CA - Desert Mountain Energy: Value Or Value Trap?

2023-07-26 19:22:26 ET

Summary

- The company recently announced a shift to New Mexico after facing permitting delays. This resulted in a stock price implosion.

- Investors have not conducted due diligence on the New Mexico pre-existing gas operation. We will explore its potential to generate revenues.

- If New Mexico pans out and Arizona is revisited several years from now, (assuming permits are issued) the stock might represent a speculative value play.

- The long term plan to expand via multiple plants is intact but the time lines have been extended. Patience is required.

Recently Desert Mountain Energy ( OTCQX:DMEHF ) announced it was uprooting its Arizona helium plant due to permitting delays. Investors were less than thrilled, with the stock taking quite the battering having dropped over 60%. In this article we will take a non-emotional viewpoint and see if Desert Mountain has a future. If so, what is that future and what does it look like long-term? Will the company generate revenue off the announced pivot from Arizona to New Mexico? What happens after New Mexico? Is Arizona still in the cards?

What Happened To Desert Mountain Energy

Since our last coverage of DME several events have taken place. First the company engaged in a private placement with Beacon Securities. This put negative pressure on the stock as private placements often do. We posted a buy rating when the stock was $1.77 CDN. Since then, a series of delays occurred that culminated in the need for a fracking permit. This permit was delayed and rather than sit and hope you get a permit eventually, the company is moving the helium production plant to New Mexico . While this is a logical move and necessary, it is not a popular move with the masses.

Yet, Arizona is still in the cards. It will just take some time. For the patient gambler, these developments might offer up interesting decisions. DME could be a value stock, but it could also represent a value trap. I am better on the former.

Value Investing or Value Trap

I've made my biggest money (and lost gobs too) when value investing. My absolute favorite thing is to understand a stock in great detail and invest in it when it is beaten to ribbons and unloved. Then sit back and wait for the masses to catch on. This takes time, sometimes years, but if you have smart management at the helm, a war chest of capital and assets, then turn around plays can pan out. At times though, they do not. Hence, we must ponder & model most likely, least likely, and worst-case outcomes to come up with a risk assessment. Given my high-risk tolerance, I am betting that DME is now a value play.

Show Me The Money - Desert Mountain in New Mexico

While stock traders are currently very emotional concerning the implosion in DME share price, what investors should be looking at is --- will the New Mexico property generate meaningful revenues and will DME resume Arizona operations given time?

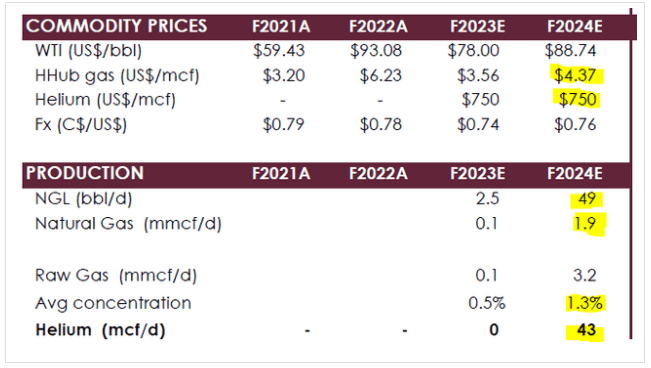

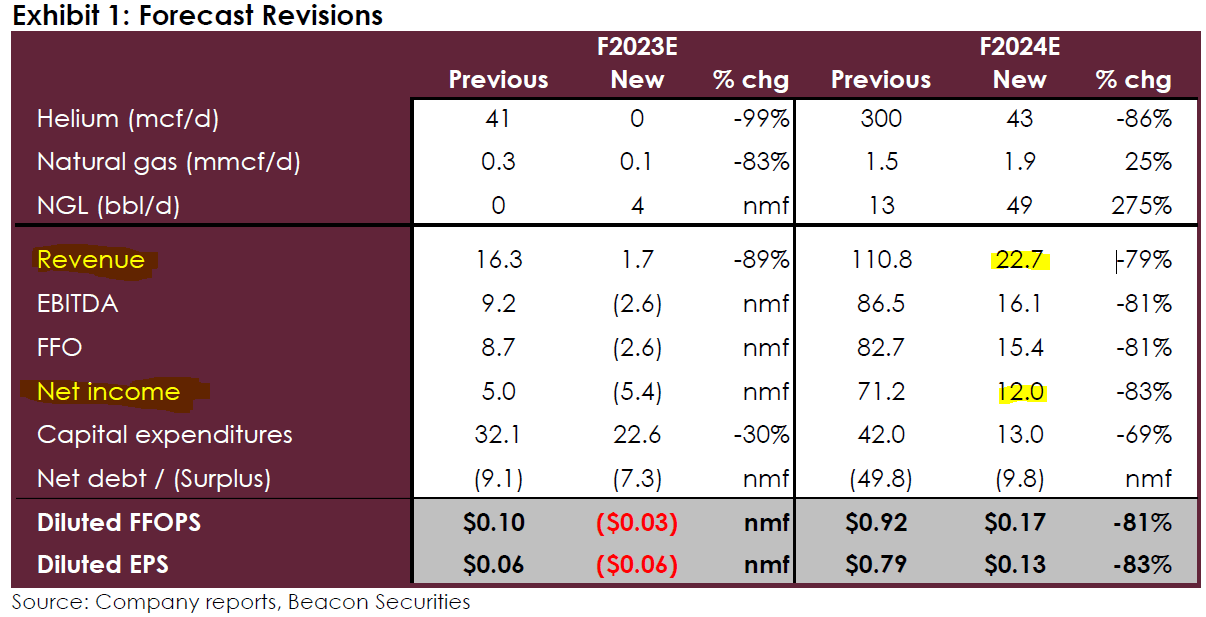

Let's look at this 76,500-acre property in New Mexico and run some simple math to see if this endeavor could generate revenue. Looking at the Beacon report we see that DME acquired 188 wells and 1 water disposal well from a pre-existing natural gas operation in New Mexico. That is quite a lot of wells that can be reworked to increase production hopefully. Let us take a quick glance at the Beacon Securities numbers concerning potential revenue:

{kind=link}

Potential Production Values (Beacon Financial)

Per press releases, we see a 25% compression fee and a 24% royalty fee on the natural gas. NGL's appear to have a 24% royalty fee only. Helium has no such fees. Now let's play discovery to see what the property might potentially yield if things pan out with a little luck.

Possible Revenue Stream

First investors need to realize that New Mexico field could generate revenue from 4 sources: Natural gas, Oil Condensates (aka NGL), Helium, and lastly the workover rig. Hydrogen might be a potential 5th source given time, but it is too early to estimate that. An additional source of revenue is the trucking fleet and potentially the Arizona solar facility along with carbon credits. Let's run some calculations based on the Beacon report broken down by each asset.

Potential Natural Gas Revenue

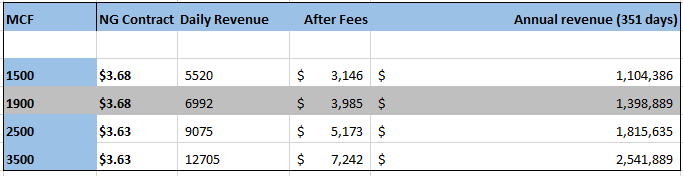

First, we need to look at the estimated existing production numbers for New Mexico field at 1.5 mmcf/d and multiply that by 1000 to get mcf. I am also factoring in 2 weeks of downtime for repairs annually. The current contract (that expires in April) for the natural gas is priced at $3.68 an mcf. The follow up contract could be for more (or less) depending on market conditions.

To calculate revenue just multiply 1500 x $3.68 and factor in the 25% reduction via the compression fee and a 24% reduction for royalty payments.

We have added a 1900 MCF field to correspond with Beacons report from July 6th (in gray below). It should be noted that the 24% compression fee may or may not go away post April when a new natural gas contract should come into play. If the fee goes away, then obviously Natural Gas revenues will increase by 24%. However, we will assume the compression fee stays to error on the side of caution and to keep our estimates low.

{kind=link}

Potential Natural Gas Revenue (Author / Beacon)

Potential Oil Condensate Revenue

Next up is oil condensate (aka NGL), Beacon places this estimate at 49 barrels a day in 2024. Note these figures include a -24% reduction due to the royalty fee but no compression fee. Also factored in is 351 days of production and 2 weeks of downtime.

Oil prices vary but we can use WTI (West Texas Intermediate crude oil) as a rough basis to estimate revenue. WTI can be found here . Currently WTI is at $78.89 USD a barrel as of 7/25/23. Hence using $75 dollars for NGL revenue seems logical but we will show a possible range of $60, $75, and $90 to give readers various possibilities due to oil price fluctuations.

Potential Oil Condensate Revenue (Author / Beacon)

Potential Helium Revenue

DME will not have to pay a royalty fee of 24% on the helium or the 25% compression fee. We will assume various helium rates below using 351 days and a helium grade of .007% (early production) to .013% (2024 production estimate via Beacon noted in gray).

Potential Helium Revenue (Author / Beacon)

Carbon Credits and Trucking Revenue

Potential solar facility revenue is currently unknown as is any potential environmental credits. We will assume this is carbon sequestration since the Federal government is pushing that very strongly via the Inflation Reduction Act. Per DME concerning New Mexico and carbon :

{kind=link}

Potential Carbon Capture Credits (Desert Mountain Energy)

Trucking revenue is about 276k a quarter per company filings. We might assume this revenue increases with time as additional trucking hardware were purchased. The workover rig and the drill rig should also contribute to revenues, but I am not including them since we have no color concerning how much they might bring in revenue wise. Trucking revenue is estimated at $1,104,000 annually. Solar is unknown as is any CO2 sequestration revenues.

Revenue Guesswork

In this section we will look at short term revenue estimations assuming the lowest values. This assumes no optimizations or improvements.

Then we will look at mid-range and lastly high estimates which would assume optimizations, higher flow rates, and high oil prices given time. These are just rough assumptions and should be taken very lightly. Consider them guesswork subject to great variation and error on the side of caution. Natural gas revenue might increase (or decrease) due to market fluctuations.

Potential DME Revenue 2024E (Author / Beacon)

Potential DME Revenue 2024E (Author / Beacon)

Desert Mountain Energy Financials

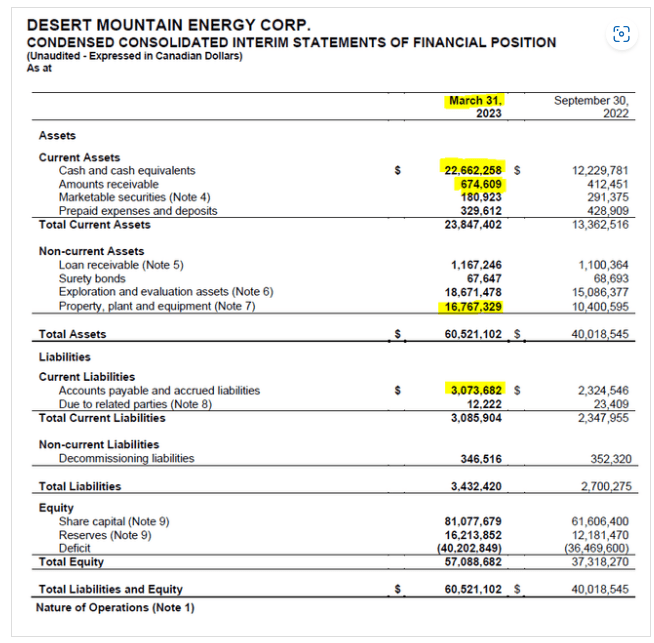

Given the below financials and the above revenue estimates, a future capital raise in the short term is unlikely. Long-term the company can fund future plant construction from organic revenues but if they were to want to accelerate production of future plants to say building 5-10 at once they would obviously need a partner with deeper pockets or they would have to approach financial mechanisms to fund accelerated construction . Speculation aside, lets glance over the March numbers posted on SEDAR .

While the company has a nice war chest of capital saved up of $22.6 million CDN as of last March (or $20.8 million CDN FQ2/23 per Beacon in July), the move of the helium facility to New Mexico is estimated to cost roughly $1.3 million CDN and acquiring the New Mexico property cost $3.30 CDN. This leaves us with an estimate of $16.2 million CDN in the company treasury. Liabilities come in at over $3 million but most of this is future well plugging liability that is 15 years out. Given the acquisition of many wells in New Mexico this number should go up as well.

{kind=link}

DME Financials March 2023 (SEDAR)

The next interesting tidbit is the 2024 estimation via Beacon. We can see that if things pan out the company will have a revenue steam of $22.7 million per Beacon along with a net income of $12 million CDN. Capital expenditures clearly assume plant #2 being built out.

{kind=link}

2023-24 Revenue Estimations (Beacon )

The Future is Multiple Helium Plant Construction

Assuming the pre-existing natural gas / helium play works in New Mexico, what does this revenue stream do for DME? Obviously DME will continue to rework older wells to improve efficiency in 2024-2026+ but what is the big picture? First, a working helium plant would prove to wall street & potential business partners that the helium extraction plant works.

Second it will allow DME to accelerate plans to bring plant #2 and potentially #3 online faster due to an active revenue flow. This would allow the company to construct a new facility in AZ assuming the permits are granted in time. It also opens the possibility of putting plant #3 elsewhere.

We must remember, that in various interviews, DME has said they want to purchase multiple plants at once to gain economy of scale. This makes sense. The 55% energy savings that the company claims, would make such helium production plants very appealing to various environments be they helium or hydrogen rich but this is just intent.

In the short term the company must focus on New Mexico and having that pan out. Then onward to helium plant #2 and so on. Then Desert Mountain can get to bigger dreams of signing deals with various gas companies for co-location helium deals. This will take time, patience, and hard work.

Risk

When investing in penny stocks one must assume that anything and everything can and will go wrong. The risk with Desert Mountain is extreme. No guarantee exists that the pre-existing operation in New Mexico will work out. Nor does a guarantee exist that Arizona will issue a permit for the helium project in the next 2-3 years. The reworking of wells in New Mexico may not pan out to expected flow rates. We will not have a better picture until the company has some months to get a better idea of what lurks underground.

Additionally, trucking revenue could dry up. Economic conditions may worsen as interest rates rise. This could result in an economic slowdown. The worldwide helium and neon shortage could ease up some if the war in Russia were to come to peaceful conclusion. Natural gas prices might remain low. The point is a multitude of things may go wrong to include delays. This could result in fluctuations in share price.

The overall theme is this company is risky, and you simply must do you own research. Plan for the best, expect the worst. Concerning the strong buy rating, for the long-term investor that can incur very high risk this stock could be a strong buy. Conservative investors should consult a broker or avoid this stock all together.

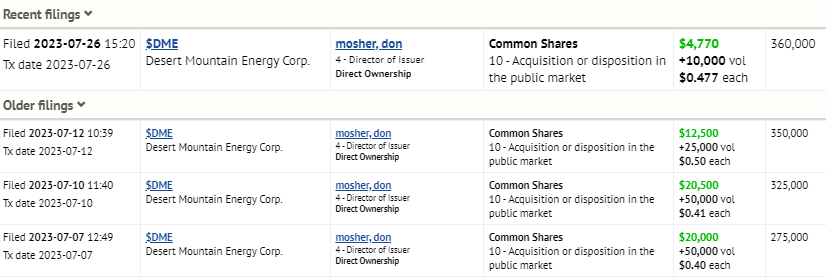

Insider Buying of Desert Mountain

Since the 90 degree turn to New Mexico, we have seen some insider purchasing on the open market. Click to enlarge.

{kind=link}

Insider Purchases Since July (Ceo.ca via SEDAR)

Conclusion

Looking at the various estimations and assuming New Mexico pans out, the company will have a revenue stream they can build upon. This might not be the solution investors in DME wanted but it is the solution we have. Improvise, adapt, overcome. To stay in Arizona waiting on regulators and enduring a burn rate is simply not logical.

If permits are approved for Arizona, the company can always build a smaller plant for that location. Given the risk levels involved and the mandatory due diligence, Desert Mountain is not a stock for everyone. This is a stock for those with patience and a near infinite risk tolerance. Yet if this plays out over the next few years, it could prove to be very profitable.

Disclosure

This is not investment advice. Please consult a license broker if you are interested in speculating in the markets.

For further details see:

Desert Mountain Energy: Value Or Value Trap?