VTRS - Despite Its Valuation Viatris Is Still A Hold

2023-06-20 05:53:32 ET

Summary

- Viatris, a healthcare company, faces weakening fundamentals and significant risks, including uncertainty regarding its execution plan.

- Despite these challenges, the company has growth opportunities, with over $3 billion in annual sales expected to mature in the next three years.

- VTRS stock is currently a Hold, as the company needs to demonstrate better execution and stabilize its declining top and bottom lines before it becomes a buy again.

Introduction

As a dividend growth investor, I seek new investment opportunities in income-producing assets, mainly stocks. I tend to add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The healthcare sector is attractive, especially when the business environment is uncertain, as we see it nowadays. While the stock market recovers, we still see economists predicting a significant slowdown and even a recession. Healthcare is relatively resilient as people tend to prioritize it. Viatris ( VTRS ) is a company I once believed was a STRONG BUY and has shifted to HOLD since then. In this article, I will revisit the company.

I will analyze Viatris using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

Viatris operates as a healthcare company worldwide. The company operates in four segments: Developed Markets, Greater China, JANZ, and Emerging Markets. It offers prescription brand drugs, generic drugs, complex generic drugs, biosimilars, and active pharmaceutical ingredients. The company offers drugs in various therapeutic areas, including noncommunicable and infectious diseases, biosimilars in the areas of oncology, immunology, endocrinology, ophthalmology, and dermatology, and APIs for antibacterial, central nervous system agents, antihistamines/antiasthmatics, cardiovascular, antivirals, antidiabetics, antifungals, and proton pump inhibitor areas, as well as support services, such as diagnostic clinics, educational seminars, and digital tools to help patients better manage their health.

Fundamentals

The revenues of Viatris have increased significantly since the merger with Mylan, and reached $17.89B at the end of 2021, the first full year of trading. Since then, the company has seen its fundamentals weaken as the revenues decreased due to slower sales in most geographies and most dominantly in the United States. In Q1 of 2023, the company missed the estimates and showed an 11% sales decline YoY. In the future, as seen on Seeking Alpha, the analyst consensus expects Viatris to keep decreasing sales at an annual rate of ~3% in the medium term.

The EPS (earnings per share) has increased since the merger when using GAAP measures. However, adjusting the EPS shows that the company's EPS, just like its sales, has decreased yearly since 2018. The increase in costs and the higher rates may pressure them even more. The margins as free cash flow margins decrease from 32% to 25% between 2021 and 2022. The decline in margins is also affecting the results in Q1 of 2023. The company reported an EPS of $0.19 compared to $0.33 a year before. In the future, as seen on Seeking Alpha, the analyst consensus expects Viatris to keep decreasing EPS at an annual rate of ~2% in the medium term.

The company is a new dividend-paying company since it didn't pay dividends when it was still Mylan. The company has one year of dividend growth in its track record. The dividend seems safe with a payout ratio of 30%, and the dividend yield is attractive at 4.66%. However, due to deteriorating fundamentals, investors shouldn't expect significant dividend increases. The company has not raised the payments for six quarters.

In addition to the $ 582M the company paid in dividends in 2022, it also spent $250M on buybacks. Buybacks are an additional way to return capital to shareholders. They are highly efficient when the valuation is low, as they lower the number of shares for less capital and support EPS growth. The company has rescued the number of shares by 0.65% since the spin-off and intends to keep executing the buybacks.

Valuation

The company's P/E (price to earnings) ratio stands at 3.5 when using the EPS estimates for 2023. The current valuation looks very attractive as a profitable company sells for a low single-digit valuation. However, the current low valuation of the company means that investors lack trust and are uncomfortable with the short track record of the company when it comes to execution. Achieving growth will allow the company to enjoy multiple expansions.

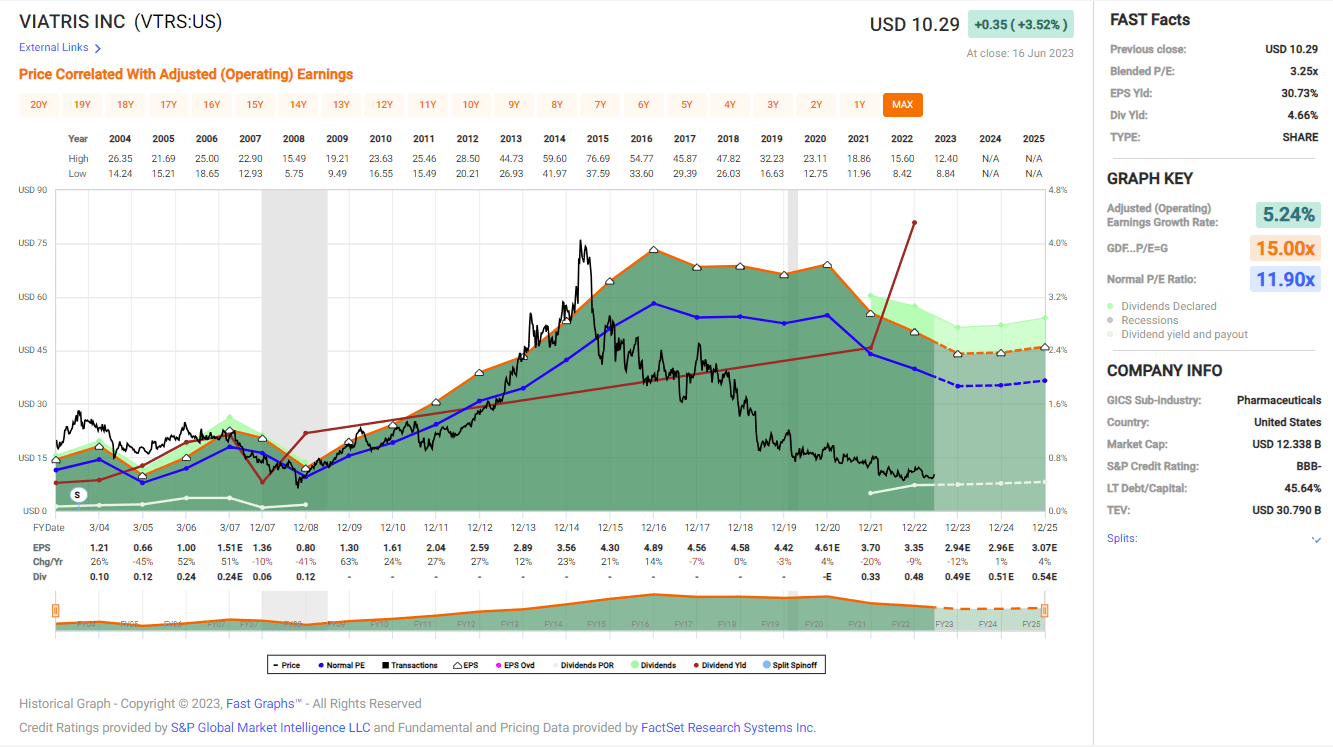

The graph below from Fast Graphs also shows how cheap the shares of Viatris are. In the last twenty years, most of them as Mylan, the company traded for 12 times earnings. Today it sells for three times its earnings. However, the challenge is the lack of EPS growth and investors' low trust in the company. The declining EPS, and the fact that we see no bottom yet, push the valuation lower. In my opinion, the shares are incredibly cheap now.

{kind=link}

Opportunities

The first opportunity for the company is its pipeline. The company achieved new product revenues of $483M in 2022. The company believes it has the potential for $2B in annual sales from its current pipeline by 2027. While this is enough to increase the revenues to their 2021 figures, it is still not the significant growth investors wish for.

The company is focusing on its newly established eye care division with the acquisition of Oyster Point & Famy Life Sciences. The division was formed in January 2023, and the company believes it can potentially add more than $1B in sales by 2028.

Eyecare is the company's foremost growth opportunity, and it has decided to turn it into a core part of its business. With the current pipeline, there is an opportunity for sales growth, and with the divestitures of less profitable products, the company can improve its margins and grow its EPS. The key here is the robust pipeline, the new division, and strong execution to build trust between the management and the investors.

Risks

The first risk for the company is the company's poor execution which has sent the estimates lower. The first two charts show that in April 2022, the estimate for 2023 EPS was $3.42, and in June 2023, the estimate for 2023 is for an EPS of $2.95. The EPS estimates are 17% lower, as the company doesn't execute as analysts expected. These two charts show lower forecasts across the board in sales and EPS. Moreover, the third chart shows that the company struggles to maintain its guidance. It missed its guidance for sales and was on the very low side of the FCF guidance. With such execution, the lack of trust by investors makes sense.

April 2022 Estimates in Seeking Alpha June 2023 Estimates in Seeking Alpha Q4 2021 Results

The reasons for the worse-than-expected execution are the competition, which makes it harder to maintain market share, and the debt burden, affecting the company's ability to raise capital to participate in M&A activity. We will now dwell on both these challenges:

First, there is the debt burden that the company is dealing with. I will note that the company has lowered its long-term debt by more than 25% with its divestitures and free cash flow. It paid more than $3B of debt in 2022 alone. However, the debt burden is still high, with almost $19B in debt and a debt-to-EBITDA ratio of 3.2 when the EPS is still shrinking. The burden limits the company's ability to acquire more companies without divestitures, and the current business environment may be an excellent time to participate in the M&A market.

Second, there is the risk of the competition that Viatris is dealing with. A third of the company's sales are coming from generic drugs, where the company is competing mainly for cost. The other two-thirds are branded drugs, where the company must constantly invest in research and development to replace them with new branded drugs. Both segments are highly competitive, and the company is competing with giants like Merck, Johnson & Johnson, and more, especially in branded drugs.

Conclusions

To conclude, Viatris is a new company following a spin-off from Pfizer ( PFE ) and a merger with Mylan. It suffers from weakening fundamentals and some significant risks, mainly regarding the uncertainty of its execution plan. On the other hand, the company has several growth opportunities, and it looks like more than $3B in annual sales in its pipeline will mature in the coming three years, replacing lower-margin sales.

The company is pricing these risks well, with a P/E ratio of 3.5. Therefore, I believe the shares are a HOLD at the moment. The price is low, but the execution has been disappointing so far. Moreover, the growth forecasts are still in the medium term in 2025, and I'd be more comfortable when they're in plain sight. Therefore, I believe shares will be a buy again when the company shows better execution and starts showing signs of top and bottom line growth.

For further details see:

Despite Its Valuation, Viatris Is Still A Hold