CURLF - Cresco Labs Has Pulled Back And Could Be A Buy

2023-10-09 08:53:10 ET

Summary

- Cresco Labs is a Chicago-based MSO operating in multiple states with 14 production facilities and 71 dispensaries.

- The company reported Q2 revenue of $198 million, up 2% sequentially, and adjusted EBITDA of $40 million, exceeding expectations.

- Analysts project a decrease in 2023 revenue by 10% but anticipate a 2% increase in 2024.

- I include CRLBF in my model portfolios after a recent purchase.

I have always liked Cresco Labs (CRLBF), but I had a very difficult time owning it in my model portfolios until recently. Recall that in February, as the spread was widening to the price implied by its pending acquisition, I liked what was then Columbia Care. It was too cheap! I ended up exiting Columbia Care after the merger failed as the stock rallied. Last week, I wrote about The Cannabist Company (CBSTF), which is the renamed Columbia Care, discussing why I find it so attractive right now.

Investors need to be careful with MSOs in my view, as they have rallied so much since the news broke about the HHS asking the DEA to reschedule cannabis. The stocks, though, have pulled back, and some, like Cresco, are now down year-to-date. I added Cresco to both of my model portfolios this week. In this piece, I discuss the company, assess its financial performance in H1, review the outlook, analyze its valuation and take a look at the chart.

The Company

Cresco Labs is one of several Chicago-based MSOs that trade publicly. Of the largest five MSOs, three are based in Chicago, including Cresco, Green Thumb Industries ( GTBIF ) and Verano ( VRNOF ). Illinois is a big state for the company, which also operates in nine others. It has 14 production facilities and 71 dispensaries. Production facilities are in Arizona and California (2) to the west, and in Florida, Illinois (3), Massachusetts (2), Michigan, New York (1 and 1 under construction), Ohio, Pennsylvania to the east. The Sunnyside dispensaries are in Arizona (1), Florida (33), Illinois (10), Massachusetts (4), New York (4), Ohio (5) and Pennsylvania (14). Most of these are medical-only.

CEO Charlie Bachtell, a lawyer, has been running the company since he co-founded it in 2015. CFO Dennis Olis joined in 2020 and was previously the CFO of AllScripts. Another executive is Greg Butler, Chief Transformation Officer. He was previously at Molson Coors before joining Cresco in 2018.

2023-H1 Financials

According to Sentieo, analysts had expected Q2 revenue would be $195 million, with adjusted EBITDA of $31 million. On 8/16, the company reported revenue of $198 million, up 2% sequentially. Retail sales grew 4%, while wholesale sales were flat. Compared to a year ago, revenue fell 9%. Adjusted EBITDA of $40 million was far better than expected, and it grew 38% sequentially.

H1 revenue of $392 million fell 9% from a year ago. Gross profits fell, and operating expenses rose slightly. The company experienced an operating loss of $7 million relative to a $43 million operating profit in the first half of 2022. Adjusted EBITDA fell from $101 million to $70 million. The company generated $18 million from its operations in Q2 and over $21 million in H1. While capital spending fell, it did spend more than what it generated from operations, with purchases of property and equipment totaling $38 million.

Cresco Labs ended Q2 with cash of $73 million and debt of $496 million. Its income tax payable increased by $12 million from Q1 to $92 million in Q2. Tangible book value at the end of Q2 was -$166 million. The ratio of current assets to current liabilities is 1.1X.

The Outlook

Ahead of the Q2 report, analysts had expected 2023 revenue to be $791 million and for 2024 revenue to be $857 million. They now project that 2023 revenue will $757 million, down 10%, and that it will increase 2% in 2024 to $776 million. Adjusted EBITDA had been expected to be $140 million in 2023 and $188 million next year. Now they project 2023 adjusted revenue will be $144 million, down 17%, with 2024 of just $174 million, up 17%.

For 2025, three analysts expect revenue will increase 13% to $873 million. Expected adjusted EBITDA is $227 million, up 30%.

Stock Is Reasonably Valued

Cresco Labs trades at a discount to its peers, especially Curaleaf ( CURLF ). I like Trulieve ( TCNNF ) more, and I remain cautious on Verano ( VRNOF ), which has projected margins that I think are too high. Here is the enterprise value to adjusted EBITDA projected for 2024 for the top 5 MSOs, which includes Green Thumb Industries ((GTBIF)) too:

Alan Brochstein, using Sentieo

Ahead of the Q2 report, my outlook was not great, as I had a year-end target of $0.70 based on only 5X projected 2024 adjusted EBITDA. With the lower projected adjusted EBITDA, my price for year-end might be lower now, but with 280E potentially going away, the stock would trade a lot higher if that were to happen.

As I look out a year and use 75% of the 2025 projection (reduced, though, to a 24% margin of revenue or $210 million) along with 25% of the 2024 and use a multiple of 10X, I get an enterprise value of $2.01 billion. This works out to an equity value of $1.59 billion, which is $3.55, up 114%.

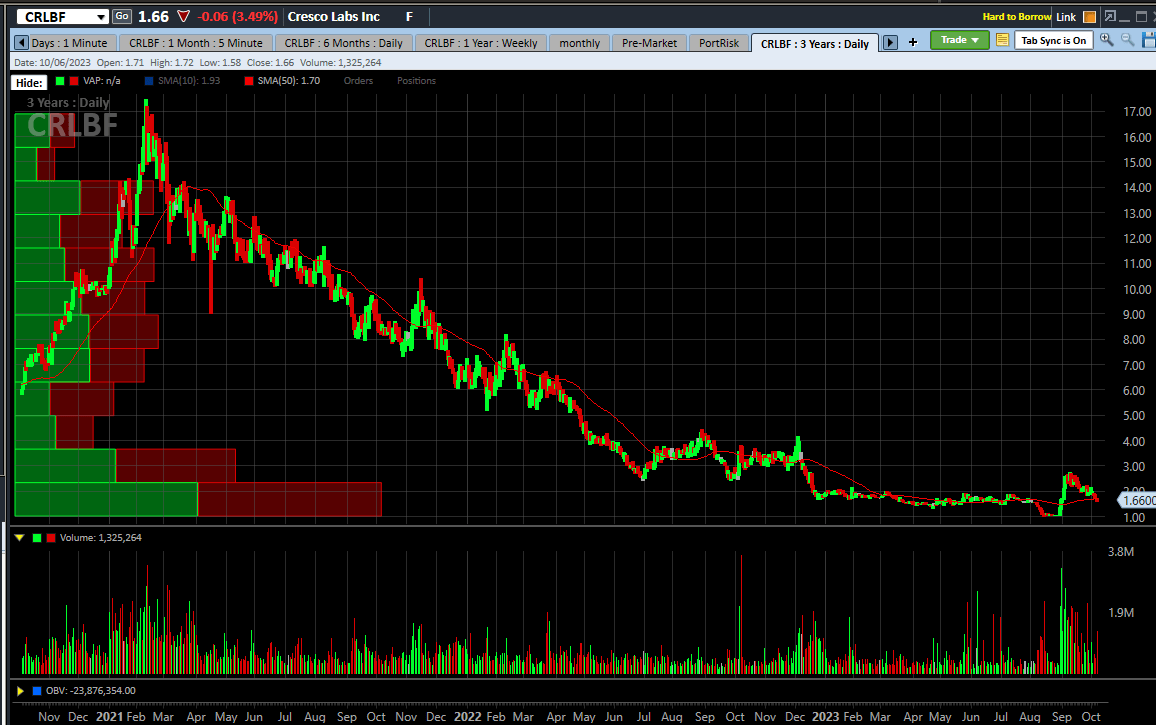

Chart Looks Like This Is a Dip to Buy

The stock made a new all-time low near $1 in August before soaring to just under $3 after the news broke regarding potential rescheduling. It pulled back and is below the 50-day moving average and near support of $1.55:

{kind=link}

Taking a longer-term look, the stock is now down by about 7% year-to-date, and it has pulled back a ton from its high in early 2021:

{kind=link}

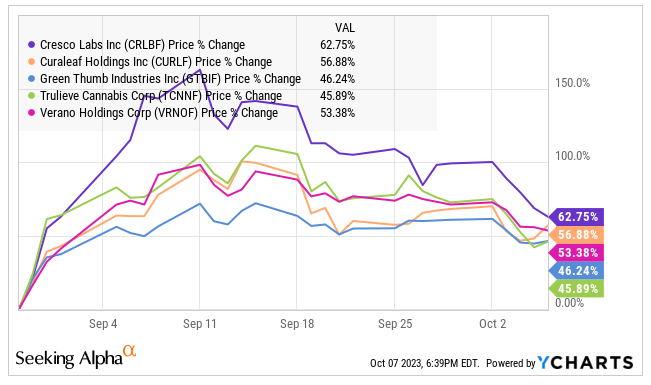

Compared to peers since 8/29, the day before the potential rescheduling news broke, the stock has outperformed its peers:

{kind=link}

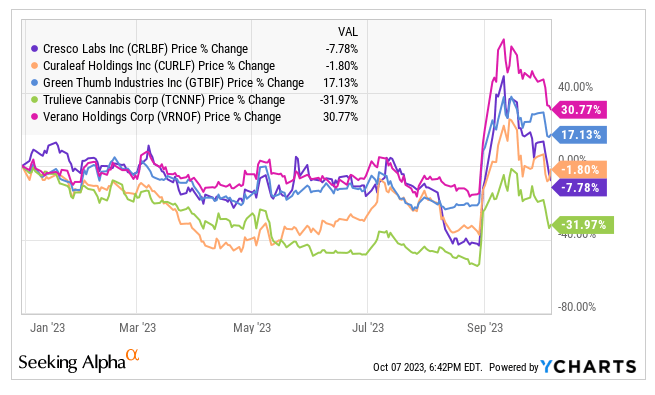

Year-to-date, though, CRLBF has underperformed VRNOF, GTBIF and CURLF:

{kind=link}

Conclusion

My model portfolios had no CRLBF coming into the week, but I ended with a position of 3.8% in the Beat the Global Cannabis Stock Index model portfolio. This is similar to its weight in the index. In the Beat the American Cannabis Operator Index model portfolio, CRLBF is 10.5%, a bit ahead of its weight in the index.

My biggest concern currently is that the rescheduling doesn't take place, leaving 280E taxation in effect. The company has negative tangible equity and a relatively low current ratio, and it would likely need to sell stock, as would its peers. I continue to warn investors not to make investments solely in MSOs.

For further details see:

Cresco Labs Has Pulled Back And Could Be A Buy