CURLF - Curaleaf Has More Risk Than Peers

2023-10-22 16:23:26 ET

Summary

- Curaleaf's stock has rallied on the potential rescheduling, but it still has a high relative valuation compared to its peers.

- Analysts project modest revenue and EBITDA growth for Curaleaf in 2023 and 2024.

- The company's balance sheet and high debt levels remain concerning, but the elimination of 280E tax could impact its stock price positively.

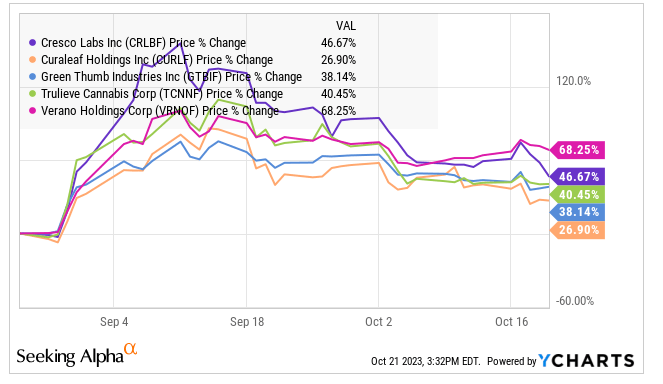

I have been negative all year on Curaleaf ( OTCPK:CURLF ). Most recently, ahead of the potential rescheduling, I predicted that it could break $2 to the downside when the stock was at $2.90 in late August. I actually called out $2.20 as my year-end target. The stock has rallied on the potential good news, closing at $3.68, up 27%. In that article, I called out its excessively high relative valuation, and it has lagged all of its large MSO peers:

{kind=link}

YCharts

Since the end of 2022, the stock has declined 14.4%, a little less than the Global Cannabis Stock Index. In mid-January, I called it out for its high relative valuation . The stock has declined 8.2% since then.

While the stock may not hit that $2 area that I was predicting, it is still very expensive relative to its peers. In today's piece, I review the outlook, discuss the valuation and assess the chart.

Looking Ahead

In late August, analysts, according to Sentieo, were looking for 2023 revenue to be $1.36 billion, with 2024 revenue projected to expand to $1.47 billion. Now they expect 2023 revenue to still grow 2% to $1.36 billion, but the 2024 outlook is a bit less strong, with analysts projecting 6% growth to $1.44 billion. Adjusted EBITDA is expected to shrink 1% in 2023 to $301 million and to grow 20% in 2024 to $361 million.

For forming year-end targets, I believe the 2025 estimates will play a key role. Right now, only 4 analysts have provided them. They are projecting that revenue will grow 21% to $1.74 billion with adjusted EBITDA rising 45% to $522 million, a 30% margin that sounds too high. In 2021, the prior peak annual margin, the company had an adjusted EBITDA margin of 25%

Of course, how rescheduling plays out will impact the company's cash flow, but it will have no impact on the EBITDA because taxes are excluded. If the DEA follows the recommendation from the HHS to move cannabis from Schedule 1 to Schedule 3, the onerous tax 280E would stop. 280E forces cannabis companies to pay tax on gross profits rather than net profits. For 2024, analysts currently project diluted EPS of just $0.09 per share.

One thing that has changed since my review in August after the Q2 report is that the company has applied for listing on the TSX. I don't think that this will matter much if the company is successful.

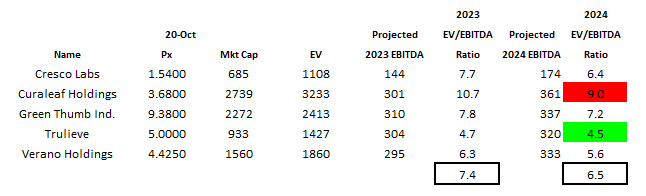

Relatively Expensive

Curaleaf trades at an enterprise value to adjusted EBITDA for 2023 of 10.7X, which seems low relative to its history. It trades at 9.0X the projected 2024 adjusted EBITDA.

While the valuation seems low, it is high relative to its four peers:

{kind=link}

Alan Brochstein, using Sentieo

As I look out to the end of 2024, about 14 months from now, I think that Curaleaf could trade at 12X projected adjusted EBITDA if 280E goes away, but it might pull back to 6X if not. The company has a lot of debt outstanding, even after the recent capital raise. At the current price, I assume that the share-count will be boosted by 7.9 million shares, as the $2.89 options are in the money. That cash would reduce the net debt to $494 million.

I think that the analysts are too high in their estimate of 2025 adjusted EBITDA, but I am using their estimate nevertheless. The stock could reach $7.75 if 280E gets wiped out, but it could also fall to $3.55 at 6X. Again, I think that the projection is too high, so the price could be lower. I continue to believe that the stock could test $2.

I continue to find the balance sheet to be concerning. The company has tangible equity that is quite negative at -$722 million at the end of Q2. The recent capital raise and the potential options exercise brings this to -$687 million. The company will need to raise capital in my view due to the large debt.

Another concern is that the AdvisorShares Pure US Cannabis ETF ( MSOS ) owns a lot of the stock, way more than it should in my view at 19.8% of the fund. Only GTI, at 24.2%, is larger. The top 6 holdings of MSOS total 83% of it. The ETF has seen some inflows recently after seeing outflows in late 2022 and into 2023. If it suffers redemptions again, it will need to sell CURLF.

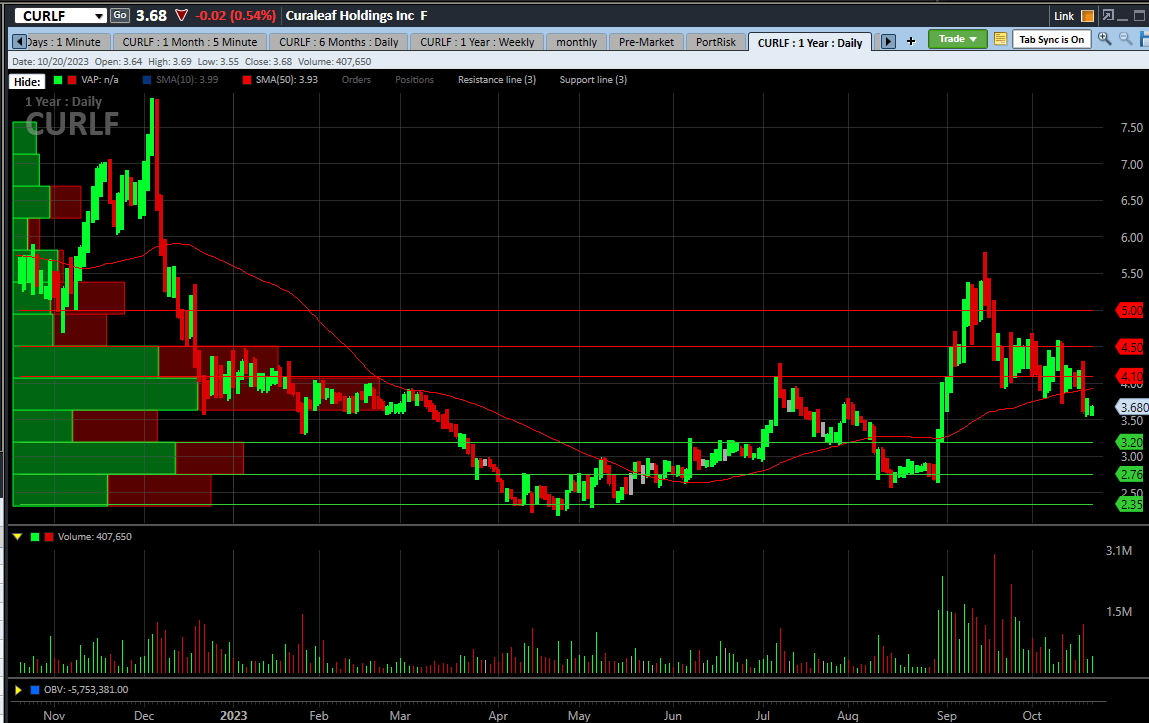

The Chart

Curaleaf had a huge bounce recently, doubling in just a few weeks, but it has lost most of those gains:

{kind=link}

Charles Schwab

I see support just above $3 and then below it. I see resistance just above $4.

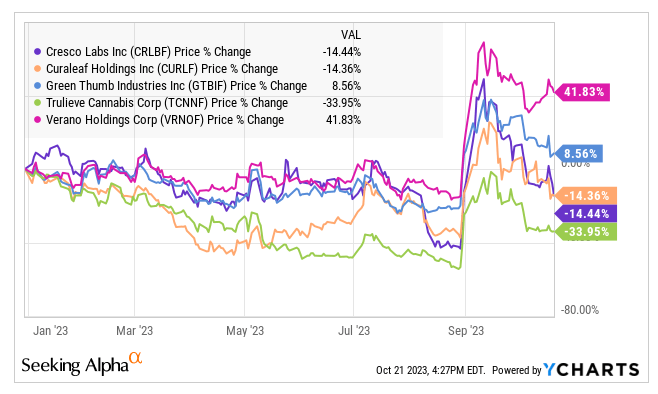

Above, I showed how the chart has compared to its four large peers since late August. Here is the year-to-date perspective:

{kind=link}

YCharts

Cresco Labs ( OTCQX:CRLBF ), which I prefer, and Trulieve ( OTCQX:TCNNF ), which I also prefer, have lost more, while Verano ( OTCQX:VRNOF ) and Green Thumb Industries ( OTCQX:GTBIF ) have done better and are up year-to-date.

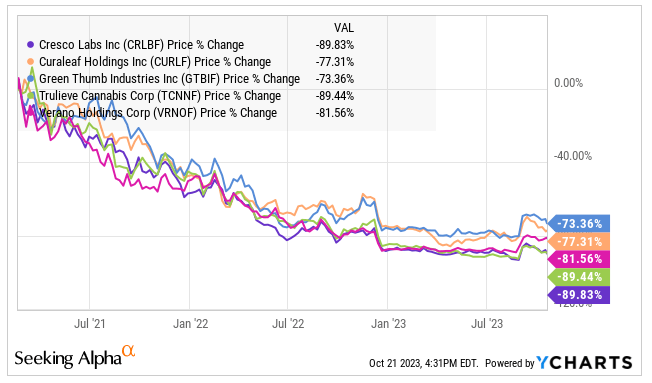

Since the peak in February 2021, Curaleaf, down 77%, has done better than all but GTI:

{kind=link}

YCharts

Conclusion

Curaleaf has declined a lot over the past few years and appears to be cheap. It is relatively expensive, though, to its peers. With the elimination of 280E, the stock would likely go up. If 280E stays, the stock will likely decline.

Investors who want to participate in the cannabis market can take less risk with CURLF peers or other types of cannabis companies and potentially make greater returns too. I have written about some Canadian LPs that trade below tangible book value and have a lot of cash and no debt. One of these federally legal companies trades at a lower enterprise value to projected adjusted EBITDA a year ahead too. I also find some better ideas among the ancillary companies.

For further details see:

Curaleaf Has More Risk Than Peers