CA - CT REIT: The 6.1% Yield Will Continue To Increase Despite Higher Interest Expenses

2023-09-05 10:30:00 ET

Summary

- CT REIT has a strong anchor tenant, Canadian Tire Group, accounting for 80% of base rent.

- The REIT reported a 6% increase in NOI and a 7.6% increase in AFFO in the second quarter.

- CT REIT has a conservative balance sheet, low payout ratio, and plans for further development, making it an attractive investment.

Introduction

I like commercial REITs that have a very strong anchor tenant with a vested interest in remaining a tenant of the REIT. And that’s the main reason why I thought CT REIT ( CRT.UN:CA ) ( CTRRF ) was a strong buy the last time I discussed the REIT. Its largest shareholder and largest tenant is the Canadian Tire Corporation ( CTC.A:CA ) ( CDNAF ) ( CDNTF ), which accounted for about 80% of the base rent last year.

A satisfying FFO and AFFO result

As of the end of June, CT REIT had 371 operating properties and two development properties as one asset moved from the development stage to the operating stage subsequent to the completion of a C$70M investment. As you can see below, the vast majority of the GLA is located in Ontario and Quebec.

CT REIT Investor Relations

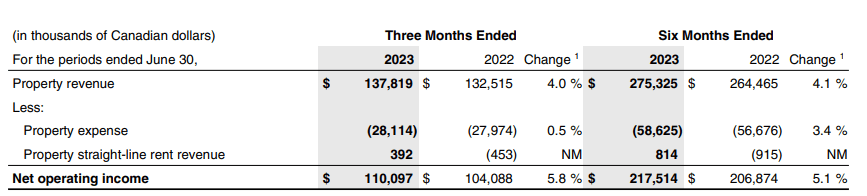

When looking at CT REIT, I obviously want to make sure the REIT is able to charge market rents to its main tenant and shareholder to make sure there’s nothing suspicious going on that could have a negative impact on the shareholder value. The first step is to have a look at the Net Operating Income. As you can see below, the REIT reported an increase of approximately 6% in its NOI in the second quarter of the year as the NOI increased to C$110.1M.

{kind=link}

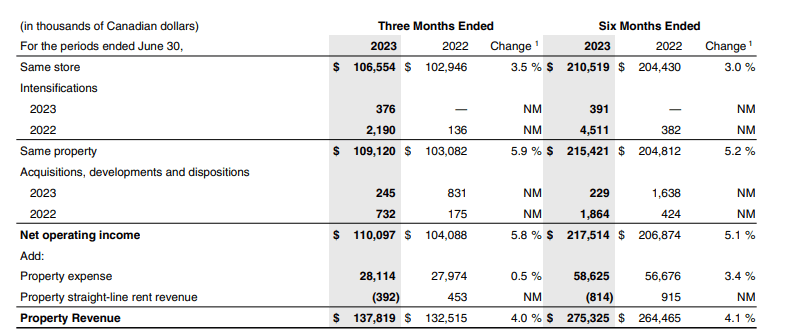

And as you can see below, there was a 3.5% NOI increase on the same store level while the intensifications added a few million Canadian Dollar in additional NOI as well.

{kind=link}

As we see a substantial increase in the Net Operating Income, it’s only fair to also expect a similar increase in the FFO and AFFO result. The only issue there would be increasing interest rates having a negative impact, but as CT REIT has fixed rate debt, this is not an issue for the REIT.

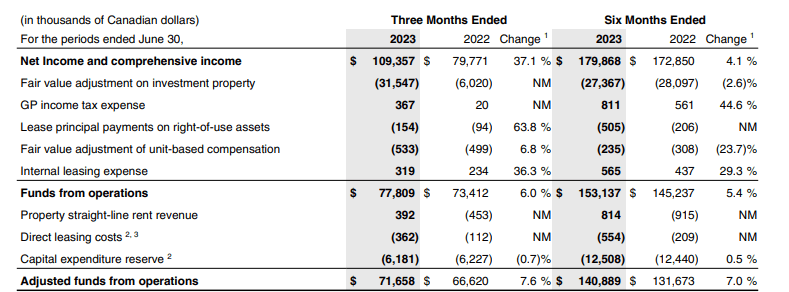

As you can see below, the FFO increased by about 6% to C$77.8M while the AFFO increased by a very strong 7.6% to C$71.7M.

{kind=link}

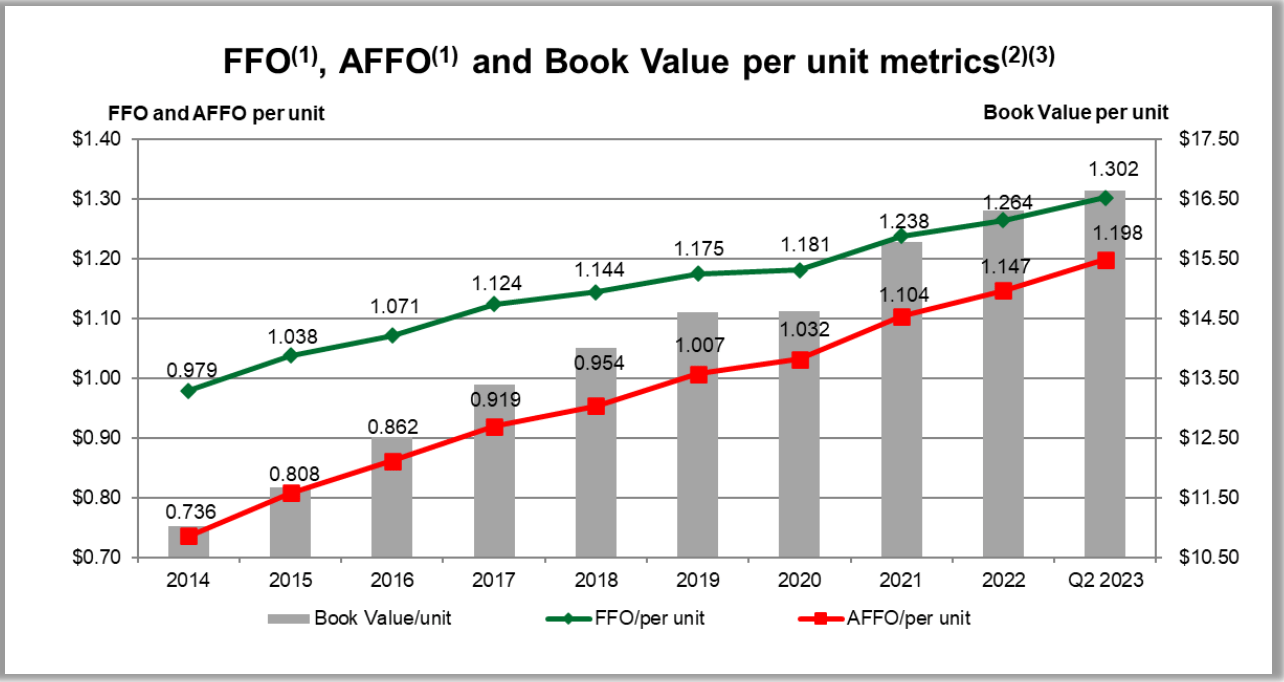

Divided over the 235.2M units outstanding (108M common units and 127.2M Class B LP Units with the same economic rights as the common units), the AFFO per share in the second quarter was approximately C$0.305. On an annualized basis, this represents C$1.22 per share while the AFFO per share in the first semester was approximately C$0.60. Thanks to the rent hikes and the completion of a development property, the AFFO is still accelerating somewhat.

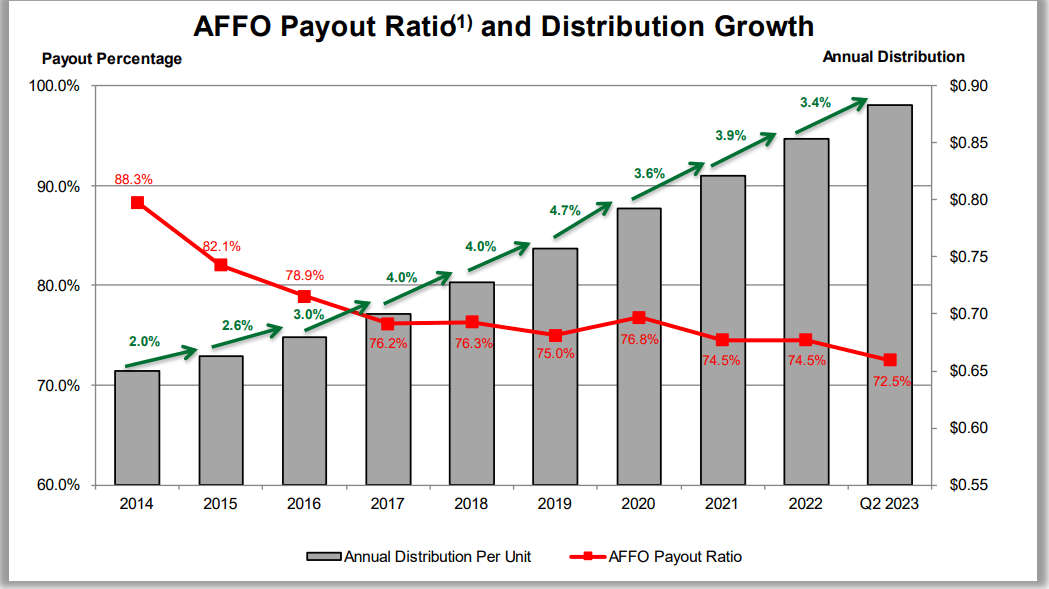

This also means the current monthly distribution of C$0.07485 is very well covered with a payout ratio of less than 74%. And as CT REIT has a history of increasing its distribution along with the AFFO increases, shareholders of CT REIT can likely look forward to continuous distribution increases.

{kind=link}

As you can see above, in the past 10 years the distribution has increased by in excess of a third while the payout ratio has decreased very substantially. At the current distribution rate, the yield is approximately 6.1%.

{kind=link}

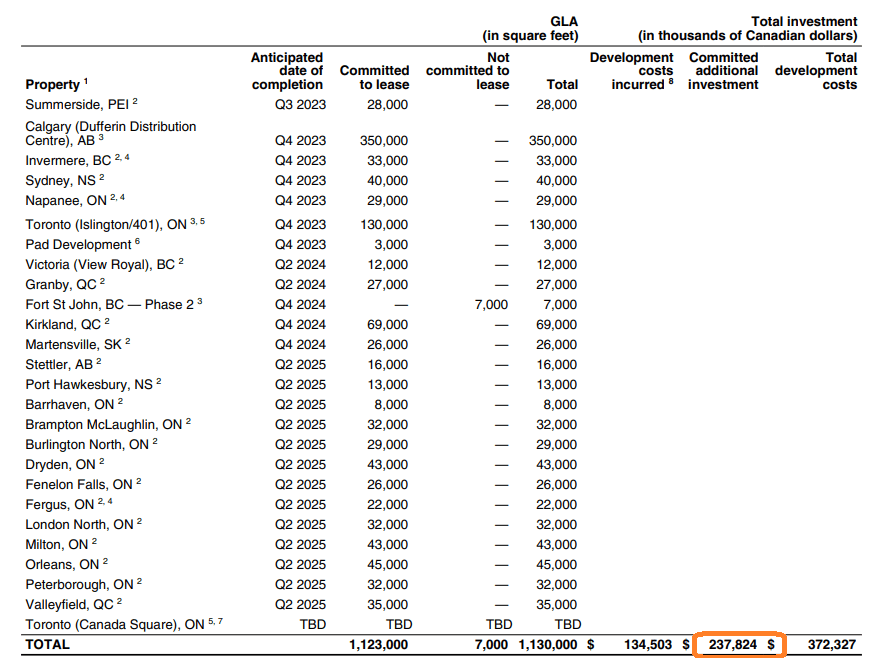

This also means that assuming a full-year AFFO of C$1.21 per share, the REIT is able to retain about C$73M per year in earnings, which it can redeploy in its development pipeline. As you can see below, CT REIT has committed to spend an additional C$240M on its development pipeline between mid-2023 and mid-2025 (when the last development stage project should be completed). Being able to retain north of C$70M per year means that about C$146M of the C$238M (or in excess of 60%) can be funded by equity. And that’s why CT REIT will still be able to increase its AFFO result: it did not and does not rely on too much debt to fund the expansion plans. It runs a conservative balance sheet and payout ratio and that will allow it to keep its balance sheet healthy.

{kind=link}

Assuming a capitalization rate of 6.75% for the new assets (similar to the currently used cap rate ) and assuming C$100M would have to be borrowed at a cost of debt of 6%, the C$372M in completed expansion should result in an additional NOI of around C$25M while the interest expenses would increase by just C$6M. Of course some of the other expenses would increase as well, but a very basic back of the napkin calculation shows it should be very doable to add C$15M in AFFO based on the existing development portfolio. That’s in excess of C$0.06 per share in additional AFFO which means I wouldn’t be surprised to see CT REIT exit 2025 at an AFFO run rate of around C$1.30.

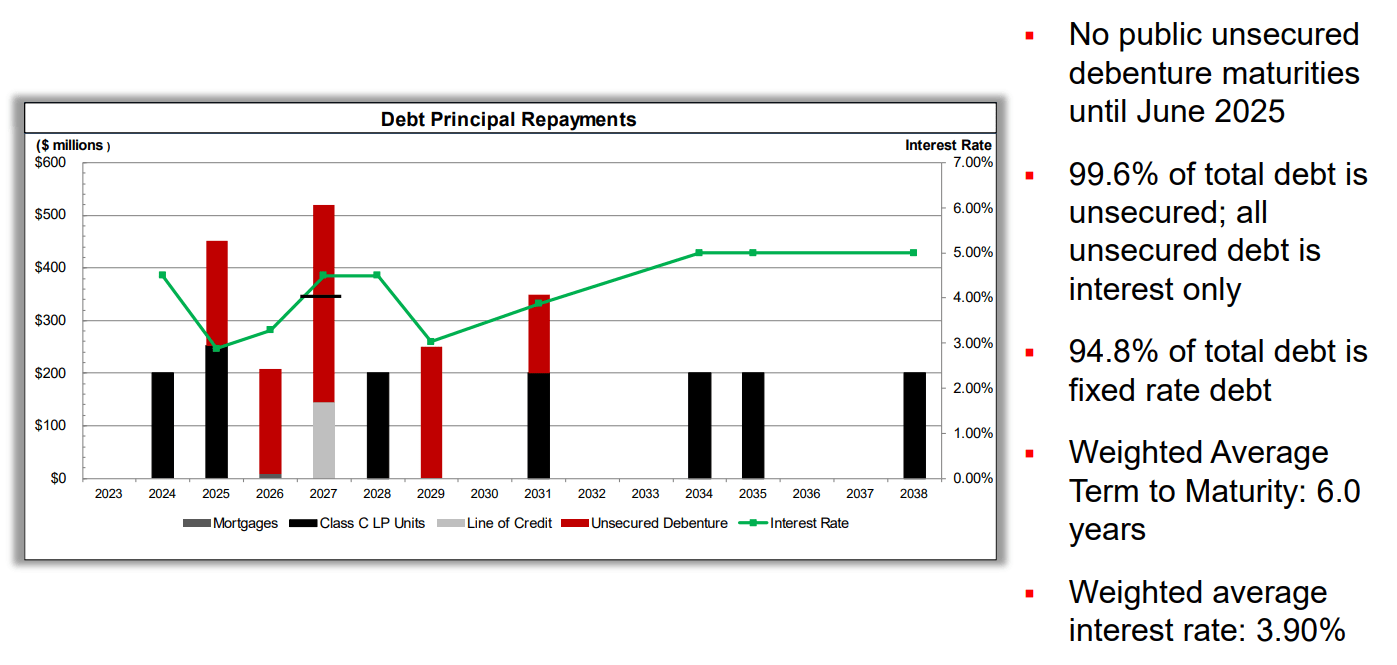

And yes, interest rate increases will cause the interest expenses to increase. But as the majority of the debt consists of fixed rate mortgages and fixed rate debentures, the total interest expenses will only increase relatively slowly.

{kind=link}

As you can see above, the REIT generally only has to refinance a few hundred million in expiring debt per year. Which means that even at a cost of debt increase towards 6%, the impact will be just a few million Canadian Dollar per year. The C$200M debenture maturing in 2025 for instance has a coupon of 3.527%. Even if that increases to 5.75%, the AFFO would be negatively impacted by just C$0.019 per year and this should be absorbed by the completion of the development projects.

Investment thesis

CT REIT currently has a dividend yield of approximately 6.1%, which is very impressive considering the payout ratio is less than 75%. I expect the REIT to report a full-year AFFO of at least C$1.20 and likely around C$1.22-1.23 this year which means the current AFFO multiple of 12 appears to be too low as well, especially considering the REIT, is main tenant and main shareholder have a common interest in protecting shareholder value.

Based on the growth profile, the relatively small impact from interest rate increases and the good (and well-covered) distribution yield in combination with an LTV ratio of around 40%, I will add to my position in CT REIT.

For further details see:

CT REIT: The 6.1% Yield Will Continue To Increase, Despite Higher Interest Expenses