XOM - Delek US Holdings: Some Near-Term Concerns But Useful For Diversification

Summary

- Delek US Holdings, Inc. is a downstream energy company that operates in Texas and the surrounding states.

- Downstream companies can be useful hedges for portfolios that contain many upstream companies because they benefit from low crude oil prices.

- Delek might have some near-term issues if the economy goes into a recession, but oil prices do not decline, which is a likely scenario.

- The company employs a great deal of leverage relative to its peers, increasing its risks.

- Delek looks rather expensive compared to its peers when it really should be trading at a discount.

Delek US Holdings, Inc. ( DK ) is one of the largest downstream companies in the energy industry. The company is perhaps best thought of as a refiner, but as with most refiners, the company also has a presence in chemicals and renewable fuels. It also owns a fairly substantial logistics operation and a network of gasoline stations that provide fuel to ordinary motorists. This was generally a fairly good business to be in over the past year, as high gasoline and diesel prices drove the company's revenues upwards.

With that said, downstream companies do not really benefit as much from high oil prices as many investors might think, and the company's overall operating profits did not climb much. Delek has been able to reward its shareholders in much the same way as some other energy companies, though, as it reinstated its dividend this year and even paid investors a special dividend. As is the case with most of the things in the energy industry, Delek also boasts a reasonable valuation that could make it a good addition to a portfolio consisting mostly of upstream or midstream energy companies today.

About Delek US Holdings

As stated in the introduction, Delek US Holdings, Inc. is a downstream energy company that has holdings in a diverse array of petrochemical sectors.

{kind=link}

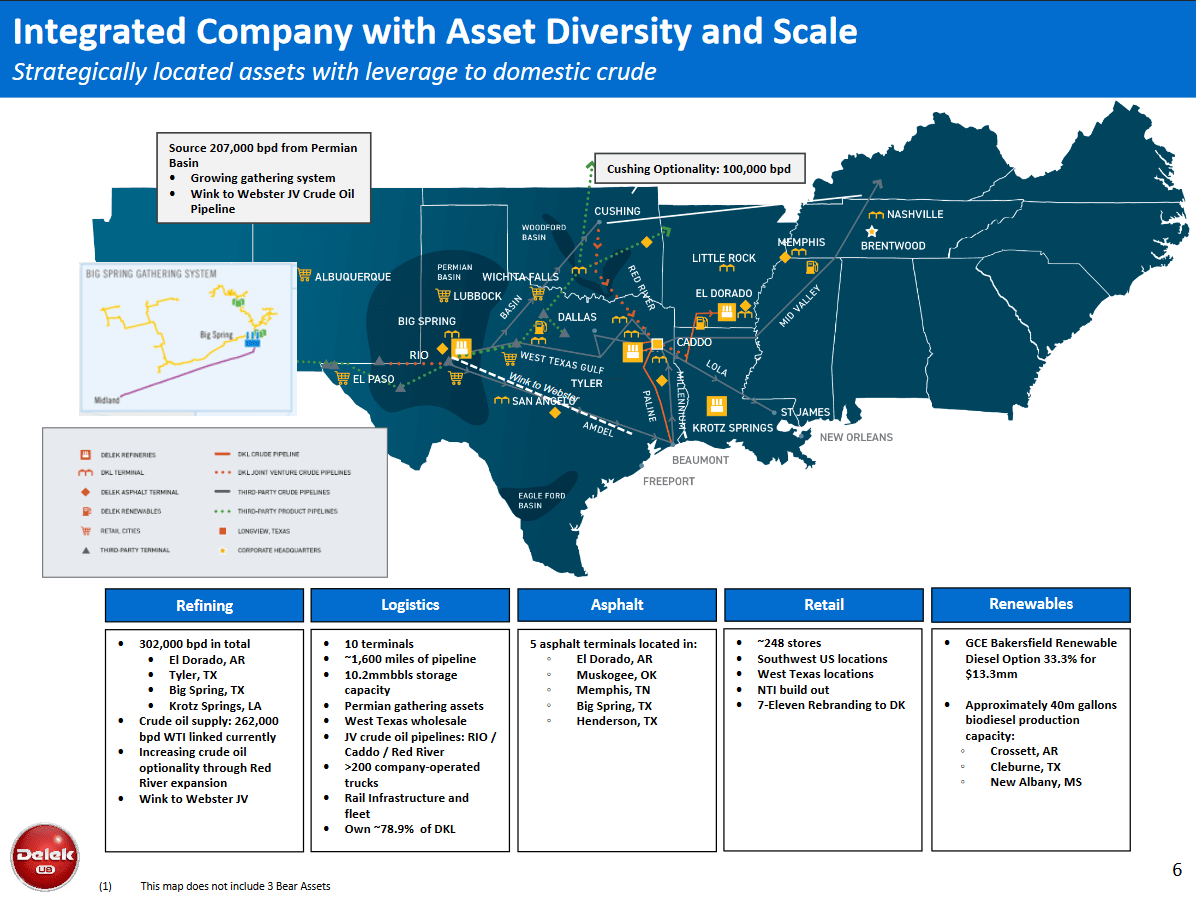

Without a doubt, the company is best known for its refining operations. Delek US Holdings has the ability to refine a total of 302,000 barrels of crude oil per day across its four refineries in Texas and surrounding states. The company has more operations than this though as it is also a major producer of asphalt. That is not particularly surprising for a refinery, as asphalt itself is produced through the refining of crude oil. The company also owns approximately 248 gasoline stations located throughout West Texas and the Southwestern United States. This is also not particularly surprising as it gives Delek US Holdings an outlet to sell the gasoline that it produces in its refineries.

We see many other refinery operators conducting business in the same way, including Marathon Petroleum ( MPC ), Phillips 66 ( PSX ), and Exxon Mobil ( XOM ). The fact that the company owns its own network of gasoline stations in no way limits it from selling its gasoline to other stations or even internationally, and in fact the location of the business is quite close to the vast infrastructure networks of Enterprise Products Partners ( EPD ) and Magellan Midstream Partners ( MMP ), which provide Delek US Holdings with access all across the domestic and international markets.

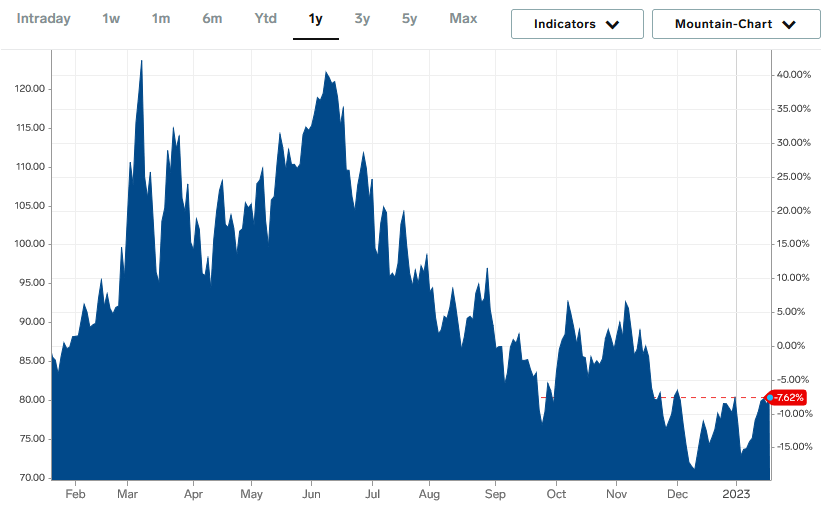

It is not going to be a surprise to anyone reading this that 2022 was characterized by a great deal of strength in the energy markets. That strength has tapered off a bit lately as fears of a recession have permeated the U.S. markets. As of the time of writing, West Texas Intermediate crude oil trades for $80.92 per barrel, which is actually a 7.62% decline over the price that it had a year ago.

{kind=link}

With that said, the price of crude oil is still quite a bit above its 2019 high of $74.34 per barrel so it remains elevated relative to pre-pandemic prices. This is generally considered to be a good thing for traditional energy companies, and indeed we have seen many of the upstream companies produce enormous profits over the past twelve months. This has not been the case for Delek US Holdings, however. In fact, the company's gross profits have not really changed much over the past eleven quarters despite its revenue surging:

{kind=link}

As we can see, the company's gross profits during the second quarter of 2020, which was the period in which the COVID-19 lockdowns crashed energy prices, were almost identical to the numbers that the company posted in two of the three quarters in 2022! The biggest reason for this is that refineries do not particularly benefit from high oil prices. This is mostly because their costs increase because they have to purchase the crude oil to be refined at higher prices and they are not able to pass on all of those costs to the consumers.

In addition, consumers tend to cut back on their consumption of gasoline when prices are high, hurting sales volumes of refiners. In fact, downstream companies tend to do best during periods of falling energy prices. We can see that reflected above, as Delek US Holdings did reasonably well in terms of gross profit during the worst of the pandemic. This characteristic is one reason why including a downstream energy company in your portfolio may be a good idea, as it acts as something as a hedge against lower oil prices that would hurt a shale producer like Pioneer Natural Resources ( PXD ).

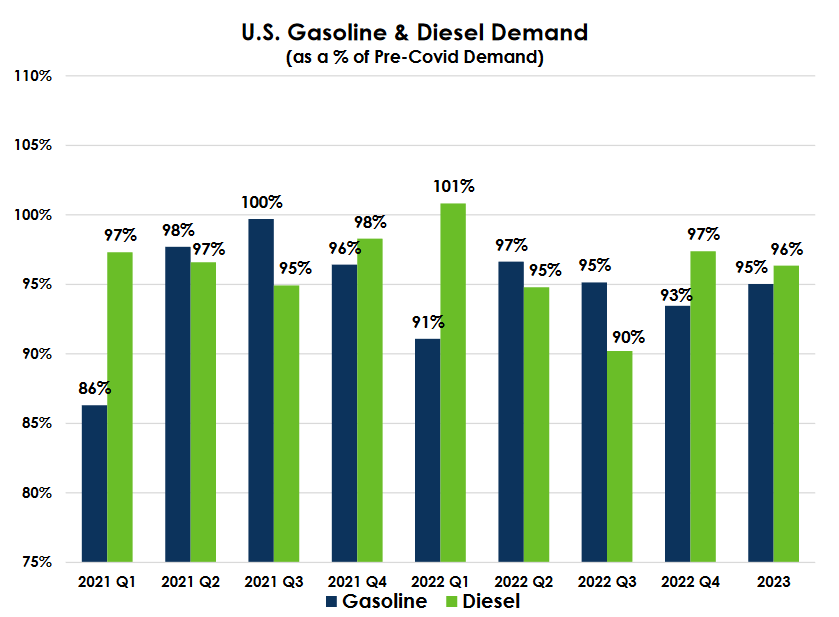

We have begun seeing some signs that demand for diesel fuel in the United States has been increasing, following some weakness during the third quarter. As we can see here, diesel demand during the fourth quarter increased to 97% of pre-pandemic demand, which is a marked increase over the 90% level that it held during the third quarter:

{kind=link}

This is due at least partly to the fact that prices have come down a bit, as we just discussed. It could prove to be a good thing for Delek US Holdings, though, as the company primarily makes its money based on volumes sold and not so much on the price of energy. With that said, it is possible that ESAI is being a bit optimistic here. There are some very real reasons to believe that the United States will enter into a recession during 2023. In fact, that is currently the consensus among nearly every analyst and economist that studies such matters.

One of the characteristics of recessions is that the demand for gasoline goes down because many consumers have lower discretionary income and others attempt to increase their savings in response to the uncertainty. In addition, diesel demand will frequently drop due to lower demand for transporting goods to stores. After all, there is no reason for a store to keep a significant amount of inventory on hand if fewer people are interested in purchasing it. As I discussed in a recent blog post , it is highly unlikely that crude oil prices will decline more than 10% even in a worst-case scenario. Thus, Delek US Holdings may be facing a situation in which the demand for gasoline and diesel fuel declines but energy prices do not. That is pretty much the worst-case scenario for a refiner. Thus, while it may be a good idea to include shares of a downstream company in your portfolio as a hedge against declining prices, it may be a good idea not to overdo it with your allocation.

Financial Considerations

It is always important to investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance an operation than equity because debt must be repaid at maturity. This is normally accomplished by issuing new debt and using the proceeds to repay the existing debt. This process can cause a company's interest expenses to increase following the rollover depending on the overall conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flows to decline can push it into financial distress if it has too much debt. This is something that can be a particularly large risk with Delek US Holdings, as energy prices cause the company's cash flows to vary significantly from quarter to quarter, as we can see here:

{kind=link}

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is funding its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, Delek US Holdings had a net debt of $2.0615 billion compared to $1.283 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 1.61 today. This is unfortunately a bit worse than the 1.51 ratio that the company had following the second quarter (see here ) but the important thing is to compare it to some of the company's peers to determine how its financial structure compares:

| Company |

| Net Debt-to-Equity |

| Delek US Holdings |

| 1.61 |

| Valero Energy ( VLO ) |

| 0.32 |

| Marathon Petroleum Corporation |

| 0.50 |

| Phillips 66 |

| 0.46 |

| HF Sinclair ( DINO ) |

| 0.23 |

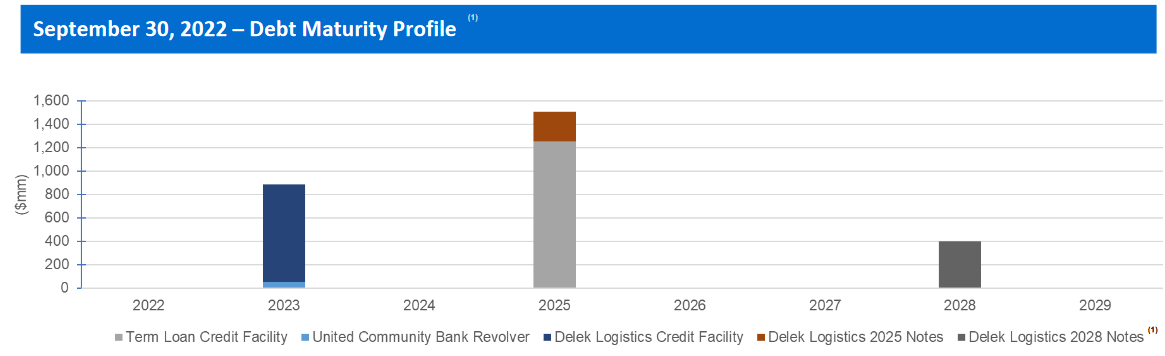

As we can clearly see here, Delek US Holdings is far more reliant than most of its comparable peers on debt. This is a concerning situation as the company may be exposing itself to too much debt-related risk. That is something that could be particularly relevant today, as interest rates have been rising. Thus, we may see Delek's costs increase fairly rapidly when it needs to roll over its debt at maturity. That could very easily be a concern in the near future, as the company has a significant amount of debt maturing this year:

{kind=link}

With that said, the majority of the debt maturing this year is the revolver for Delek Logistics Partners ( DKL ) and not a debt of Delek US Holdings itself. The fact that it is a revolver is somewhat comforting because that implies that the company can easily alter the amount that is actually outstanding and impose interest charges upon it. It is almost certain that the interest rate of this credit facility will increase in the near future, though, so it is still something that we should consider in our decision to invest.

Delek US Holdings does have $1.1538 billion in cash as of September 30, 2022, so it could conceivably pay off or significantly reduce the size of this debt at maturity, though. The risk here is probably not too bad, but we should expect to see Delek's interest costs increase in 2023, which will apply some downward pressure on its cash flows.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a downstream energy company like Delek US Holdings, one metric that we can use to value it is the price-to-earnings growth ratio. This ratio is a modified form of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to the company's forward earnings per share growth and vice versa. As I have pointed out in many previous reports though, pretty much everything in the traditional energy sector is quite reasonably valued. As such, we will want to compare Delek US Holdings' price-to-earnings growth ratio against that of its peers in order to determine which stock currently offers the most attractive valuation.

According to Zacks Investment Research , Delek US Holdings will grow its earnings per share at a 5.18% rate over the next three to five years. This gives the stock a price-to-earnings growth ratio of 1.16 at the current price, which is a reasonable valuation in today's market, albeit somewhat expensive compared to some of the upstream and integrated energy companies. Here is how Delek US Holdings compares to its refining peers:

| Company |

| PEG Ratio |

| Delek US Holdings |

| 1.16 |

| Valero Energy |

| 1.13 |

| Marathon Petroleum Corporation |

| 0.26 |

| Phillips 66 |

| 0.40 |

| HF Sinclair |

| 0.63 |

As we can see, Delek US Holdings appears to be a bit overvalued relative to its peers, although it still has a very low valuation in today's market. Indeed, outside of the traditional energy sector, almost nothing has a price-to-earnings growth ratio of very close to 1.0. Delek's reasonable valuation is further evident in the fact that its forward price-to-earnings ratio is 6.01 compared to 19.57 for the S&P 500 Index ( SP500 ). Thus, it may make sense to buy Delek today. However, I would recommend waiting for the price to come down, as the stock does look expensive compared to its peers and the company has significantly more debt and, therefore, more risk. As such, Delek probably should be trading at a discount to its peers, and it currently is not.

Conclusion

In conclusion, Delek US Holdings, Inc. is a downstream energy firm that could serve a useful purpose as a hedge and diversifier in a portfolio that contains a number of upstream companies. This is because the company does fairly well when energy prices decline, unlike upstream firms. However, there may be some near-term pressure on the company due to the impending recession. In addition, Delek US Holdings, Inc. looks a bit expensive relative to its peers that have stronger balance sheets. The company is still worth considering, though.

For further details see:

Delek US Holdings: Some Near-Term Concerns But Useful For Diversification