CA - CT REIT: A 6.1% Yield With A Sub-75% Payout Ratio

2023-06-19 10:00:00 ET

Summary

- CT REIT saw its AFFO increase by more than 6% and is on track to generate C$1.15-1.20 in AFFO per share this year.

- This means the stock is trading at less than 13 times the AFFO.

- The payout ratio is just 75% which means CT REIT is retaining plenty of cash to fund additional investments and/or strengthen its balance sheet.

- The majority of its debt has a fixed rate interest component, and maturity dates are well spread out in time.

- I expect rent hikes to completely cover the impact of interest expense increases in the next three years.

Introduction

I like commercial REITs that have a strong relationship with their main tenant. I specifically like the few grocery-anchored REITs like Choice Properties where the REIT and the main tenant have the same controlling shareholder. Another REIT I’d put in this category is CT REIT ( CRT.UN:CA ) ( CTRRF ), where the ‘CT’ stands for ‘Canadian Tire’ . Indeed, Canadian Tire ( CTC.A:CA ) ( CDNAF ) ( CDNTF ) is the main tenant of CT REIT (representing almost 80% of the total base rent in FY 2022), and it is the REIT’s largest shareholder as well. Needless to say, these strong ties between the companies indicate the retention rate of the largest tenant is superior. I discussed Canadian Tire in another article here .

The FFO and AFFO continue to increase

Before moving over to the FFO and AFFO result of CT REIT in the first quarter, I wanted to spend a few minutes on the income statement as this contains interesting information on the NOI and how the interest expenses are evolving.

{kind=link}

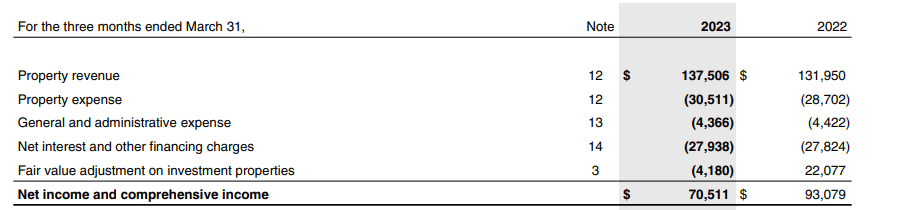

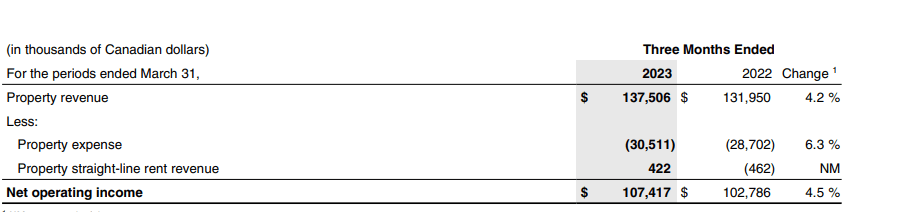

As you can see above, the REIT reported a total revenue of C$137.5M and expenses of C$30.5M for a net property result of C$107M. The NOI was slightly higher than C$107M due to the addition of about C$0.4M in straight-line rent revenue provisions. As you can see below, CT REIT saw its property Net Operating Income increase by approximately 4.5% compared to the first quarter of 2022.

{kind=link}

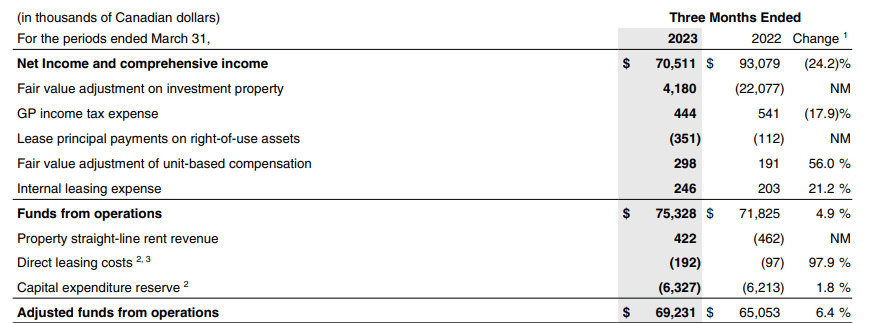

That’s great, mainly because the REIT’s interest expenses barely changed at all. And as the G&A expenses also remained very stable, I had high hopes for an FFO and AFFO improvement based on the income statement. While the C$70.5M in net income is irrelevant as it includes the changes in the property valuations, it does provide the starting point of the FFO calculation, which you can find below.

{kind=link}

The FFO increased by almost 5% to C$75.3M while the AFFO increased at an even more impressive 6.4% to C$69.2M . As there are currently 235M units outstanding (including the impact of the Class B LP Units which can be converted into common units), the FFO and AFFO per share came in at C$0.32 and C$0.29 respectively.

{kind=link}

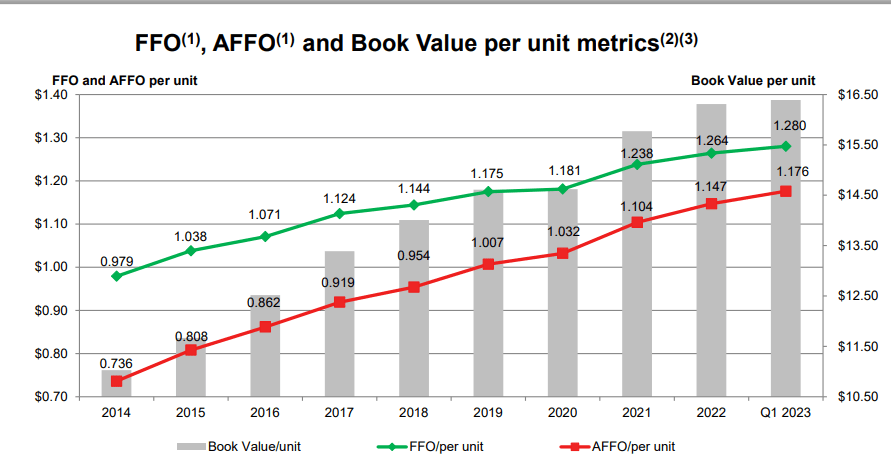

This means that on an annualized basis, CT REIT seems to be well underway to report an AFFO per share of C$1.15-1.20. This indicates CT REIT’s impressive growth trajectory will likely just continue. Just half a decade ago, the annualized AFFO/share was just C$0.92, and this will likely increase by about 30% by the time the current year is over.

{kind=link}

The conservative balance sheet means the increasing interest rates will be manageable

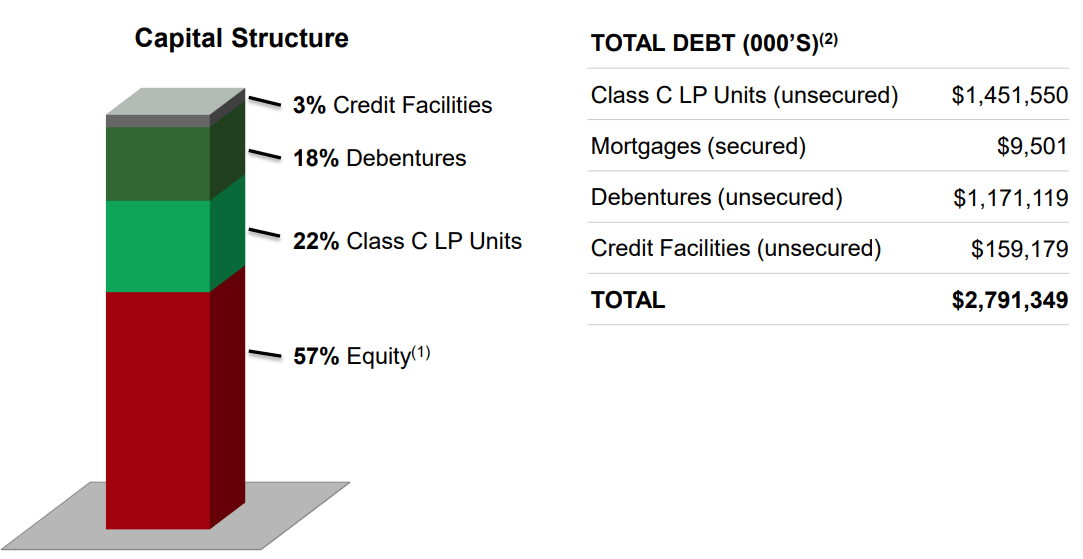

The most impressive element of the steady AFFO growth is the way CT REIT manages its balance sheet. While the cheap debt was very appealing for other REITs, CT REIT continued to focus on running a very robust balance sheet. As you can see below, about 57% of the balance sheet consists of equity, and not mortgages or debentures but Class C LP Units are the main source of debt funding.

{kind=link}

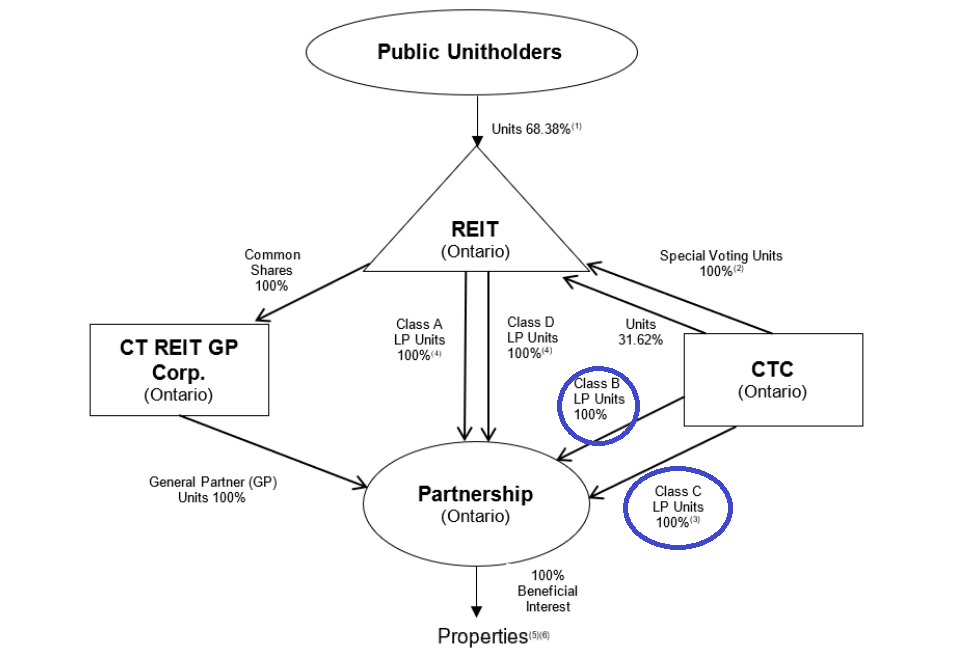

An important part of the financing structure comes from the Class C LP Units, which are all held by Canadian Tire (see below).

{kind=link}

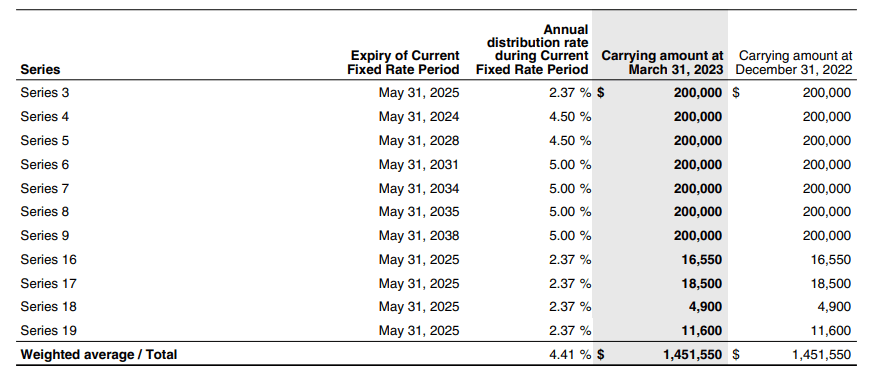

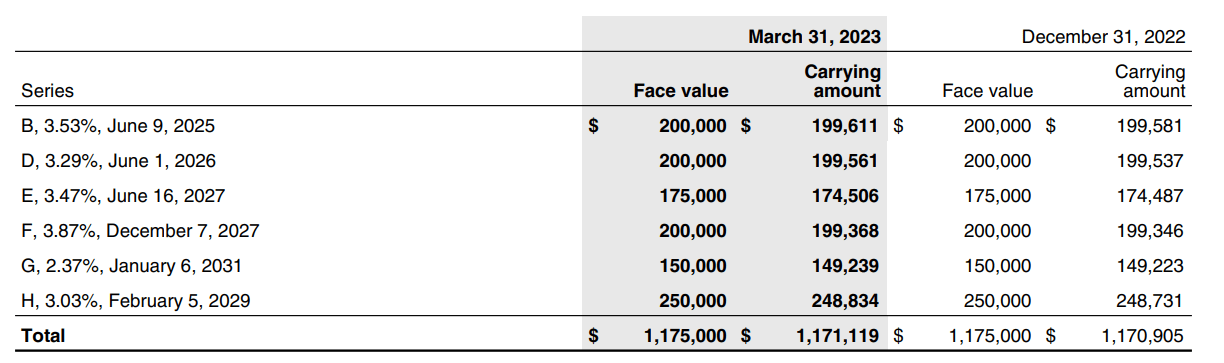

Although these are added to the balance sheet as a liability, one could argue to consider these units to be some sort of preferred equity. However, as the partners owning the units can request the REIT to redeem them every five years, they are classified as a liability. As you can see below, the average weighted distribution rate is approximately 4.41%. And as you can see below, most of these securities have a fixed rate period for in excess of half a decade. In excess of half of the Class C units has a fixed interest rate until well into the 2030s.

{kind=link}

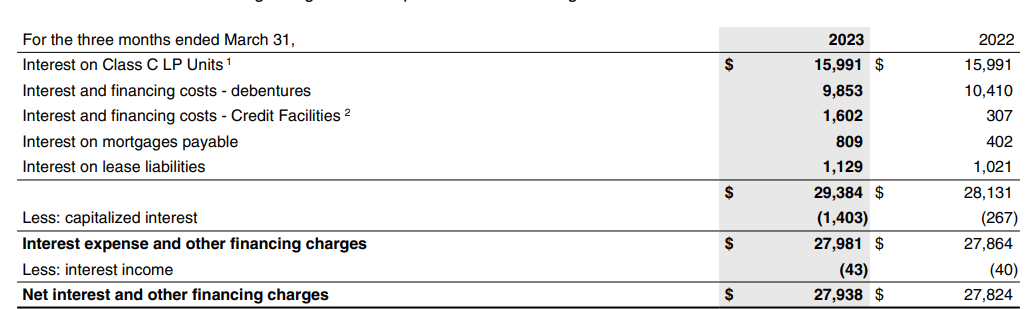

Please note, the payments on these securities are classified as an interest expense and are included in the total interest expenses, as you can see below.

{kind=link}

It’s also important to note the vast majority of the debt has a fixed interest rate. Only the credit facility (C$159M drawn as of the end of Q1, C$99M as of the end of FY 2022) has a variable interest rate, and that explains the increase in interest expenses on the image above).

CT REIT also did a phenomenal job in locking in the low interest rates for its debentures. The average cost of debt of its debentures was 3.28%, and that helped to keep the consolidated average cost of debt relatively low, to just 3.9%.

{kind=link}

And just like the Class C LP Units, the refinancing dates are nicely spread out in time. Within the next three years, the REIT only has to refinance C$400M in debentures (with a weighted cost of capital of 3.41%) and C$450M in Class C LP Units (with a weighted cost of capital of 3.32%).

Even if we would assume the total cost of debt will increase to 6% (I think it might be lower as CT REIT could elect to refinance its unsecured debentures with mortgages or other secured financial instruments to reduce the cost of capital), the annual interest expenses will increase by C$23M per year. That’s less than C$6M per quarter and represents just 5.5% of the current Net Operating Income. Which means I am fairly confident in CT REIT being able to hike the rental income and thus boost its net operating income at a faster pace than the interest expenses will increase.

Just to give you an example, if I would assume a 3% rent hike in 2024, 2.5% in 2025 and 2% in 2026, the NOI would increase from C$430M per year to C$463M. And that C$33M increase in NOI should be more than sufficient to cover the impact of the higher interest rates.

Investment thesis

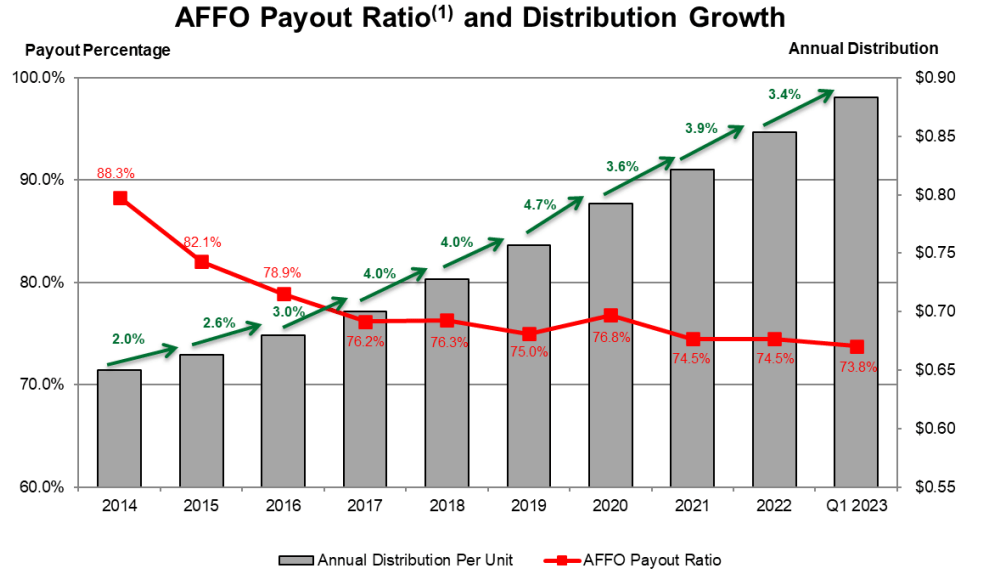

This also means I’m not worried about the current dividend coverage levels. As CT REIT hiked distributions at a slower pace than its AFFO growth (see below), its payout ratio has continued to decrease.

{kind=link}

The REIT recently hiked its distribution to C$0.0749 per month (a 3.6% increase) and the almost C$0.90 per share per year now represents a yield of 6.07%.

The strong ties with Canadian Tire are positive as it means the main tenant which accounts for 80% of the rental income will likely stick around. Canadian Tire owns 100% of the Class B and Class C LP Units and almost 32% of the common units but there doesn’t appear to be a conflict of interest as CT REIT has been able to hike the rent it charges Canadian Tire in an orderly fashion.

The stock is currently trading at less than 13 times its anticipated AFFO and at less than 12 times the AFFO of C$1.25 I’m expecting for next year. Combined with a robust balance sheet and a well-covered dividend, I think CT REIT is a strong buy down here.

I have a small long position in CT REIT but will likely add to this position within the next few weeks as I feel adding to CT REIT is a more opportune move than adding to my Plaza Retail position due to CT’s stronger balance sheet and the anticipated smaller short-term impact of increasing interest rates.

For further details see:

CT REIT: A 6.1% Yield With A Sub-75% Payout Ratio