SKX - Crocs: The Profitable Footwear Juggernaut Returning 15.7%

2023-08-11 09:02:32 ET

Summary

- Crocs, Inc. recently reported strong Q2 results and crossed $1 billion in quarterly revenue for the first time.

- Crocs's track record is extremely strong, with 13 straight quarters of top and bottom-line beats, along with stable, scalable margins.

- Despite this, the company's shares are trading at a discounted valuation compared to historical multiples and peers.

- Selling put contracts on CROX stock may be a less volatile and more lucrative option for investors, generating income and potentially reducing the cost basis in the stock if assigned.

Crocs, Inc. ( CROX ), a well-known player in the apparel sector, stands out in today's investment landscape due to its robust Q2 results and strong overall brand affinity.

In an otherwise murky macroeconomic environment, the company has consistently demonstrated resilience, growth, and good strategic decision-making, proving its worth in our eyes.

Currently, the company's shares trade at an attractive valuation, both relative to its own multiple historically, as well as when compared with peers, which presents a compelling opportunity to opportunistic investors.

However, rather than buying shares outright, a less volatile and potentially more lucrative option may be in play: selling put contracts. This strategy, suitable for a high-quality stock like CROX, can generate income, reduce cost basis in the stock if assigned, and allow investors to benefit even if the stock price remains stable or decreases moderately.

Before explaining more, let's start with a look at CROX's recent financial results.

Financial Results

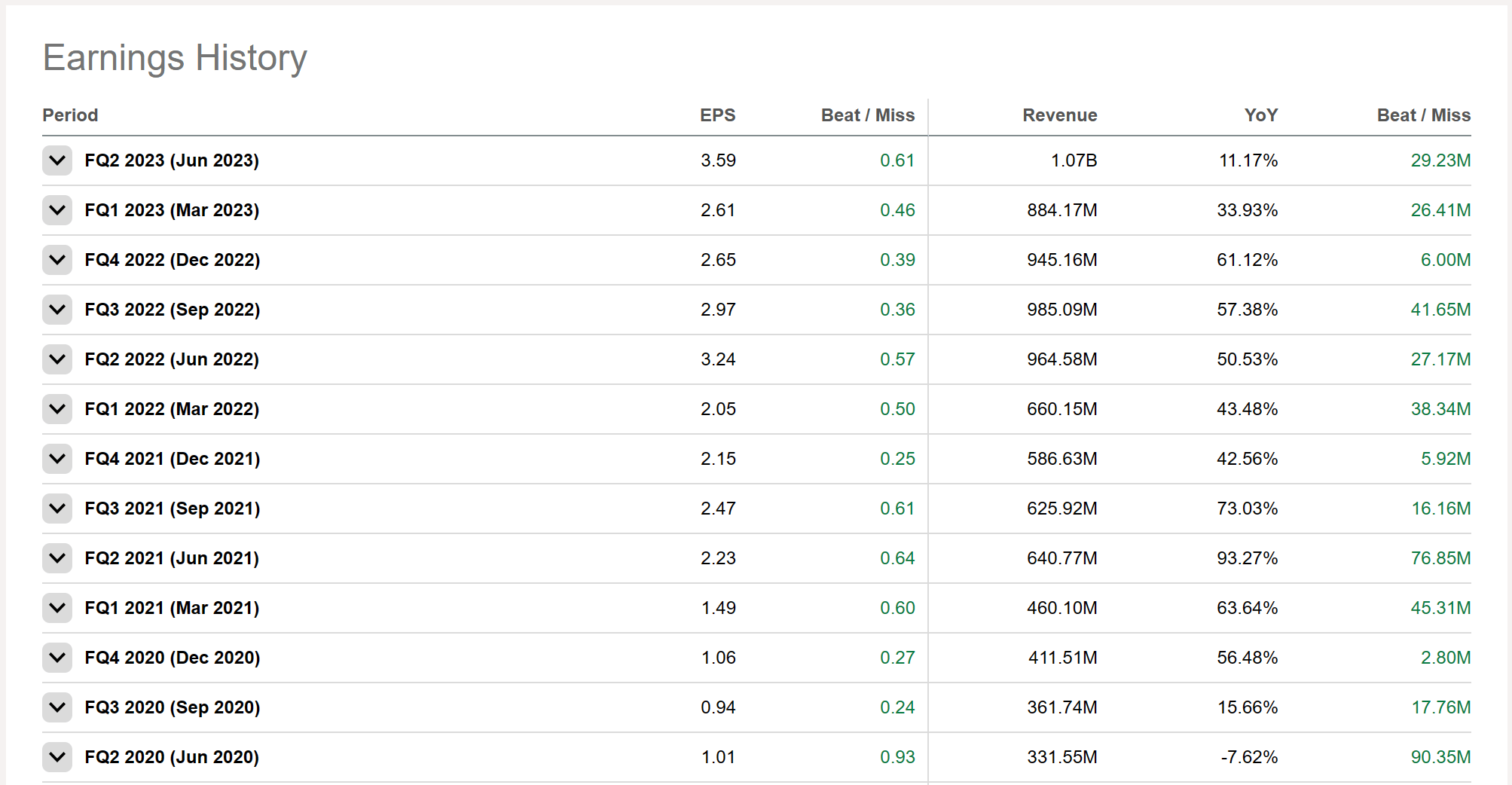

Since the pandemic in 2020, CROX's financial performance has been nothing short of astonishing. Over the last 3 years, the company has quietly grown quarterly revenue from ~$330 million to over $1 billion, while beating EPS and sales expectations for 13 straight quarters:

{kind=link}

This growth appears to be driven by its focused product portfolio and persistent market demand, the latter of which management attributes to continued product innovation and creative marketing arrangements:

{kind=link}

{kind=link}

The latter, specifically, is of particular interest to us. While many brands focus on making themselves the subject of their own marketing, CROX takes a different approach.

As many of the company's products are easily adaptable to clever collaboration (often with minimal new tooling), CROX's footwear acts as a canvas upon which other brands and popular figures can express themselves. These partnerships drive continued cultural relevancy for CROX, which leads to the results we have seen.

The best part is the evergreen nature of this strategy. Fads will come and go, but CROX and its apparel will likely remain relevant well into the future on the back of this unique framework.

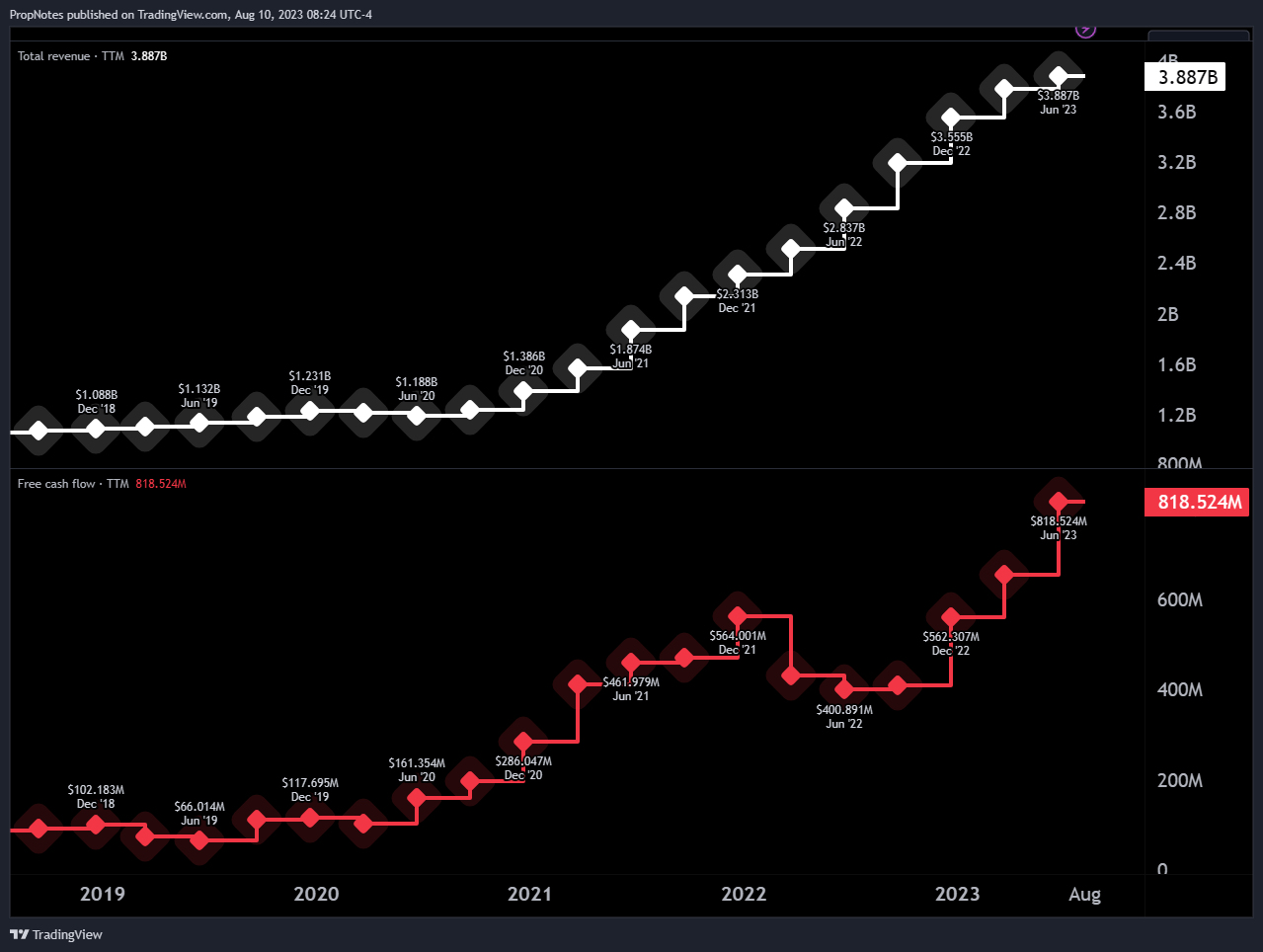

In addition to the top line beats, CROX's free cash flow has also seen a substantial uplift, reaching $818 million over the last twelve months, a clear indicator of the company's healthy operational efficiency:

{kind=link}

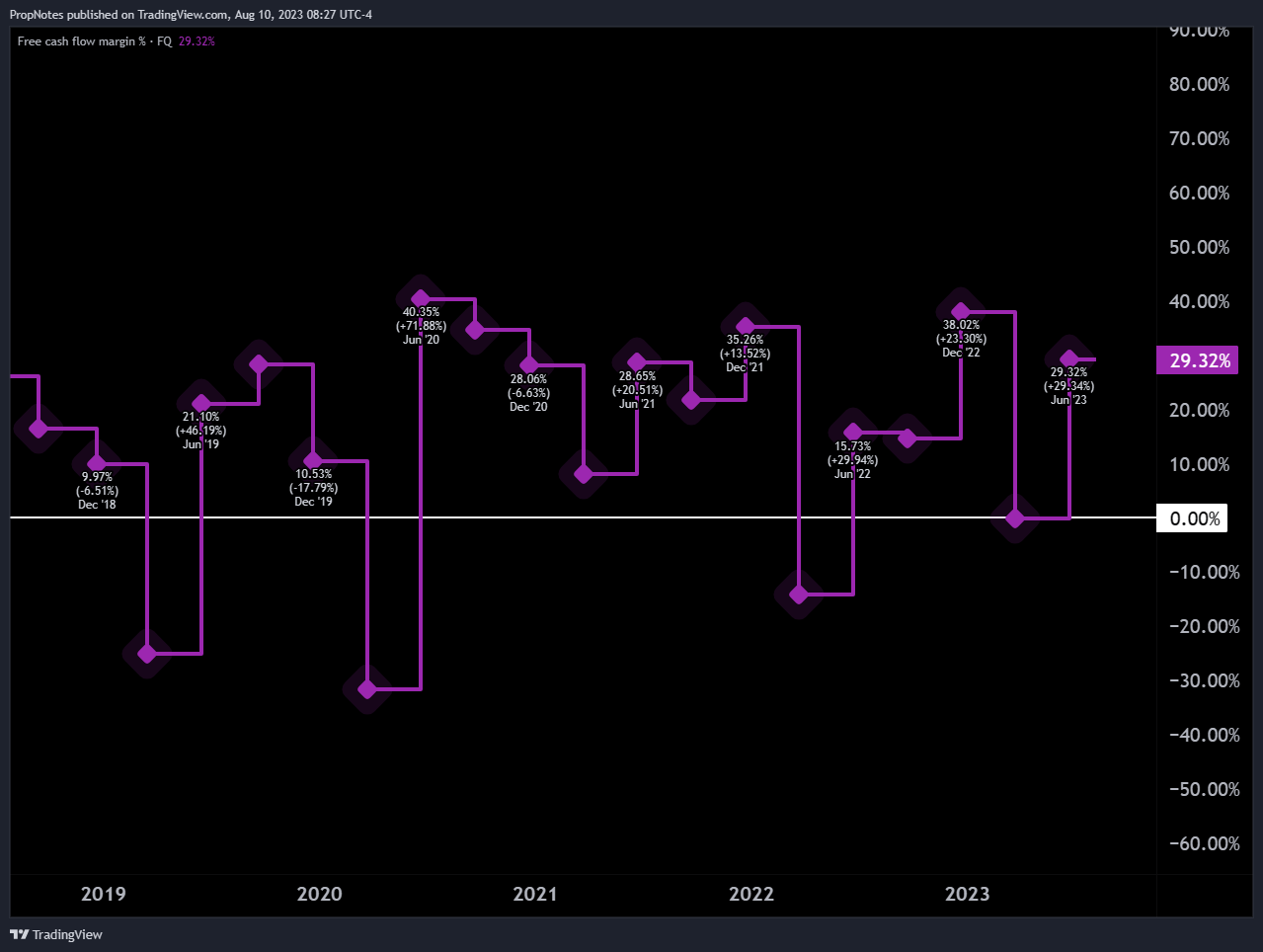

The top line sales growth has been great, but it would mean little if the company wasn't keeping more in profits to return to investors. Thankfully, average margins have stayed mostly stable throughout this period as well:

{kind=link}

This speaks to the company's strong cash conversion and scalability.

On the liquidity front, CROX maintains a solid current assets position of more than $1 billion, ensuring it has the financial flexibility to weather potential bumps.

However, CROX's recent acquisition of HEYDUDE muddied the pristine balance sheet somewhat with around $2 billion in long term debt. The good news is that the company has been paying this back in double-quick time, making more than $500 million in payments to get this down significantly over the last two quarters.

Taken together with the strong growth and profitability, and we think that the company is well positioned for further success.

Valuation

Here's the interesting part.

Given the strength shown in the company's recent earnings, one would probably assume that CROX is trading at a somewhat elevated multiple, but the opposite is true.

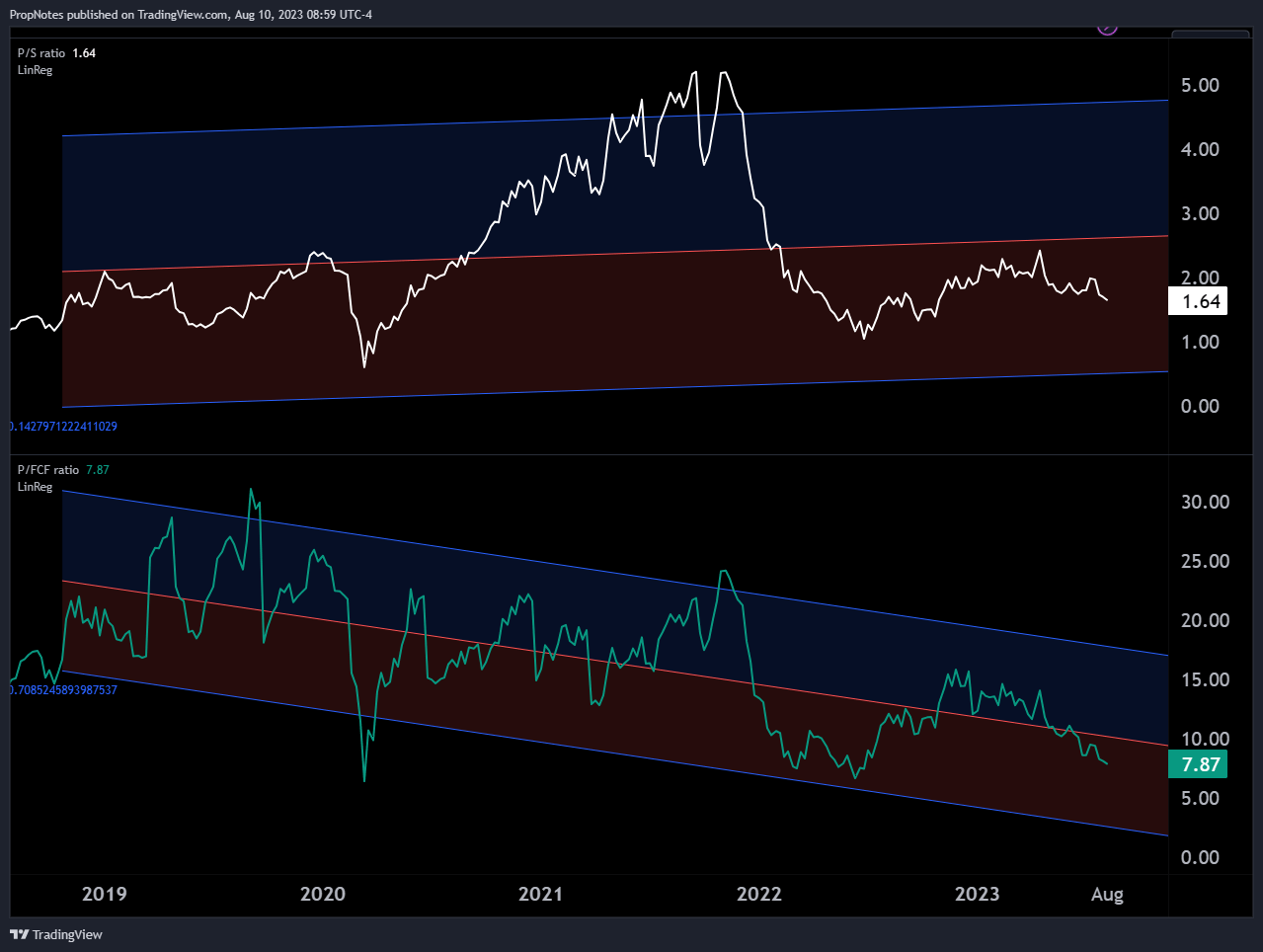

Right now, CROX is trading at 1.6x sales, and 7.8x free cash flow.

{kind=link}

As you can see from the chart above, this places the current multiples squarely on the lower end of the ranges seen over the last 5 years.

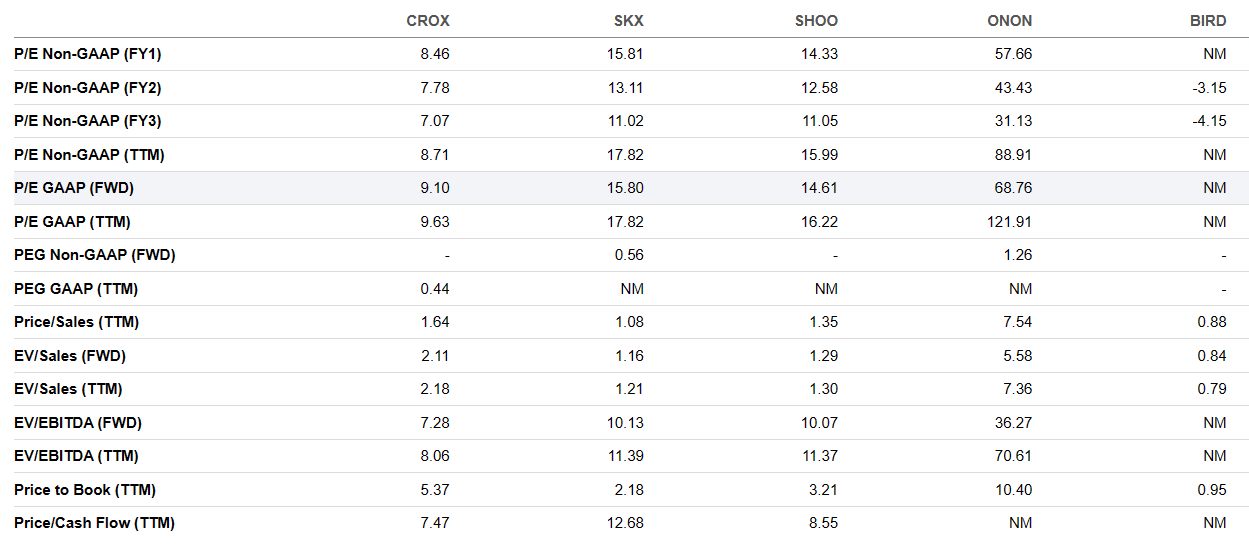

CROX is similarly discounted vs. its peers, like Skechers ( SKX ), On Holding ( ONON ), and Allbirds ( BIRD ):

{kind=link}

With the cheapest P/CF and GAAP P/E, CROX appears to be the most well priced of the bunch.

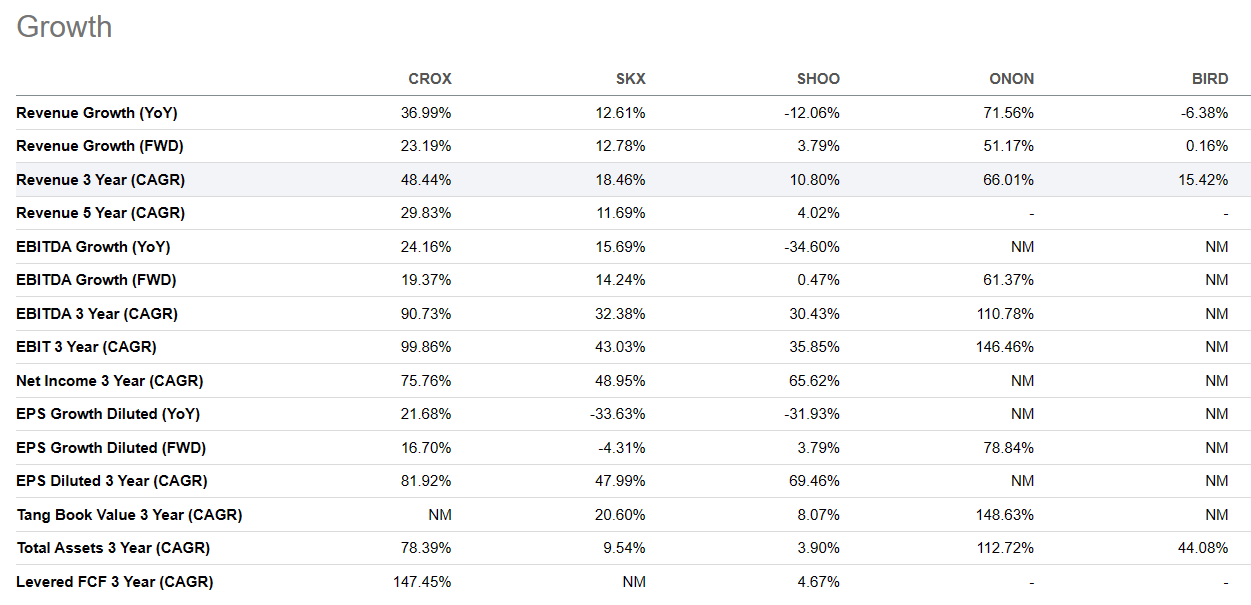

This is especially befuddling given CROX's superior growth profile and aforementioned stable margins:

{kind=link}

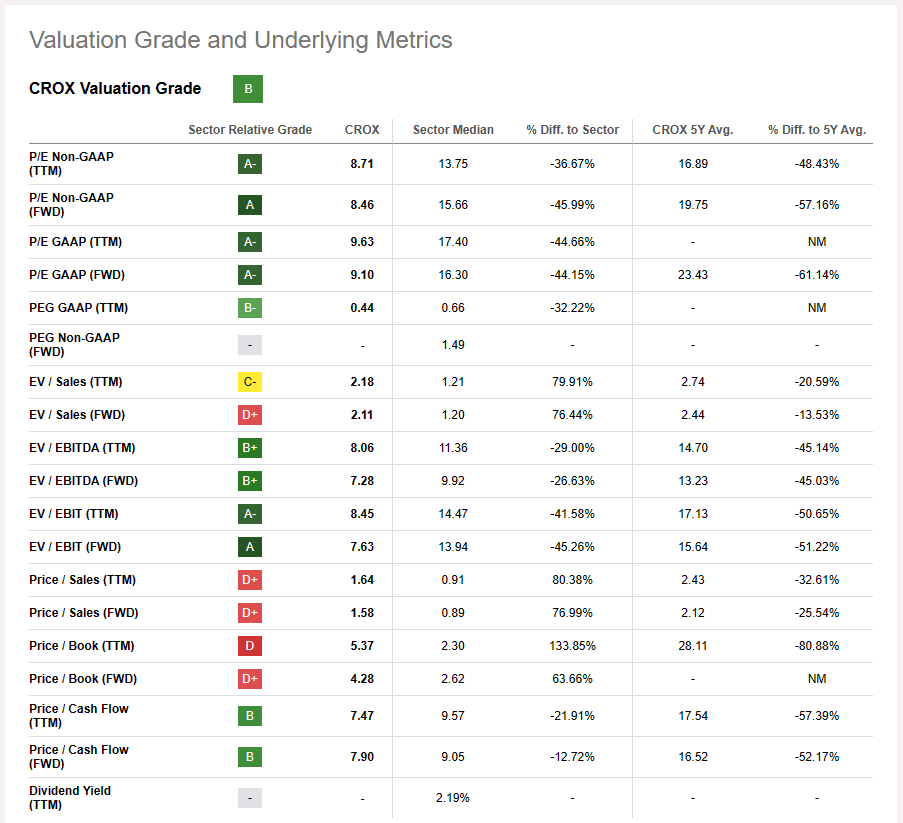

Seeking Alpha's Quant rating system also rates CROX a "B", which we think is fair, if a little low:

{kind=link}

CROX's Price / Book does look a little expensive, but frankly we're not all that concerned about the book multiple when the cash conversion has been strong, and the revenue growth has been robust.

Why the discount?

In our mind, there are two potential reasons for this undervaluation.

The first could be worries about a slowdown in revenue growth. Over the last few quarters, YoY revenue growth has slowed somewhat, which some may expect will continue. This seems natural to us, though, because what footwear company can grow revenues by 30% YoY for any considerable length of time?

This doesn't really matter, either, as the stock is already priced at a value.

Secondly, there could be fears around the company's HEYDUDE acquisition. However, as we addressed before, the debt doesn't appear to be concerning, and the acquisition seems to be performing well:

Earnings Presentation

In short, we don't think the valuation is justified, and net-net, CROX seems like a great company at a great price.

The Trade

As we mentioned before, buying the stock is one option for investors looking to get into this story. However, another, potentially more profitable setup may exist - selling put options.

But how does selling puts work?

When you sell a put option, you're essentially agreeing to buy CROX stock at a certain price (the strike price) before a specified date (the expiration date). If the stock price remains above the strike price, the put option will expire worthless, and you keep the premium you received for selling the option. If the stock price falls below the strike price, you will be obligated to buy the stock, effectively at a discount when factoring in the premium received.

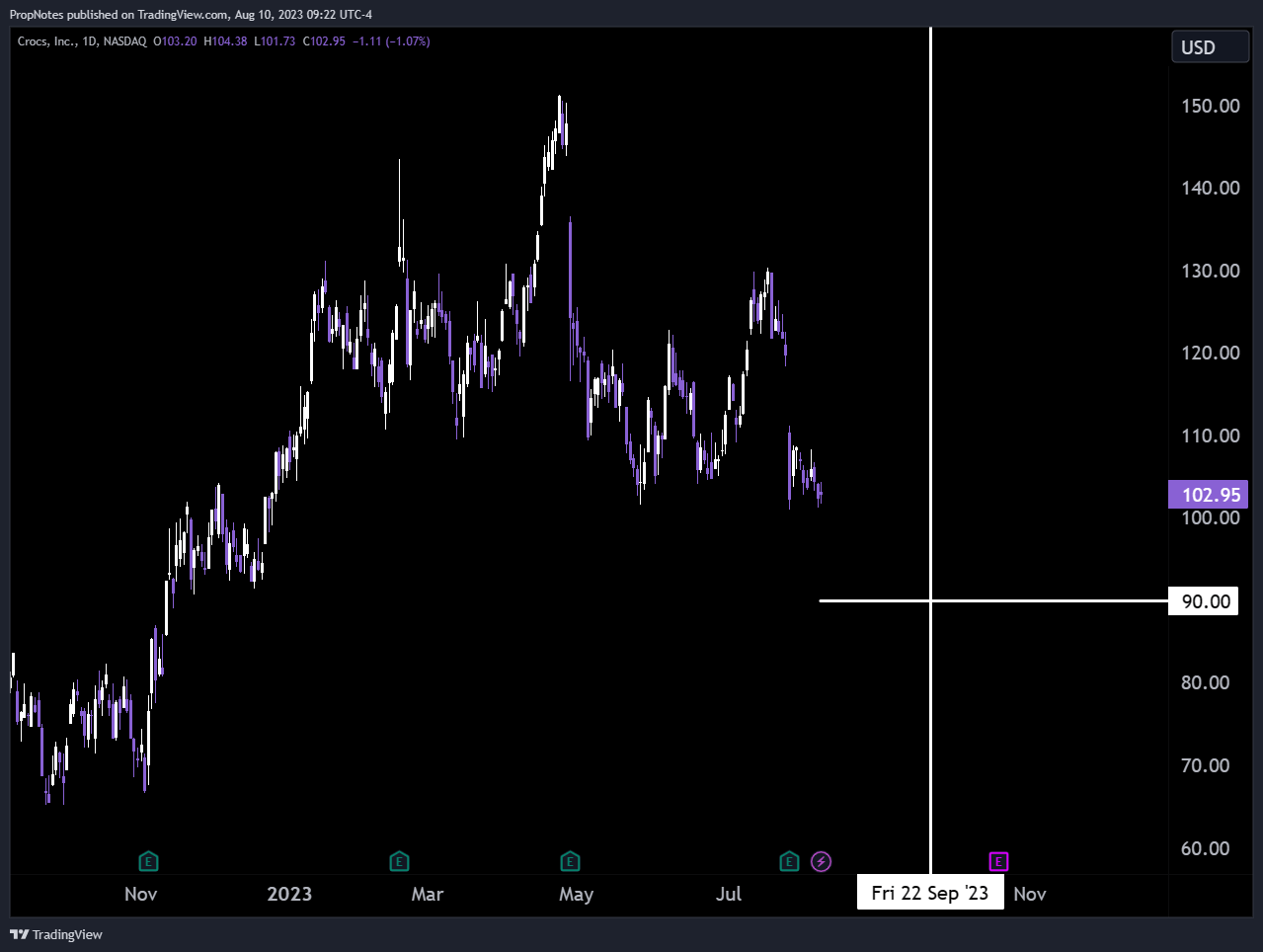

In this case, we like the idea of selling the September 22nd, $90 strike put options:

{kind=link}

They're currently trading at $1.65 per option, which translates to a 1.87% return over the next 43 days ( 15.7% annualized ).

If the stock stays stable or goes up, then it's a profitable trade. If the stock goes down, then you might be obligated to buy the dip in this strong company, which to us seems like a win-win.

Based on the current market volatility and the underlying stock's price behavior, the estimated probability of this trade being successful—i.e., the stock price staying above the strike price until expiration—is approximately 82%.

We think that this probability, coupled with the potential return and discount if assigned, makes selling put options on CROX highly attractive.

Risks

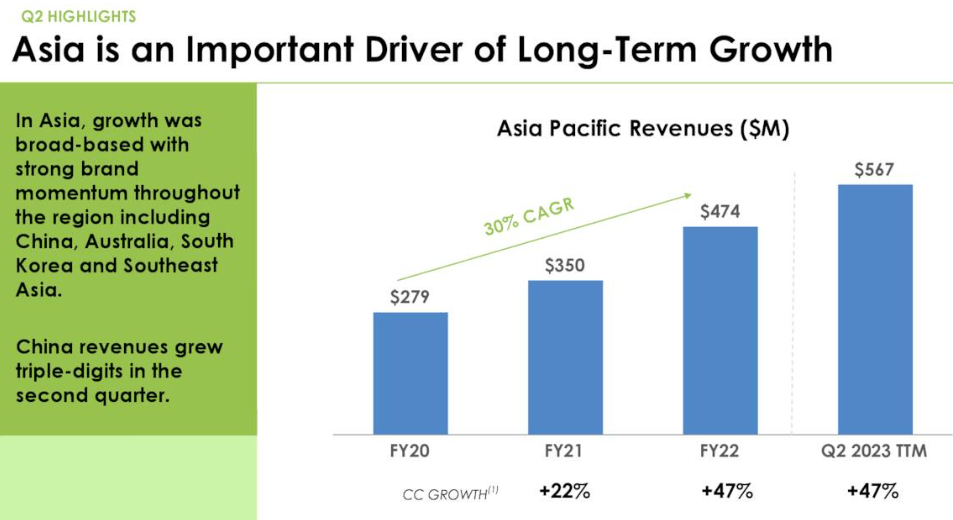

The main risk to this trade, in our view, is CROX's exposure to China.

While China doesn't make up a huge chunk of sales yet, it is one of the faster growing pieces of the CROX story:

{kind=link}

If things get heated with China from a geopolitical standpoint, or trade tensions rise, then CROX's Chinese exposure could suffer. This could, in turn, cause the stock to re-rate lower.

We see this as unlikely to occur in the next 43 days, but it could affect the position long term if shares are assigned.

Summary

In summary, CROX presents a compelling opportunity for investors. Despite some investor unease around the company's recent HEYDUDE acquisition, CROX's solid operational plan, impressive financial performance, and robust cash flow point towards a bright future.

With an attractive valuation well below its historical averages, a solid trade setup offering substantial yield, and a fair balance of risk and reward, CROX is an opportunity worthy of serious consideration.

Cheers!

For further details see:

Crocs: The Profitable Footwear Juggernaut Returning 15.7%