NVDA - Dell: This Industry Leader Is Still Undervalued

2023-07-21 05:10:55 ET

Summary

- Dell Technologies is a promising business with robust long-term investment potential, despite facing a challenging macroeconomic environment and soft demand from consumers and enterprises due to cautious IT spending.

- Dell's Infrastructure Solutions Group segment, which accounts for 40% of its revenue and focuses on cloud operations, on-premises storage infrastructure, and AI technologies, presents significant growth potential for the company.

- Despite a decrease in revenue YoY, Dell's strong cost discipline resulted in a strong YoY and sequential gross margin performance, and the company is committed to its long-term targets.

- Dell remains very well-positioned, resulting in a very strong long-term outlook that should allow it to outperform peers.

Investment thesis

I maintain my Buy rating on Dell Technologies Inc. ( DELL ) and update my revenue and EPS estimates following my in-depth analysis of the company, the underlying industry trends, and its latest financial results.

In my analysis, Dell stands out as a promising business with robust long-term investment potential. It is navigating a challenging macroeconomic environment, but it has shown impressive resilience in its recent performance. The company's share price has surged 46% since November 2022, primarily driven by the enthusiasm surrounding the emergence of AI and a more positive outlook for PC sales.

The company faces soft demand from consumers and enterprises due to cautious IT spending. However, there are positive signs of stabilization in PC demand, especially in the commercial segment, where Dell has a stronger market share. And while the short-term outlook for the PC industry remains uncertain, the long-term prospects are promising. Dell has been gaining market share consistently and offers a competitive product portfolio. Meanwhile, investors should focus on Dell's Infrastructure Solutions Group ((ISG)) segment, which accounts for 40% of its revenue. ISG focuses on cloud operations, on-premises storage infrastructure, and AI technologies, presenting significant growth potential for the company. Its strategic partnerships and industry-leading hardware make it well-positioned to capitalize on the increasing demand for cloud and AI solutions.

The company's focus on increasing margins and delivering strong EPS growth bodes well for investors, offering attractive returns. Additionally, Dell's solid dividend yield provides an added benefit and as management is more committed than ever to reward shareholders, we should expect decent growth in the dividend as well.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

Dell is trying to navigate a very challenging macroeconomic environment

Since I last covered Dell in November 2022, the share price performance has been impressive, with this up 46%, primarily driven by the enthusiasm surrounding the emergence of AI and the improving outlook for PC sales.

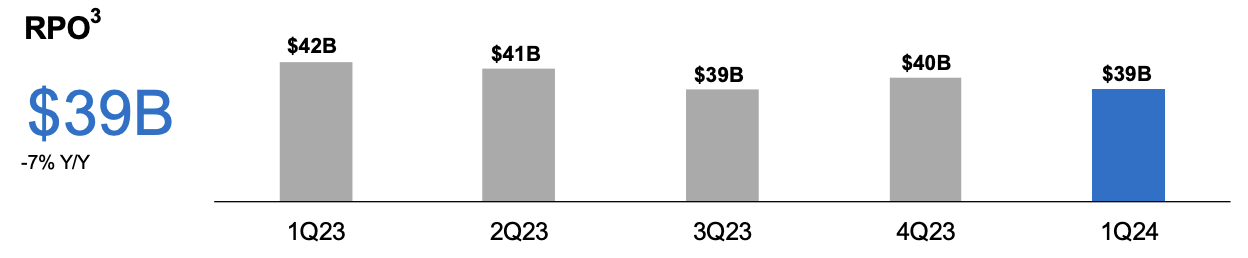

Looking at its latest financial results, Dell reported Q1 revenue of $20.9 billion, which beat the Wall Street consensus by $630 million despite being down 20% YoY. The leading subject during the Q1 earnings call remains the treacherous operating environment Dell management needs to navigate. The company is seeing very soft demand across both consumers and enterprises as these are staying cautious and deliberate in their IT spending. In short, Dell practically saw weakness across the board. The only financial positive was the growth in recurring revenue, which was up 6% YoY. Also, RPO stood at $39 billion and remained relatively stable.

{kind=link}

On a more positive note, Dell is seeing some stabilization in PC demand, which is obviously a good development. The improvement is ahead of management expectations. This resulted in Q1 CSG revenue of $12 billion, down 23% YoY. This was mainly driven by the decline in PC shipments but partially offset by higher average selling prices. Somewhat surprisingly and despite the worsening demand for PCs, Dell, as opposed to competitors, has not been lowering its prices to clear out channel inventory, resulting in higher average selling prices. Crucially, despite not lowering its selling prices, the company was able to lower inventories by $800 million sequentially in Q1 and $2.3 billion YoY.

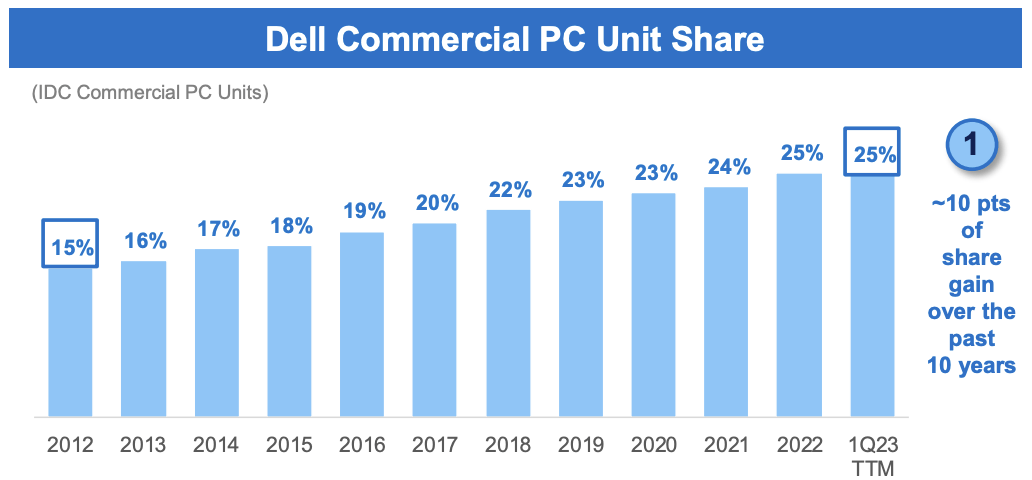

Furthermore, the performance in the commercial PC segment remains much stronger (down 18%) compared to consumer (down 41%) as the decreasing consumer spending due to high inflation and the threat of a recession drive down consumer sales. Luckily, Dell is largely focused on the more valuable and resilient commercial market as this accounted for $9.9 billion in Q1, compared to just $2.1 billion in consumer PC sales. Dell also holds a stronger market share in the commercial PC segment, as highlighted below.

{kind=link}

In ISG, demand was very soft overall as deals were pushed forward or deal sizes were reduced. This resulted in a YoY decrease of 18% to $7.6 billion for this segment, simply because enterprises are cautious with their IT spending. Still, Dell did see continued solid demand for storage solutions. Dell also saw a meaningful increase in server demand, specifically for AI-optimized solutions. Yet, management remained conservative here and warned investors that a significant impact of AI on the company's financials should not be expected over the next couple of quarters as Dell is still working on rolling out the product and satisfying demand.

Moving to the bottom line, despite the decrease in revenue YoY, strong cost discipline resulted in a strong YoY and sequential gross margin performance. The company lowered its operating expenses by 6% to partially offset the decrease in revenue, leading to a 2 percentage point increase in gross margins to 24.7%. Management plans on lowering operating expenses further over the remainder of the year to further offset the top-line weakness.

Despite these cost-saving efforts, operating income still fell by 25% to $1.6 billion, while net income decreased by 33% due to a lower operating income and a higher tax rate. Looking at the revenue decline, these lower bottom-line margins are no surprise and should rebound strongly once demand returns and Dell gets back into growth mode. As a result of these lower margins, EPS decreased by 29% to $1.31 and beat the consensus by a staggering $0.46 or 35%. This was helped by a lower share count.

At the end of Q1, Dell had $9.2 billion in cash and investments on the balance sheet and a total debt position of $29.37 billion. Dell has been rapidly improving its balance sheet over recent years, paying down its debt using the spectacular cash flows generated in the pandemic electronics boom. This has reduced its core leverage from 3.2% pre-pandemic to 1.7% today. In Q1, the company repurchased 6.1 million shares of stock for $251 million and paid $276 million in dividends, which was well covered by operating cash flow of $1.8 billion.

Shares currently yield 2.71%, which is a very decent starting yield considering management's target of returning 40 - 60% of adj. FCF to shareholders, and with the expected growth over the next several years, this should result in some decent dividend growth. Also, the dividend is very safe with a payout ratio of just 19%, leaving plenty of room for further dividend increases, even if the financial performance disappoints. So, while I definitely do not view Dell as a stock to buy specifically for its dividend, it is a very nice and secure extra for Dell investors. Also, Dell is increasingly focusing on its shareholders with the company returning more and more cash. This is what management stated during the earnings call regarding this:

We have returned $5 billion to shareholders over the last six quarters through share repurchase and dividends, approximately 96% of our adjusted free cash flow over that time period, well in excess of our 40% to 60% return target. We value our relationships with our shareholders and we are actively listening to your feedback. We increased our annual dividend by 12% last quarter and we recently put in place new governance enhancements to our Board and oversight structure.

Now, let's dive into the latest developments and trends for each of Dell's operating segments to get a better idea of its long-term prospects.

Investors should be focusing on the ISG segment

Whereas Dell might be most well-known for its PCs, it derives only 60% of its revenues from PC shipments. The other 40% comes from its infrastructure solutions group, which provides comprehensive solutions for enterprise IT infrastructure. It encompasses a range of products, services, and solutions designed to address the needs of modern data centers and IT environments. Moreover, it focuses on cloud operations and on-premises storage infrastructure, exposing the company to AI, data analytics, cybersecurity, and HPC technologies. The company has cloud partnerships with Microsoft ( MSFT ), Oracle ( ORCL ), SAP ( SAP ), and VMware ( VMW ). This is what I wrote regarding this segment in October and not much has changed:

All in all, this is a very broad segment for Dell, with huge growth potential and a way to offset the cyclical weakness of the hardware segment. The growing digitalization will be a driving force for Dell in this segment. Areas such as cloud, hybrid cloud, working from home, and cybersecurity will be growing topics in which enterprises will be forced to spend more. With the huge exposure Dell has in this sector already, it is in a great position to leverage its IT hardware to offer more digital services.

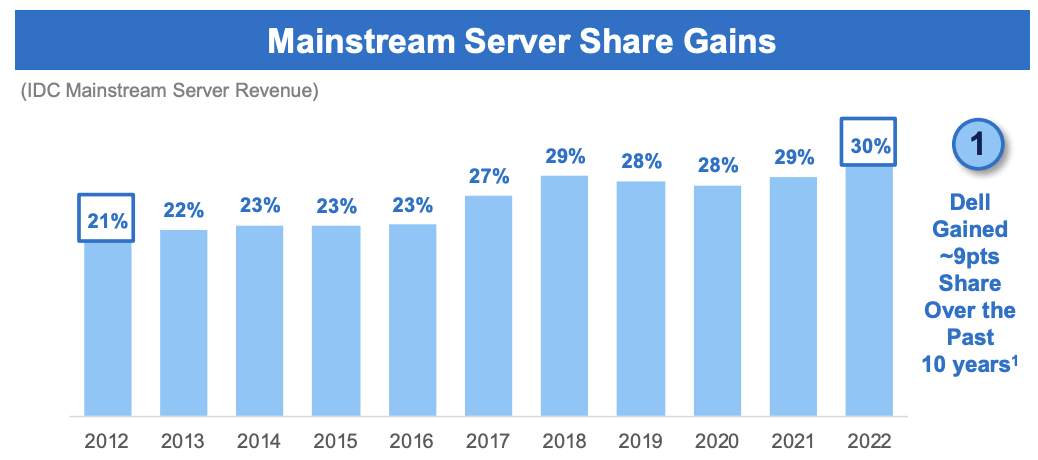

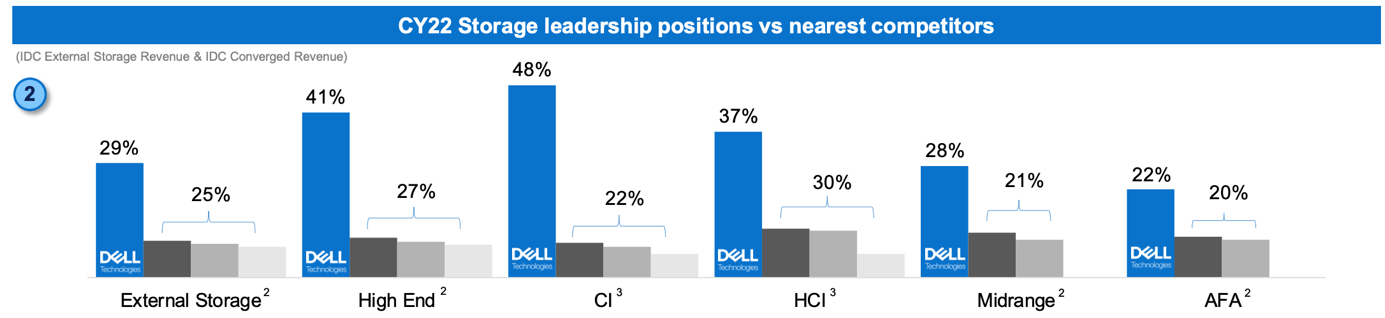

I expect this segment to remain Dell's most important growth driver over the next several years, especially with IT spending on cloud, data storage, and AI rapidly expected to increase. And Dell is a very much understated and underestimated beneficiary here. We should not forget that Dell and HP ( HPQ ) still account for a third of worldwide server hardware sales and are crucial in hybrid cloud and on-premises cloud servers. According to IDC , Dell even holds a 30% market share in mainstream servers, up from 21% in 2012. This highlights the company's positive development in this industry. And as one of the leading manufacturers of server hardware, Dell is poised to benefit from the rapid expected growth in server capacity, driven by the integration of heavy AI models.

{kind=link}

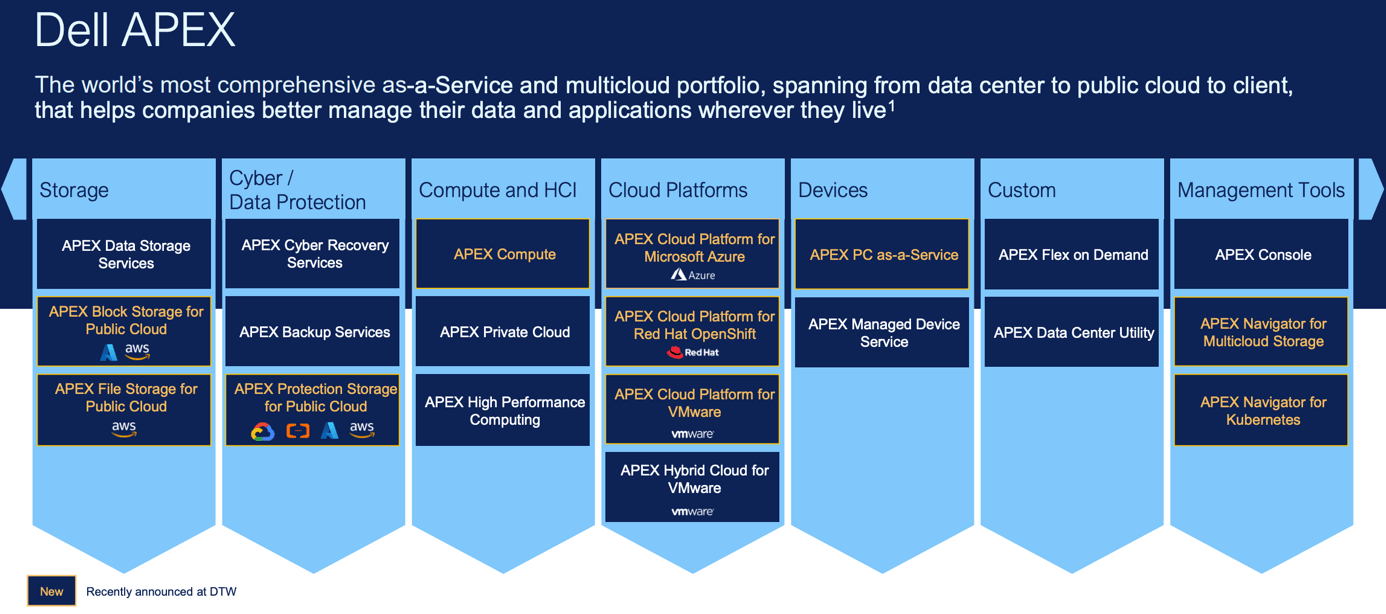

Dell should do especially well because it focuses on on-premises and hybrid cloud hardware and software solutions. Dell Apex, the company's cloud software and hardware stack, can deliver on-premises, off-premises, and cloud hybrid solutions to solve customer needs. This allows it to also benefit from the rapidly growing demand for hybrid cloud solutions - an industry that is expected to grow at a CAGR of close to 22% until 2028.

{kind=link}

In addition, the company's on-premises cloud storage solutions should see meaningful growth over the next decade as developments like the growing volume of unstructured data and increased demand for AI, IoT, automation, and analytics drive increased demand. Fortune Business Insights believes this particular industry will grow at a CAGR of 23.4% through 2030. Dell should be a primary beneficiary of this, being the industry leader and having a strong market share advantage .

{kind=link}

Furthermore, Dell is leveraging its on-premises datacenter and IT specialty to make use of the boom in AI demand in its very own way. Through a partnership with Nvidia ( NVDA ), the company has started project Helix which works on integrating generative AI in on-premises datacenters for enterprises. Dell combines its servers with Nvidia's H100 GPU to allow companies with on-premises datacenters to enjoy the full capabilities of generative AI. This also includes Nvidia AI Enterprise software, which supports Nvidia's large language model framework for building responsible generative AI chatbots, and includes Dell's CloudIQ for optimal security. The company offers versions of its Dell Precision Workstations optimized for machine learning, deep learning, and artificial intelligence, all of which are key components for building a future AI-enabled workflow. Featuring Xeon CPUs and Nvidia GPUs, this hardware offers state-of-the-art technologies for building, training, and developing AI workflows.

With demand in AI skyrocketing and the hybrid cloud approach looking like the way to go for enterprises, Dell is positioning itself very well. Moreover, through this partnership with Nvidia, the company is currently far ahead of competitors in cloud and AI, allowing it to take market share from the likes of HPE, IBM ( IBM ), and Cisco ( CSCO ).

Considering everything discussed above, clearly, the growth potential for this operating segment is massive with exposure to fast-growing verticals like on-premises cloud storage, hybrid cloud, and AI. And still, despite this exposure and even industry-leading positions, Dell is often seen as just a PC hardware company. Clearly, it is much more, and the growth potential should not be understated.

While the PC industry performance might look depressing lately, the long-term outlook is better than perceived

While I believe that investors should be increasingly focusing on the company's performance in its ISG segment, for now, CSG remains the largest one, and incredibly important to this segment is the overall health and growth in the PC industry, both long-term and short-term. Sadly, PC shipment data has not looked overly positive lately. PC shipments in Q2 dropped for a sixth consecutive quarter in a row as the industry remains impacted by a weak macroeconomic environment and a shift in IT budget spending. Yet, there is a positive development visible in the data as shipments only dropped by 13.4% YoY in Q2, down from a staggering 29% in Q1, according to IDC. This shows that while demand is still weak, this is slightly returning as inventories normalize and customers are willing to invest in hardware again.

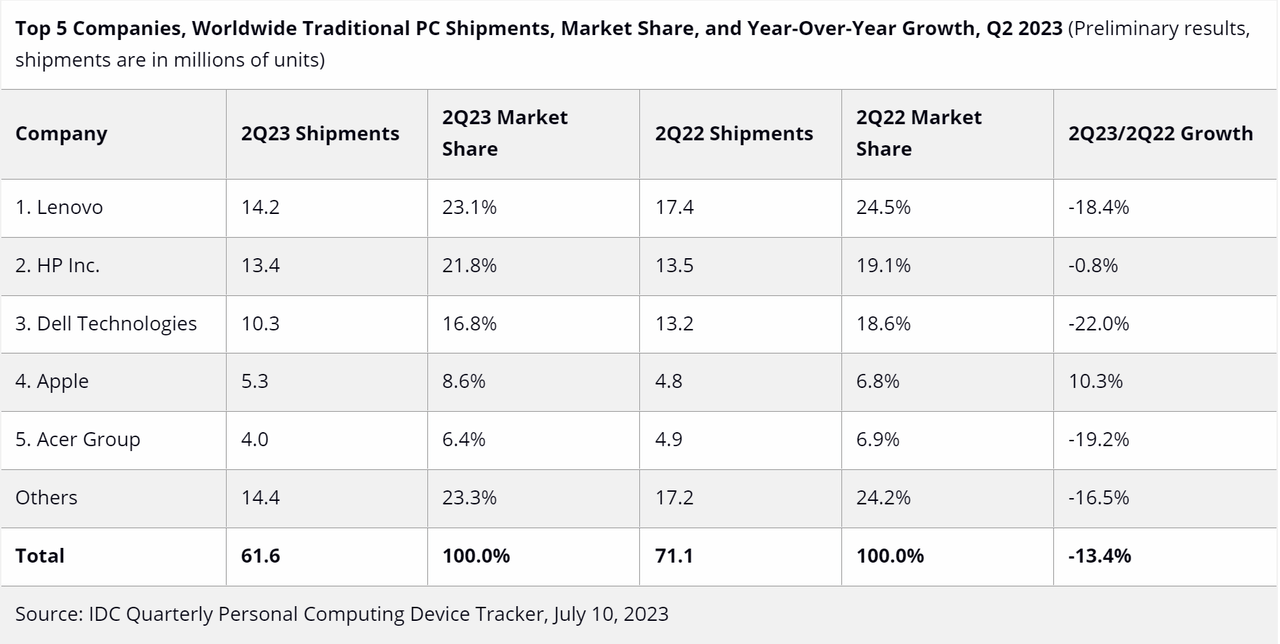

Still, one of the worst performers in the second quarter was Dell as it saw a 22% decline in shipments, resulting in a 1.9 percentage point drop in market share to 16.8%, according to data collected by IDC. Most PC manufacturers saw double-digit declines, apart from Apple, which grew its shipments by 10%, now accounting for 8.6% of global PC shipments. Lenovo and HP remained the industry leaders, with a 23.1% and 21.8% market share, respectively.

{kind=link}

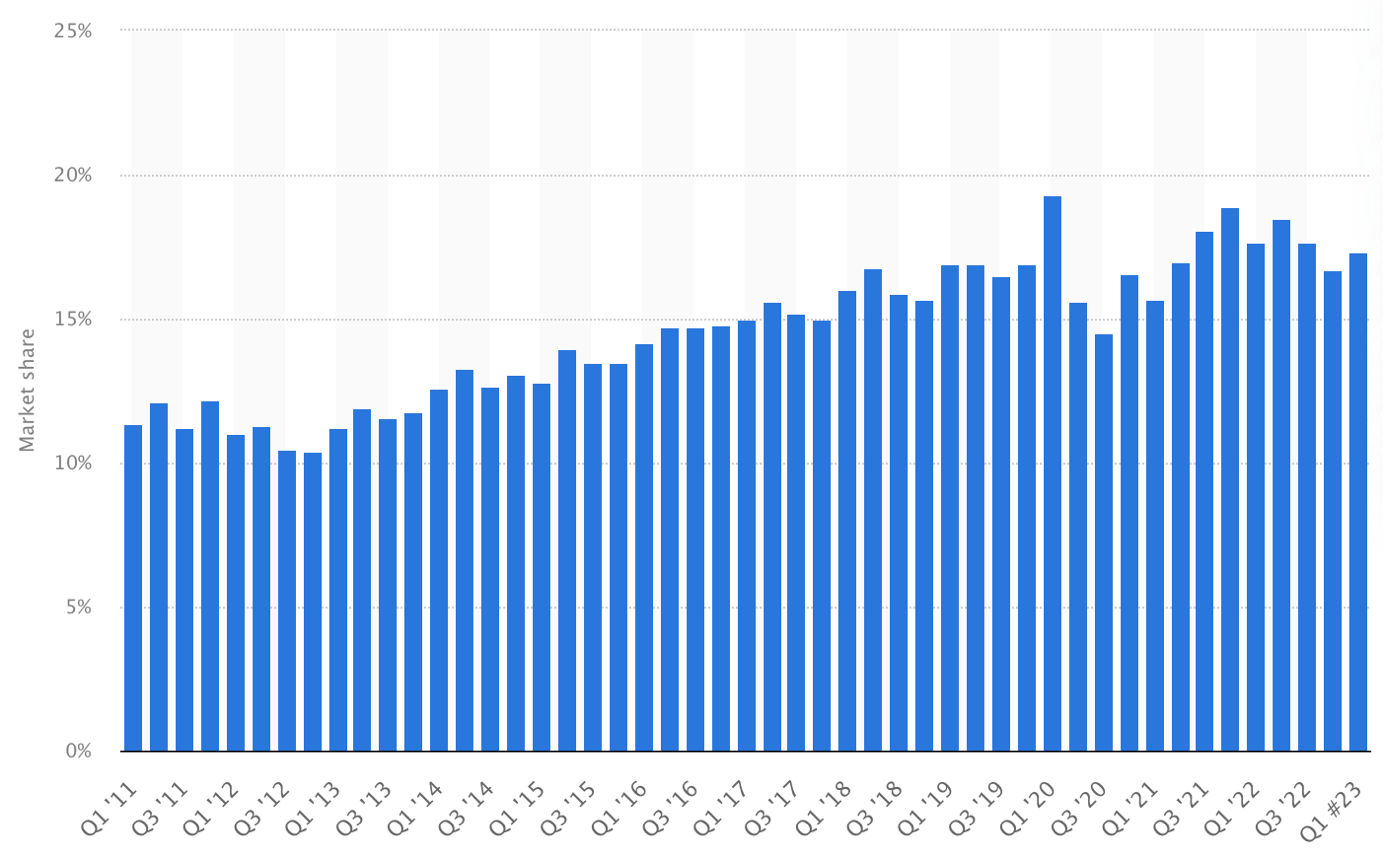

Overall, this paints a pretty negative picture for Dell as the worst performer in Q2. Yet, this data should be taken with a grain of salt as this highly fluctuates from quarter to quarter (as visible in the graph below), driven by new product releases and a whole bunch of other factors. It is essential that investors focus on the long-term trends, and this remains incredibly positive for Dell if we look at the graph below.

Dell market share in PCs (Statista)

{kind=link}

We can see that Dell has been gaining market share over the last decade relatively consistently. In 1Q11, Dell only held a market share of 11.4% and this has grown to the 16.8% in the last quarter, which, despite Q2 being a relatively weak quarter for Dell, is still a meaningful increase. Crucially, the market share has only once dipped below 16% over the last 2 years and has risen to a high of 19%. In a very competitive industry, Dell's positive market share trend is an ode to its improving technology and competitiveness compared to leaders HP and Lenovo. Dell is incredibly strong, especially in the enterprise segment, which should allow it to keep taking market share. During the Q1 earnings call , management also stated that it remains confident in its ability to remain a structural share gainer over the long term.

Also, the company's PC offering today is incredibly competitive across most segments, possibly the strongest it has been in a long time. Several sources rate it as either the number one or two choice across the PC industry. The company has a well-diversified offering from budget to high performance, high build quality, more customization across the board than any competitor, and uses the newest and most advanced materials. Some may call the company cutting-edge from these perspectives.

According to my analysis, Dell should be able to slowly keep increasing its global share in the PC market over the next several years. The biggest threat to this is probably Apple as it keeps expanding its popular and superior laptop and PC offerings. As highlighted by IDC's Q2 data , Apple outperforms its PC industry peers and even overtook Dell in the first quarter, according to Canalys. As Apple keeps expanding its PC offering and, therefore, its market share, this could very well make it harder for Dell to do the same.

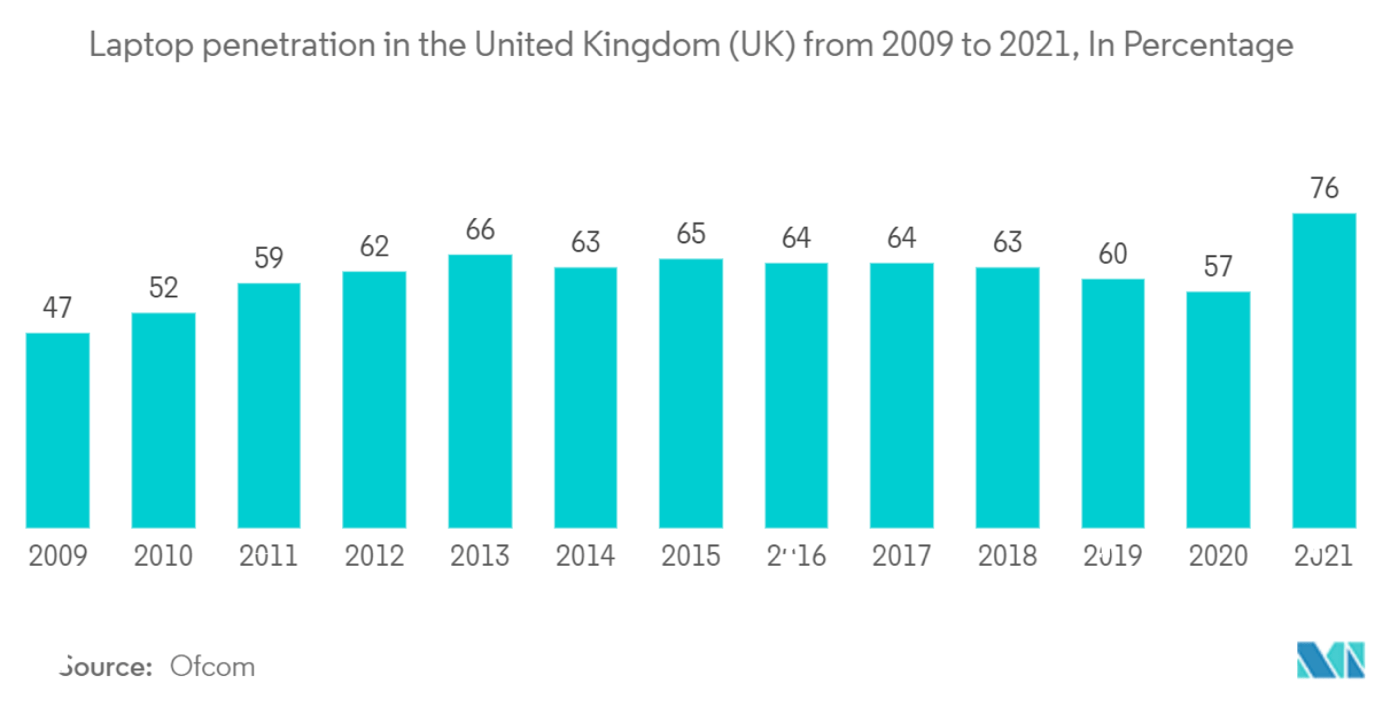

The global PC industry is projected to grow at a 9.1% CAGR through 2028, primarily driven by a rebound in PC sales over the next several years and a low basis point in 2023. Long-term, the normalized growth rate probably sits in the range of 1-3% due to the maturity of the market. Still, several important trends could boost demand for PCs. One of the most important ones is the growing adoption of the portable laptop variant due to the increase in remote working. Ideally, employees work with a laptop if their work location varies, whereas, before the COVID-19 pandemic, most employees worked on on-premises PC systems. This development in the adoption of remote working has massively increased laptop adoption. For example, in the UK, this stood at only 47% in 2009 but this has risen to 76% in 2021, with a clear "covid boost" from 2020 to 2021.

{kind=link}

And while this percentage will most likely not remain this elevated, a higher normalized level is highly likely, probably in the high 60 to low 70 percent range. The result of this higher adoption is a higher PC user base, which results in more PC sales across the cycle, which could boost the industry's normalized growth rate to 3-5% through the economic cycles (also taking into account rising prices as technology improves and the rate of inflation).

Outlook & DELL stock valuation

Looking ahead, management expects to see similar trends witnessed in Q1, with continued cautious IT spending. Yet, management is expecting the PC market to slowly return to historical sequentials as demand slowly picks up again. In ISG, management expects muted growth as businesses continue to push forward IT spending, though the massive growth in AI and demand for storage and server hardware could offset some of the weakness.

According to management, these expectations should result in Q2 revenue to be in the range of $20.2 billion and $21.2 billion, or down around 21.5% YoY based on a midpoint of $20.7 billion. By individual segment, management projects CSG revenue to be flat sequentially, resulting in revenue of approximately $12 billion, down 22.5% YoY. This shows a sequential and YoY improvement compared to Q1. For the ISG segment, management expects to report a low single-digit decrease YoY, resulting in revenue of approximately $7.45 billion, down 21.5% YoY, and showing a further deceleration as businesses remain cautious with IT spending. Furthermore, the gross margin is expected to decrease by 50 basis points sequentially due to more competitive pricing. This should result in EPS of around $1.10, plus or minus $0.10.

The Q1 results and Q2 outlook result in Dell maintaining its fiscal FY24 revenue expectation of a decrease of between 12% and 18%. At the midpoint, this results in a revenue expectation of $86.96 billion, with a sequential improvement in the second half of the year. In addition, management is upgrading its EPS expectation to $5.50, plus or minus $0.25, driven by a better-than-expected impact from cost savings.

Overall, despite the near-term uncertainty and challenging macroeconomic environment, Dell remains committed to its long-term targets of 3% to 4% revenue growth and 6%+ EPS growth.

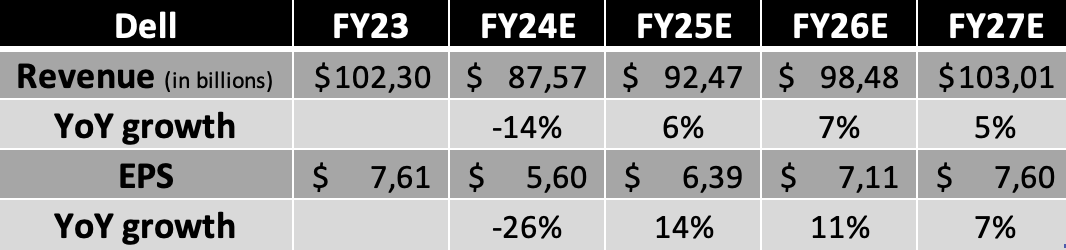

Following this guidance from management, the Q1 results, and promising business developments, I now project the following results for the years until the company's fiscal FY27 (ending January 2027).

Financial projections (Author)

{kind=link}

(Q2 estimate includes revenue of $20.71 billion and EPS of $1.13)

Shortly explaining these estimates, I now expect Dell to report a revenue decline of 14% in FY23 as overall PC demand remains weak throughout the year and businesses keep pushing forward IT investments. Still, we should see an improvement in demand in the second half of the year, with an especially decent performance in Q4. Also, increasing demand for on-premises storage and AI-specialized hardware will be a tailwind for Dell this year. Meanwhile, the decline in EPS is expected to come in at 26% as a lower revenue basis causes thinner margins, despite management's excellent efforts to bring down costs.

The company's fiscal FY25 should be a recovery year, although I do expect this to gradually improve instead of a robust V-shaped recovery as consumer spending will remain under pressure in FY24 and businesses remain cautious. Still, this should drive decent revenue growth for Dell, which in turn should cause an improvement in margins and therefore stronger EPS growth. In the following years, I expect Dell to report revenue growth in the mid-single digits, somewhat above its own projections. I expect solid demand in its ISG segment and better-than-expected growth in PC demand. As the company continues to improve margins and buy back its own shares, EPS growth should remain in the low double to high single digits range, driving very decent shareholder returns, especially when taking into consideration management's commitment to sustainably increasing the dividend in line with FCF growth.

Overall, the outlook for Dell over the next few years is much better than its historical growth profile. Therefore, the business also deserves to be awarded a higher valuation. Shares are currently valued at a forward P/E of approximately 9.5x, which is above its average P/E of 8.5x after a significant share price boost over recent months and in line with peers like HP. Yet, the growth expectations for Dell are far more impressive than its peers. Looking at its P/E non-GAAP (FY3), it is among the cheapest of its peers.

As I see even more upside for this business due to its excellent PC offering and significant exposure to enterprise IT hardware, software, and AI, I believe a relative premium for this business is justified compared to its historical valuation and peers. Therefore, an 11x P/E is warranted when considering the growth potential, moat, and capital return commitments from management.

Based on this P/E and my FY25 estimate, I calculate a target price of $70 per share, leaving an upside of approximately 30%. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Conclusion

Dell's recent share price performance has been impressive, primarily driven by AI's emergence and improved PC sales outlook. While Q1 revenue showed a decline YoY, the company managed to beat Wall Street consensus and show operational resilience by improving its margins, nevertheless.

The Infrastructure Solutions Group segment presents significant growth potential for Dell, accounting for 40% of its revenue. This segment focuses on cloud operations, on-premises storage infrastructure, and AI technologies, making it a crucial driver for Dell's future success. The company has a strong moat here and is well-positioned to fully benefit from increasing demand. At the same time, the PC market faced some struggles, but Dell remains competitive and has been gaining market share over the years. This should position it favorably to benefit from the recovery in PC demand over the next few years, while its competitive offering should allow it to keep gaining share.

Overall, the company's long-term outlook is positive, backed by its commitment to target 3-4% revenue growth and 6%+ EPS growth. Driven by a recovery of both its segments, these financial targets should be achievable.

With a target price of $70 per share and an upside of around 30% from its current share price of around $54, I believe shares offer very decent value and a sufficient margin of safety at below $57 per share. Therefore, I maintain my buy rating on the company despite a significant run-up in the shares over recent months. Dell remains favorably positioned for market share gains and above-average growth, making it a top pick among its peers.

For further details see:

Dell: This Industry Leader Is Still Undervalued