CA - Crew Energy: Waiting For Higher Natural Gas Prices

2023-05-14 11:40:00 ET

Summary

- Crew Energy is a natural gas producer in Canada. Existing hedges allow for a "soft landing" and the company remains profitable and free cash flow positive.

- Crew Energy plans to spend almost C$200M in the second semester to push its production higher.

- Its existing infrastructure can handle a 20% production increase without any additional investments.

- It may use some of the cash proceeds from the Spartan Delta special dividend to rebuild a stake in Crew, but I'm in no rush.

Introduction

Needless to say the entire North American natural gas space is hurting due to weak gas prices in Canada and the US. Companies producing a decent amount of oil or condensate as a by-product are fine but companies with predominantly natural gas as an output are suffering. Crew Energy ( CR:CA ) ( OTCQB:CWEGF ) is one of those Canadian natural gas producers I have been keeping an eye on and I wanted to see how the company dealt with the lower natural gas price in the first quarter of the year.

The first quarter of the year started weak

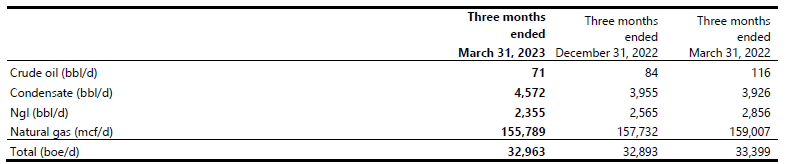

Crew is a sizable producer. Its total oil-equivalent production rate is just under 33,000 barrels of oil-equivalent per day, and as you can see below, less than a quarter of a percent of the oil-equivalent output actually consists of oil. The condensate and NGL production represent about 21% of the output and this means Crew Energy is a predominantly natural gas focused producer.

{kind=link}

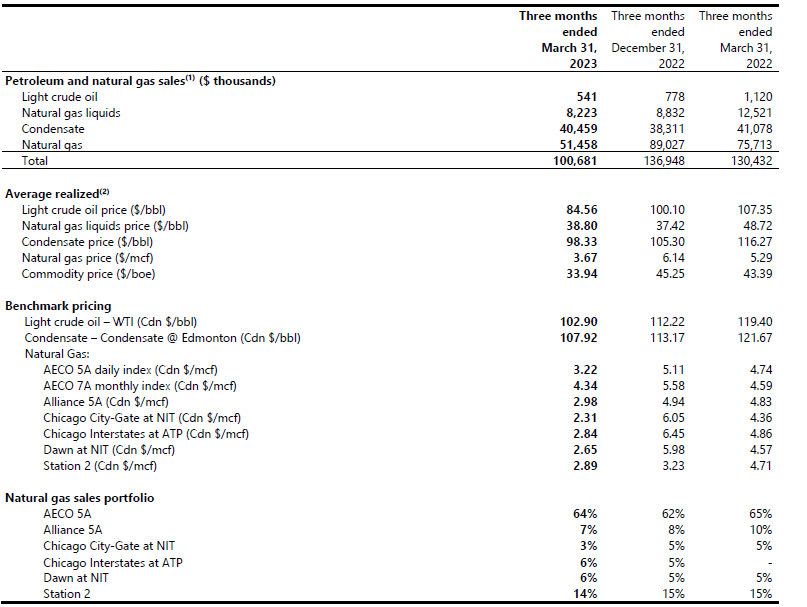

Thanks to the pretty strong condensate price (which came in at almost C$100/barrel during the first quarter), Crew Energy was able to mitigate the impact of the lower natural gas prices. I’m using the word "mitigating" as it for sure wasn’t able to compensate for it. As you can see below, the average natural gas price decreased by approximately 40% compared to Q4 2022 and the average realized price per barrel of oil-equivalent decreased by approximately 25%, mainly thanks to the lower decrease of the condensate price (minus 7%) and a small increase of the NGL price which increased by almost 5%.

{kind=link}

And seeing how weak the US natural gas market was, the 64% exposure to the AECO natural gas market in Canada in Q1 2023 wasn’t even a deterrent. The image above also shows that although natural gas represents almost 80% of the production, it generates just over 50% of the revenue, so the impact of the condensate sales should definitely not be underestimated.

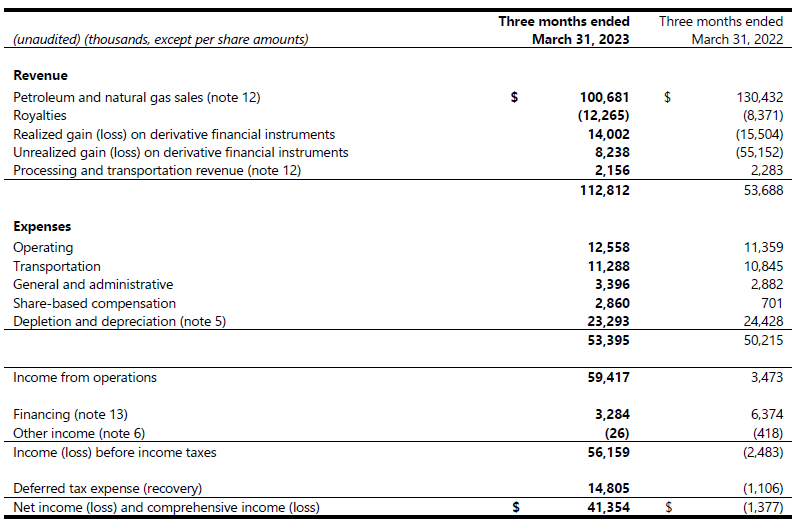

Thanks to its ultra low-cost production base, Crew Energy remained profitable. As you can see below, the company reported a total net revenue of C$113M (but this includes about C$22M in realized and unrealized gains on the hedge book). The operating expenses were very low at just over C$12.5M and the transportation expenses also were pretty stable at just over C$11M.

{kind=link}

This resulted in operating income of C$59.4M and a pre-tax profit of C$56.2M. After deducting the corporate taxes, the net income was C$41.4M which was C$0.27 per share (or C$0.26 on a fully diluted basis ).

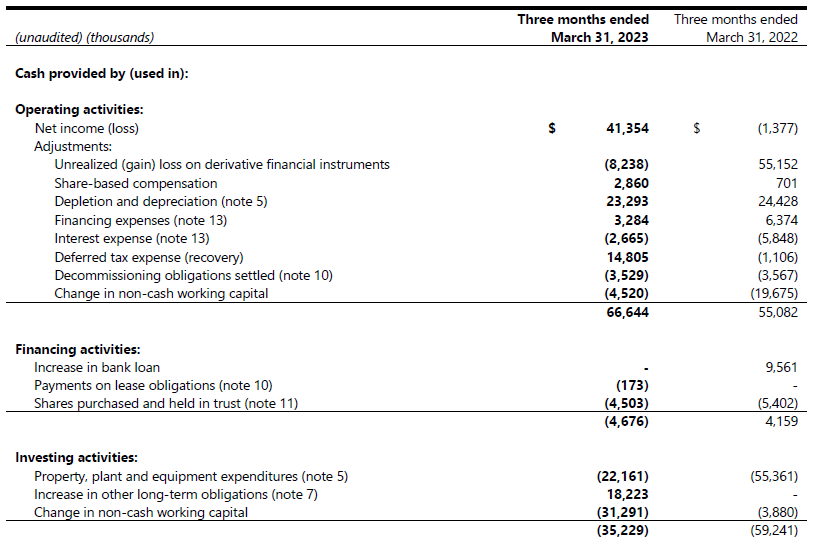

That’s great but keep in mind about 40% of the pre-tax income was generated by the hedge gains. That being said, the C$14M realized gain on hedges is already included in the average realized price of C$3.67 per mcf I mentioned above and in the cash flow statement only the C$8.2M in unrealized hedging gains is deducted again. As you can see below, this resulted in a reported operating cash flow of C$66.6M, and after adding back the C$4.5M in working capital investments and deducting the C$0.2M spent on lease payments, the adjusted operating cash flow was C$70.9M.

{kind=link}

Keep in mind this includes the C$14.8M in deferred taxes. As Crew Energy is still able to use historical losses to offset its pre-tax income, it does not have to pay cash taxes and that’s definitely a boost to the cash flow results.

The total capex was just C$22M which means the underlying free cash flow was a surprisingly strong C$49M. And even if cash taxes would have to be paid, the free cash flow would still have been approximately C$35M or C$0.23 per share.

Crew Energy took advantage of its strong performance and healthy cash position to retire the final batch of C$172M of the 6.5% senior unsecured notes which had a March 2024 maturity date. The company likely used a combination of cash on hand and an existing credit facility to retire the debt.

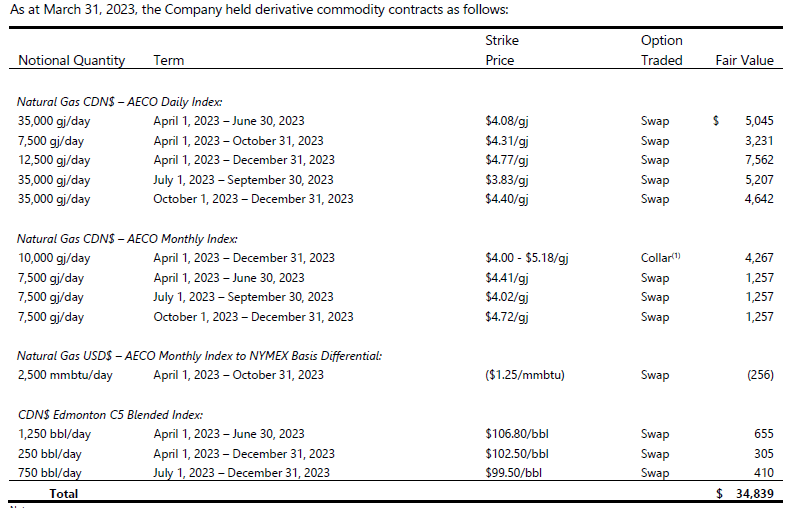

I’m not too worried about the near-term cash flows as the company still has some decent hedges in place which will boost the average realized price (vs. the current market price).

{kind=link}

The company continues to add to its reserves

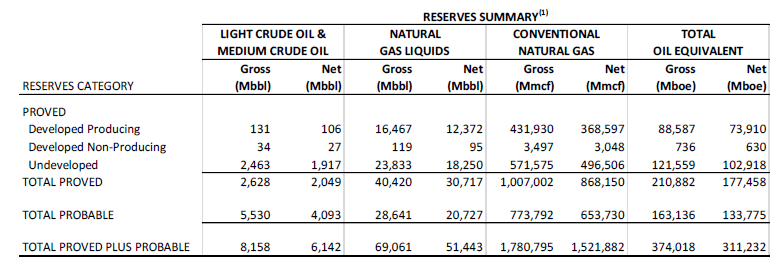

Crew Energy’s year-end reserve update was also positive. As of the end of 2022, the total 2P reserves contained 373 million barrels of oil-equivalent with 311 million barrels net to Crew Energy. Approximately 81% of the oil-equivalent was generated by the natural gas reserves.

{kind=link}

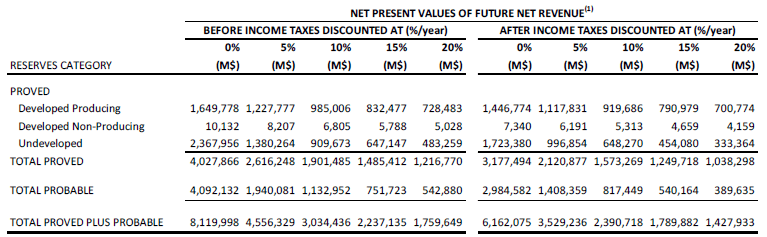

I always like to have a look at the PV10 calculations as well: The sum of the net cash flows discounted by 10% per year. While it isn’t exact science and there are a few variable parameters like the natural gas price and the timing of realizing existing tax assets, it does give investors a pretty good idea of the value of these reserves. According to the official calculation, the after-tax PV10 of the 2P reserves is a very strong C$2.39B. And even using a discount rate of 15% would still result in an after-tax PV10 of around C$1.8B.

{kind=link}

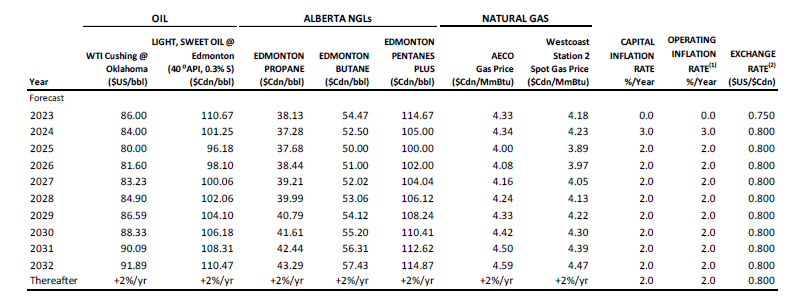

Of course this entire calculation depends on the natural gas price (and oil/NGL/condensate price) used by the company’s independent consultants. And unfortunately the natgas price is pretty optimistic. As you can see below, the base case scenario uses a C$4.33 and C$4.44 average realized price for 2023 and 2024 which is about 20% higher than the average realized price (including hedges!) in the first quarter of this year. While natural gas bulls will be fine with a price higher than C$4 I would have liked to see more conservative parameters.

{kind=link}

Investment thesis

I like the long reserve life index ( 31 years based on the 2P reserves ) and Crew’s low production costs. The C$2.4B in PV10 calculation is attractive but considering the PV10 value was calculated using optimistic natural gas prices I'm a bit more cautious. That being said, even if I would use the PV15 calculation and deduct the approximately C$100M in net debt, the after-tax PV15/share still exceeds C$10/share. And even if you’d apply a 20% discount rate on the future after-tax cash flows you would still end up with an after tax PV20 of C$8.50/share which is about twice the current share price.

Crew is pretty lucky it won’t have to pay taxes in the foreseeable future and the company also made the right decision to have plenty of processing and transportation capacity available (40,000 boe/day vs. the current production rate of about 33,000 boe/day.

I currently have no position in Crew Energy but I may buy shares after receiving the special cash distribution from Spartan Delta ( SDE:CA ) ( OTCPK:DALXF ).

For further details see:

Crew Energy: Waiting For Higher Natural Gas Prices