CA - Crestwood Equity Partners: Solid Q4 Results And Improving Finances

Summary

- Crestwood Equity Partners LP showed the general financial stability that we have come to expect from this company in its fourth-quarter results.

- Crestwood is selling off a natural gas storage facility and using the proceeds to reduce its debt.

- The company is positioned to deliver cash flow growth in 2023 which will enable it to conduct further debt reductions.

- The company's leverage is not especially high, but it would still be beneficial for it to reduce debt due to the hostility of external capital to fossil fuel companies.

- The 10.47% yield is easily sustainable, although Crestwood Equity Partners LP will probably not raise its distribution in 2023.

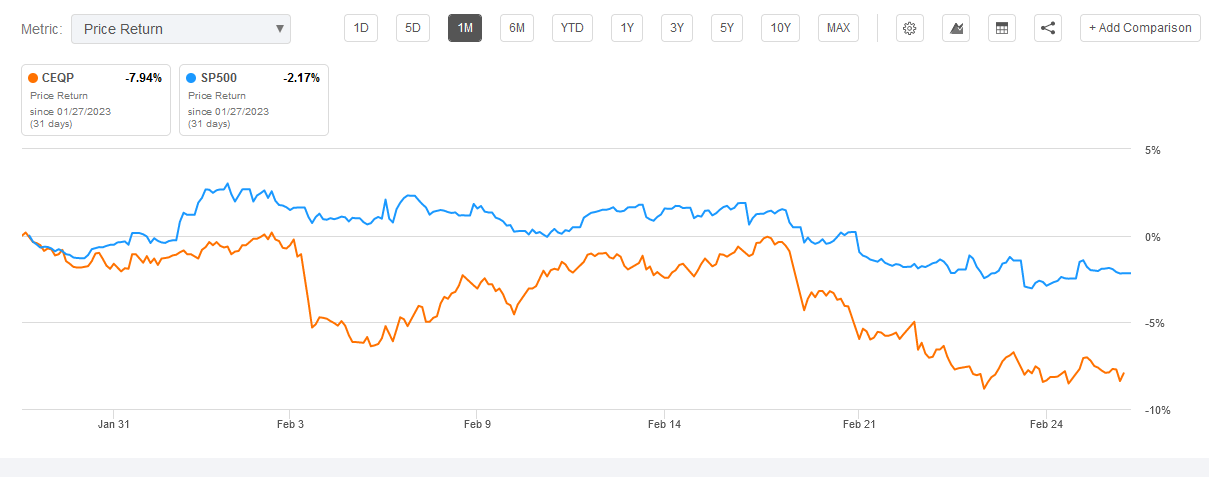

On Tuesday, February 21, 2023, natural gas-focused midstream partnership Crestwood Equity Partners LP ( CEQP ) announced its fourth-quarter 2022 earnings results. At first glance, these Q4 results were mixed, as Crestwood Equity Partners missed the expectations of its analysts in terms of revenue but still managed to achieve an earnings beat. The market was not exactly impressed with these results, as the company’s units continued the decline that has been occurring for the second half of February:

{kind=link}

With that said, though, a deeper look at the company’s earnings report reveals that it performed much better than one might think simply from looking at the disappointing market return. In fact, Crestwood Equity Partners posted significant cash flow growth during 2022, and cash flow is by far the most important metric to use when evaluating a midstream master limited partnership. The company is quite well positioned to continue this growth in 2023, and when we combine this with the company’s 10.47% current yield, there is still a lot to like here.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Crestwood Equity Partners’ fourth-quarter 2022 earnings report:

- Crestwood Equity Partners brought in total revenue of $1.4092 billion during the fourth quarter of 2022. This represents a 2.09% increase over the $1.3804 billion that the company reported during the prior-year quarter.

- The company reported an operating income of $104.1 million during the most recent quarter. This was roughly in line with the $104.2 million that it reported during the year-ago quarter.

- Crestwood Equity Partners gathered an average of 1.0565 billion cubic feet of natural gas per day during the reporting period. This represents an 11.94% increase over the 943.8 million cubic feet of natural gas per day that the company gathered on average last year.

- The company reported a distributable cash flow of $110.8 million in the current quarter. This represents a significant 21.62% increase over the $91.1 million that the company reported last year.

- Crestwood Equity Partners reported a net income of $53.9 million in the fourth quarter of 2022. This represents a 31.42% decrease over the $78.6 million that the company reported in the fourth quarter of 2021.

It seems certain that the first thing anyone reviewing these highlights will notice is that Crestwood Equity Partners generally performed better than during the prior-year quarter. The notable exception to this is that the company’s net income dropped fairly significantly year-over-year. However, as I have pointed out in various previous articles, net income is not especially important for a midstream company because it is affected by a variety of factors that do not actually represent money coming into or leaving a business. The most important financial metric to use to evaluate one of these companies is cash flow and as we can see above, Crestwood Equity Partners saw its cash flow increase year-over-year.

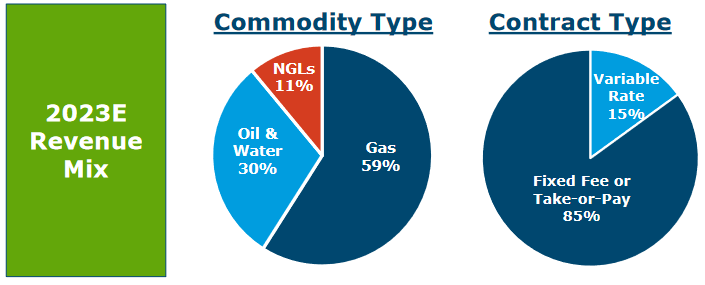

The majority of energy companies that have reported their fourth-quarter results thus far have shown a general year-over-year improvement. In many cases, this was because oil prices were higher during the fourth quarter than during the prior-year quarter. I mentioned this in a few previous articles, such as this one . However, this does not really benefit Crestwood Equity Partners. One reason for this is that the company is more focused on natural gas than on crude oil. In fact, approximately 59% of the company’s revenue comes from natural gas:

{kind=link}

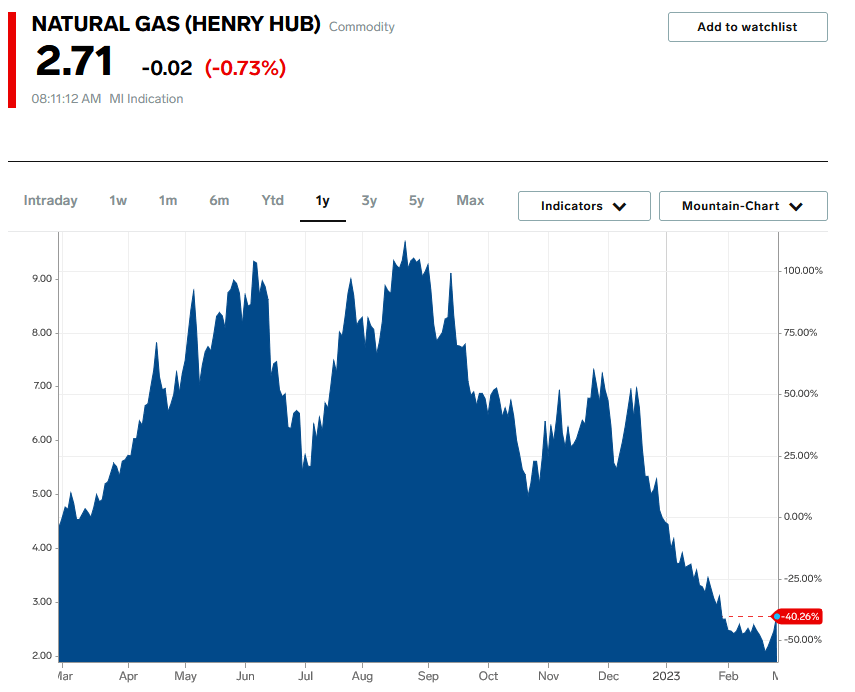

Unlike crude oil, natural gas prices have been performing quite poorly recently. As of the time of writing, natural gas at Henry Hub is down 40.26% over the past twelve months:

{kind=link}

Crestwood Equity Partners is not particularly dependent on natural gas or crude oil prices because of the business model that it uses. In short, the company enters into long term (usually five to ten years in length) contracts with its customers under which the company transports resources and the customer pays Crestwood Equity Partners based on the volume of resources transported, not their value. This business model provides a great deal of insulation against changes in energy prices and is what gives companies like this their general financial stability. We can see this quite clearly by looking at the highlights above. Crestwood Equity Partners’ results did not change nearly as much over the past year as natural gas prices did. That stability is something that we typically appreciate because it provides a great deal of support for the distribution.

One of the things that we have always liked about Crestwood Equity Partners is that the company is more focused on the transportation and storage of natural gas than of crude oil. This is because natural gas has much stronger long-term fundamentals than crude oil, which I discussed in a recent blog post . However, the comments made in the company’s earnings press release by Robert G. Phillips, Crestwood Equity Partners’ founder, and CEO, suggest that the company may be attempting to shift its focus toward crude oil. Mr. Phillips stated ,

“2022 was another transformational year for Crestwood as we continued to realign our midstream portfolio by expanding the Williston, Delaware, and Powder River Basins, which are highly economic, oil-weighted resource plays, while divesting our Barnett and Marcellus assets, which were non-core, gas-weighted, and low-growth. We have continued that strategy with the recent sale of our Tres Palacios natural gas storage facility to reduce debt and improve our balance sheet.”

The Tres Palacios facility is a natural gas storage site located in Matagorda, Wharton, and Colorado Counties in Texas. It became jointly owned by Crestwood Equity Partners and Brookfield Infrastructure Group ( BIPC ) back in 2014, when the two entities formed a joint venture and purchased it in a $130 million deal. Prior to that, it was owned solely by Crestwood Equity Partners. As the sale price announced in the fourth-quarter earnings report is $335 million, it appears that Crestwood Equity Partners will realize a substantial capital gain on this sale. The company stated that it will receive a total of $168 million from the sale, which it intends to use to reduce its debt. That would be a smart move since, as I pointed out in a recent article , Crestwood Equity Partners’ leverage ratio is a bit above what we really want to see. This is in some ways reminiscent of the capital recycling strategy used by the various Brookfield entities. In short, the company appears to be trying to sell off assets that are not part of its core focus in the Permian Basin, Bakken Shale, and Powder River regions and using the money to reduce its debt and acquire additional assets that are in those core areas. This strategy could work out pretty well for the company, especially since it does not really seem to be reducing its natural gas focus despite the comments made by Mr. Phillips. We can see that in the fact that 59% of the company’s 2023 revenue is expected to come from natural gas.

Forward Growth Analysis

One of the advantages of Crestwood Equity Partners’ contract-based business model is that it provides Crestwood Equity Partners with a great deal of financial stability. After all, the company is paid based on the volume of resources that it transports, not on their value. In addition, the contracts specify a certain minimum volume of resources that the customer must move through the partnership’s infrastructure or pay for anyway. Thus, it can count on its revenue and cash flow being pretty stable no matter what the conditions are in the broader economy. However, as investors, we want to see growth and not just mere stability. Fortunately, Crestwood Equity Partners is well-positioned to deliver that growth. During the earnings report, the company provided adjusted EBITDA guidance of $780 million to $860 million. That would represent a moderate to significant increase over the $762.1 million that the company reported in the full-year 2022 period. As adjusted EBITDA is essentially a proxy for pre-tax cash flow, it is easy to see why this growth should prove attractive to investors. The company expects that it will deliver this growth in the form of steady quarterly improvements over the course of 2023:

Crestwood Equity Partners

There are some reasons to believe that Crestwood Equity Partners will actually be able to deliver this growth. The company’s customers are currently planning to drill 260 new wells on acreage covered by Crestwood’s gathering infrastructure over the January 2023 to December 2023 period. It is quite likely that this drilling activity will actually occur since it is typical for exploration and production companies to provide their midstream partners with their drilling plans so that the midstream company can have the infrastructure in place. It is also typical for a drilling company to have some idea of how productive a well will be before it actually drills it.

Thus, Crestwood Equity Partners can make a reasonably accurate projection of its full-year volumes and then extrapolate its cash flows from that. As any increase in cash flows adds support to the distribution, we should appreciate this as investors. Crestwood Equity Partners specifically stated that it will be using its incremental free cash flow to pay down its debt, so unfortunately, we probably will not see a distribution increase in the near term. However, the added cash flow will still improve the safety of the current one.

Financial Considerations

It is always important to look at the way that a company finances its operations before investing in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt to repay the existing debt, which can cause a company’s interest expenses to increase following the rollover. That is something that could prove especially important today as the Federal Reserve has been steadily raising interest rates and shows no sign of changing this policy. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although midstream companies like Crestwood Equity Partners tend to have remarkably stable cash flows, this is still a risk that we should not ignore.

The usual way that we judge a midstream company’s ability to carry its debt is by looking at its leverage ratio. The leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio, essentially tells us how many years the company would require to completely repay its debt if it were to devote all of its pre-tax cash flow to this task. As of December 31, 2022, Crestwood Equity Partners had a leverage ratio of 4.2x based on its full-year 2022 adjusted EBITDA. This is not a bad ratio per se as Wall Street analysts typically consider anything under 5.0x to be reasonable. However, many midstream partnerships have been working to get their ratios down under 4.0x over the past two years. This is in direct response to the collapse in capital market support that occurred during the COVID-19 pandemic and the rising popularity of environmental, social, and governance principles at many major institutional investors. These factors have reduced the industry’s ability to access outside capital and as such, it is taking steps to reduce its reliance on such capital.

Crestwood Equity Partners is focused on reducing its leverage as well. The company’s aforementioned sale of the Tres Palacios storage system should net it $168 million, which Crestwood will be using to reduce its debt. That alone should bring the company’s leverage ratio down to 4.0x but it expects to go further and use its growing cash flow in 2023 for the purposes of debt reduction:

Crestwood Equity Partners

Crestwood Equity Partners has the stated goal of bringing its leverage ratio down to under 3.5x over the long term, although it has not specifically stated when that goal will be reached. That would easily bring the company’s debt load down to a comparable level with the best-financed midstream companies in the industry. Unfortunately, it does seem unlikely that we will see a distribution increase until it accomplishes that goal. However, if it does manage to achieve the projected 3.7x ratio by year-end 2023 then we could see it positioned to hit its 3.5x target in 2024 and reward our patience with a distribution increase soon after that.

Distribution Analysis

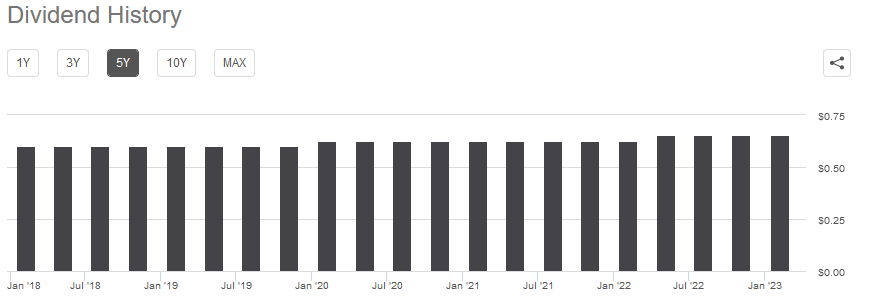

One of the main reasons why investors purchase partnership units in midstream master limited partnerships is because of the relatively high distribution yields that these companies tend to possess. Crestwood Equity Partners is certainly no exception to this as the partnership yields 10.47% as of the time of writing. This is one of the highest yields in the sector and Crestwood Equity Partners has historically been more reliable about its distribution than some of its peers, with the company maintaining its distribution instead of cutting it after the lockdowns began in March 2020:

{kind=link}

Unfortunately, it does appear that Crestwood Equity Partners will probably not increase its distribution in 2023 for reasons that were already discussed. This is rather disappointing for those that are depending on their portfolios for income as the high levels of inflation that we have seen throughout the economy over the past eighteen months have greatly reduced the number of goods and services that we can purchase with the company’s distribution. Thus, it likely feels as though we are getting poorer and poorer with the passage of time. Fortunately, the high yield at least allows some of the distribution to be reinvested so we can boost our incomes that way.

The most important thing to investors today though is the company’s ability to maintain its yield. After all, we do not want to find ourselves the victims of a distribution cut since that would reduce our incomes and almost certainly cause the company’s unit price to decline.

The usual way that we judge a midstream partnership’s ability to maintain its distribution is by looking at its distributable cash flow. The distributable cash flow is a non-GAAP measure of financial performance that theoretically tells us the amount of cash that was generated by a company’s ordinary operations and is available to be distributed to limited partners. As stated in the highlights, Crestwood Equity Partners reported a distributable cash flow of $110.8 million during the fourth quarter of 2022. The company’s distribution costs it $68.9 million quarterly so this gives Crestwood Equity Partners a distribution coverage ratio of 1.61x.

Generally speaking, Wall Street analysts consider anything over 1.20x to be reasonable and sustainable. However, I am more conservative and like to see this ratio above 1.30x to add a margin of safety to the distribution. As we can clearly see, Crestwood Equity Partners easily meets both of these requirements. As such, we should not really have to worry about the distribution’s sustainability.

Conclusion

In conclusion, Crestwood Equity Partners LP’s most recent results showed the strong performance that we have come to expect from this company. Despite some comments by the CEO, the company does not appear to be exiting the natural gas midstream business, which is good as the global demand for natural gas is likely to grow substantially over the coming decades. The company is making efforts to reduce its debt load while still maintaining its attractive 10.47% yield, which is quite nice to see. Overall, it still looks like Crestwood Equity Partners LP deserves a place in an energy income portfolio.

For further details see:

Crestwood Equity Partners: Solid Q4 Results And Improving Finances