NVDA - Dell And VMware Earnings Preview: Less Than Meets The AI?

2023-08-30 08:30:26 ET

Summary

- Dell Technologies and VMware are expected to report their second quarter results tomorrow, August 31. The article takes a look at the chances of the companies beating earnings estimates, taking into account recent news.

- Since I haven't covered VMware stock before, I'll give a brief overview of the company, its profitability and balance sheet, and recent events.

- The recent performance of both stocks is largely attributable to the AI narrative, which I don't think is really justified in Dell's case and only indirectly so in VMware's.

- I consider VMware the better company, but I don't think either stock is a good investment at current levels, despite Dell's sub-10 P/E and VMware's arbitrage opportunity.

Introduction

Dell Technologies Inc. (DELL), the enterprise hardware giant, and VMware, Inc. (VMW), the virtualization specialist, are certainly two interesting companies to consider in the context of capitalizing on the coming artificial intelligence ((AI)) boom. Compared to stocks like Nvidia Corp. (NVDA), trading at a TTM P/E of nearly 90 , shares of DELL and VMW appear to be much more compelling opportunities. Granted, neither stock has a moat comparable to Nvidia, but at P/E ratios of 8.1 and 24 , respectively , they are worth a closer look. After all, the rising ((AI)) tide lifts all boats, or does it?

I covered DELL stock back in December 2022 in a comparative analysis with HP Inc. (HPQ), discussing the top reasons I believe Warren Buffett chose HPQ over DELL stock. In a later update , I looked at the two stocks again from the perspective of a long-term dividend growth investor. As such, I won't go into detail about Dell's fundamentals in this article, but will briefly review VMware, which I haven't covered before. Given the pending acquisition by Broadcom Inc. (AVGO), VMW's fundamentals may not seem that important, but are probably still worth a look in case the deal falls through. The main focus of the article, however, is to discuss my expectations for the upcoming quarterly reports (both DELL and VMW report tomorrow , August 31st), with an emphasis on whether and how the two companies will benefit from what appears to be around the corner.

VMware Inc. - Brief Overview

VMware is probably best known for its virtualization technologies on widely used x86-based servers. As a leader in this area, especially in data centers (another well-known virtualization technology, Hyper-V , comes from Microsoft Corp., MSFT ), VMware benefits from relatively high switching costs. When an IT landscape is built on a virtualization technology that allows the operator to run a wide range of applications that are completely separate and optimized for individual needs (including resources), switching to another technology is inherently difficult, labor intensive and risky. However, VMW has also become a leading provider of hybrid cloud computing offerings and is growing aggressively in this domain.

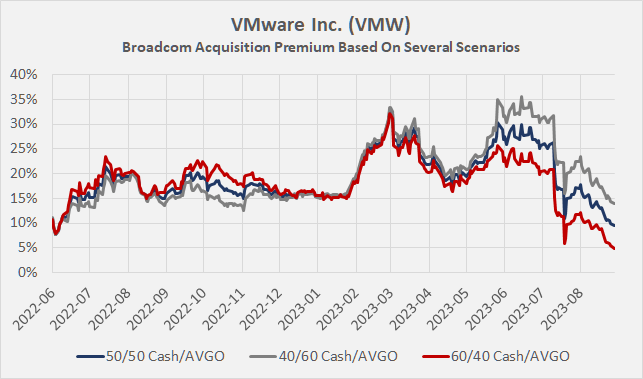

VMW was previously majority owned by Dell Technologies, but the 81% stake was spun off in late 2021. As part of the transaction, VMW agreed to pay a special dividend of $11.5 billion. The companies maintain a commercial agreement to ensure continued alignment of sales and marketing strategies, and development of certain technologies. In May 2022, VMware and Broadcom entered into a merger plan agreement that was approved by VMW shareholders in November 2022. The proposed transaction was cleared by U.K. regulators in August, and U.S. regulators did not challenge the takeover. Since the pre-merger waiting periods have expired, Broadcom expects the transaction to close by the end of October. As an aside, Dell CEO Michael Dell is still a major VMW shareholder, owning about 30.7 million shares , or about 40% of the voting power (p. 38, MW fiscal 2023 10-K ). VMW shareholders will receive either $142.5 in cash or 0.252 AVGO shares, subject to proration, so most likely a 50/50 split. Since AVGO stock is currently trading at about $890, this translates to a premium of about 10% to yesterday's closing price of VMW stock (Figure 1). The arbitrage opportunity is quite limited, but that is not surprising given the likelihood of the transaction going through.

Figure 1: VMware Inc. (VMW): Broadcom acquisition premium based on several scenarios (own work, based on daily closing stock price of AVGO and VMW)

{kind=link}

VMware is solidly profitable (gross margin in the low-to-mid 80% range), while operating margin of 19.3% (ten-year average, 3.1% standard deviation) is somewhat improvable. However, its free cash flow margin is typically 20% or higher (adjusted for stock-based compensation and working capital movements), confirming a solid cash flow conversion. Stock-based compensation is very significant, in my opinion, having accounted for about 25% to 30% of operating cash flow over the last three fiscal years. I'm not a big fan of such pronounced stock-based compensation, especially considering that the company adjusts its earnings per share ((EPS)) accordingly, suggesting better earnings power than is actually the case (after all, the shares granted must be repurchased to offset dilution). For example, VMW reported EPS of $1.49 in the first quarter of fiscal 2024, but the figure would have been 45% lower if stock-based compensation had been included.

VMware's return on invested capital ((ROIC)) has been quite volatile (19% ± 16% over the past decade), but the company generally generates a return above its estimated cost of capital .

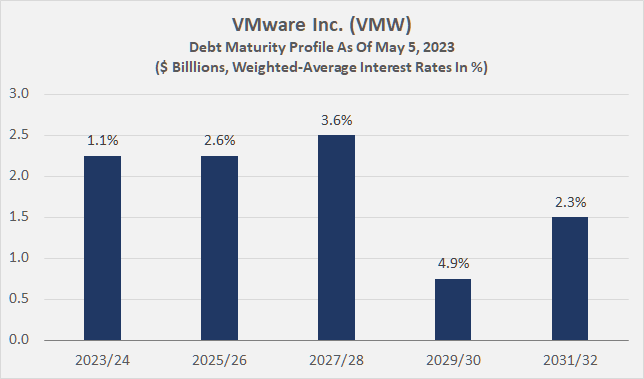

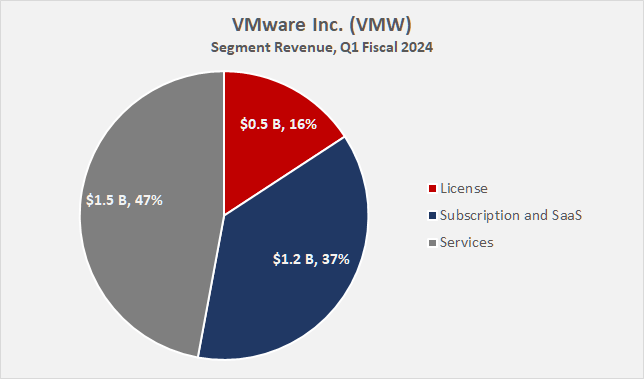

The balance sheet is in good shape, with net debt of only $3.9 billion at the end of the first quarter of fiscal 2024, translating to only 1.4 years of adjusted three-year average free cash flow. Upcoming maturities are not a problem given the solid free cash flow and high probability of refinancing at acceptable rates ( Baa3 rating with stable outlook ) should the Broadcom deal fall through. However, the debt maturity profile in Figure 2 shows that VMware's interest coverage ratio is likely to decline as a result of such refinancing transactions if interest rates remain high for longer or continue to rise. While this may sound worrisome, it should not be over-interpreted given the company's conservative interest coverage ratio of about 12 times free cash flow before interest and only moderate cyclicality given its significant reliance on subscription revenue (Figure 3) and strong growth. Subscription and software as a service (SaaS) continues to be the company's growth engine, with revenue growth of 25% in fiscal 2023 and 35% in the first quarter of fiscal 2024. However, one should also keep in mind that VMware is not currently expanding its services segment and licensing revenue will likely continue to decline (in fiscal 2023, revenue was already down 9.4% year-over-year).

Figure 2: VMware Inc. (VMW): Debt maturity profile as of fiscal 2024 Q1 end own work, based on company filings (own work, based on company filings) Figure 3: VMware Inc. (VMW): Fiscal 2024 Q1 segment revenue (own work, based on company filings)

{kind=link}

{kind=link}

Can We Expect Dell And VMware To Beat Estimates Tomorrow And Is The Recent Rally Justified?

Both companies' fiscal years end on the Friday closest to January 31, and Dell and VMware will report second-quarter fiscal 2024 results tomorrow. Given that both stocks have risen significantly alongside most other tech companies that stand to benefit from the coming artificial intelligence boom, their earnings reports will likely focus on this area of growth.

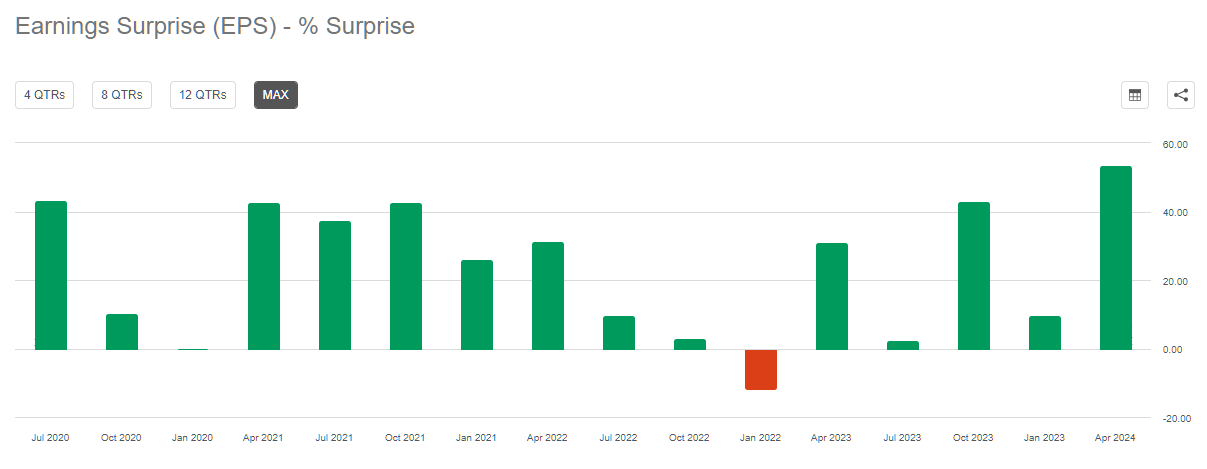

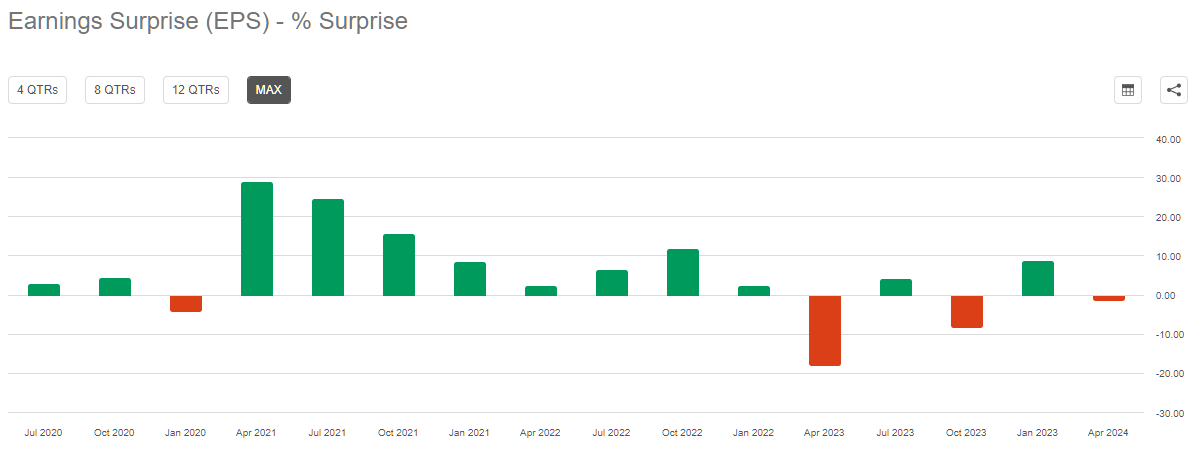

Let's take a look at how well management met analyst estimates on a quarterly basis. Dell routinely beats both EPS (Figure 4, 15 of 16 quarters) and revenue estimates (14 of 16 quarters). VMW has seen similar performance in revenue surprises (13 of 16 quarters), while the company has exceeded EPS estimates in only 12 of 16 quarters (Figure 5).

Figure 4: Dell Technologies Inc. (DELL): Quarterly earnings per share surprises (Seeking Alpha) Figure 5: VMware Inc. (VMW): Quarterly earnings per share surprises (Seeking Alpha)

{kind=link}

{kind=link}

It is quite likely that both companies will report positive surprises tomorrow. On a head-to-head basis, I think an earnings beat for VMware is more likely, given that analyst revisions have been fairly insignificant and relatively easy to project revenue. Downward earnings revisions for Dell Technologies have been fairly significant in recent months, but given HP Enterprise's (HPE) improved profit outlook released Tuesday, I wouldn't rule out a positive surprise either. It should be noted, however, that HPE's earnings and revenue estimate revisions were similarly insignificant to VMware's . Also, yesterday's news of HP Inc. having cut its free cash flow and earnings outlook is likely to weigh on market sentiment, even though the company is clearly end-consumer focused (HPQ stock is down 9% at the time of writing).

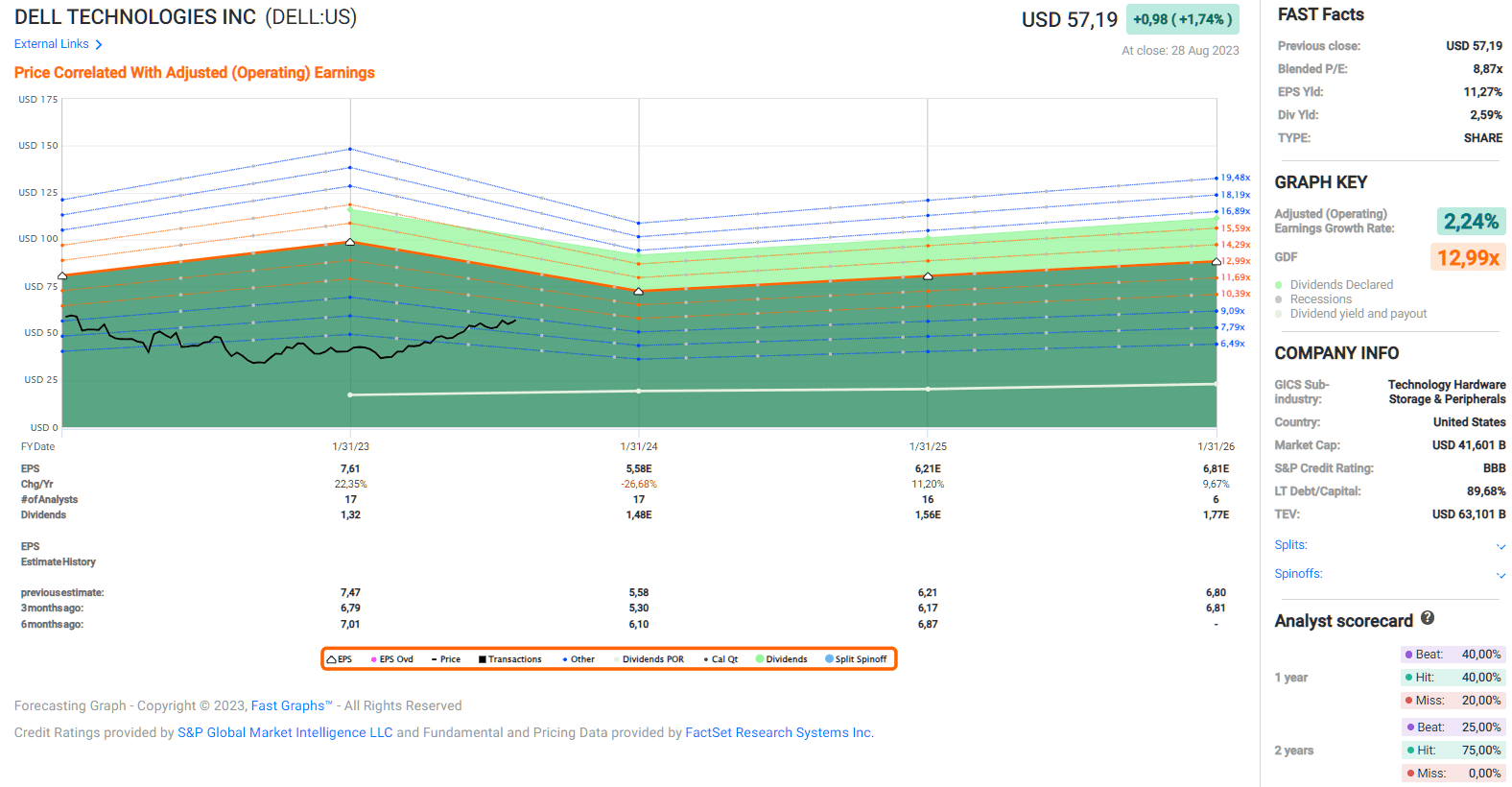

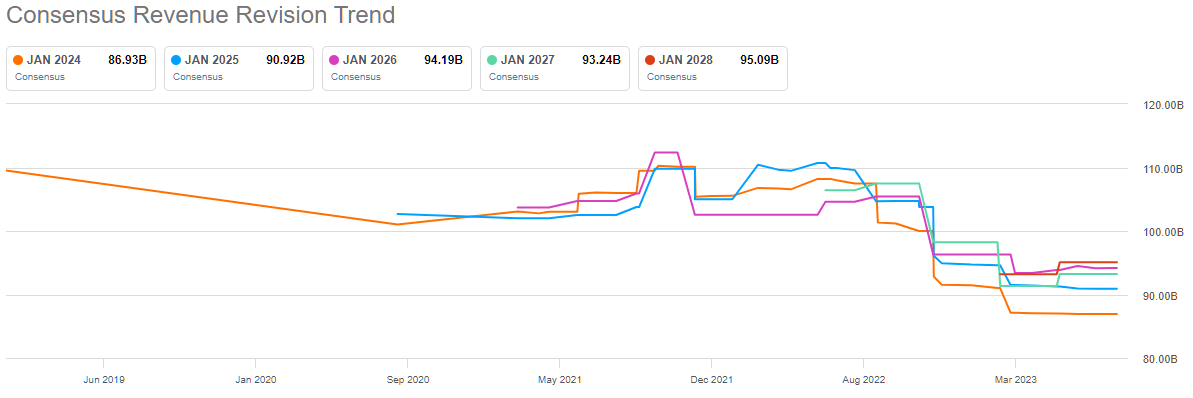

Far more important than the likelihood of beating or missing earnings and revenue estimates tomorrow is the fact that both stocks have rallied significantly amid the boom in AI-related stocks having started earlier this year. VMW and DELL shares are up 42% and 38% , respectively, year-to-date, and earnings multiples have expanded accordingly. The multiples expansions are almost entirely based on the AI narrative. In fact, also longer-term analyst estimates for Dell's earnings have been revised downward over the past six months - contradicting market expectations (Figure 6). Longer-term revisions to EPS and revenue estimates by analysts quoted by Seeking Alpha are similarly negative. Analysts even assume that Dell's revenue will not return to fiscal 2022/2023 levels (> $100 billion) until 2029 at the earliest (Figure 7).

Figure 6: Dell Technologies Inc. (DELL): Forecasting calculator, based on adjusted operating earnings per share (FAST Graphs tool) Figure 7: Dell Technologies Inc. (DELL): Revenue revision trend - annual basis (Seeking Alpha)

{kind=link}

{kind=link}

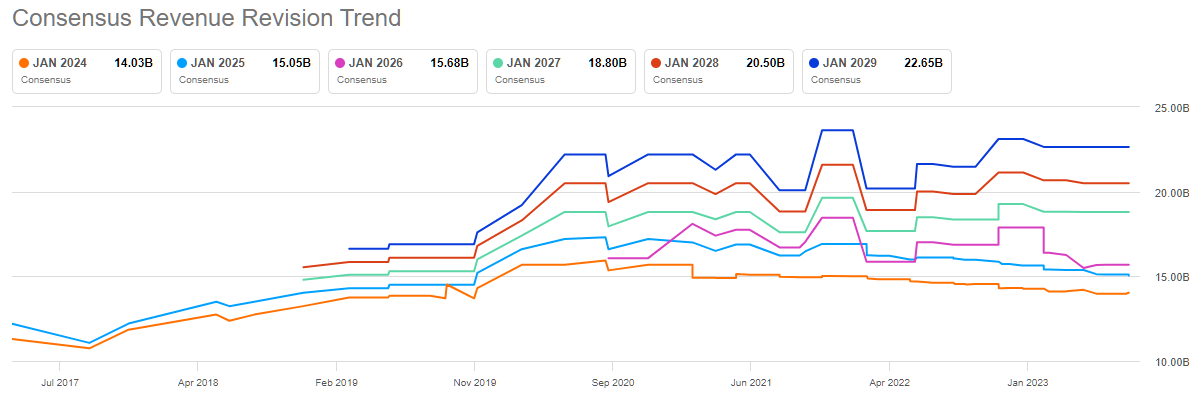

For VMW, revenue revisions for the next few years are also quite negative, but at least the company is expected to grow revenue in the low to mid-single digits - not what I would expect from a company "set to benefit strongly from the AI boom" (Figure 8).

Figure 8: VMware Inc. (VMW): Revenue revision trend - annual basis (Seeking Alpha)

{kind=link}

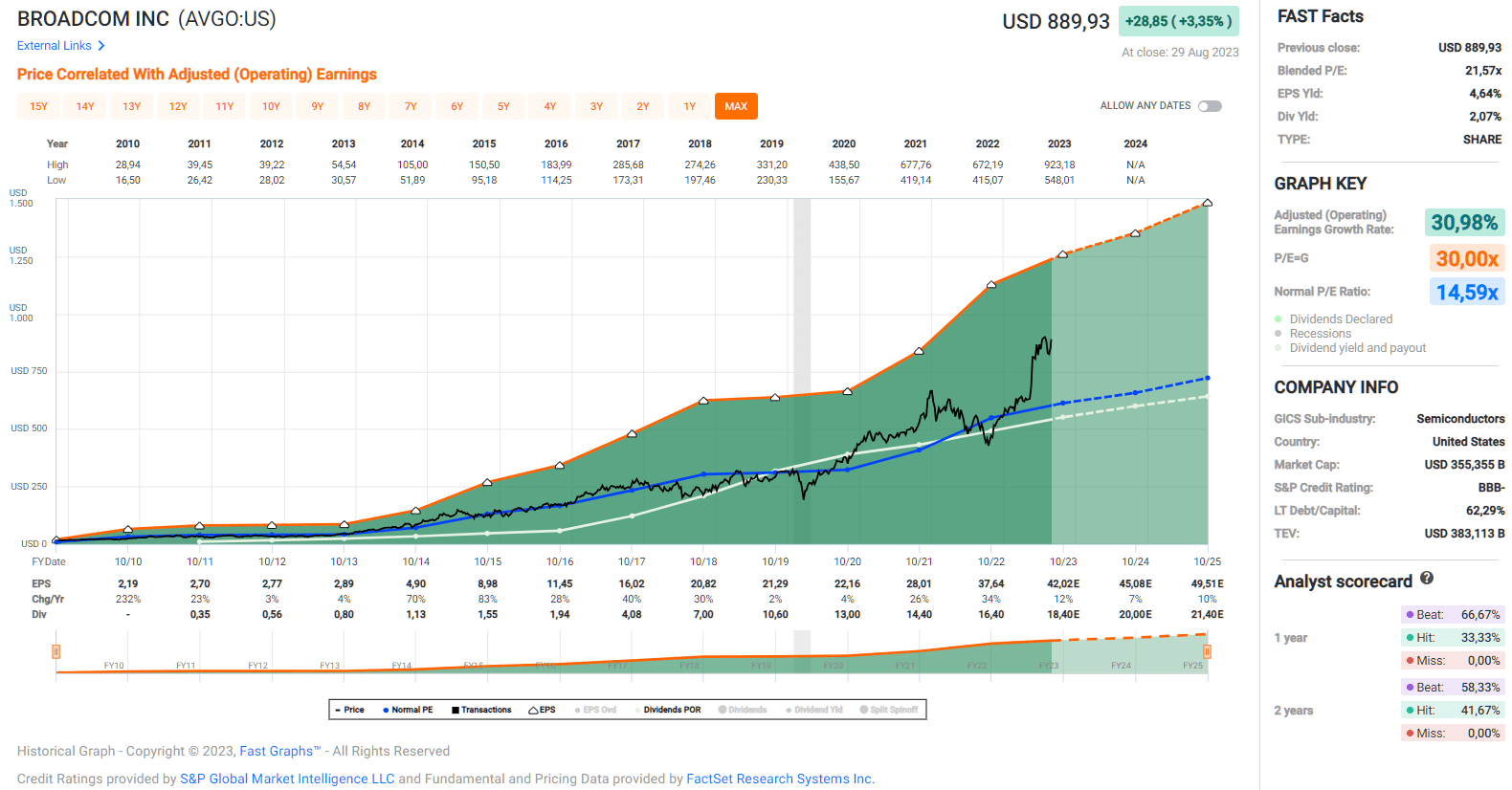

However, for fiscal 2029 and beyond , analysts have revised their expectations upward significantly in recent months. VMware recently made headlines regarding AI-powered autonomous workspace integration and its partnership with Nvidia to enable companies running on VMware infrastructure to easily customize and run generative AI applications. All in all, I think it's reasonable to conclude that VMware stock is trading less on actual fundamentals than it is on narrative. Most importantly, however, I think is the fact that AVGO's stock price supports VMW's valuation via the abovementioned takeover offer (Figure 1). AVGO stock trades at a high valuation compared to its historical average, and its balance sheet is definitely comparatively poor, but I think a point can be made that the company has an excellent track record, is well diversified, and its prospects are definitely good. With a blended price-to-earnings ratio of approximately 22 (Figure 9) and a free cash flow yield of 4.5% (stock-based compensation is much more modest than VMW), I don't think the stock is overvalued despite doubling from its October 2022 low. That, in turn, means that those who buy VMW stock today will benefit from some downside protection, but that assumes, of course, that the acquisition closes as planned. News of AVGO exiting the transaction for any reason - while highly unlikely - would likely send VMW stock sharply lower.

Figure 9: Broadcom Inc. (AVGO): FAST Graphs chart based on adjusted operating earnings per share (FAST Graphs tool)

{kind=link}

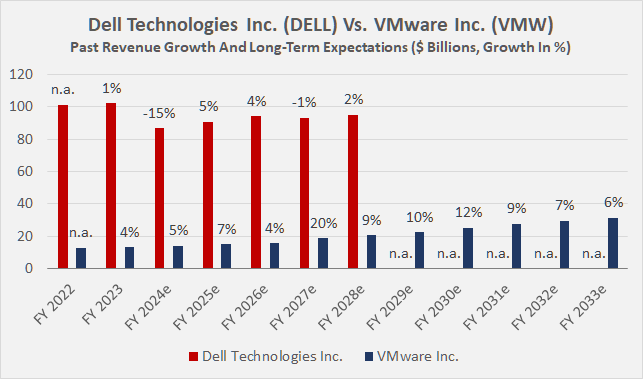

Returning to Dell, and considering that there are no revenue estimates that far into the future, one might think that the hardware giant will experience growth similar to VMware in later years. However, I don't think investors should overinterpret Dell's AI-related growth potential because it operates in a de facto commoditized industry and lacks a meaningful economic moat (its main competitors are HP Enterprise and Inspur in the server space, and IBM, Lenovo and HP Inc. in other areas). For comparability, I have plotted analysts' long-term revenue expectations for Dell and VMware in Figure 10.

Figure 10: Dell Technologies Inc. And VMware Inc. (VMW): Past revenue and long-term growth expectations (own work, based on data from Seeking Alpha)

{kind=link}

Conclusion

Dell Technologies Inc. and VMware Inc. will release their second-quarter results tomorrow. Given the solid track record of both companies, it is likely that earnings and revenue estimates will be exceeded.

Dell could post results better than expectations given rival HPE's improved earnings outlook reported yesterday, but that doesn't mean the market will treat the stock accordingly. Sentiment is far from optimal, also considering (consumer-facing) HPQ's recently reported poor outlook and the resulting share price action.

In my previous articles, I have outlined why I am not very enthusiastic about investing in Dell, and the recent surge has made me even more cautious, even though the stock is still trading at less than ten times earnings. As I've shown, the stock's recent performance is largely attributable to the AI narrative, and analysts' expectations have actually been revised significantly downward over the past six months, contradicting the market consensus. Currently, analysts believe it will take Dell until at least fiscal 2029 (likely longer) to return revenues to fiscal 2022/2023 levels. There is no doubt that Dell will benefit from the increasing adoption of AI, but it is important to remember that the company operates in a largely commoditized industry where competition is fierce. Having participated in IT infrastructure negotiations myself on several occasions, I realized that suppliers are in a difficult position given the relative ease with which bids can be compared.

In this context, I see VMware's moat as much more tangible and quite durable, as the company dominates the data center virtualization market and its cloud offerings are growing strongly. Revenue expectations for the coming quarters and years have also been revised downward, although not as significantly as Dell. Long-term expectations are quite solid (high single digit to low double digit revenue growth), but still somewhat modest given the stock's valuation. In my view, VMW stock - like DELL - has become disconnected from fundamentals, but for different reasons. While Dell stock has rallied almost entirely on the AI narrative, the market is (rightly) assuming a successful close of Broadcom's acquisition of VMW. Since VMware shareholders will likely receive around 50% of the consideration in cash and the other half in AVGO stock (0.252 shares for each VMW share), it's only natural that VMW stock is highly correlated with AVGO stock. Since I believe Broadcom is a great company, I have been thinking about opening a position indirectly through VMware, and capture a 10% premium in the process. AVGO stock has more than doubled since its October 2022 low, so it appears expensive, but I think the valuation is justified based on its solid track record and growth prospects. However, as a value investor, I require some margin of safety, which I don't think Broadcom stock currently offers. The (small) risk of the deal failing - which would likely send VMware stock plummeting - is another reason why I ultimately decided against this maneuver.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Dell And VMware Earnings Preview: Less Than Meets The AI?