction).

Management Rationale

(This is a Canadian company that reports using Canadian Dollars unless otherwise noted.)

Here is the basis for the bargain:

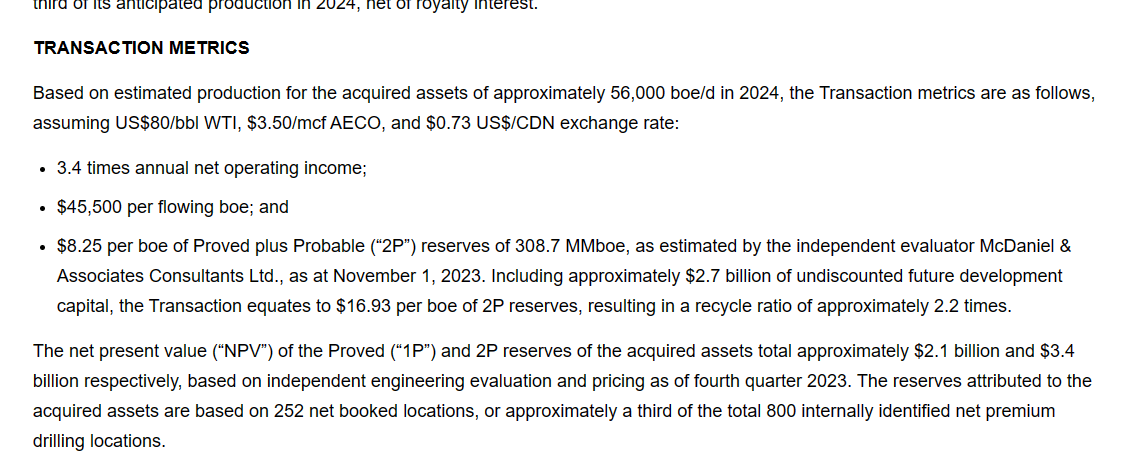

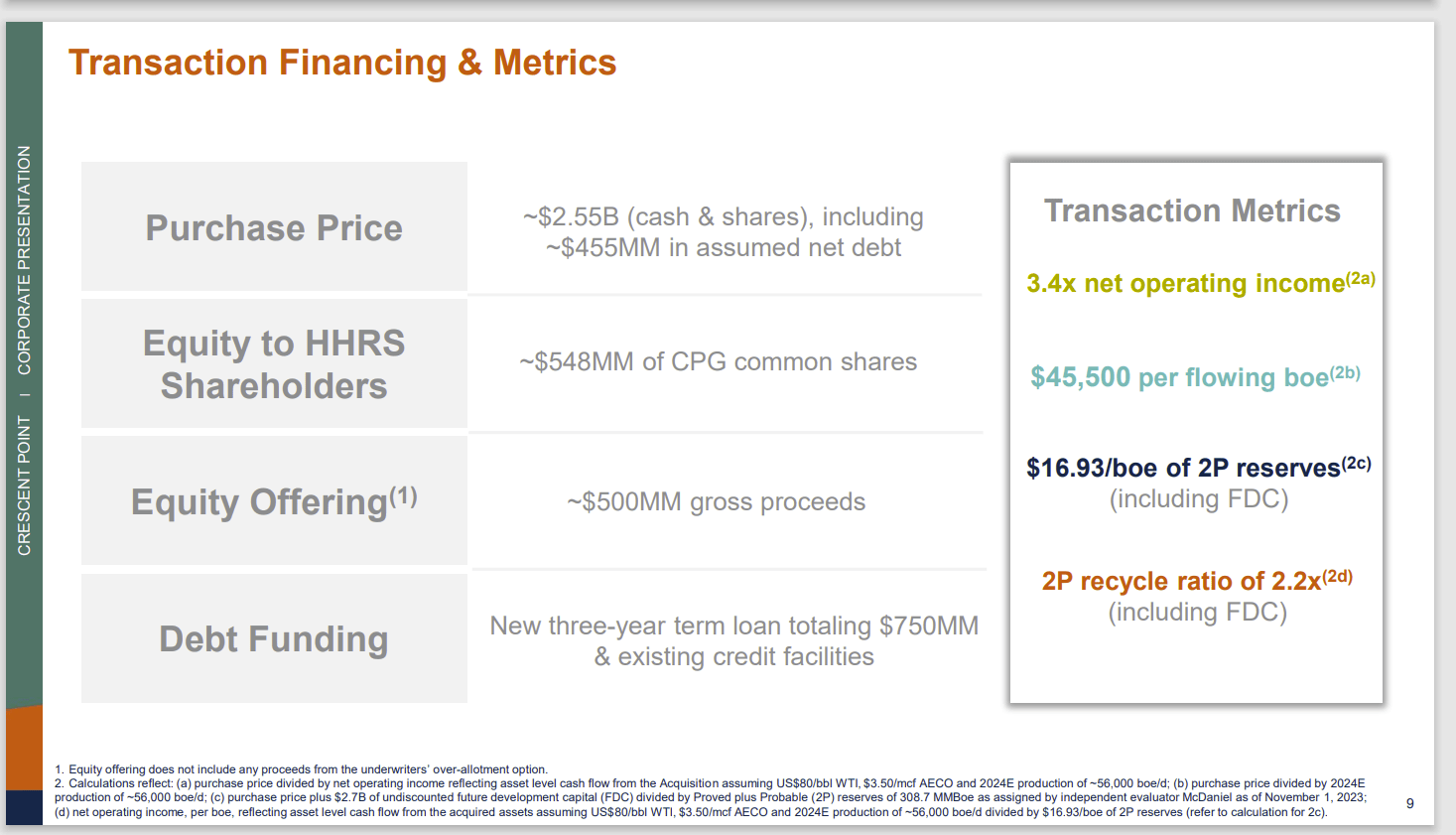

Crescent Point Energy Management Transaction Metrics For Acquisition (Crescent Point Energy Acquisition Announcement November 2023)

{kind=link}

Management calls this the transaction metrics. My accounting background usually directs me to this first even though it's nea r the end of the announcement.

The big deal is the C$2.1 billion of production coming from what's already producing. That leaves roughly C$400 million for infrastructure noted below that management believes is worth C$500 million with absolutely no value of the purchase attached to the 2P reserves which are estimated to net out to a value of C$3.4 billion.

That zero for the $3.4 billion means management is paying nothing ahead of time for additional locations to drill and produce. Those costs already are in the calculation complete with time value of money included as a discount rate in the report to get to that profit. Now that's one heck of a bargain.

Compare to the American companies who often report paying as much as $3 million (US dollars) per location in the Permian. This deal beats almost any Permian deal by a mile and yet it's very typical of good (for shareholders) Canadian deals.

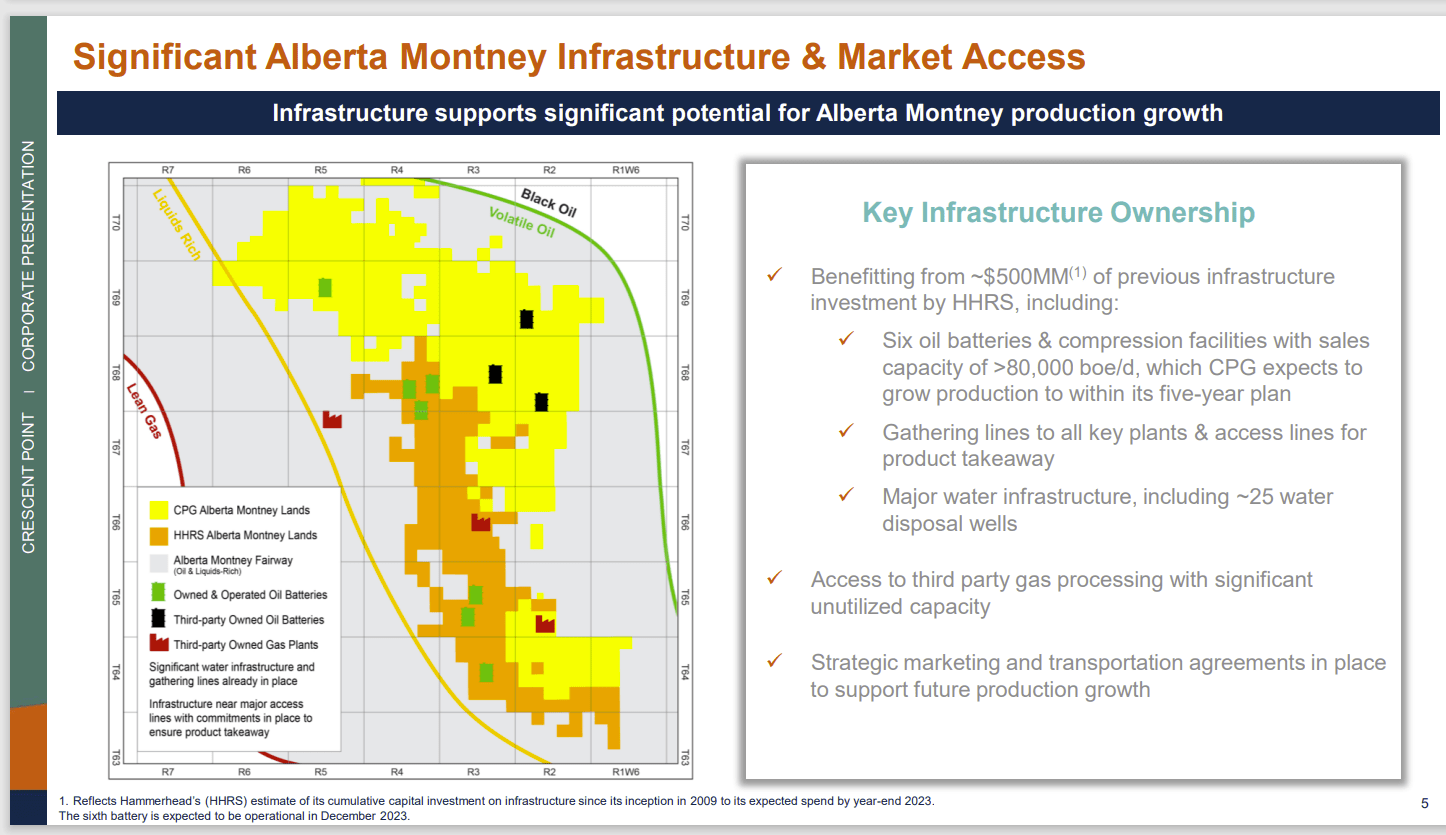

Crescent Point Energy Infrastructure Details (Crescent Point Energy Acquisition Presentation November 2023)

{kind=link}

The company also is getting infrastructure that can at least in (probably big) part handle 80,000 BOED. Since production is closer to 50,000 BOED, that means management can fill up these assets to capacity with little to no additional capital. Idle capacity in this business is often worth a lot more than book value because it would have to be built new instead of using what's already there.

Third Quarter Results

This management has long focused upon well profitability while turning the company around. The main idea is where possible, management would hang onto low costs while increasing the value of the production from the well.

{kind=link}

Crescent Point Energy Capital Budget Decrease (Crescent Point Energy Third Quarter 2023, Earnings Press Release)

The first thing to note is that managements I follow are often satisfied with good geology because it often gives them a sustained advantage for some time over the competition. They don't have to be detail oriented and "driven." Instead, they just show up for work and allow the geology to make them look like geniuses to the market. The market may never find out they could have done better because they are doing well just by getting the location. You would think we are talking about real estate.

But notice above, this management is decreasing the capital budget. That often means past acquisitions are doing better than originally assumed. Investors can likely expect more of the same in the future.

Strategic Realizations

Management has been using stock and selling non-core acreage. The cash flow statement and the deleveraging are the first to show progress. This will spread to the income statement as non-repeating costs fade into history.

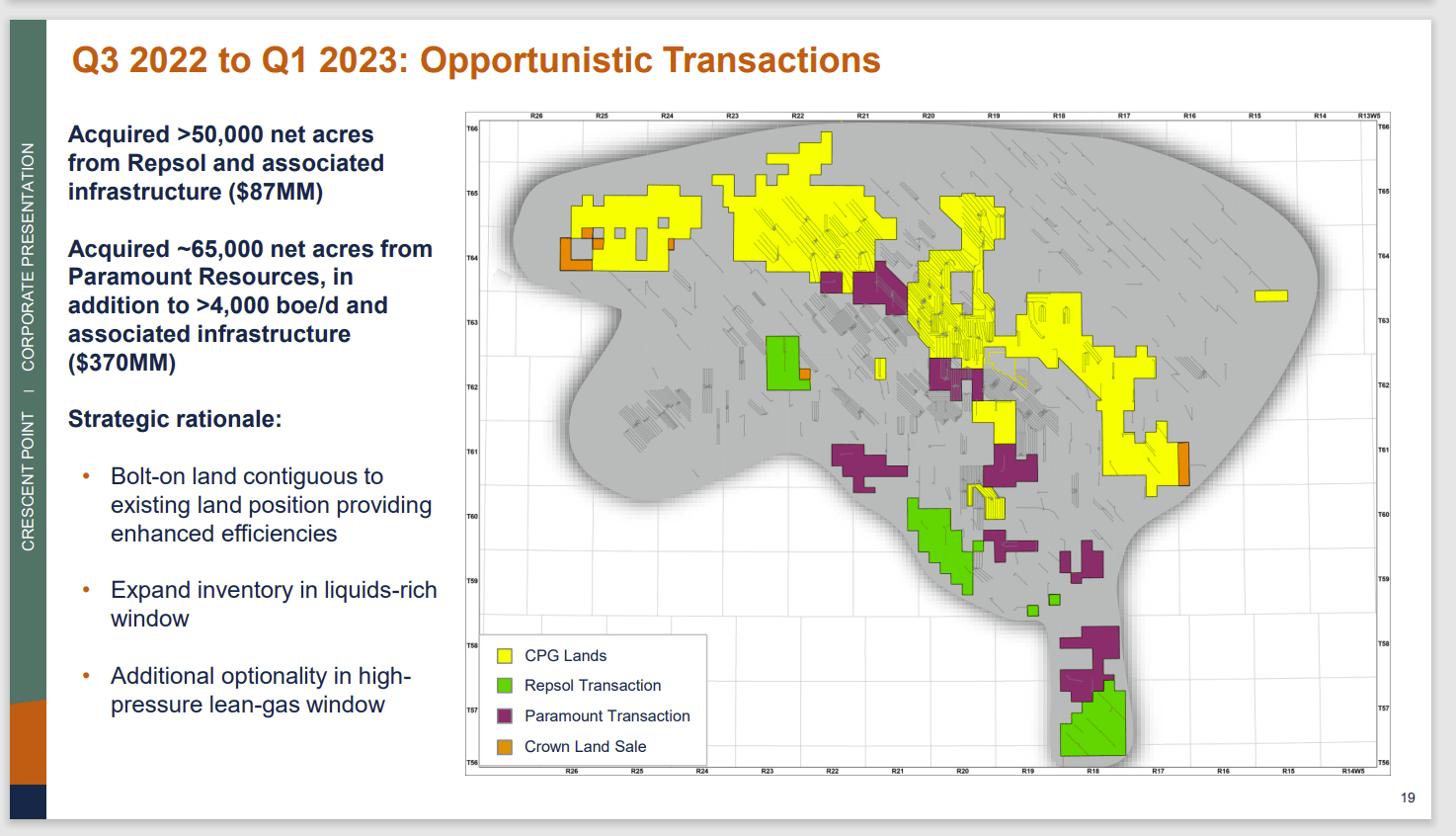

Crescent Point Energy Kaybob Duvernay Acquisition History (Crescent Point Energy Management Presentation On Thoughts Of Acreage Advantages March 2023)

{kind=link}

The company already has made several significant acquisitions before the third quarter. The Hammerhead acreage increases company exposure to far more profitable acreage than the company had before this process began. Management is counting on not only the bargains noted, but also synergy strategies in the future.

The income statement likely reflects the previous management's decisions rather than the current management. Established production does not automatically become more profitable under a new owner (although reworks may change that if profitable to do). That income statement also has a lot of "noise" until acquisition and optimization costs related to recent acquisitions are complete. The cash flow statement, however, has shown clear improvement over the years.

Even though management is doing their best to optimize operations and drill better wells, it will take time for those changes to become significant. The performance of acquired wells will dominate for some time to come. In the meantime, management is prioritizing the payment of debt as long as there are bargains out there to acquire.

What will likely happen is the company will become big enough that each additional bargain will be less significant. Then it will be easier for the market to see management progress as the one-time costs of each acquisition become less significant.

For now, investors can look at companies like EQT ( EQT ) and Baytex Energy ( BTE ) which are now reporting results based upon the companies holding a lot of these acquisitions for several years. Therefore, any improvements will show on the income statement, the cash flow statement and eventually the balance sheet. Baytex, for example, has reported improved results for years now even considering the latest acquisition . At that point, the market begins to value management improvements.

Latest Acquisition, Other Considerations Ending With Risks

The one major thing that clouds the "improvement" issue appears to be the industry wide collapse of price-earnings ratios throughout the industry, the pandemic challenges hid this issue. However, the sheer number of low price-earnings ratio stocks that has emerged since 2020 definitely puts the industry on the "cheap side" of valuations in the stock market.

This shows in the low prices for acquisitions as well. But it's also allowing the industry to recover from a very challenging 2015-2020 period. When investors ask about a lack of stock price confirmation, this is the main issue contributing to that complaint. No matter at what point, the price-earnings ratios collapsed in the eyes of an investor, it is clear that the ratios remain historically low.

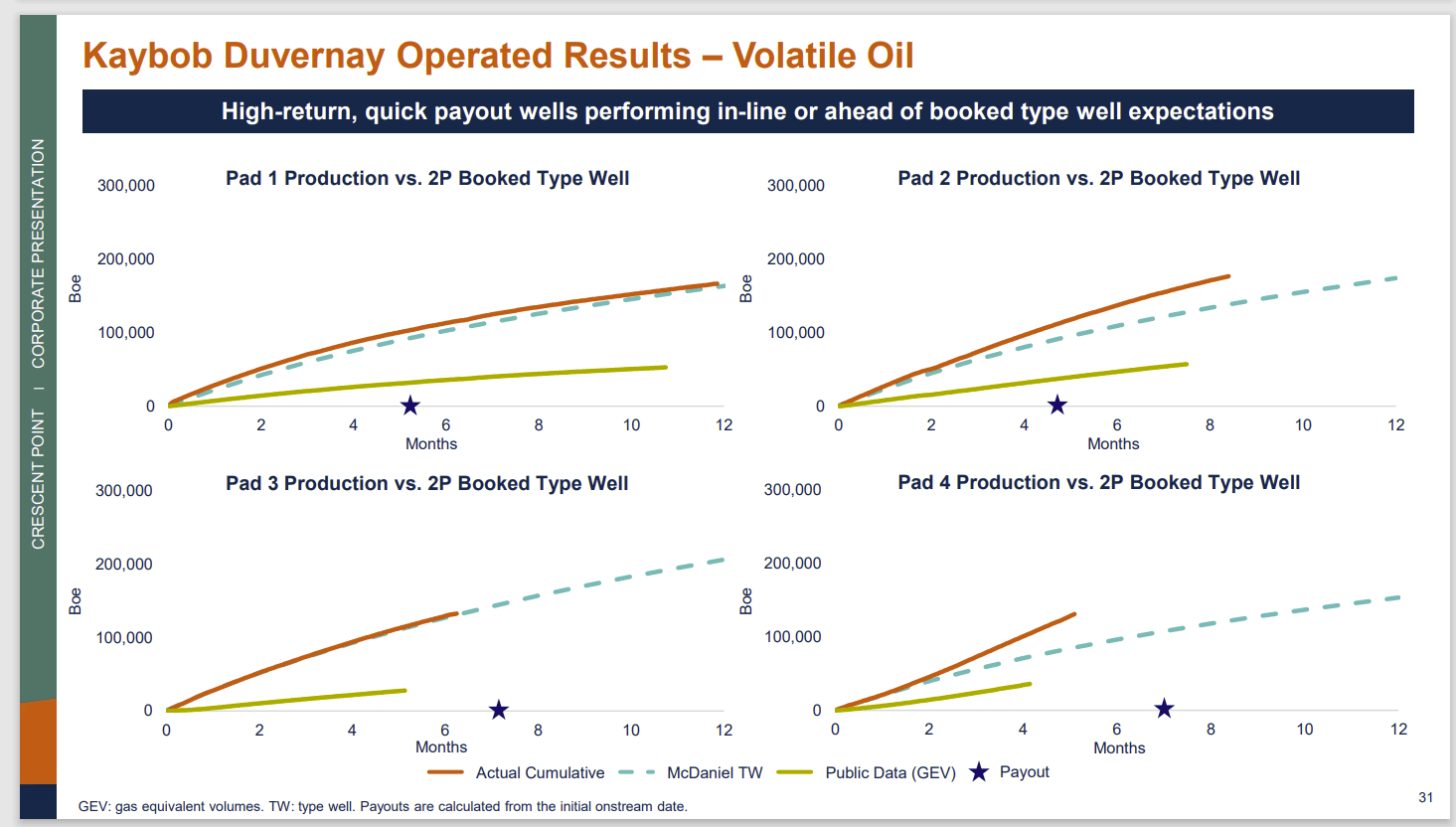

Crescent Point Energy History Of Beating Reserve Report Assumptions (Crescent Point Energy Duvernay Kabob Basin Presentation March 2023)

{kind=link}

Management expects to continue to beat the reserve report assumptions upon which acquisition negotiations resulting in the Hammerhead acquisition were made. Shown above is the history of some of the previous acquisitions. There are more examples in the presentation. This is not included in any presentation of savings, value, or synergy talk. Actually, what this is would be technology advances that frequently make the deal even better than anticipated.

I would therefore applaud management for continuing the strategy that likely saved the company from a far worse fate and will likely lead to a superior price performance in the future or possibly an acquisition offer for the right price and terms.

Price earnings ratios will eventually return to historical levels once the market realizes that the 2015-2020 series of events was probably not ever going to be replicated again.

The price measured as net operating income for the Hammerhead proposed acquisition would seem to indicate that prices are beginning to move up. The metrics given there refer to net operating income whereas many announcements use EBITDA.

But by any measure that price is fantastic compared to many I have covered for investors over the years. Therefore, it would appear that the latest spate of acquisitions still has room to run. On the other hand, the slight increase in price (acquisition valuation climbing) would appear that maybe the seeds of ending the current spate of acquisitions are finally sowed.

{kind=link}

Crescent Point Energy Key Financial Considerations For Acquisition (Crescent Point Energy Acquisition Presentation November 2023)

The primary risk to the transaction is that management made a mistake in stating "premium acreage." That's unlikely because management is specializing in that area and should know the acreage pretty well.

Rapid growth also can have some risk. But so far this management appears to have handled fairly rapid growth. It was probably more challenging in the beginning to start turning this company's finances around for a far more favorable future. Once that got done, this is more like icing on the cake. But future results need to demonstrate that.

The recycle ratio shown above marks this as a fairly profitable proposition. Management does review how accretive the transaction is. The management improvements already are on the books. This should give them some leeway on this acquisition.

Key Ideas Going Forward

Most investors would agree that this management brought about some major financial and strategic focusing of the company that made the company's future far better than before this management team got there.

{kind=link}

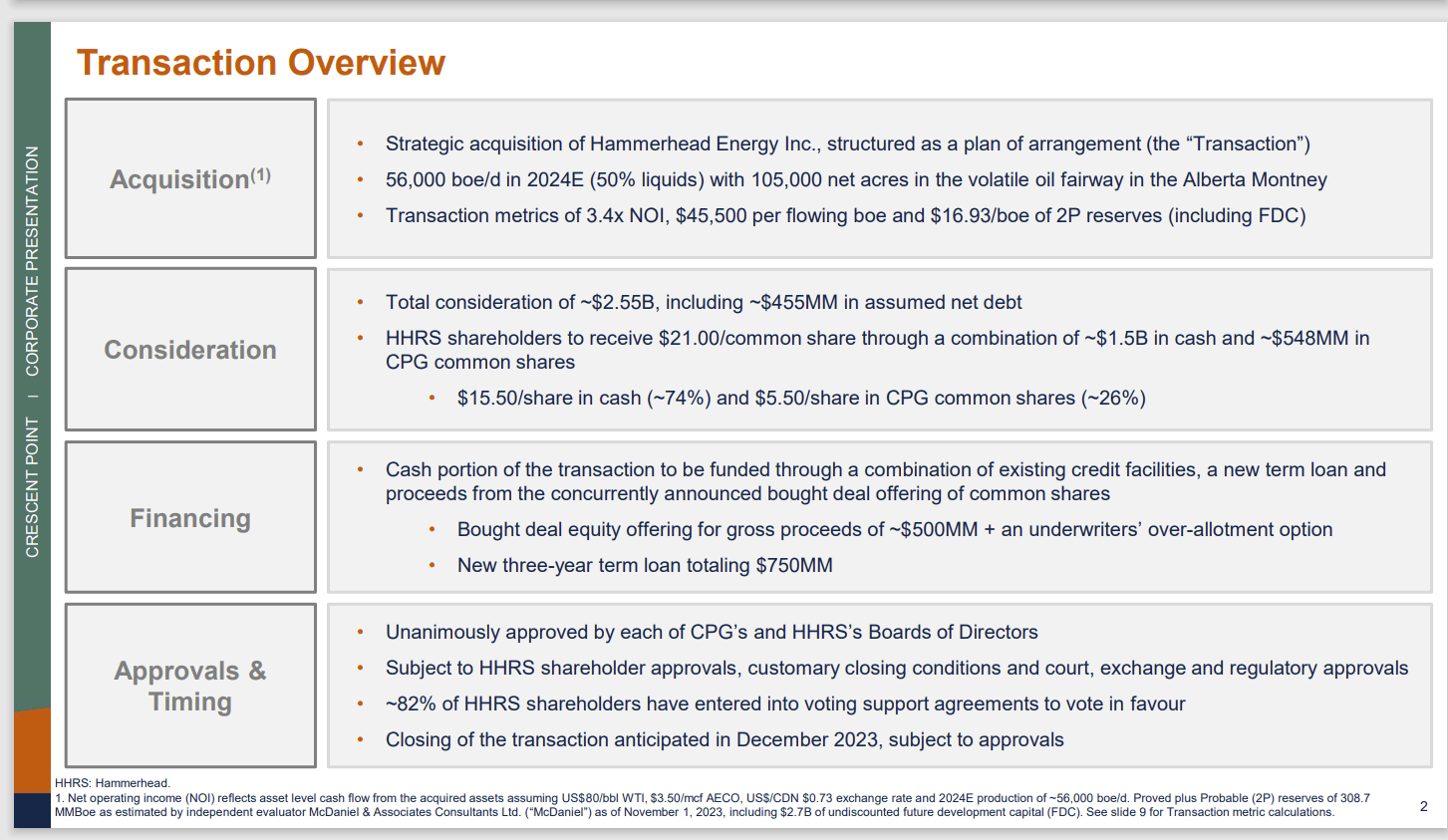

Crescent Point Energy Comprehensive Proposal To Acquire Hammerhead Energy (Crescent Point energy Acquisition Proposal November 2023)

The guidance uses WTI $80 as noted throughout the presentation as the pricing assumption going forward. That assumption can be hedged for a year or two at least to guarantee a cash flow level for this production if needed.

There are some safety factors in that the natural gas price assumption could prove conservative as the North American market likely joins the stronger world market for commodity prices due to the increasing ability to export natural gas in the near future.

The other major consideration is that technology is advancing very fast in unconventional business. This often turns a perceived mistake into a bargain a few years down the road. This is not something you see every day in any industry. It's definitely not something that can be bargained (as a rule). But it's a benefit many acquirers count on to make them look smart in the future.

It's very rare, however, for any management to turn around a company that was once headed to the hereafter (and on the express train too). This management clearly has done that and more. For me, that relatively rare track record marks this management as above average (probably way above average) and worth investing in.

Another consideration touched on is a lot of these deals are made during times of low prices (like earlier in the fiscal year) and are announced when prices are strengthening. This is part of the buyers' market phenomenon. A lot of these buyers have "had it" and just want out. Meanwhile management sees industry consolidation, a market demand for dividends (and not growth), and "live within your means" (except acquisitions which ironically allow for per share growth). This management found a way to grow per share results at a time when the market is very hostile to organic growth. That's liable to serve investors very well in the future over companies that just return capital.

The balance sheet repair that occurred by using stock in all the deals was "icing on the cake." Many managements had their hands full just repairing the balance sheet (let alone increasing profitability and growing production per share). This management clearly goes the extra mile.

Much of the industry is dirt cheap including this company. It's a strong buy that management will consider reporting improvements as they have in the past. The l ow dividend may dissuade conservative investors. But a lot of investors can figure out the successes attained so far that will make the investment proposal here attractive.

For further details see:

Crescent Point Energy: Management Found Another Bargain With Hammerhead Acquisition