ET - Crestwood Equity To Become Part Of Energy Transfer Empire

2023-08-17 02:48:52 ET

Summary

- Crestwood Equity announces acquisition by Energy Transfer at an enterprise value of $7.1 billion.

- The deal is an all-equity deal with an exchange ratio of 2.07x and no premium.

- This is a good deal for CEQP unitholders, who get to upgrade their assets with no tax consequences.

I’ve written positively on Crestwood Equity ( CEQP ) and its preferred shares ( CEQP.P ) a few times. Today, the company announced that it would be acquired by Energy Transfer ( ET ). The stock has returned about 9%, including distributions, since my last write-up in June , and 8% since my initial write-up in February.

Energy Transfer Deal

CEQP announced on Wednesday that it would be acquired by ET at an enterprise value of $7.1 billion. The deal will be an all-equity deal with an exchange ratio of 2.07x. ET will issue about 219 million units to fund the $2.7 billion equity portion of the deal. It will also take on about $2.85 billion in long-term CEQP bonds. The deal comes with no premium.

The deal is expected to close in Q4 of this year. The deal will need approval from CEQP unitholders, as well as regulatory approval. CEQP unitholders will own about 6.5% of ET once the deal closes

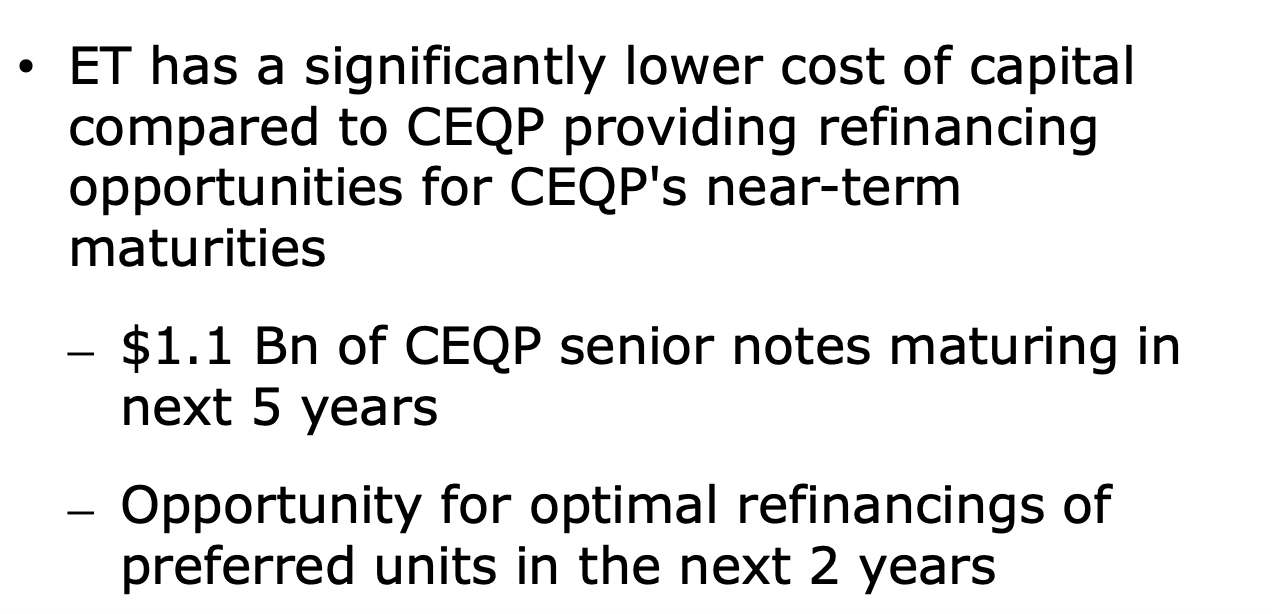

ET is expecting to see $40 million a year in cost synergies, with half realized in 2024 and the rest in 2025. The deal is expected to be immediately accretive to CEQP unitholders, and ET is projecting to grow its distribution by 3-5% a year over the next 3 years. CEQP also noted in that there could be an opportunity to refinance its preferred units over the next two years. This is something preferred holders likely won't like to hear.

{kind=link}

CEQP also noted that ET has a much lower cost of capital, which will benefit unitholders as the company has $1.1 billion of senior notes it needs to refinance over the next 5 years.

Commenting on the transaction on a call to discuss the deal, CFO Robert Halpin said:

“In connection with our valuation of this transaction, and consistent with the all-equity financial structure, we consider the relative value of both Energy Transfer and Crestwood. At the current unit price levels, we believe Energy Transfer has significant unit price appreciation potential based on a number of valuation metrics including the research analyst price target median of approximately $17 per unit. At the transaction exchange ratio of 2.07x, the analyst price target of $17 represents an approximately $35 per unit price on an exchange basis for CEQP, representing a more than 30% upside potential from current CEQP pricing levels. In addition, we believe there is further upside potential in Energy Transfer's unit price over time through execution of the business plan and the company re-rating towards the peer group meeting and trading multiple of above 9x firm value to EBITDA. We believe exchanging into Energy Transfer units meaningfully derisk the status quo business outlook and provide significant upside value for our unitholders over the long-term.”

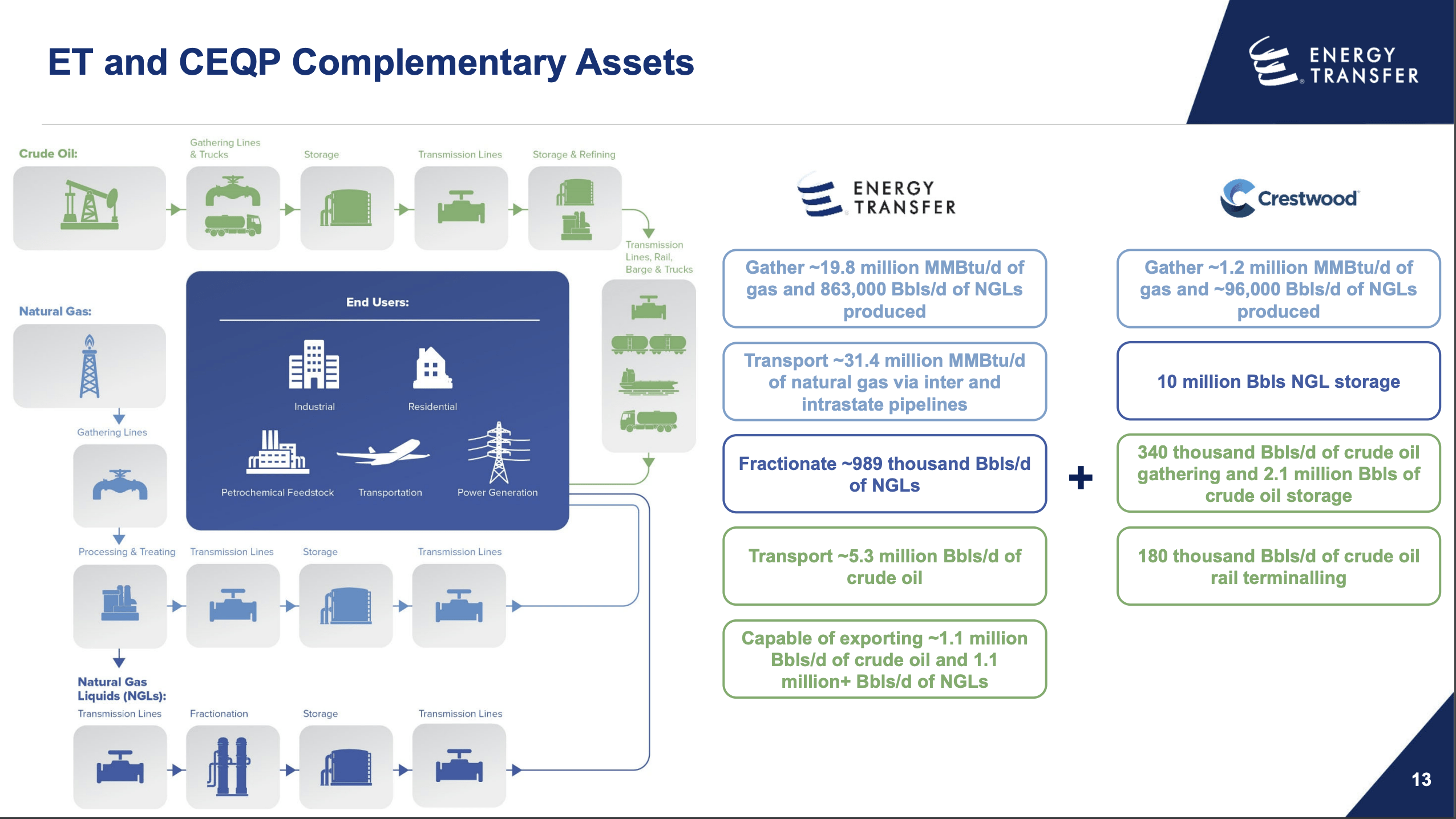

In a presentation, CEQP said that the deal will extent ET’s position in the Williston (Bakken) and Delaware, and that its substantial processing capacity in those basins complement ET’s downstream fractionation capacity at Mont Belvieu and hydrocarbon export capability from its Nederland terminal in Texas and its Marcus Hook complex in Philadelphia. The G&P also noted that ET will be able to execute more growth projects around its assets given its balance sheet, as well as pursue more private bolt-on deals around CEQP’s assets.

{kind=link}

The combined company with have a pro forma enterprise value of around $108 billion, and adjusted EBITDA of around $14 billion. That puts a 7.7x multiple on the combined company. That compares to a 9.1x multiple for fellow integrated midstream operator Enterprise Products Partners ( EPD ), 9.5x for natural gas pipeline giant Williams ( WMB ), and 10.5x for integrated Canadian midstream operator Enbridge ( ENB ).

Asked why now was the right time to be bought out after years of transforming the company, Halpin said:

“I would say that a lot of the actions that we have undertaken over the last several years were designed to build scalable franchise positions in the core areas in which we have competitive advantages to grow our platform over the long-term. And nothing has changed with respect to that. And I think we still -- in response to Tristan's question earlier, still very much are excited about the inventory outlook and producer activity across all of our core G&P assets. What has always been the case, as we've said, is the integration of gathering and processing assets into the market-oriented assets or downstream assets, has always enhanced competitive positioning significantly, enhanced returns on investment and just drives a much larger value opportunity going forward for wellhead-oriented assets. And so that view and thesis has never changed. And as we evaluate our portfolio and the growth outlook, we expect that we'll continue to see heightened levels of activity across all 3 basins from our customers, driving supply growth. But now through the combination and have our investors have an opportunity to benefit in the full value chain, downstream of our assets through the integration, which we think is an extremely compelling opportunity and one in which we do not believe we could have created on a status quo basis.”

Conclusion

If anyone is aware of my background, they may know that CEQP was the top position and one of the biggest contributors to the fund I previously worked for back several years ago. At the time, CEQP was a beaten down stock trading in the single digits that no one would touch will a 10-foot pole, but we heralded the name with our “ Crestwood Comeback ” presentation and formed a constructive conversation with management. Through a series of transactions, the company was able to transform itself into what it is now today. The CEQP management team deserves a lot of credit for what they were able to accomplish over the last seven years. Congratulations to them.

Today, I still own a lot of CEQP in my personal account, with a cost basis that is $0. My other largest midstream holding just happens to be ET, which we also owned at the fund after CEQP. While receiving no premium is a disappointment, given the discounted value of ET and the fact that I believe it has the best midstream assets in the midstream space, I still like this deal for CEQP. Essentially CEQP unitholders are upgrading the stock without any tax consequences.

I like to view ET as the largest energy arbitrageur in the U.S., and a company that is integral in the midstream space. In my view, it has the premier assets in the midstream sector and a lot of growth opportunities ahead of it. The stock has traded at a discount to peers as former CEO and current Chairman Kelcy Warren hasn't always been on the side of LP holders, but past conflicts of interest are now well behind the stock and interests are aligned. When this valuation gap eventually closes, ET’s stock has a lot of upside.

Overall, I think this is a pretty good exit for long-term CEQP unitholders. I would vote “yes” for the deal.

For further details see:

Crestwood Equity To Become Part Of Energy Transfer Empire