UNP - CSX Q1 Earnings: This Stock Could Go Much Higher

2023-04-21 09:35:49 ET

Summary

- CSX Corporation just reported in Q1 2023 earnings, which came in higher than expected, thanks to strong shipments, pricing benefits, and a lower operating ratio.

- The company saw fantastic improvements in its operations and benefits from supply chain re-shoring investments.

- While macroeconomic challenges remain vicious, I believe that any future correction provides a good buying opportunity for CSX stock, given the company's capabilities and valuation.

Introduction

After discussing the earnings of America's largest independent public railroad company, Union Pacific Corporation ( UNP ), it's time to dive into the earnings of its peer CSX Corporation ( CSX ), the railroad giant which dominates rail transportation in the east with its competitor Norfolk Southern Corporation ( NSC ).

Despite macroeconomic and supply chain-related challenges, CSX reported fantastic Q1 earnings , beating revenue and EPS estimates backed by strong volumes across the board and an outlook that sees positive full-year growth.

I was truly impressed by the numbers and believe that CSX will have a very bright future if it gets support from bottoming economic demand.

In this article, I will put everything into perspective, discuss the bigger picture, walk you through the company's numbers and comments, and explain how I would deal with CSX from a long-term investors' point of view.

So, let's get to it!

Macro Headwinds Keep A Lid On CSX

As usual, I am going to start this article with an overview of the bigger picture and things to keep in mind before discussing the railroad's quarterly earnings.

Roughly one week ago, I wrote an article on CSX covering its new strategy and challenges related to the macroeconomic environment.

Since then, not a lot has happened, except that we're now seeing even more confusion.

For example, I monitor multiple leading (forward-looking) economic indicators. Two of them are the Philadelphia and New York Federal Reserve manufacturing surveys. While both usually move in lockstep, we're seeing a massive divergence in April. New York numbers point at a steep recovery, while Philly numbers do the exact opposite.

Leo Nelissen (Raw Data: Federal Reserve Banks Of New York, Philadelphia)

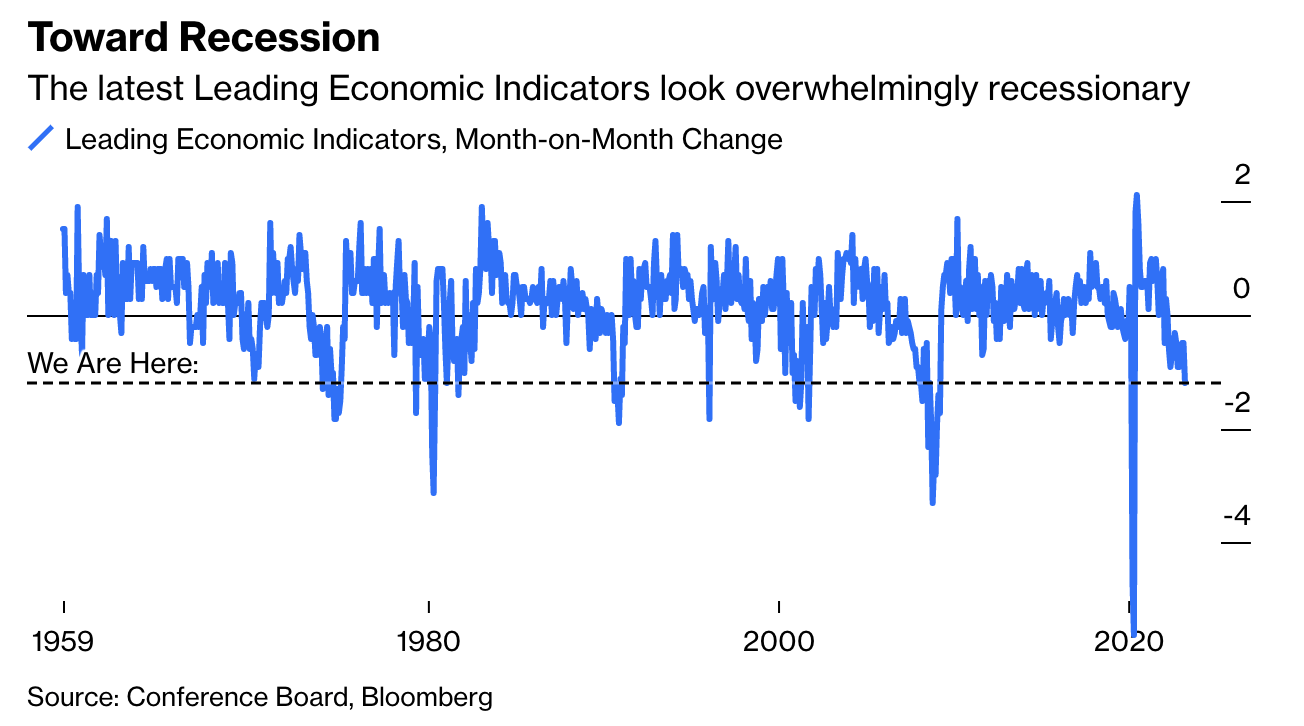

The worst part is that it looks like the Philly Fed index might be right, as other indicators confirm that we're in a downtrend. Not only are jobless claims rising and earnings under fire, but we're seeing that the U.S. leading economic index ((the LEI)) fell to its lowest level since November 2020.

{kind=link}

According to The Conference Board , which publishes this indicator (emphasis added):

The weaknesses among the index’s components were widespread in March and have been so over the past six months, which pushed the growth rate of the LEI deeper into negative territory. Only stock prices and manufacturers’ new orders for consumer goods and materials contributed positively over the last six months. The Conference Board forecasts that economic weakness will intensify and spread more widely throughout the US economy over the coming months, leading to a recession starting in mid-2023.

The Conference Board used the R-word, which is in line with other indicators like the NFIB Small Business Conference Index - and a number of other indicators like the yield curve.

Real Investment Advice

It also didn't help that J.B. Hunt Transport Services, Inc. ( JBHT ), the biggest owner of intermodal containers in North America and a heavyweight in trucking and related services, reported that it saw a mix of negative pricing headwinds and demand issues when it reported earnings earlier this month (emphasis added):

To start, we're in a challenging freight environment where there is deflationary price pressure for an industry that continues to face inflationary cost pressures . Simply stated, we're in a freight recession .

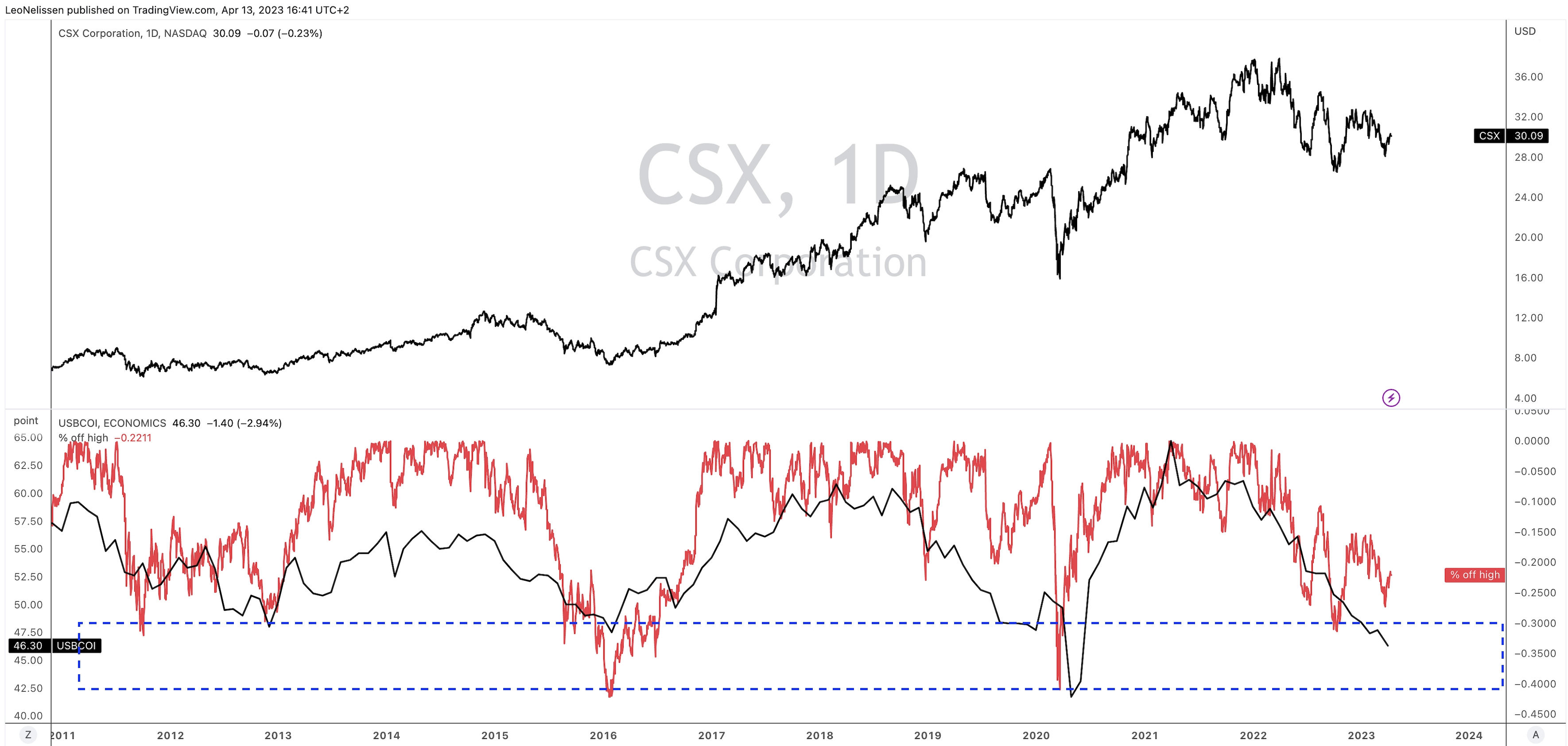

In my prior CSX article, I highlighted what these issues meant for its stock price. I used the chart below, which displays two things:

- Upper part : the upper part of the chart below displays the CSX stock price.

- Lower part : the lower part displays the ISM Manufacturing Index (black line) and the total sell-off from CSX's all-time high.

{kind=link}

With all of this said, we're dealing with a mix of:

- Weakening economic growth and steadily increasing recession odds.

- Sticky inflation, which prevents the Fed from taking its foot off the brake.

- Nervous markets that punish cyclical stocks like CSX.

Based on this context, CSX did extremely well in its first quarter. Not only that, but the company had rather good guidance, and it showed tremendous progress when it came to improving its operations.

CSX's First Quarter - What Happened? And Why Does It Matter?

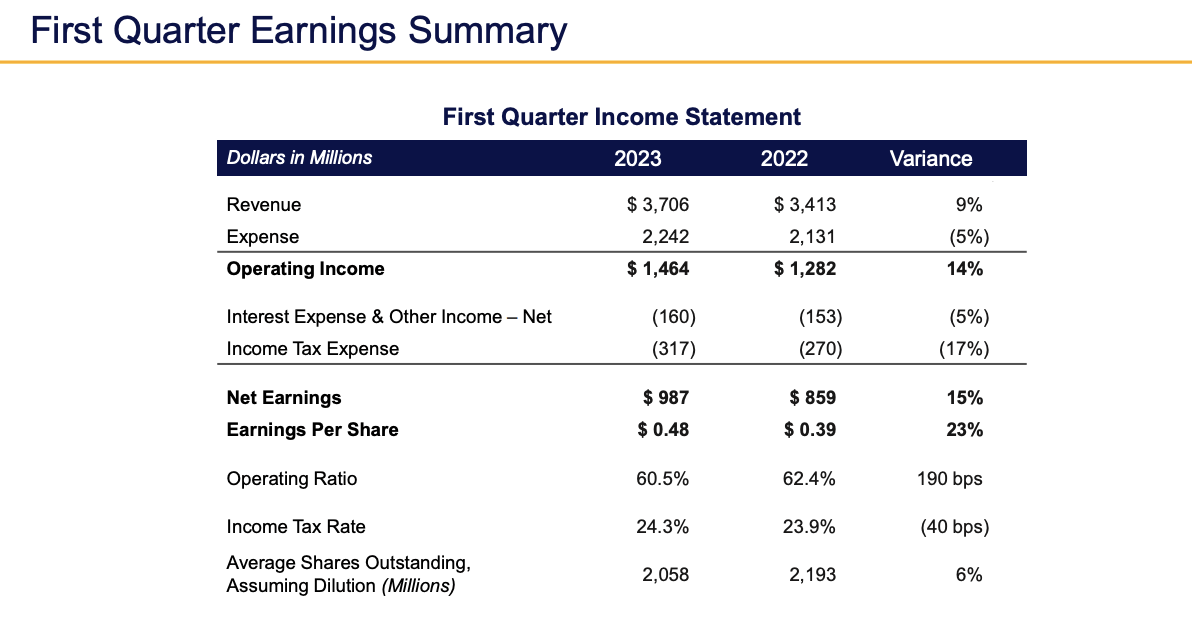

In 1Q23, CSX reported $3.71 billion in revenue, up 8.8% compared to the prior-year quarter and $130 million higher than expected. It allowed the company to boost EPS by 23% to $0.48, which was $0.05 above estimates.

With this in mind, let's dive deeper into the numbers. After all, we want to know what happened and what it could mean going forward.

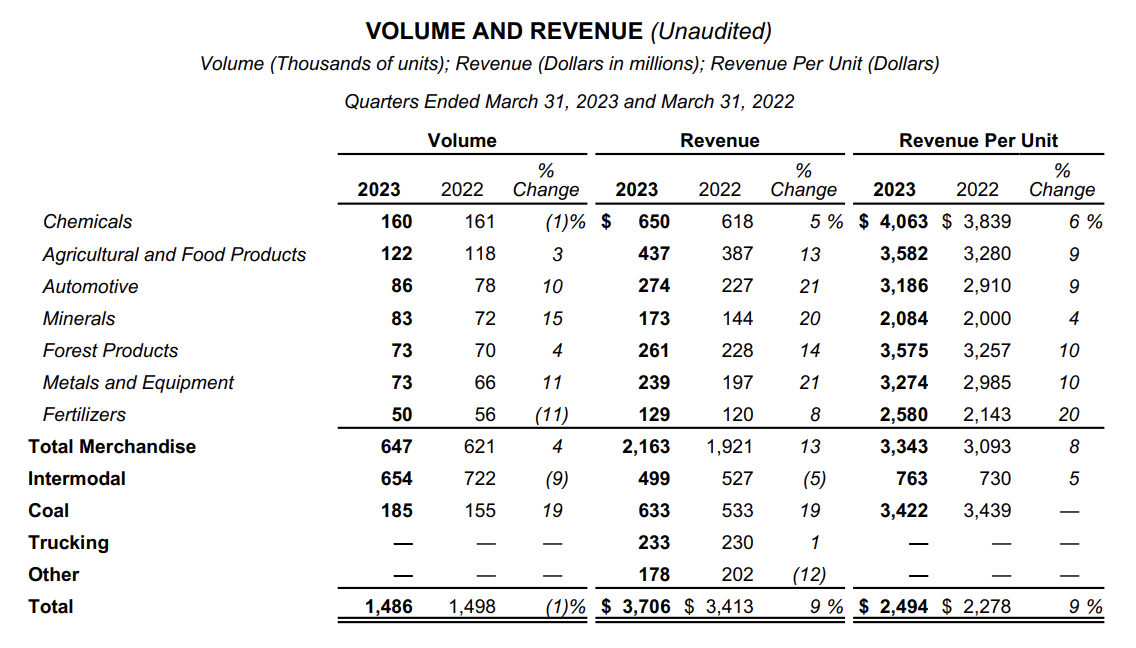

Volumes & Pricing

I have to admit that I was surprised when I saw the company's strong volume performance. Despite economic challenges, total volumes were just 1% lower compared to 1Q22.

{kind=link}

The company reported that the merchandise segment revenue increased by 13%, with a 4% increase in volume and an 8% increase in revenue per unit. Despite customer production issues impacting volumes in the automotive sector, the company expects a strong outlook for automotive volumes for the rest of the year. Additionally, minerals and metals outperformed, with steel demand driving growth, and pricing was up year-over-year.

In the coal sector, revenue increased by 19%, and export volumes were strong, while domestic shipments improved on utility restocking demand and improved rail capacity. The international coal market is expected to be supported by healthy commodity prices that should drive positive year-over-year volume growth through the rest of the year. However, the domestic market could face a more challenging backdrop if natural gas prices remain low. My personal opinion is that natural gas is likely to benefit from long-term tailwinds, which are likely to keep (global) coal demand higher than expected.

Intermodal revenue decreased by 5%, mainly due to weakness in international intermodal markets affected by slowing import activity and elevated retail inventories. The CSX team has initiatives underway to continue to drive truck conversion by introducing new lanes of service where there is market demand. That's a smart move, as it cannot change the fact that consumer weakness and supply chain-related inventory de-stocking are hurting intermodal volumes.

That said, the company is also encouraged by its ability to convert improved service into new business wins and gain wallet share with existing customers. This was something I also mentioned in my prior article, and I'm glad that this strategy is seeing strong results already.

Furthermore, with regard to pricing, CSX expects to continue to see benefits from a supportive pricing environment and improved rail service. It also sees a significant opportunity to win market share back from the trucking industry across the company's merchandise portfolio. This is also something I've highlighted in the past, as (well-run!) should be in a good spot to exploit secular challenges in the trucking industry.

Supply Chain Re-Shoring

Another hot topic we frequently discuss is supply chain re-shoring. The pandemic has triggered the need to de-risk supply chains, which is fueled by highly unfavorable business conditions in regions like Europe. This is benefiting North America tremendously.

- North America is home to the largest group of consumers in the world.

- It has access to affordable energy and a wide range of commodities.

- It benefits from companies leaving China due to political and economic risks.

- European de-industrialization is benefiting North America.

- The Biden Administration is further fueling this trend through subsidies (i.e., the Inflation Reduction Act).

{kind=link}

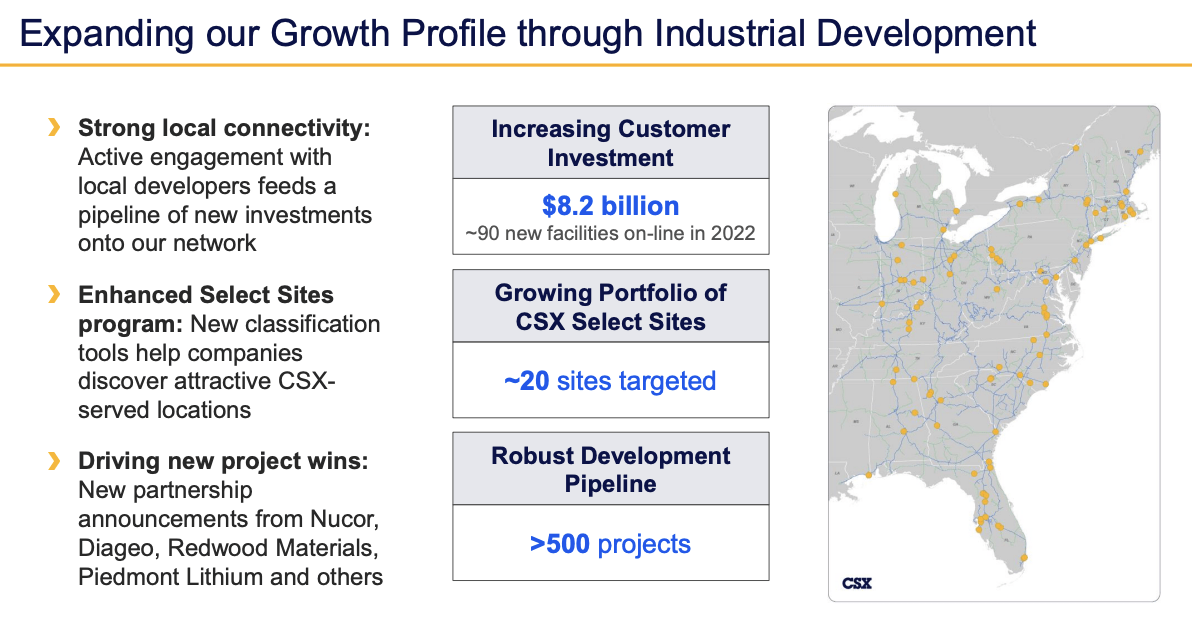

Kevin Boone, EVP and Chief of Sales & Marketing at CSX, discussed the company's industrial development opportunities in its earnings call . As more companies look to diversify their supply chain and bring capacity closer to their key end markets (re-shoring), CSX sees a great opportunity to capitalize on that. The company's industrial development team aims to partner with these companies and provide them with a rail service location where they can leverage the benefits of the CSX network and industry-leading service. Boone reported that in 2022 alone, CSX's customer partners brought nearly 90 new facilities online, representing $8.2 billion of total investment across the company's network and on its short-line partners. The pipeline remains robust, with over 500 projects in process across the entire industrial development pipeline. Boone believes that over time, these projects will represent a key driver to the company's growth algorithm as they help their partners bring in an increasing number of expansion projects onto the CSX network, driving volumes and revenue higher.

That's big news, and it confirms that I'm betting on the right horse by making rails a cornerstone of my portfolio and supply chain re-shoring thesis.

Operations And Cost Management

While we already briefly discussed that CSX sees improving pricing power, we need to focus on operating expenses and network fluidity. After the pandemic, railroads struggled with increased demand and lower employee and material levels. Furthermore, the past two years came with high inflation, which made it impossible to improve the operating ratio.

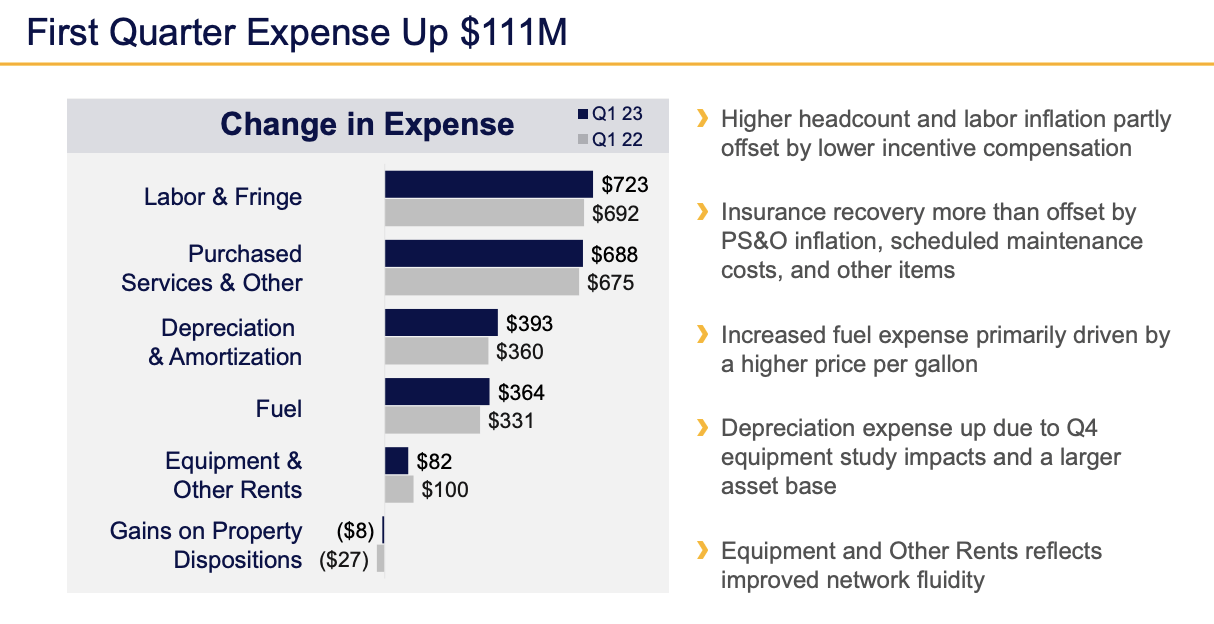

The good news is that despite challenges, CSX improved its operating ratio from 62.4% in 1Q22 to 60.5% in 1Q23. This was the result of just 5% higher operating expenses, which underperformed the aforementioned revenue growth rate of 9%.

{kind=link}

Here's an overview of changes in costs and management comments:

{kind=link}

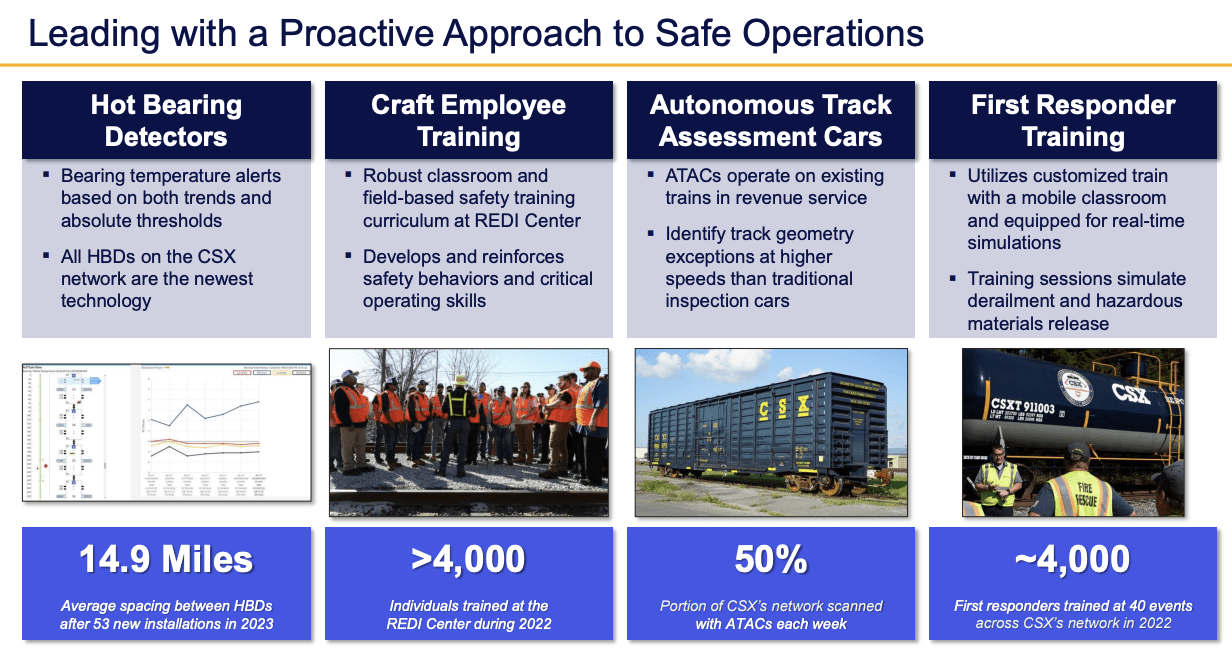

In light of the Norfolk Southern derailment in Ohio earlier this year, CSX is taking proactive steps to ensure network safety, including installing additional hot box detectors, integrating safety culture into employee training, using autonomous track assessment cars, and developing relationships with first responders in the communities in which they operate.

{kind=link}

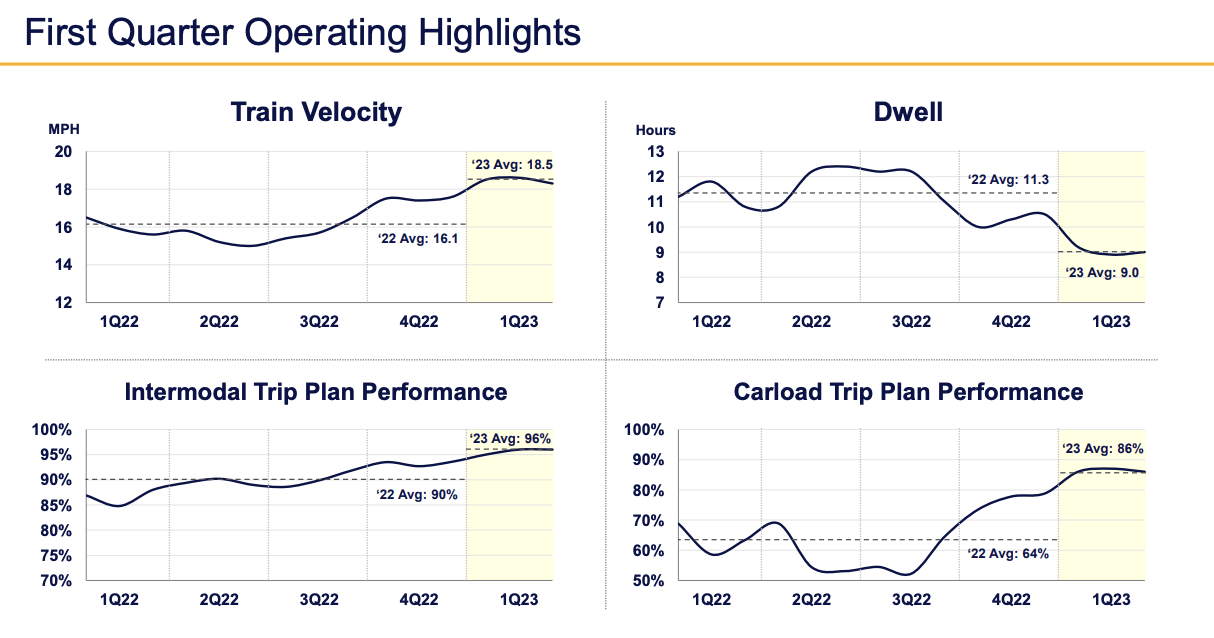

Furthermore, operating performance has significantly improved, with carload trip performance reaching an all-time record level and intermodal trip plan performance matching a record high. The company aims to sustain these service improvements to drive long-term growth.

{kind=link}

Based on this context, while CSX is less dependent on intermodal supply chains, it has done a tremendous job improving operations, and I have little doubt that it will help them to win new business deals going forward.

So, with that said, what about the outlook?

CSX's Outlook Is Good - Given The Circumstances

During CSX's 1Q23 earnings call , CEO Joseph Hinrichs discussed the company's outlook for the year ahead. He expressed satisfaction with the strong performance of the merchandise business, which has seen a surge in demand for grains, metals, minerals, automotive products, and new business wins related to improved operations and the aforementioned re-shoring benefits.

However, the intermodal business has performed below expectations due to reduced international activity and elevated inventory levels, which is related to consumer weakness (pictured below). This has led to slower volume growth for the quarter, which may make it challenging for CSX to meet its previous guidance and grow faster than GDP.

{kind=link}

Nonetheless, Hinrichs remained optimistic about the company's future, emphasizing its efforts to drive efficiency, reduce excess costs, and increase merchandise volume. He also highlighted the company's commitment to providing safe and reliable service to customers and driving profitable growth.

With this in mind, the company expects low-single-digit revenue ton-mile growth on a full-year basis. I did not expect this. While I expect downward revisions unless economic growth expectations bottom, I believe these expectations display the company's progress and success despite challenges.

Shareholder Benefits & CSX Stock Valuation

In 1Q23 , the company generated $816 million in free cash flow (excluding $232 million in retroactive payouts to employees). Without these factors, the company would have increased total free cash flow versus 1Q22.

As a result, the company was able to stick to high buybacks, reducing its share count by 6%, as it bought back shares worth $1.1 billion. It paid $226 million in dividends. This includes a 10% dividend hike announced on February 15.

The company currently yields 1.4%. Its payout ratio is just 21%.

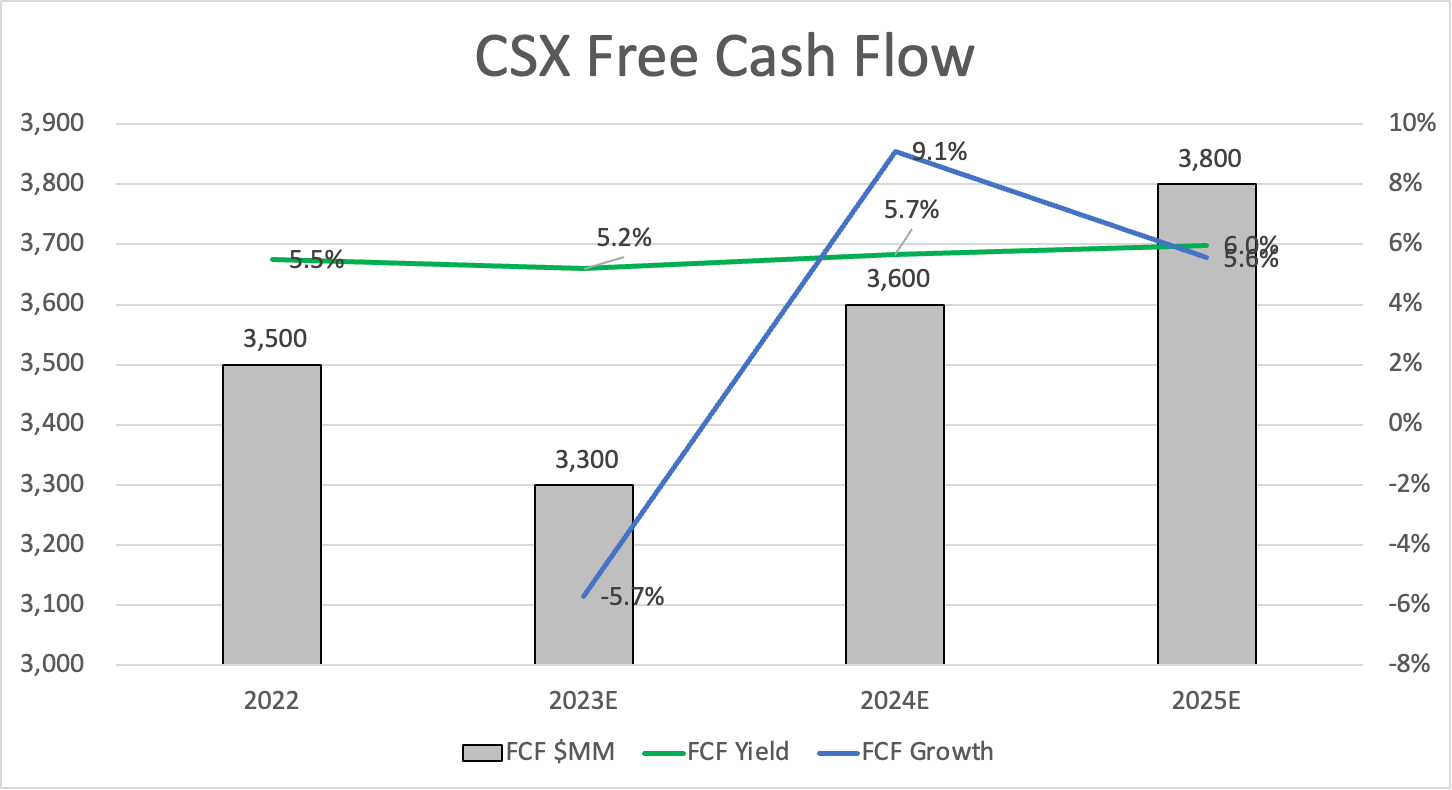

This year, the company is expected to generate $3.3 billion in free cash flow. That number is expected to rise to $3.6 billion in 2024 and $3.8 billion in 2025. This implies a lot of room to further hike the dividend and engage in buybacks. The balance sheet supports these buybacks. The 2023 net debt ratio is expected to be just 2x EBITDA. The company's balance sheet has a BBB+ rating.

{kind=link}

It also helps the valuation. The company is trading at 19.3x 2023E free cash flow. That's a fair valuation.

The same goes for its EV/EBITDA multiple, which is now in fair value territory.

While the stock is up close to 3% after its earnings release, I stick to what I wrote in my prior article:

[...] there's a downside risk to $25 if economic growth triggers a bigger sell-off - especially in the cyclical space.

In other words, if I did not have three other railroads, I would be a buyer at these levels. However, I would buy gradually, as I believe in a high probability of lower prices in the months ahead.

FINVIZ

Essentially, it's the same thing I wrote in my UNP article. We're not out of the woods yet, but we're at prices that warrant careful buying.

Takeaway

While macroeconomic circumstances are terrible, I'm impressed by CSX's results. The new CEO, Joseph Hinrichs, presented fantastic results as the company benefits from secular tailwinds boosting shipments, improving pricing power helping to grow revenue, and an impressive improvement in service levels.

The company is winning new clients and benefiting from billions worth of investments related to supply chain re-shoring efforts.

While the economy is not out of the woods (far from it), CSX believes it can grow its sales this year.

That said, ongoing economic challenges could provide us with one more correction, which I would use to buy CSX shares if I didn't own three other railroads already. If current business improvements are further supported by recovering economic demand, I have little doubt that CSX shares will move much higher, along with its dividend and buybacks.

So, if you're in the market for a high-quality transportation stock, CSX might be right for you.

For further details see:

CSX Q1 Earnings: This Stock Could Go Much Higher