NVDA - Dell Q3 Earnings Preview: Executing Well But Upside Is Limited (Downgrade)

2023-11-29 11:00:19 ET

Summary

- Dell Technologies Inc.'s Q2 results exceeded expectations, driven by improved demand for PCs and AI-enabled servers, leading to a share price increase of 40% since my July article.

- While I remain bullish on the company’s long-term potential, I see no possibility for a significant Q3 earnings beat and believe somewhat conservative guidance from management for Q4 is likely.

- It is safe to say that Dell shares are no longer undervalued, with these priced at a premium to peers and historical averages.

- All things considered, with Dell still facing significant headwinds and demand uncertainties, I don’t believe the current risk-reward profile is attractive enough, and I recommend investors look for prices below $70 per share.

Introduction

I lower my rating on Dell Technologies Inc. (DELL) from "Buy" to "Hold" as I believe shares present limited upside from current share price levels. I last covered Dell back in July, when I reiterated my "Buy" rating on the shares. Despite the company facing macroeconomic pressures driven by its strong long-term prospects, I continued to view Dell as a compelling long-term investment opportunity.

This is what I wrote last time out:

The company faces soft demand from consumers and enterprises due to cautious IT spending. However, there are positive signs of stabilization in PC demand, especially in the commercial segment, where Dell has a stronger market share. And while the short-term outlook for the PC industry remains uncertain, the long-term prospects are promising. Dell has been gaining market share consistently and offers a competitive product portfolio. Meanwhile, investors should focus on Dell's Infrastructure Solutions Group ((ISG)) segment, which accounts for 40% of its revenue. ISG focuses on cloud operations, on-premises storage infrastructure, and AI technologies, presenting significant growth potential for the company. Its strategic partnerships and industry-leading hardware make it well-positioned to capitalize on the increasing demand for cloud and AI solutions

The company's focus on increasing margins and delivering strong EPS growth bodes well for investors, offering attractive returns. Additionally, Dell's solid dividend yield provides an added benefit and as management is more committed than ever to reward shareholders, we should expect decent growth in the dividend as well.

Since my July coverage, Dell shares have performed extraordinarily well, with the share price up 40%. Furthermore, since I first expressed my enthusiasm toward Dell approximately one year ago, shares have delivered a total return exceeding 100%, driven in part by investor enthusiasm toward the company's AI exposure and the recovery of the PC industry, as well as the company easily surpassing the consensus with its Q2 results .

Now, going into this article, I can already tell you that my bullish stance toward the company hasn't changed. I remain bullish on Dell's long-term prospects within the PC and cloud infrastructure industry. However, despite my overall bullish view, valuation-wise, the company obviously isn't as attractive as it was 6 or 12 months ago.

Even as Dell management blows away the consensus with its Q2 results and guides for a strong end of the year, leading to a significant upgrade of my near-term expectations, the valuation multiples have come up significantly. As a result, shares no longer trade at a discount and even seem slightly overbought.

Furthermore, even as I remain bullish on the company's long-term potential, I see no possibility for a significant Q3 earnings beat ( release expected post-market on Thursday, November 30th) and believe somewhat conservative guidance from management for Q4 is likely. Therefore, I moved my rating to a "Hold."

I will take you through my findings and expectations in the remainder of this article.

Dell reported a blowout Q2 quarter, easily surpassing the consensus as demand improved

Before we turn to the expectations for next quarter and beyond, let's first quickly look back at the company's Q2 results , which it released at the end of August. Dell reported revenue of $22.9 billion, down 13% YoY, and RPO of $39 billion. While this shows that revenue is still down due to macroeconomic headwinds resulting in depressed PC shipments and IT infrastructure investments, this is an improvement from Q1, with revenue up 10% sequentially and the 13% YoY revenue decline being much better than the 20% decline reported in Q1. In fact, Dell reported a remarkably strong Q2 quarter, which blew away analysts' and my own expectations , beating the revenue consensus by 10% and EPS by a staggering 52.5%.

The beat was driven by the demand environment improving faster than anticipated, with PC demand improving sequentially much more significantly than expected and Dell seeing significant demand strength for its AI-enabled servers. Whereas I was expecting a gradual recovery instead of a V-shape, it seems like reality will sit somewhere in the middle as the industry showed some improvement in Q2.

Now, let's look at the performance under the hood by looking at the operating segments' performance, starting with CSG. Revenue for Dell's "PC segment" was down 16% YoY and up 8% sequentially to $12.9 billion, accounting for 56% of Q2 revenue, driven by a 14% YoY decline in units. Overall, in Q2, the PC market continued to show weakness, but also showed renewed strength as orders accelerated.

Furthermore, Dell's performance was much better than that of many peers, which was driven by the company's little reliance on consumer revenues as Dell is mainly focused on the commercial PC market, which accounts for 79% of its CSG revenue.

Dell continues to be a leader in the PC industry with a market share of just over 16%, which is up meaningfully from the 11.4% reported in 2011. Dell has a strong PC offering, and this, combined with its focus on the commercial market, has allowed it to gain a lot of market share over the last decade. As a result, the company is the third largest PC supplier, only trailing Lenovo (LNVGY) and HP (HPQ).

Dell's market share in the PC industry (Statista)

On the one hand, this makes the company sensitive to the economic climate with the PC industry highly sensitive to consumer health (as clearly visible today), but at the same time, this makes the company a primary beneficiary of the projected 9.1% growth CAGR of the PC industry through 2028, primarily driven by a rebound in PC sales over the next several years and a low basis point in 2023. In the long term, the normalized growth rate probably sits in the range of 1-3% due to the maturity of the market, but this nevertheless presents a decent growth outlook for Dell. While the PC industry sure is not the preferred market to invest in, from current levels, it looks quite attractive, and with Dell continuing to gain share, it should have no trouble growing this segment strongly once the economy recovers.

However, I am much more bullish on the company's ISG segment, which I project to be the company's main growth driver in the long term. This one provides comprehensive solutions for enterprise IT infrastructure. It encompasses a range of products, services, and solutions designed to address the needs of modern data centers and IT environments. Moreover, it focuses on cloud operations and on-premises storage infrastructure, exposing the company to AI, data analytics, cybersecurity, and HPC technologies.

Dell is often an understated beneficiary of the rapidly growing demand for cloud computing and AI. Yes, it is not as exciting as Nvidia (NVDA), but Dell is the leading supplier of on-premises cloud servers and storage solutions with a market share of 30%, making it a crucial enabler of hybrid cloud and on-premises cloud solutions.

Dell server hardware market share (Dell)

Dell has been partnering with many different cloud providers to make its on-premises servers suitable for hybrid-cloud offerings, and has also been partnering with the likes of Nvidia and Meta Platforms (META) to make its servers the top choice in the industry by featuring Nvidia GPUs and Meta's Llama 2 AI models.

Dell has been rapid in bringing its newest AI servers to market, giving it an edge over the competition in this high-demand environment and allowing it to offset some of the IT hardware weakness. PowerFlex, Dell's proprietary software-defined storage solution, has now grown eight consecutive quarters, with demand in Q2 more than doubling year-over-year, highlighting the demand improvement. Furthermore, the company's PowerEdge XE9680, its first 8x GPU PowerEdge server, using the latest NVIDIA H100 GPU accelerators, is the fastest ramping new solution in Dell's history, and it has a backlog of over $2 billion for this product alone.

As a result of this demand improvement and new product releases, Dell reported revenue of $8.5 billion for the ISG segment in Q2, down 11% YoY but also up 11% sequentially as server and storage demand improved. A lot of this is driven by AI, with this technology now accounting for over 20% of server order revenue.

All in all, Dell is seeing demand for its infrastructure solutions improve, and the company's leadership in this segment means it is a primary beneficiary of the growing demand for AI. The company has the broadest Gen AI infrastructure portfolio that spans from the cloud to the client, and with many enterprises preferring workloads to be run on-premises, Dell could see substantial growth for its AI-enabled servers in the near to medium term. This, combined with Dell increasing its production capacity for these new products, should support a stronger recovery in the second half of the year.

Meanwhile, the better-than-expected top-line growth also allowed for a very impressive bottom-line performance. Dell reported a 270 basis points YoY improvement in the gross margin to 24.1% or $5.5 billion, which is outstanding considering the top-line decline and was driven by lower input costs and pricing discipline.

This also allowed the company to improve its operating margin by 120 basis points to 8.6% or $2 billion, as the declining top-line was offset by the improved gross margin and lower operating expenses (down 4% to $3.6 billion). This resulted in a net income of $1.3 billion, up 1% YoY. This represented an EPS of $1.74, up 4%, which also saw a lower share count benefit.

These improved margins led to an FCF of $3.1 billion, which allowed the cash position on the balance sheet to increase by $0.7 billion at the end of Q2, incorporating the effect of $1.1 billion in debt paydown and $0.5 billion in capital returns. This meant the company ended the quarter with $9.9 billion in cash on the balance sheet and debt of slightly below $16 billion, representing a core leverage of 1.6x.

Dell has improved its financial health over the last several years as it used the excessive cash flows from the COVID-19 electronics demand boom to strengthen its financial position . For reference, net debt improved to just $6.1 billion at the end of Q3 from a pre-covid level of $36.7 billion. As a result, the company is in a much better position today, making it a lot more attractive to investors as it increases the risk profile and allows for more significant shareholder returns.

Shares currently yield just below 2%, which is decent, especially when considering the growth potential. The payout ratio currently stands below 20%, leaving much room for upside and meaning the dividend is very well covered. As earnings growth is projected to be strong going forward, I expect the same for the dividend and believe a 6-9% dividend growth CAGR is achievable. Again, it is the company's much better financial position that makes it a meaningfully more attractive investment compared to previous years.

In closing of this segment of the article, I believe it is safe to say that Dell performed really strongly, and as it easily surpassed expectations, I see plenty of room for an upgrade of my financial projections, and this outperformance makes me quite bullish on the company's Q3 results.

So, without further ado, let's see what we can expect upcoming Thursday.

I see little room for Dell to beat Q3 expectations as PC headwinds persist

Moving our view to the company's fiscal Q3, management has guided for revenue to be in the range of $22.5 billion and $23.5 billion with a midpoint of $23 billion, flat sequentially. This includes the expectation for revenue in both the CSG and ISG segments to be roughly flat sequentially as well.

Furthermore, as management expects some pricing headwinds to offset the disciplined cost management, the gross margin is projected to fall by 150 basis points sequentially to a level of around 22.6%, down 110 basis points YoY. Meanwhile, management believes it should be able to further lower operating expenses sequentially, leading to an EPS of $1.45 plus or minus $0.10.

In the overall business, management has been seeing signs of stabilization, and while I am pretty sure not all weakness has passed, these are promising signs of improvement. Yet, the company is also seeing continued weakness among large enterprises when it comes to IT spending, and we can see this reflected in Q3 PC shipments as well.

In Q3, PC shipments fell 9% YoY for the entire industry. Dell PC shipments were down 14.2% YoY compared to the 14% reported by Dell in Q2. Note that Dell's fiscal quarter is slightly off, so this data from Gartner does not include the October quarter, while this is included in Dell's Q3 results. Crucially, in the October quarter, we saw a significant slowdown in the improving PC market momentum with shipments down 24% month-over-month. This will likely be reflected in Dell's Q3 results.

Furthermore, Dell's 14.2% drop in shipments in the calendar year Q3 was worse than its leading peers, with HP reporting growth of 6.4% and Lenovo reporting a limited 4.4% decline. This underperformance for Dell represents the continued weak IT spending from enterprises, a category to which Dell has more exposure, as explained before. Moreover, this also means that Dell's market share has fallen to 16.1% from 17% one year earlier.

Overall, this means Dell shipments are down just under 1% sequentially. However, including the October underperformance and the expected pricing pressure, I now project a sequential volume decline of 1.1% and a revenue decline of 1.4% for the CSG segment to approximately $12.72 billion.

Furthermore, while demand for Q4 is still unclear, the expectation is currently that this might come in slightly below expectations as it turns out that companies further up in the supply chain are still working down inventory. Analysts expect notebook shipments to be down 13% sequentially in Q4 and 3% YoY, slightly worse than earlier anticipated. This also means that current guidance from Dell could be slightly too aggressive when considering depressed demand levels remaining and average selling prices falling. In Q2, Dell did not see much of an impact from the lower prices, but I expect this to become more meaningful in Q3 and Q4. Therefore, I also expect a Q4 sequential improvement to come in below management's prior expectations.

However, despite this negative view of the PC industry, which continues to lag, I am optimistic about the company's ISG segment. Positively, growth in cloud infrastructure investments is expected to remain strong in the second half of the year, according to the latest calculations by IDC , which increased its FY23 growth outlook to 10.6% from a previous 7.3%. Meanwhile, weakness in non-cloud infrastructure is expected to persist, with this projected to be down 7.9% YoY in FY23. Furthermore, worldwide IT spending is projected to total $4.7 trillion in 2023, an increase of 4.3% from 2022, according to the latest forecast by Gartner . This should further support growth for Dell.

Overall, as I explained before, I believe the improving demand for the company's infrastructure solutions, in combination with the ramp-up in production of its newer AI-enabled products, for which there clearly is a lot of demand, should support growth in the ISG segment in the second half of the year. Therefore, while management guides for flat sequential growth in this segment in Q3, I believe it is safe to expect a slight sequential increase of 2-4%, offsetting the PC weakness. Moreover, this should persist in Q4.

As a result, I now expect Q3 ISG revenue of $8.71 billion at the midpoint, resulting in a total revenue expectation of $22.88 billion, sitting slightly below the midpoint of management's guidance, primarily due to more significant weakness in the company's CSG segment.

In addition, I expect the pricing pressure to impact the company's gross margin in line with management's expectations but cost-saving efforts to offset some of this weakness, resulting in an EPS of $1.44, in line with guidance. Both these EPS and revenue levels sit far above my July projections as demand, nevertheless, is a lot better than I anticipated before.

Yet, this also means that I am not expecting Dell to meaningfully beat the consensus again in Q3 as it did in Q2.

Outlook & valuation - Is DELL stock a buy, sell, or hold?

Following the strong Q2 results, management has also increased its FY24 expectations. It now guides revenue to be in the range of $89.5 billion and $91.5 million, down 12% at the midpoint and far above my expectations. This also includes higher EPS guidance, with EPS now expected to come in at $6.30, plus or minus $0.20.

However, I believe this guidance by management might be slightly on the optimistic side of things as the weakness in PC demand in Q3 and the first months of Q4 was more significant than anticipated. While I do not foresee any issues in Q3, I expect management to narrow its guidance range to the lower end.

Nevertheless, I remain bullish on the company's long-term prospects because it is exceptionally well positioned to benefit from the rebound in PC demand in coming years and its excellent market share in on-prem server hardware, giving it meaningful exposure to the growing demand for AI globally. Therefore, I believe long-term growth should still come in at the high end of management's guide range of 3% to 4% revenue growth and 6%+ EPS growth. This is what I wrote previously, and this still stands:

In the following years, I expect Dell to report revenue growth in the mid-single digits, somewhat above its own projections. I expect solid demand in its ISG segment and better-than-expected growth in PC demand. As the company continues to improve margins and buy back its shares, EPS growth should remain in the low double to high single digits range, driving very decent shareholder returns, especially when considering management's commitment to sustainably increasing the dividend in line with FCF growth.

Taking into consideration these expectations, the company's better-than-expected Q2 results, and solid guidance for Q3, I increase my near-term estimates and fiscal FY24 revenue guidance while staying conservative in my FY25 growth expectations, as weakness could persist for longer, resulting in a gradual recovery in both its operating segments. I continue to project a more significant recovery in fiscal FY26 and growth to normalize in the following years.

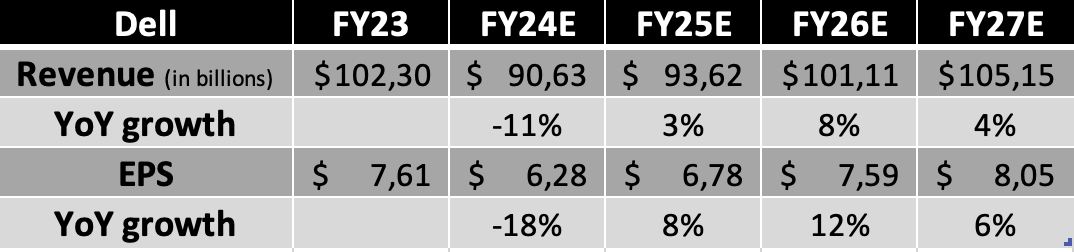

Financial projections (Author)

{kind=link}

With the company showing more pricing power and resiliency than I anticipated in July, my near and long-term expectations have come up quite a bit. And yet, the valuation multiples have meaningfully expanded as well as this positive increase in financial projections has been fully priced into the shares, and a bit more, in recent months.

As a result, shares are trading at close to 12x this year's earnings, up significantly from a 9.5x multiple back in July. Therefore, it is safe to say that shares are no longer undervalued, with these priced at a premium to peers and historical averages.

While I do believe the company deserves to be trading at a premium, shares are nowhere near as attractive as they were 6 to 12 months ago. Based on management's strong performance in recent months, the company's favorable competitive positioning, and the projected long-term outlook, I believe a 12x multiple is fair. Based on this multiple and my fiscal FY25 EPS projection, I calculate a target price of $81, leaving an upside of just below 10%. However, based on my FY26 EPS and a 12x multiple, I project limited returns for investors of just 8.5% annually (10.5% including dividends).

All things considered, with Dell still facing significant headwinds and demand uncertainties, I don't believe the current risk-reward profile is attractive enough, and I recommend investors look for prices below $70 per share before increasing or initiating a position in Dell, especially with a significant Q3 earnings beat unlikely and potentially conservative guidance from management.

Therefore, following a significant share price increase since my July article, I move my rating to "Hold" from "Buy" and recommend investors stay on the sidelines for now.

For further details see:

Dell Q3 Earnings Preview: Executing Well, But Upside Is Limited (Downgrade)