ET - DCP Midstream: Solid Q3 Results But Hold Off On Buying

Summary

- DCP Midstream showed considerable improvement in its finances YOY.

- The company seems likely to post better results in Q4 2022 than it did in Q4 2021.

- The offer from Phillips 66 is a bit of a wildcard since the company's units are far too expensive for this deal to be good for investors.

- The company has an incredibly strong balance sheet and a very sustainable distribution.

- I do not recommend buying the company until we get more visibility into how the Phillips 66 deal will pan out.

On Wednesday, November 2, 2022, the somewhat maligned midstream master limited partnership DCP Midstream, LP ( DCP ) announced its third-quarter 2022 earnings results. At first glance, these results were certainly impressive as DCP Midstream beat analysts' revenue and earnings expectations. The company also continued the trend that we have been seeing across the entire midstream sector lately by posting fairly strong year-over-year growth. A closer look at the results reveals that there is quite a bit to like here as the company continued to make progress at reducing its debt and it now boasts one of the strongest balance sheets in the entire midstream sector. Unfortunately, the company has not yet managed to return its distribution to the level that it had prior to the 2020 cut, although it has increased it slightly. There are a few other fairly important pieces of news here to discuss, including the possibility that DCP Midstream may be acquired, and given that, the company's current unit price appears to be incredibly high. The fact that the distribution yield is rather low compared to its peers also makes DCP Midstream somewhat of a second-tier choice for investment today but it does still make sense to review these results to determine how much potential could be here.

As my long-time readers are certainly well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from DCP Midstream's third-quarter 2022 earnings results:

- DCP Midstream brought in total operating revenues of $4.319 billion in the third quarter of 2022. This represents a 52.78% increase over the $2.827 billion that the company brought in during the prior-year quarter.

- The company reported an operating income of $247 million during the reporting period. This compares very favorably to the $6 million operating loss that the company had in the year-ago quarter.

- DCP Midstream transported an average of 731,000 barrels of natural gas liquids per day through its pipeline infrastructure in the current period. This represents a slight increase over the 720,000 barrels of natural gas liquids per day that the company transported on average last year.

- The company reported a distributable cash flow of $324 million in the most recent quarter. This represents a 29.60% increase over the $250 million that the company reported in the equivalent quarter of last year.

- DCP Midstream reported a net income of $312 million during the third quarter of 2022. This represents a substantial 721.05% increase over the $38 million that the company reported in the third quarter of 2021.

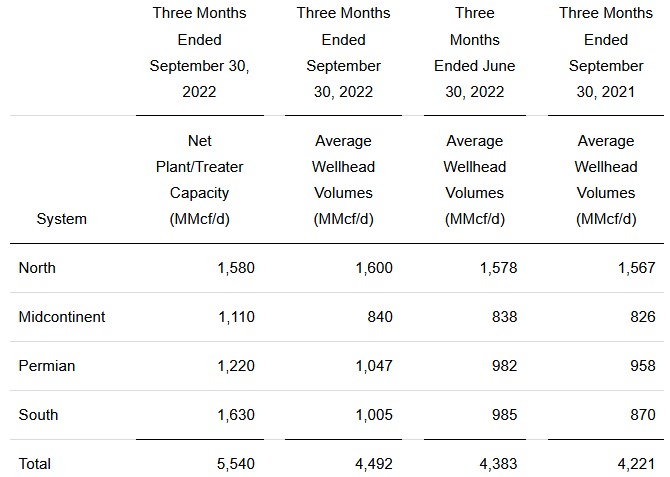

It seems essentially certain that the first thing that anyone reading these highlights will notice is that DCP Midstream experienced strong improvements in essentially every measure of financial performance. This was not unexpected as nearly every midstream company has been reporting growth over the course of this year. The biggest reason for this is that the company's transported and handled volumes increased year-over-year. We see this in the company's natural gas liquids logistics segment as mentioned above but it also applies to the company's natural gas gathering and processing operation:

{kind=link}

This business segment is not what many people ordinarily think of when picturing a midstream company. These are not the large pipelines that are used to transport resources over long distances. Instead, a gathering pipeline is a relatively short pipeline that grabs resources at the wellhead where they are extracted from the ground. These pipelines then transport the natural gas a relatively short distance to the first destination on its journey to the end-user. This is usually a much larger pipeline or a processing plant. In the case of DCP Midstream, it is almost always the latter since the company does as much processing of natural gas in-house as it can.

The overall business model of both the long-haul natural gas liquids logistics segment and the natural gas gathering pipelines is essentially the same, though. In both cases, the company enters into long-term (usually five to ten years in length) contracts with a customer under which the customer sends resources through the company's pipelines. DCP Midstream then bills the customer based on resource volumes, not on the value of the resources. This business model results in the company's cash flow generally increasing when it handles more resources. As we saw in both the highlights and the chart above, that was essentially the case across the company's entire business operation.

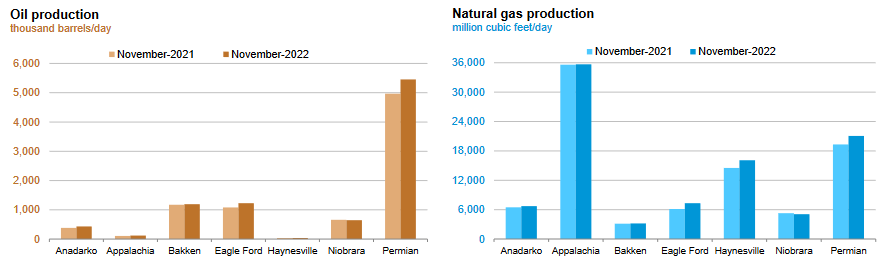

DCP Midstream is likely to be able to continue its quarter-over-quarter growth trajectory in the fourth quarter. This is due to the fact that the company's transported volumes are likely to be higher in that quarter than in the fourth quarter of 2021. We can see this simply by looking at production trends in the basins that the company operates in:

{kind=link}

As we can clearly see, upstream producers have increased their output in most of America's major resource basins. In those basins that have not seen much growth, we see that production has been more or less flat. The Niobrara Shale play is the sole exception to this statement and the decline there was negligible. DCP Midstream does have operations in the Niobrara shale but it is only a very small proportion of the company's broader business. The majority of the company's money is generated in the Permian Basin, which is currently producing more natural gas and liquids than it did in the same quarter of last year. Somebody will need to transport those resources to the market in order to be sold and given DCP Midstream's size and scope, it does seem likely that it will see at least some of this business. Thus, it seems likely that DCP Midstream will handle more resources in the fourth quarter of 2022 than it did in the fourth quarter of 2021. This should result in its cash flows being somewhat stronger during that quarter.

Back in 2020, the uncertainty in the industry caused DCP Midstream to defer or cancel many of the growth projects that it was working on. Unfortunately, unlike many of its peers, DCP Midstream has still not resumed development on any of those projects. This will almost certainly handicap the company's growth relative to that of what peers, such as Energy Transfer ( ET ) or Enterprise Products Partners ( EPD ), should be able to deliver over the next few years. DCP Midstream might still see some growth from its gathering and processing segment though since those pipelines are much faster to construct and so management of many companies rarely mentions them in earnings reports and industry presentations. The company's management has confirmed that this business unit will likely be the source of DCP Midstream's future growth. This is admittedly not surprising as this is the only business unit that the company has that specifically focuses on natural gas. As I have pointed out in many previous articles, the fundamentals of natural gas are much stronger than the fundamentals of any other fossil fuel. However, DCP Midstream is far from the only midstream company that handles natural gas and this lack of any significant growth projects will likely still handicap its growth relative to peers.

One of the most interesting developments that came about in the third quarter is that refining giant Phillips 66 ( PSX ) offered to buy DCP Midstream in August. The price offered by Phillips 66 values DCP Midstream at $7.2 billion, which is substantially below the company's current enterprise value of $13.44 billion. This is one indication that DCP Midstream might be overvalued today. This deal would result in the company's current common unitholders receiving $34.75 per unit owned, which is quite a bit below the current price. The market is likely assuming that Phillips 66 will increase its offer but it has been several months since the announcement was made and so far there has not been a higher offer. DCP Midstream's press release appears to imply that the company is considering the offer at $34.75:

"On August 17, 2022, Phillips 66 delivered a non-binding proposal to the Board to acquire all of the partnership's outstanding Common Units not already owned by DCP Midstream or its subsidiaries at a cash purchase price of $34.75 per Common Unit. The Board has authorized a Special Committee comprised of independent members of the Board to review, evaluate, and negotiate the proposed transaction."

This certainly implies that the company may be considering the purchase although it is trying to be political about it in its communications to shareholders as it does not want to be held liable if someone purchases units and the deal does not go through. It is typical for a potential buyer to increase its offer in negotiations but as already mentioned, we have already seen several months pass with no change in Phillips 66's offer so there may not be one forthcoming. With that said, RBC has stated that it expects a 10% increase in Phillips 66's offer to eventually happen. That would only result in a price of $38.22 per unit, which is still well below today's market price. Thus, it may not be a good idea to purchase any of the company's units today until we get more information about how this deal may ultimately play out.

One of the reasons that DCP Midstream reduced its distribution back in 2020 was to reduce its outstanding debt. This made some sense at the time as the market, in general, was generally hostile to midstream partnerships and the company wanted to be able to finance itself without having to care what the market thought about it. DCP Midstream has certainly made some progress in achieving its debt reduction goals since that time. In the third quarter alone, DCP Midstream reduced its outstanding debt by $300 million, which resulted in the company reducing its outstanding debt by more than $600 million year-to-date. It also gives DCP Midstream one of the strongest balance sheets in the entire midstream industry. We can see this by looking at the company's leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely eliminate its debt if it was to devote its entire pre-tax cash flow to that task. At the close of the third quarter, DCP Midstream had a leverage ratio of 2.5x. Analysts generally consider anything less than 5.0x to be acceptable but I am more conservative and like to see this ratio below 4.0x in order to add a margin of safety to the investment. Many midstream companies have, since 2020, gotten their leverage ratios down into the 3.0x to 4.0x range but DCP Midstream obviously beats even those reasonable numbers. Overall, there is absolutely nothing to be concerned about with respect to the company's debt load as it is easily one of the strongest companies in the entire sector.

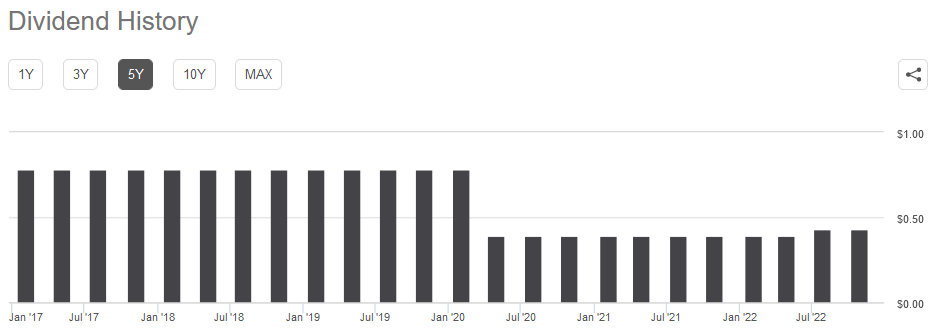

One of the biggest reasons why many people invest in midstream companies is that they historically boast a higher yield than many other things in the market. DCP Midstream is not really an exception to this as the company yields 4.46% as of the time of writing, which is significantly higher than the 1.65% yield of the S&P 500 index ( SPY ). While this is a reasonable yield in today's market, it is important to note that it is substantially below the 7.12% yield of the master limited partnership index ( AMLP ). One of the biggest reasons for DCP Midstream's current low relative yield is that the company's common units have been bid up in anticipation of the merger agreement but the company has yet to restore its distribution back to the level that it had prior to the 2020 cut:

{kind=link}

The fact that the company has not yet restored its distribution to the level that it had prior to 2020 is not unusual as most companies that cut during that year still pay out significantly less than they did prior to COVID-19 and the resulting crash in energy prices. However, there are some companies like Energy Transfer, that have been fairly aggressive about trying to get their distributions back to their previous level. However, DCP Midstream's past is not exactly the most important thing for someone investing today. This is because anyone purchasing the stock today will receive the current distribution at the current yield. Thus, the most important thing is the company's ability to maintain its current distribution. After all, we do not want to find ourselves the victims of another distribution cut since that would both reduce our incomes and almost certainly cause the share price to increase.

The usual way that we judge a midstream company's ability to cover its distribution is by looking at its distributable cash flow. Distributable cash flow is a non-GAAP figure that theoretically tells us the amount of cash that was generated by the company's ordinary operations that is available to be distributed to the limited partners. As stated in the highlights, DCP Midstream reported a distributable cash flow of $324 million in the third quarter of 2022. That was sufficient to cover the company's declared distribution 3.64 times over. Analysts generally consider anything over 1.20x to be reasonable and sustainable so we can see that DCP Midstream can easily afford its distribution. There is no reason for investors to be concerned about another cut here. The distribution is quite secure at the current level and DCP Midstream could conceivably increase it somewhat over the current level.

In conclusion, DCP Midstream continued the trend of growth that we have been seeing all across the midstream sector over the past year. The company is perhaps not as well positioned to grow as aggressively going forward though due to its lack of any major new projects but it will likely see some from its gathering operation due to upstream producers in the Permian Basin increasing their output in an attempt to take advantage of today's high energy prices. The company's common units unfortunately may be a bit overpriced today as it seems rather unlikely that Phillips 66 will increase its bid sufficiently to complete the acquisition at today's price. Thus, buying today may result in a capital loss if the acquisition is forced. The company's finances are quite strong and its distribution is quite sustainable though so the company does make sense if the acquisition does not go through. Overall though, I would prefer to sit on the sidelines until more visibility about the acquisition is available.

For further details see:

DCP Midstream: Solid Q3 Results But Hold Off On Buying