SPY - Cullen/Frost Bank: Phenomenal Buying Opportunity For This Quality Texas Bank

2023-09-11 09:00:00 ET

Summary

- Texas-focused regional bank, Cullen/Frost Bankers (CFR), presents a rare buying opportunity as its stock price has dropped 30% YTD and offers a dividend yield of nearly 4%.

- CFR is the largest Texas-based bank with a strong market share and a long history of conservative management.

- The bank faces challenges such as shrinking deposits and a portfolio of commercial real estate loans, but these issues can be overcome in the long term.

- Investors often think banks have no competitive advantages, but CFR enjoys best-in-class customer satisfaction/loyalty as well as a rare combo of loan and balance sheet conservatism.

- Plus, it doesn't hurt to have a very strong and growing market position in the Lone Star State.

What's cheap can always get cheaper.

But quality and growth prospects don't get any better when a stock gets cheaper.

That's what makes it such a rare and compelling buying opportunity when a high-quality company with strong growth prospects goes from cheap to even cheaper.

That, I would argue, is the case for Texas-focused regional bank, Cullen/Frost Bankers ( CFR ), parent company of Frost Bank.

Since I wrote my Buy-rated article on CFR in June, the Texas bank stock has slid some 15% in price. That gives this blue-chip bank stock a dividend yield just shy of 4%, well above its 5-year average yield of 2.75%. Also, the P/E ratio of 11.4x is near its COVID-era lows and well below its 5-year average of 14.8x. By 2022 free cash flow, CFR is even cheaper at 10.2x.

Year-to-date, CFR has performed even worse than the broader SPDR S&P Regional Banking ETF ( KRE ), despite being of above-average quality, in my opinion.

But of course, CFR is facing meaningful headwinds right now, such as shrinking deposits, a rising cost of deposits, and substantial portfolio of commercial real estate loans (including for office buildings).

These issues can, I believe, be overcome over time as interest rates eventually normalize and worker office utilization settles into a new normal.

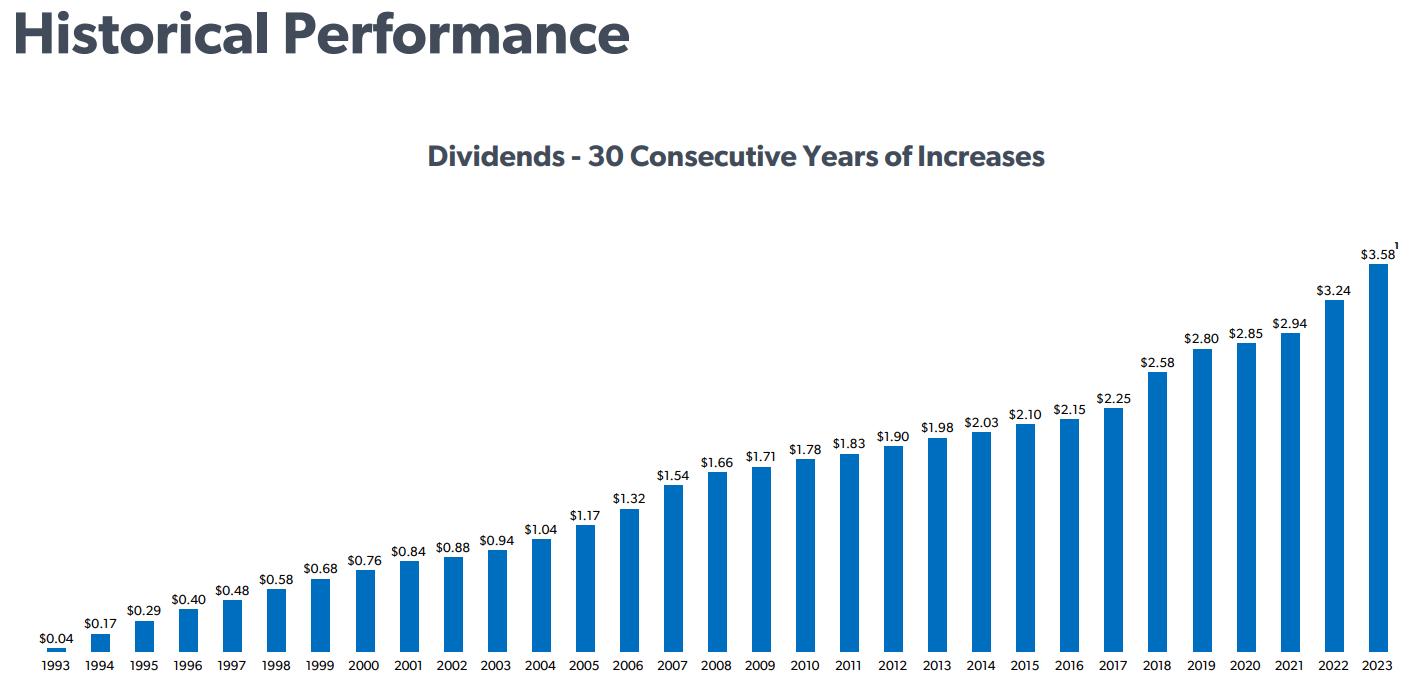

With a 30-year dividend growth record, a 20-year dividend CAGR of about 7%, a low payout ratio of about 40%, and a 4% dividend yield, CFR looks like an excellent dividend growth stock to buy today.

Update On Frost Bank

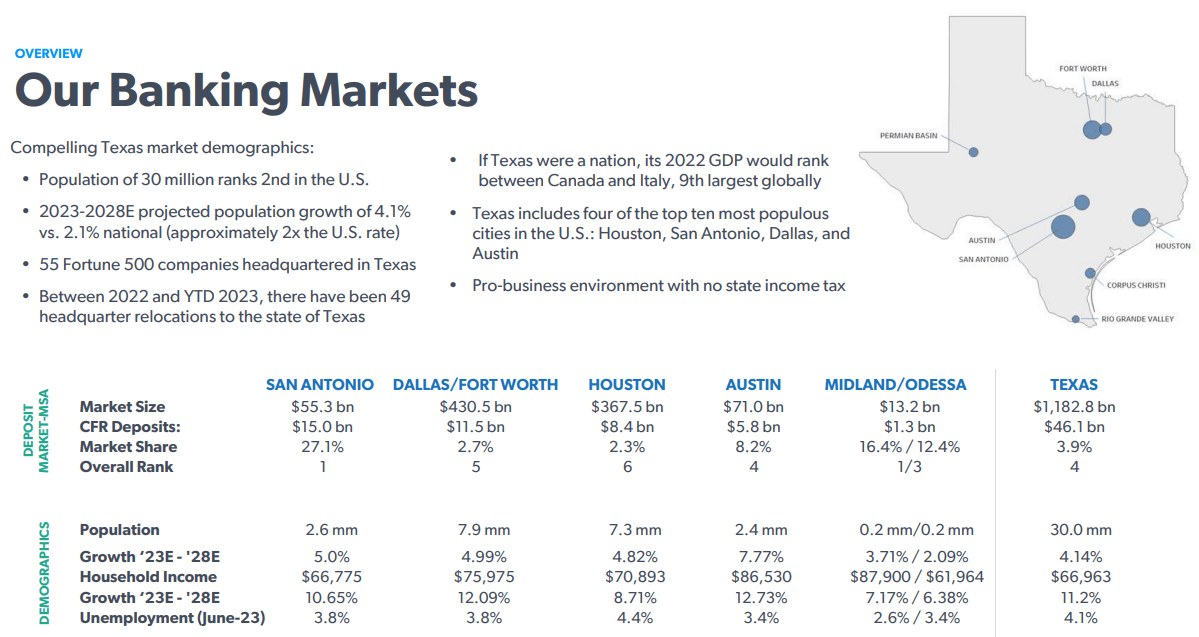

CFR is the largest Texas-based and Texas-focused bank with a strong market share of both depositors and small to mid-sized businesses and commercial landlords. The bank has been around since 1868 with continuous involvement from the founding Frost family up to today. Many of CFR's relationships have been fostered over decades, if not generations.

This long-term, even generational, mindset characterizes the way the bank is managed in virtually every way, from loan underwriting to relationship cultivation to balance sheet management.

As a result of this conservatism, CFR was the only top ten Texas bank to survive the 1980s savings & loan crisis without the need for federal assistance or a merger with another bank.

CFR focuses exclusively on Texas, although the bank is still finding growth from expansion of its branch count in major markets like Houston, Dallas/Fort Worth, and Austin.

CFR already boasts a commanding, #1 market position in San Antonio, where slightly more than 1 in every 4 deposit dollars is held in a Frost bank, but it is making a concerted (and successful) effort to grow share in the other major Texas markets as well.

{kind=link}

CFR August Presentation

But physical branches aren't the only source of deposit growth. CFR has invested heavily in its online banking presence recently, and these investments are bearing fruit. In Q2 2023, 52% of account openings came from CFR's online channel, and online account openings were up 27% YoY.

Like most banks, CFR's revenue primarily derives from net interest income at about 80% of the total, leaving roughly 20% to come from various non-interest income sources.

And like virtually all banks with this business model, CFR has suffered a deposit outflow as non-interest-bearing and low-interest-bearing deposit money seeks yield in CDs, bonds, money markets, or high-yield savings accounts outside the traditional bank setting.

In Q2 2023, CFR's total deposits declined ~11% YoY and are down 12.6% from their peak level in Q3 2022. Non-interest-bearing deposits specifically dropped 12.3% YoY in Q2.

This has pushed up CFR's loan-to-deposit ratio by about 5 points. But CFR had and still has among the lowest LDRs in its industry.

{kind=link}

CFR August Presentation

CFR was already quite conservatively managed prior to the Great Financial Crisis of 2008-2009, but the GFC seems to have made it even more conservative, as its LDR fell by nearly 30 points to the mid-40% territory.

Traditionally, banks have run the risk of failure when they've loaned out the vast majority of their deposit funds, because even a small depositor run on the bank can cause a swift and destructive chain reaction. Deposit redemptions require asset liquidations, which spur more redemptions, which triggers more liquidations, and so on, until the FDIC steps in and takes over conservatorship.

CFR runs extremely little risk of this deadly self-reinforcing cycle with such a low LDR.

Plus, it has an established record of operating with reserves well in excess of the required amounts. Moreover, management usually likes to keep around 20% of total assets as cash. In normal times, this seems incredibly conservative, but right now that cash is earning a very nice yield while having lost zero value amid rising interest rates, unlike its loan and securities portfolios.

As of Q2 2023, CFR's cash balance is "only" 15% of total earning assets, because management has put some of it to work recently in long-term securities at very attractive yields. This will be beneficial to CFR for many years to come, unlike the high yields on its cash holdings that are (probably) temporary.

Rather than the risk of failure from a bank run, CFR's primary headwind is the cost of deposits. Fortunately for CFR, its cost of deposits aren't rising as fast as the regional bank peer average, perhaps due to depositor loyalty and a commanding market share of small-dollar depositors who don't find it worthwhile to seek out an interest-bearing alternative.

CFR August Presentation

Management claims to be focused on capturing a large share of core transactional deposit accounts. This was a big reason for the heavy recent investment in building out CFR's online presence and app, making it as simple and easy to use as possible for the average customer.

In such a competitive banking environment, depositors will naturally gravitate toward convenience. CFR aims to capture people's primary transacting accounts mainly by providing that top-tier convenience and user-friendliness.

Perhaps this is why Frost Bank has been the #1 retail bank in JD Power's banking satisfaction survey for 14 years straight.

CFR August Presentation

In a time when customers can earn over 5% on cash, it's easy to overlook customer satisfaction as a competitive advantage, but I don't believe this era of yield's predominance over all will last forever.

Good old fashioned customer convenience will reassert itself someday. That makes it highly likely that when depositor banks begin to recapture share from yield vehicles, CFR will claim a disproportionate amount of Texans' money.

The Resilient Loan Book

Deposits are only one of the market's worries. Another is the commercial real estate portion of the loan portfolio, especially the loans backed by office buildings.

CFR August Presentation

As you can see, CRE makes up nearly half of CFR's $17.7 billion loan portfolio.

Of that, office real estate accounts for a little over 1/5th, the largest CRE sector for CFR. But the CRE loan portfolio is richly diversified across various sectors.

{kind=link}

CFR August Presentation

As of Q2 2023, only 0.31% of CRE loans were not performing.

Also, slightly over half (51%) of CRE loans are owner-occupied properties, which typically exhibit lower non-performance rates than investor-owned properties. So, let's look specifically at investor-owned CRE.

Of all investor-owned CRE in CFR's loan portfolio, the overall average loan-to-value sat at 54% in Q2. For investor-owned office properties specifically, the average LTV sits even lower at 52% with an interest coverage ratio of 1.42x, up quarter-over-quarter from 1.38x in Q1.

The "bad news," such as it is, is that there's a relatively steady slate of loan maturities for investor-owned office this year and next year.

CFR August Presentation

The good news is that the vast majority (92%) of CFR's investor-owned office loans are for properties in Texas. The relatively short-commute cities of Austin and San Antonio make up 50% of this category. Although there is some office stress in these markets as well, it is arguably lower than in many coastal cities with lower office utilization rates and higher urban crime.

Admittedly, markets like Austin and Houston do have high office vacancy rates of about 20%, due largely to a big spate of recent deliveries amid slow leasing. But even if defaults occur, there is so much dry powder on Wall Street waiting to pounce on distressed CRE, it's hard to imagine property values cratering in hot markets like these.

Lastly, consider the recent rush of "return-to-the-office" mandates from various companies in recent months, especially picking up after Labor Day. This should bolster the fundamentals somewhat for office landlords.

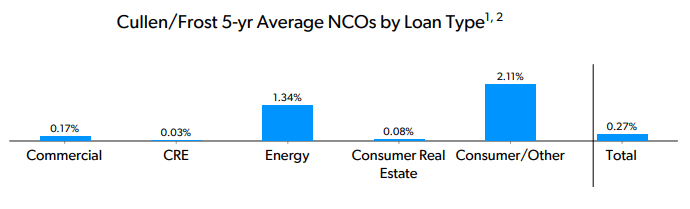

Over the last five years, CRE has seen the lowest level of net charge-offs (gross bad debt minus recoverable value) of all CFR's loan types -- a mere 0.03%.

{kind=link}

CFR August Presentation

Of course, this was before the current office real estate troubles, but the point is that CFR is very conservative in underwriting its commercial real estate loans. It is by no means the most vulnerable of office real estate lenders.

There may be worse pain to come for CFR's loan book, especially as office landlords have to refinance loans at higher rates and lower property values. I am not trying to downplay or sugarcoat the potential for real pain to manifest as interest rates stay high and office CRE faces continued headwinds.

But I am saying that CFR's history of conservative underwriting and below-average net charge-offs (unrecoverable losses) in the CRE space is being overlooked by the market right now.

A Rare Combo: Quality And Cheap

Let's look at why the valuation of CFR has become even more compelling.

Of course, I can't time the bottom. Good luck to you if you think you can do so on a consistent basis. But we can definitely determine (1) if the quality of a good business has eroded, and if not, (2) whether its current valuation is low relative to its historically average valuation range.

I think CFR remains a high-quality company worth owning, as explained in the sections above. So that leaves us to determine whether its valuation today is compelling -- i.e. on the low end of its historical range.

The answer is yes , it absolutely is.

By P/E ratio, CFR is cheaper than it was during the GFC. Only briefly during COVID-19 was CFR cheaper than today.

This has rendered a roughly 10% free cash flow yield for CFR, leaving ample cash generation to cover the dividend and to whatever else management would like to allocate capital.

Speaking of the dividend, CFR now yields roughly 4%. Not bad for a Dividend Aristocrat with a 30-year dividend growth record!

{kind=link}

CFR August Presentation

The most recent dividend increase of 5.7% is understandably more modest than CFR's usual fare, but this is still a generous raise in the current environment that signals no concern for the long-term outlook.

Bottom Line

Buying high-quality companies when they are on sale tends to work out well.

Certainly, for CFR, buying on big dips like this has worked out swimmingly. The bank stock has outperformed both the broader financials sector ( IYF ) and the S&P 500 ( SPY ) over the long run.

I do not believe the current dip will prove any different. I think this is a phenomenal buying opportunity, especially for dividend growth investors.

For further details see:

Cullen/Frost Bank: Phenomenal Buying Opportunity For This Quality Texas Bank