VZ - Deutsche Telekom: A Better Investment Than Verizon Or AT&T

2023-11-11 01:22:36 ET

Summary

- Deutsche Telekom delivered decent growth in Q3, with organic revenue growth of 0.7% and strong performance in the US and Europe.

- The company is rapidly improving margins and driving incredible free cash flow growth, leading to improved financial health and higher shareholder returns.

- Despite trading at a premium compared to its US peers, Deutsche Telekom offers a superior growth outlook and financial stability, making it a compelling investment opportunity.

- I maintain my price target of €25 per share, leaving a significant upside of 17%. I reaffirm my Strong Buy rating with Deutsche Telekom shares still looking very attractive and poised for solid returns in the medium to long term.

Introduction

Deutsche Telekom ( DTEGY ) is one of the companies I have consistently been recommending here on Seeking Alpha. Not for its incredible growth, impressive margins, or high-end technologies – the company has none of those things as a leader in the very mature telecommunications industry. Going into this article, it is good to know not to expect flashy financials. It is a boring business.

We’re not talking about the likes of Nvidia ( NVDA ), Palantir ( PLTR ), or Microsoft ( MSFT ) here, but crucially, we don’t have to in order to find “Alpha” in the market. It is very easy to entirely focus on the much-discussed and top-rated stocks in the market that present an exciting and compelling story and for which a premium needs to be paid – a premium for the promise of incredible growth. Yet, in the meantime, it is often the defensive and boring companies that can deliver market-beating returns.

No, with Deutsche Telekom, we are focusing on something completely different. While the company’s revenue is not projected to grow at incredible rates – rather low-single digits – it is still a very enticing investment opportunity today and one that has outperformed the market on many occasions over the last couple of years. Not thanks to its growth but because of the importance of its products, excellent execution, leading market positions, and defensive nature.

I last covered the company in August and upgraded shares to a strong buy, driven by a strong performance in the first half of the year and a 10% drop in the share price as an overreaction to rumors of Amazon ( AMZN ) potentially entering the sector, offering a great buying opportunity. Of course, this comes on top of an already bullish thesis. Last time out, I wrote the following:

Positioned as a global leader in the telecommunications sector, this company holds the distinction of being the largest in Europe and a prominent player on the global stage. What truly captures my enthusiasm is its extensive footprint spanning both Europe and the United States. With strategic ownership of over 50% in T-Mobile US, Inc. ( TMUS ), Deutsche Telekom has strategically established its presence across both continents. Operating across various telecommunications segments, including mobile subscriptions, fixed-network lines, and wireless networks, this industry giant showcases a robust competitive advantage. This advantage ensures revenue stability and predictability and empowers it to thrive during challenging periods.

Though, Deutsche Telekom's appeal as an investment goes beyond its stability, competitive advantage, and essential product offerings. The company's impressive EPS growth outlook is underpinned by the expectation of significant margin expansion in the years ahead. Additionally, its proactive debt reduction efforts have strengthened its financial position. Today, in my eyes, Deutsche Telekom stands out as one of the most strongly positioned telecom corporations globally, poised for substantial and enduring growth.

The shares have since outperformed the market with returns of over 10% against the SP500’s decline of 2%. In this article, I will take a look at the company’s Q3 performance and change my projections and expectations accordingly. However, I can already tell you at this point that my long-term bullish thesis laid out above has not changed. The company continues to show operational excellence, resulting in financial growth and increased shareholder returns. While this company gets far less investor attention than its American peers, Verizon ( VZ ) and AT&T ( T ), it presents a far more compelling investment opportunity today.

On that note, let’s dive into the Q3 results.

Deutsche Telekom delivered decent growth on all metrics in Q3

Deutsche Telekom released its Q3 earnings earlier this week on November 9 and showed why it deserves more investor attention. The company is firing on all cylinders on both sides of the Atlantic and seems to be untouched by everything that is happening around the world, including high inflation levels, rising interest rates, and decreasing consumer spending power.

The company reported organic revenue growth of 0.7% to €27.6 billion. This was a slowdown in growth from the year's first half and resulted in 3.3% organic growth for the first nine months. Furthermore, revenues overall in Q3 were down 4.9% YoY as a result of lower device revenues and currency headwinds. However, this has little to do with the real underlying performance, so I recommend investors focus on the organic growth levels.

Looking at the different operating regions, we can see that T-Mobile US, in which Deutsche Telekom now holds a 52.1% stake and which accounts for the company’s US operations, continues to perform strongly, easily outpacing any of its US peers.

T-Mobile added a staggering and industry-leading 850,000 postpaid phone customers in Q3. These levels of net adds reported by T-Mobile US completely blow competitors like AT&T and Verizon out of the water. For example, AT&T reported postpaid phone net adds of 468,000, not even close to the levels reported by T-Mobile. Verizon reported even less, illustrating that T-Mobile continues to win market share and outpace the competition in terms of growth, fueled by its 5G leadership, confirmed by all tests.

US segment Q3 data (Deutsche Telekom)

{kind=link}

The company also continued to see good success in high-speed Internet with almost 560,000 net adds, bringing total subscribers to 4.2 million. Churn also came in at the lowest-ever level at just 0.87%.

As a result, service revenues increased by 3.6%, driven by a postpaid service revenue growth of 6.4%. Nevertheless, T-Mobile revenues declined YoY by 8.7% due to lower equipment revenues, driven by a weakening in consumer spending. However, as explained before, this is a temporary effect and does not impact the company’s operations. T-Mobile still accounts for 64% of Deutsche Telekom's net sales.

Deutsche Telekom not only saw strong underlying growth in the US but also continues to gain share in Europe, driven by a strong expansion of its operations. The company now offers FTTH to 15.6 million European homes, up 3.4 million YoY. This, combined with strong postpaid mobile net-adds, allowed the company to add 1.4 million subscribers in Q3, driving ex-US revenue up 2.6%.

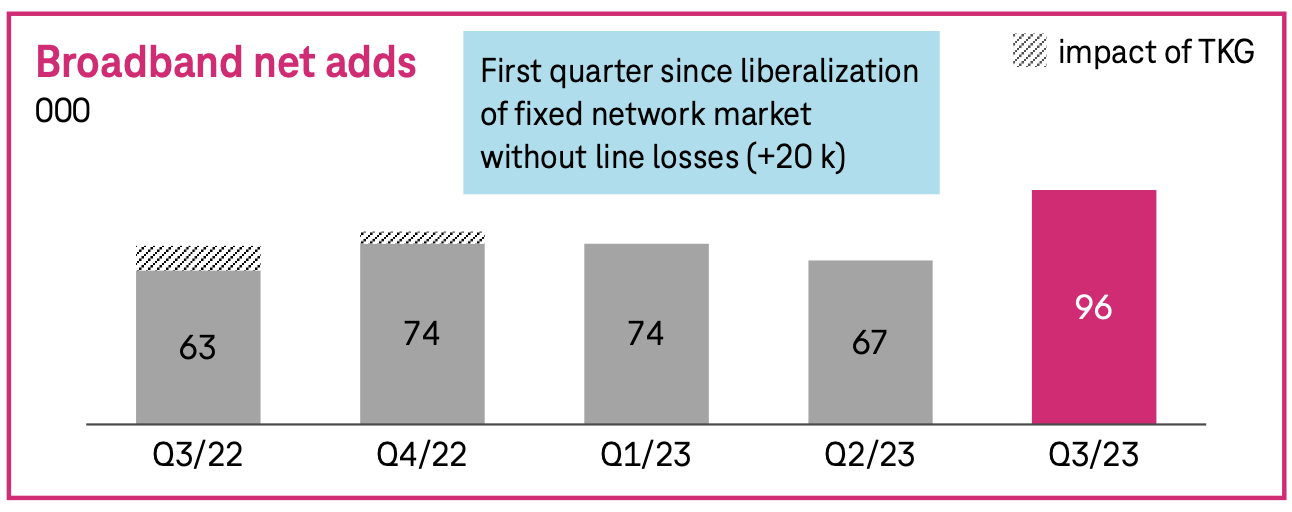

In Germany, the company’s largest European market, it reported organic revenue growth of 2.1%, driven by service growth of 2.4%. In Germany, it added a very impressive 900,000 branded postpaid phone customers and grew organic broadband subscribers by 5% or 96,000.

Germany segment Q3 data (Deutsche Telekom)

{kind=link}

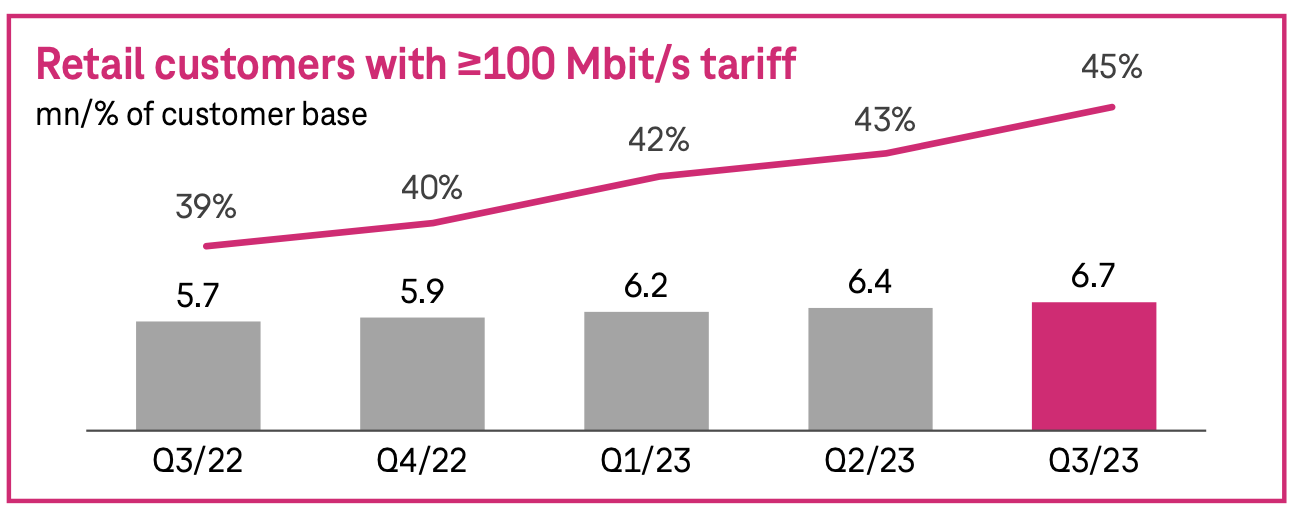

All metrics saw very strong growth trends, with TV net adds sitting at the highest level in 5 quarters and customer internet speeds still growing consistently, with 45% now using internet speeds of over 100 Mbit. This is crucial as these higher-speed contracts are worth more to Deutsche Telekom, adding more revenue without having to add customers.

Germany segment Q3 data (Deutsche Telekom)

{kind=link}

Data usage is a similar metric indicating contract value, which has also been trending upward. In Q3, data usage increased 32% YoY, indicating higher contract values. Also, churn decreased from 1% last year to 0.9% in Q3.

Finally, in the rest of Europe, Deutsche Telekom also saw strong underlying growth with strength across the board. Mobile contract net adds were 223,000, broadband net adds 76,000, and TV net adds were 52,000, far higher than we saw in previous quarters.

The company also continues outperforming its expectations with solid customer and financial growth. In Q3, organic revenue growth in Europe was 3.7% YoY.

Overall, Q3 was another very decent quarter for Deutsche Telekom, with market share gains and strong subscriber growth across the board, solidifying the company’s future revenue potential. While it faces weak hardware sales, service revenues seem unharmed by inflation and a weak consumer, as growth is visible in all metrics. Underlying this company is showing no weakness at all.

Deutsche Telekom is rapidly improving margins, driving incredible FCF growth

Moving to the bottom line, there is also plenty to be optimistic about, as the company’s cash flows are improving rapidly. The adjusted core EBITDA grew by 6.8% organically in the first nine months and 8.9% in the third quarter, which is really impressive for a company like Deutsche Telekom.

This brought the group's EBITDA to €10.5 billion in Q3. Growth was driven mostly by improving profitability in the US, which saw EBITDA grow 7.4% in Q3. Meanwhile, organic EBITDA growth in Germany was 3%, growing for the 28 th consecutive quarter. The European segment grew EBITDA by 3.3% despite significant inflationary pressures and cost inflation, including higher salaries and energy costs. This makes this performance even more remarkable.

However, EPS was down 4.2% in Q3 and down 14% for the first nine months, but this is due to a tough comparison to last year as a result of one-off benefits in 2022. Excluding one-offs, EPS was up YoY.

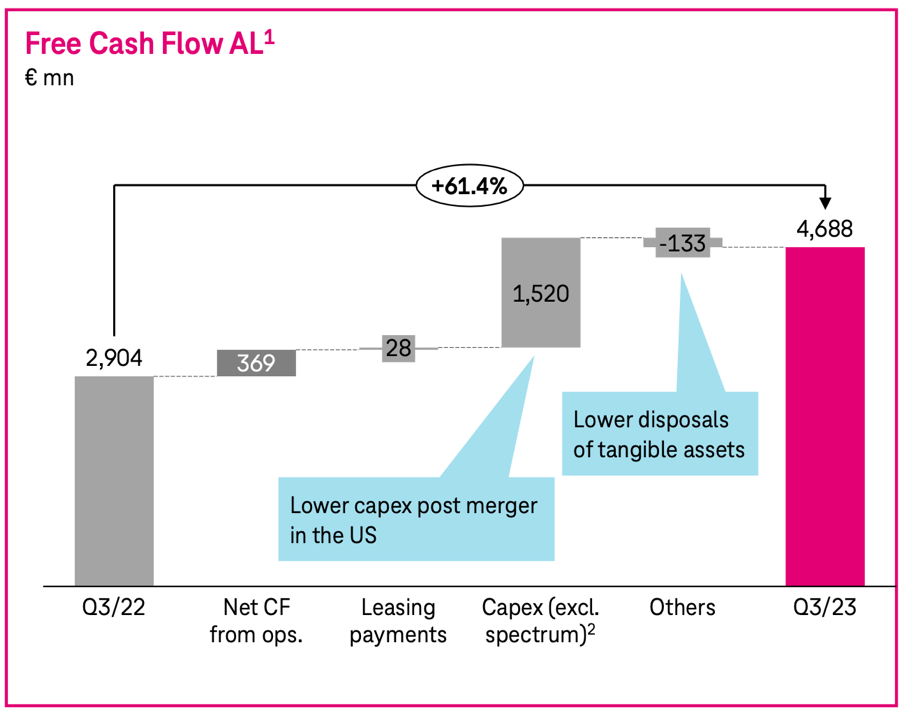

Furthermore, FCF grew 60% YoY in Q3, driven by lower Capex for T-Mobile related to the sprint integration. Capex is expected to keep decreasing over the next few years, driving significant FCF growth.

YoY FCF growth (Deutsche Telekom)

{kind=link}

This staggering improvement in FCF has helped Deutsche Telekom meaningfully improve its financial position, lowering the debt position by 11.5% over the last 12 months from €109.5 billion to €97 billion, of which 75% is on account of T-Mobile. With FCF expected to grow rapidly, we can safely assume the company will keep deleveraging the balance sheet. Net debt leverage today still stands at 2.4x. While its debt position is still significant, it is far better than that of its US peers, with AT&T and Verizon holding net debt positions of $128.7 billion and $154.4 billion, respectively. At the same time, Deutsche Telekom also has a far, far better FCF growth outlook. The difference in financial health is, therefore, significant.

In addition to improving financial health, the growing FCF also supports significantly higher shareholder returns in the form of a growing dividend and a repurchase program of up to €2 billion to start in 2024.

Deutsche Telekom plans to increase the dividend by 10% to €0.70 per share, bringing the yield to approximately 3.3% and the payout ratio to a very conservative 41% based on FY23 EPS. With EPS projected to grow in the double digits in the medium term, I expect Deutsche Telekom to keep growing the dividend at a similar rate, offering decent dividend growth to investors combined with a solid yield.

However, despite this improved shareholder returns outlook, this is also the one point where Deutsche Telekom loses to its peers who pay a dividend of over 7% on seemingly sustainable payout ratios.

Outlook & Valuation – Is Deutsche Telekom a Buy, Sell, or Hold?

Back in September, T-Mobile US already upgraded its outlook following a strong first nine months of the year. Earlier this week, Deutsche Telekom passed on this guidance increase and also raised the FY23 outlook for the third time this year.

Deutsche Telekom has raised both its EBITDA and FCF guidance by €0.1 billion, bringing the expected FY23 EBITDA to €41.1 billion and FY23 FCF to €16.1 billion. Meanwhile, the ex-US business performance expectation remains unchanged, and the company continues to expect over €1.60 in EPS for the full year. We can safely assume that these expectations are still conservative, and the company will deliver another outperformance when it reports FY23 results early next year.

Following a strong Q3 with impressive underlying growth and an upgraded FY24 outlook, I now expect the following financial results through FY26. Despite the strong performance, I have had to lower my revenue and EPS projection for this year, mostly due to the impact of FX headwinds.

Financial projections (By author)

{kind=link}

Based on these updated projections, shares are now trading at a forward earnings multiple of 12.75x. This means shares are trading at quite a premium over its US peers but a discount to its most important European peer, Vodafone ( VODAF ). However, this premium over its US peers is fully justified, even as these offer a superior dividend yield.

valuation comparison (Seeking Alpha)

{kind=link}

For one, Deutsche Telekom is in better financial health, as discussed before, as it is rapidly lowering its debt and is far better diversified with strong market positions in both the US and Europe. The company has been rapidly gaining wireless and wired internet subscribers, easily outpacing the net adds reported by Verizon and AT&T.

As a result, Deutsche Telekom also has a far superior growth outlook. Looking at the current Wall Street consensus, AT&T is projected to grow revenue at a CAGR of only slightly over 1% over the next four years. Verizon is similar, with a CAGR projected between 1.5% and 2%. Meanwhile, Deutsche Telekom is expected (by both Wall Street analysts and me) to grow revenue at 2x the CAGR of its peers at 3% to 4%.

Looking at EPS growth, the difference is night and day, with investors being lucky if Verizon grows its EPS at a CAGR of above 1% and AT&T not looking much better at approximately 2%. Meanwhile, Deutsche Telekom is poised to grow EPS and FCF at a mighty CAGR of over 10%, far better than any of its peers. Also, remember these companies have a similar market cap.

So, yes, investors looking for a high yield will most likely be better off with either Verizon or AT&T. Still, those looking for a company in the same defensive industry (making it exceptionally resistant to inflation and economic downturns, offering stability), with improving financial health, a solid and growing dividend, and much faster revenue and earnings growth should focus on Deutsche Telekom, which still has some room for multiple expansion as growth expectations are realized.

At the same time, yes, Verizon and AT&T are trading at a far lower multiple of 7.5x and 6.5x, respectively, but I would absolutely not be willing to pay much more for a company growing its top and bottom line at a CAGR of 1-2%. Even if their multiples would expand to 8x and 7x, this would still give investors no more than a total return of 10-11% annually for either of the two through 2026.

Don’t be seduced by a high yield. Looking at the total return potential for Deutsche Telekom based on a fair multiple of 13x, I calculate total returns exceeding 12% annually, with much more financial stability, room for upside, dividend growth, and better long-term financial growth. This makes Deutsche Telekom a superior investment to its much-discussed American peers today.

Finally, based on a 13x multiple and my FY24 EPS, I maintain my price target of €25 per share, leaving a significant upside of 17%. I reaffirm my Strong Buy rating with Deutsche Telekom shares still looking very attractive and poised for solid returns in the medium to long term.

For further details see:

Deutsche Telekom: A Better Investment Than Verizon Or AT&T