CA - Crew Energy: Betting On Natural Gas With A 30-Year Reserve Life

2024-01-20 10:40:00 ET

Summary

- Crew Energy Inc.'s Q3 results were impacted by weak natural gas prices, with over 78% of its oil-equivalent output consisting of natural gas.

- The company reported lower revenue and net profit compared to the previous year but maintained a strong cash flow profile.

- Despite the current challenges, Crew Energy is positioned to benefit from future increases in natural gas prices, with a favorable forward curve.

Introduction

In a recent article on Tourmaline Oil ( TOU:CA , TRMLF ), I explained why the company stock was a good way to have exposure to natural gas prices. However, I obviously also wanted to have another look at some of my older ideas. Crew Energy Inc. ( CR:CA , CWEGF ), for instance, is a relatively "pure" natural gas player , as close to 80% of its oil-equivalent output consisted of natural gas. Unfortunately, this also means the weak natural gas prices we have recently seen (except for the cold spell-induced spike in the past week) have weighed on the company's results.

The natural gas price isn't cooperating

Crew Energy obviously still has to publish its Q4 results, but I wanted to have a look back at its Q3 results to try to figure out what we can expect from the company going forward. As mentioned in the introduction, the company is definitely a gas-dominant player, as in the third quarter, its average production rate was almost 27,000 boe/day with 78% of the oil-equivalent output actually consisting of natural gas. In fact, very little oil was produced, but fortunately the condensate prices remained strong due to a pretty strong production result at the oil sands in Alberta, as condensate is used for the transportation of heavy oil.

{kind=link}

The strong oil and condensate price helped the company to report a decent average realized price per barrel of oil-equivalent but with an average realized natural gas price of just C$2.71, it definitely wasn't a great quarter. On top of that, the company has been producing below capacity, as the 26,800 boe/day definitely represents less than its ability to produce. The full-year guidance provided by the company mentions a full-year production rate of 30,000-31,000 boe/day, including the impact of a third party pipeline shutdown during Q4. To reach the mid-point of the full-year guidance, the Q4 production rate will have to increase to in excess of 32,000 boe/day. The production increase will be fueled by a strong increase in the oil and condensate output, which is anticipated to reach 7,000 barrels per day in the fourth quarter.

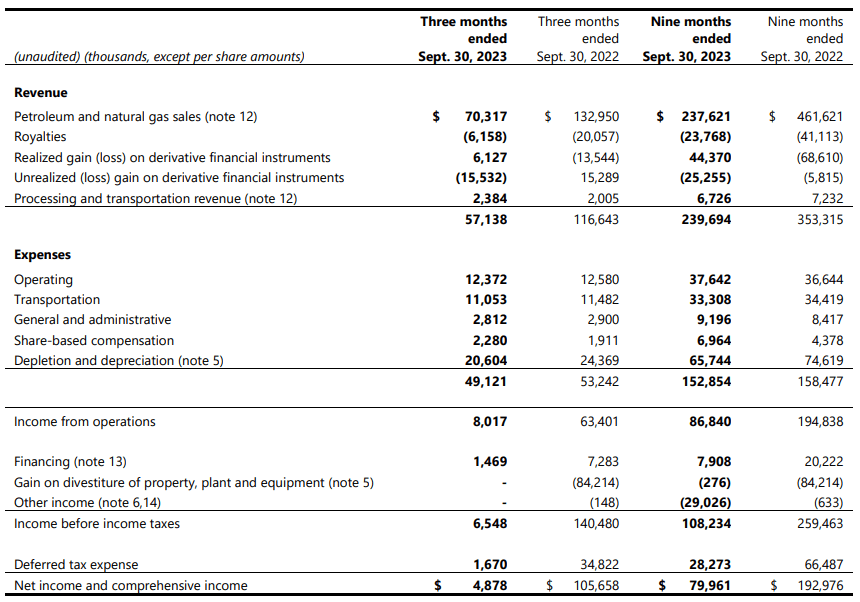

Going back to Crew's financial results, we see the company reported a total revenue of C$70M. That is just over half the revenue it generated in the third quarter of 2022, when production was higher and the natural gas price was more than twice as high.

{kind=link}

The net revenue was C$57M after also taking a net C$9M loss on hedges into account. Crew does have one of the lowest production costs in the business, and its total operating expenses were less than C$29M if you'd exclude the non-cash depreciation and amortization expenses. Including those expenses, the pre-tax income was C$6.55M, resulting in a net profit of C$4.9M or C$0.03 per share.

Of course, we can't just ignore the depreciation and depletion expenses, as a company has to continue to drill and develop wells to offset the decline rate of the oil and gas wells. But it is important to establish the company's relatively strong cash flow profile, which ultimately funds the capex programs.

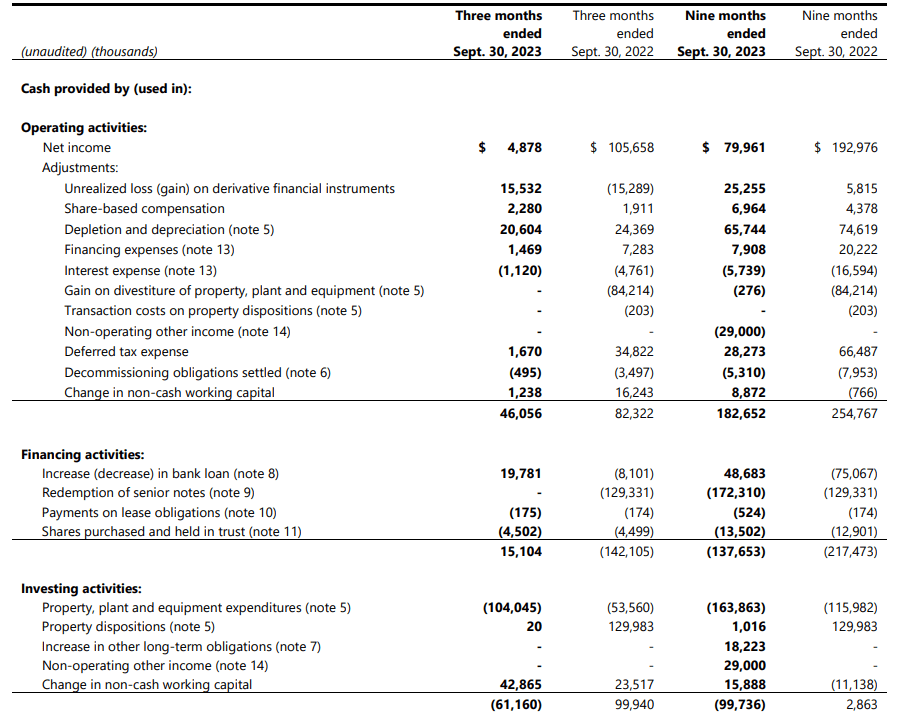

As you can see below, Crew Energy generated C$46.1M in operating cash flow, but we need to deduct C$1.2M in working capital changes and the C$0.2M in lease payments from this equation, resulting in an underlying operating cash flow of C$44.7M. Note: this includes a C$6.1M hedging gain and adds the deferred taxes back to the equation as well.

{kind=link}

The company spent C$104M on capex which means it was indeed massively overspending during the third quarter, but keep in mind the capex program isn't proportionally spread throughout the year: the total capex in the first nine months of the year was C$164M, and given the company's full-year guidance of C$220-230M, the Q4 capex will be lower than the Q3 capex. And, based on the anticipated cash flows for Q4 (the Q3 drill program included some ultra condensate rich wells which will boost the oil and condensate production during Q4), that capex program will be fully funded.

Investment thesis

Crew Energy still is a good idea to take advantage of the natural gas price (NG1:COM). While the AECO natural gas price will remain weak this year, with forward prices below C$2 during the summer, the forward curve shows an average price of in excess of C$3 in 2025, with spikes to in excess of C$4 during the winter of 2025/2026. Of course, Crew Energy will also have benefited from the price spike in January when the AECO natural gas price jumped to C$14, but it's difficult to estimate the impact on its FY 2024 results, as the company still has to publish its (production and capex) guidance for this year.

I currently have no position in Crew Energy, but with a 2P Reserve Life Index of in excess of 30 years, the company is in a good position to make hay when the sun shines again.

For further details see:

Crew Energy: Betting On Natural Gas With A 30-Year Reserve Life