VZ - Deutsche Telekom AG: Investors Should Likely See Solid Returns

Summary

- Deutsche Telekom (DT) delivered an impressive outperformance during 2022, both in share price performance and financial results.

- The latest quarter saw DT outperform its own outlook again, driven by strength across all its regions.

- I remain very bullish on DT as the best positioned telecommunications giant in a very mature industry. Its 49.6% ownership of T-Mobile US gives it solid exposure to the US.

- The strong positioning and pricing power make this company a very resilient as well as consistent performer.

- Based on very strong free cash flow, dividend, and EPS growth expectations, I believe the stock can return over 10% per year to investors through share price performance and dividends.

Introduction

Deutsche Telekom (DTEGY) has been one of my highest conviction stock picks of the last year due to the necessity of the products and services it offers. The company is one of the largest telecommunications companies on the planet and the largest in Europe. While it has a lot of exposure to several countries in Europe, what gets me most enthusiastic about this telecom giant specifically is the exposure to both Europe and the US. Deutsche Telekom owns close to 50% of T-Mobile US, positioning them well across both continents. The company operates in all segments of telecommunications involving mobile subscriptions, fixed-network lines, and wireless networks.

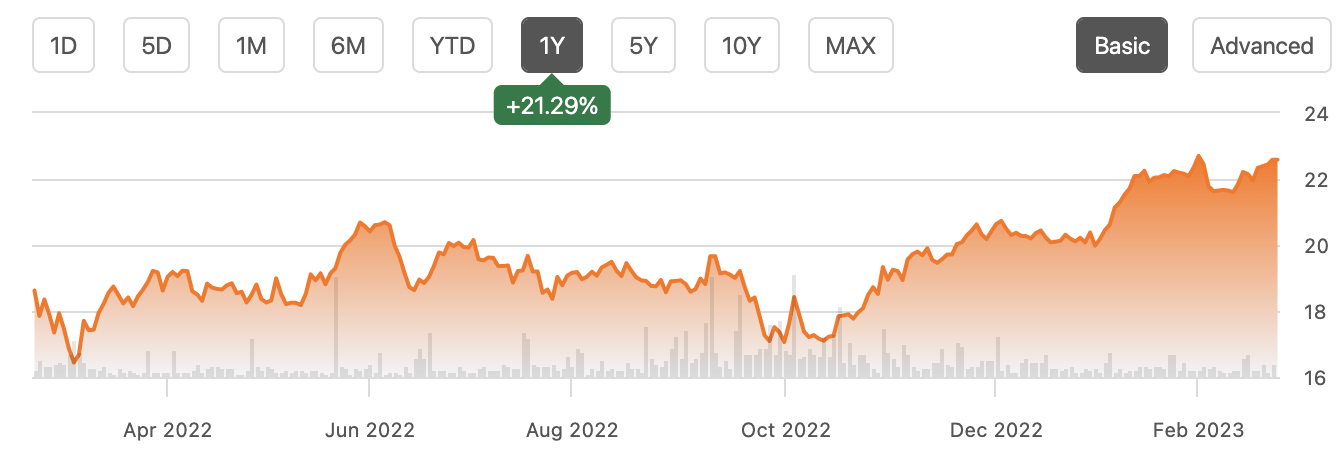

That the company, indeed, has an incredibly strong position was highlighted during the last year which was heavily impacted by a weakening economy, high inflation, and a war in Ukraine. Yet, despite all these issues, Deutsche Telekom did see much impact and managed to continue on its growth trajectory without any signs of serious weakness. Inflation was easily offset and the necessity for its products caused it to feel very little influence of the weakening economy. As a result, it managed to easily outperform the major indices with the stock up over 21% over the last year, compared to a 5% drop for the SP500. Surprisingly, despite a solid share price performance over 2022, it is not underperforming in the bull market of 2023 either with the share price up 12% so far, also outperforming most indices.

DTEGY share price performance (Seeking Alpha)

{kind=link}

And it is not just its resiliency, lower volatility, and consistency that make the stock an attractive pick. The growth outlook is also very decent in my eyes compared to many of its mature telecom peers. Due to its exposure to the fast-growing T-Mobile US ( TMUS ) and strong positioning in Europe, the growth outlook is very decent and should easily outpace European peers like Orange ( ORAN ) or Vodafone (VODPF), and American peers AT&T ( T ) and Verizon ( VZ ).

I wrote my initial coverage on the company back in October and revisit my thesis after the third quarter results in November. The stock is up 33% and 17% after the release of these articles, respectively. This is what I concluded back in November, roughly in line with what I have just described above:

Deutsche Telekom is a slow-growing giant, with few long-term risks. Within the current economic climate and the risks of a recession getting bigger, it is no bad choice to invest in solid companies with strong cash flows. The need for internet services will only increase, and people and businesses will remain to be dependent on internet services. Deutsche Telekom is perfectly placed to benefit. The almost 50% stake in T-Mobile US will remain to be a growth driver as the fastest-growing provider in the US.

On February 24, 2023, Deutsche Telekom released its fourth quarter and FY22 results and managed to put down another impressive performance. The company outperformed its own outlook, even after increasing it three times during the year already, and managed to surprise analysts once more with its strength. Following these results, in this article, I will revisit my thesis by analyzing the latest earnings report, quarterly trends and happenings, balance sheet, valuation, and outlook.

So, without further ado, let’s get to it!

Quarterly review

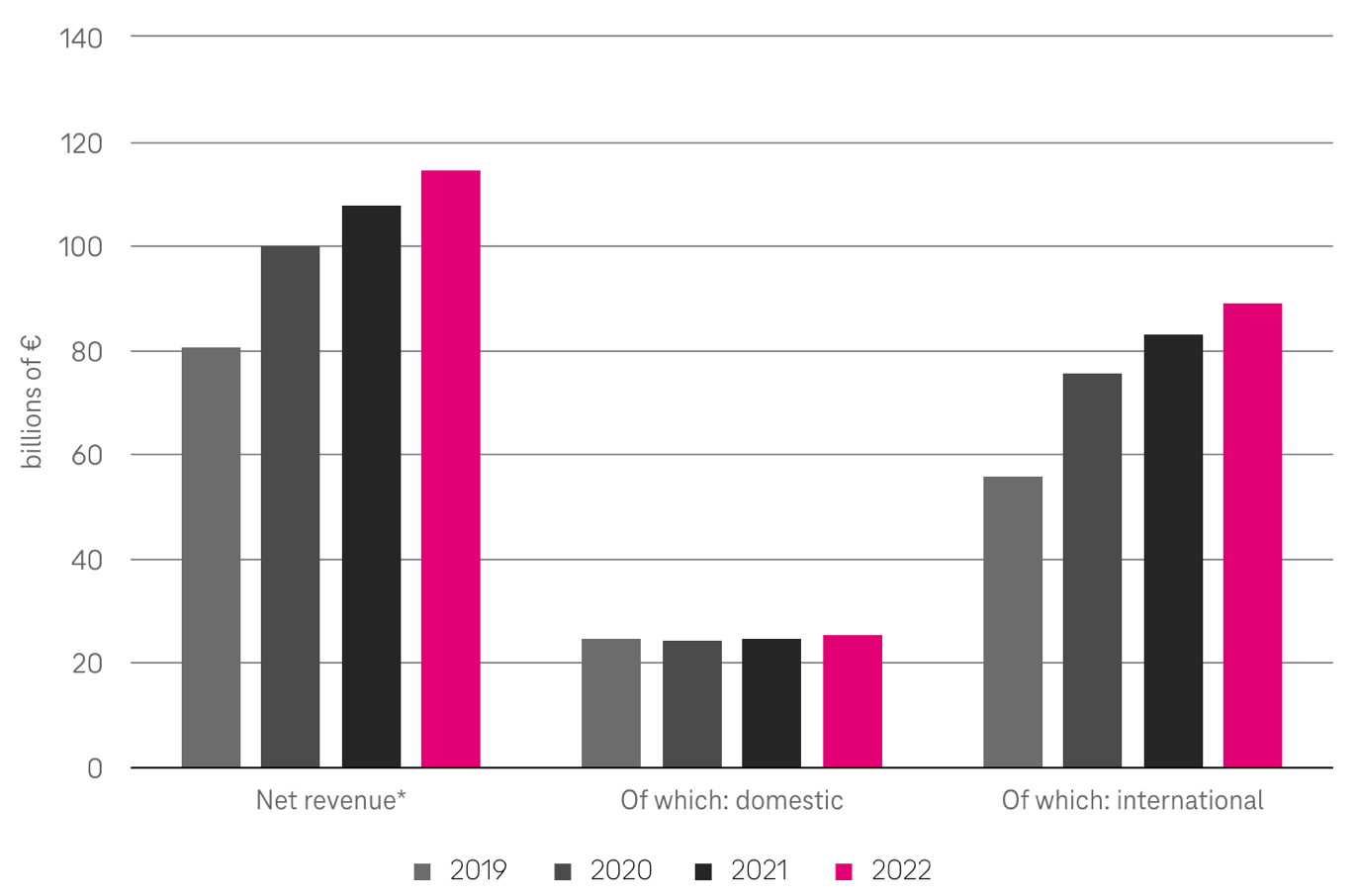

Deutsche Telekom reported revenue of €29.8 billion for 4Q22, bringing the FY22 total to €114.4 billion. This represents growth of 4% and 6.1%, respectively, and shows very decent top-line growth during a very challenging year. In fact, as shown below, Deutsche Telekom has shown very decent and consistent revenue growth over the last 4 years, driven primarily by international revenue growth. Organic service revenue growth came in at 3.7% which is still very decent, but overall group organic revenue growth was flat YoY. DT is witnessing somewhat slower growth in Europe with organic service revenue growth from this region of just 1.8% and much faster growth coming from the US.

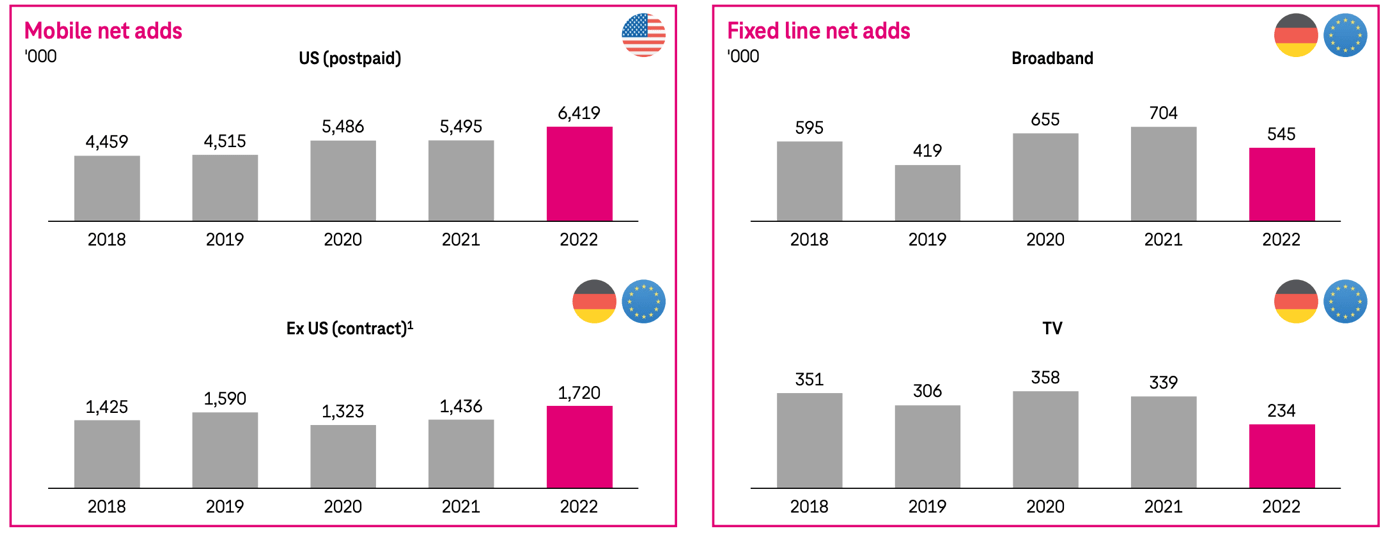

Now, driving strong US growth numbers is of course primarily net customer additions and 4Q22 delivered strong commercial numbers. Mobile net adds came in at 930,000 with the lowest churn quarter ever. Postpaid accounts increased by 314,000 and brought the FY22 total to 1.4 million net additions. High-speed internet customers increased by over 500,000 during the quarter and 2 million for FY22. Most of these customer addition metrics are industry-leading as T-Mobile US continues to take away market share from competitors.

Deutsche Telekom revenue growth (Deutsche Telekom)

{kind=link}

As for the other regions/segments, Germany saw a growth of 1.7%, whereas mobile services revenue grew by a faster 3.5% YoY. Management did admit that the higher mobile services revenue did see a non-recurring tailwind of about 1%. Still, growth is at the upper end of the target range of 1% to 2% and so came in higher than anticipated. At the same time, EBITDA for the German segment grew by 3% YoY. This growth was driven by solid broadband net adds of 74,000 and tv net adds of 51,000, both the highest of 2022. Also, people are increasingly choosing the higher-speed home contract driving up revenue per customer. This resulted in broadband revenue growth of 5%, in line with the previous 5 quarters. DT is still increasing its coverage of broadband connections in Germany and is confident that it can offer broadband to 10 million households by FY24, increasing the broadband potential for Deutsche Telekom in revenue through expansion and upsell opportunities.

Mobile net adds for the German segment were also strong at a total of 225,000.

{kind=link}

In the European business segment, DT also saw another consistent and strong performance with organic revenue growth of 2.2%. Yet, realistic revenue growth was just 0.3% and EBITDA fell by 0.6% YoY. The European segment is clearly fighting off some headwinds like a new Hungarian revenue tax, higher energy costs, and spinoffs. According to management, EBITDA growth would have come in at a more solid 3.5% YoY without these “artificial headwinds”. More positive about this segment were the customer net additions which remained very constant YoY and in line with the previous 5 quarters.

For the entire business, EBITDA for 4Q22 was €10 billion and grew by an impressive 10.6% YoY. For FY22 EBITDA has grown by 7.7% and came in at €40.2 billion, of which €14.6 billion was generated outside of the US. To put these numbers and performance into perspective, DT at the start of the year guided for an EBITDA of €36.5 billion, which means that DT managed to outperform its own start-of-the-year EBITDA guidance by over 10%.

{kind=link}

Both revenue and EBITDA growth were driven by growth from all regions and segments of DT, illustrating the broad strength of the firm. The German part of the business has now recorded 25 consecutive quarters of growth, while Europe is standing at 20. This, again, shows the consistency of both top and bottom-line growth.

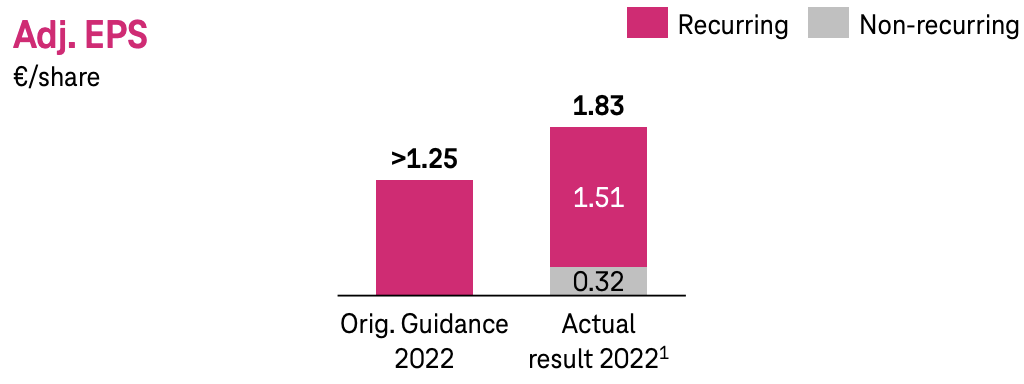

These strong overall numbers resulted in a very impressive bottom line for DT as net income for FY22 was €8 billion and grew by a staggering 91.6% YoY, and resulted in EPS of €1.83, growing 50% YoY. In fact, EPS stood at a record high during FY22. On top of this, the EPS reported by DT for FY22 was almost 50% higher than guided for at the start of the year. Yet, I will need to add to this that the outperformance was in part driven by non-recurring items like M&A and interest rate volatility, but even without the effect of these items, the outperformance came in at 21% which is still impressive.

Free cash flow for FY22 came in at €11.5 billion after generating €2 billion in free cash flow during 4Q22. These represent 16.9% and 14.8% YoY growth, respectively.

Deutsche Telekom EPS (Deutsche Telekom)

{kind=link}

Capital Markets Day

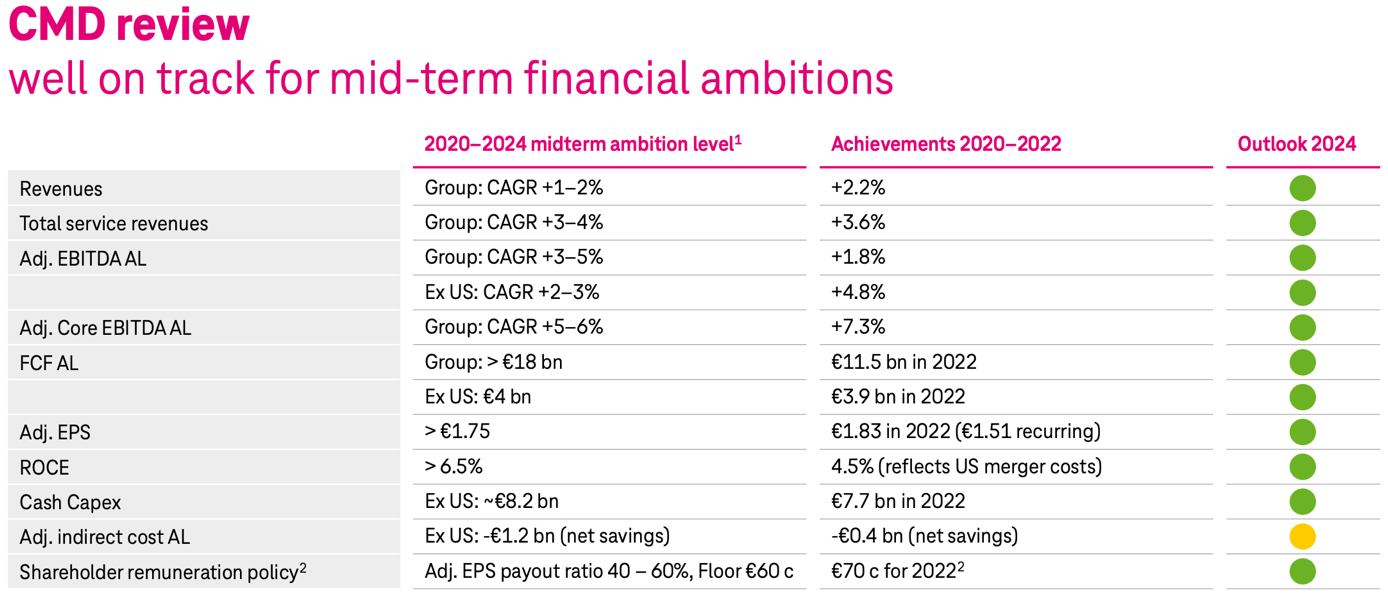

Important to investors, Deutsche Telekom holds its capital market day (CMD) every four years in which it discusses its targets for the following four years. With the last one being in 2021, we are now halfway past the four-year period. Therefore, management took some time during the earnings call to also reflect on the last 2 years and the progress of the targets.

The foundation of these growth plans is network leadership and DT looks to be doing very well on this front proven by the numbers given during the earnings call:

We now passed 13.5 million homes passed in FTTH, up 3 million year-on-year. We passed 5.4 million in German homes with FTTH already. Our ultra-capacity 5G network reaches 265 U.S. POPs, way ahead of our competition. And we will reach 300 million POPs by the end of this year. In Germany, we now cover 95% of the population with 5G. In the European segment, we stand at 47%, up 6 percentage point in the quarter.

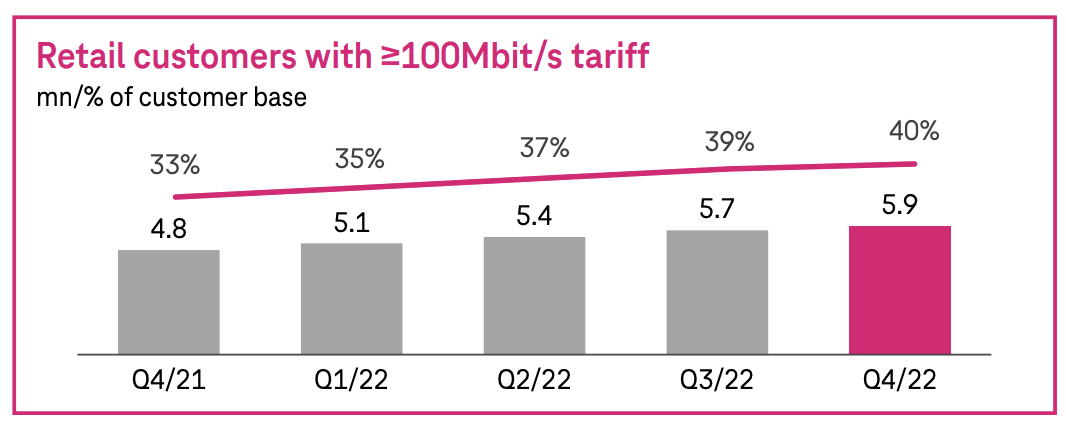

As I already mentioned, DT delivers the full stack of solutions in both the US and Europe, and through this expands its presence. Product and network dominance play a crucial role in this, and DT seems to have this under control. The quality of the network is then reflected in customer net additions as well as through its 5G dominance and a great offering of home internet solutions. The company has seen the highest mobile customer net addition numbers in 5 years during 2022, despite all headwinds. Yet, fixed line net adds are slightly underperforming from a historic perspective, but this in part is due to people returning to their workplace and demand for broadband and TV falling slightly as a result.

Customer additions performance (Deutsche Telekom)

{kind=link}

One of the capital market targets besides growth is cost reduction and this has been disappointing so far, according to CEO Tim Höttges. This is primarily due to some economic trends like inflation working against them. DT has lowered its ex-US workforce by 3% over the last 2 years to lower costs, but high inflation and extreme energy prices in Europe have been pushing this in the wrong trajectory. And whereas this is not great, this does mean we should expect to see solid cost savings kick in once energy prices drop further and inflation eases. This should then drive up the bottom line and cause an EPS outperformance. Good news for shareholders.

Overall, growth trends for DT are well in line with or above expectations and both the US and European segments have been reporting excellent and, above all, consistent growth. And there is absolutely no reason to expect anything else for the next couple of years as economic trends start working in favor of DT. With a 2.2% CAGR in growth over the last 2 years, it is above its 1% to 2% target and looks like it should be able to continue this track record over the next 2 years. We are seeing similar trends for EBITDA and EPS as well.

{kind=link}

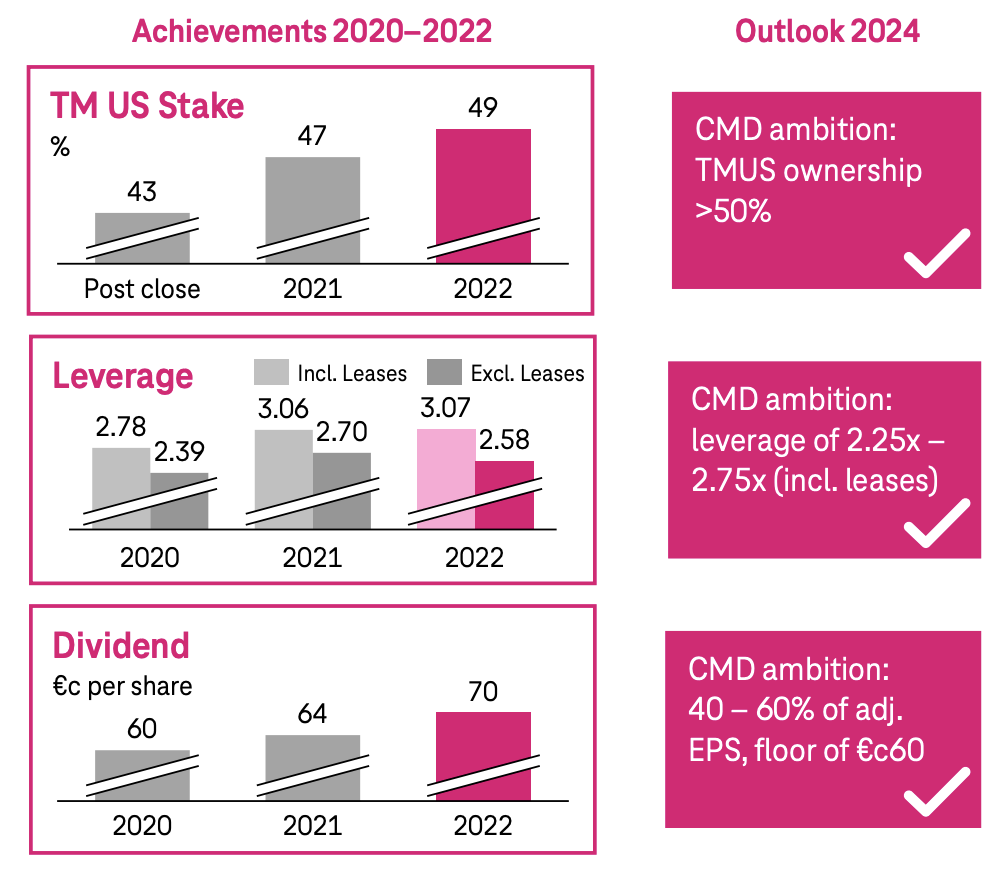

Yet, to achieve solid growth for the next couple of years, good capital allocation is crucial. DT put a couple of important goals down for itself back in 2021 and these were increasing ownership in T-Mobile US to over 50%, lower the debt leverage to 2.25, and returning solid amounts of cash to shareholders through dividend increases.

By the end of 2022, DT owned approximately 49.6% of T-Mobile US and is well underway to achieving the 2024 target of 50%. To be able to afford these heavy investments, DT has sold 75% of T-Mobile Netherlands for €3.8 billion, of which it has reinvested €2.2 billion into T-Mobile US. It also sold 51% of GD Towers for a total of €10.7 billion to be able to lower both its debt and increase its stake in T-Mobile US.

Where many companies have been buying back their own shares over the last several years, DT management chose to not do this, but use this cash to increase its stake in T-Mobile US to drive future growth and benefit from T-Mobile buying back shares itself, indirectly also benefitting DT and its shareholders. The company has already bought back $3 billion in shares and has another $11 billion under its current program. In addition to this, DT has also solidly increased the dividend for the last 2 years now and is on course for its 2024 targets as shown below.

CMD capital allocation targets (Deutsche Telekom)

{kind=link}

Balance sheet & Dividend

One important thing to keep an eye on with most telecom companies is debt. With the telecommunications industry being an investment-heavy industry, most telecom giants have large debt piles, despite decent free cash flow for most. The large debt piles are also caused by many acquisitions by these giants, in addition to high dividends and share repurchases to boost investor returns in this very mature industry.

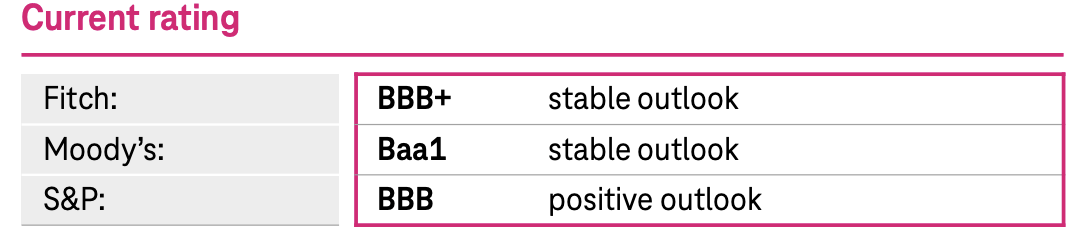

DT is no exception here. Net debt at the end of FY22 stood at a massive €103 billion but was impacted by the sprint acquisition. Still, DT has brought down its leverage ratio to a more acceptable 2.58x, down from 2.7x last year. As will be discussed in the outlook, DT expects to increase its free cash flow generation over the next couple of years, in addition to the Sprint merger now finalized. This should cause DT to be able to lower its leverage ratio over the next 2 years as part of its 4-year goals. I am very glad that bringing down the debt burden and ratio is a primary focus for management as I always prefer companies with a healthier balance sheet. With the focus on the balance sheet from management, I am willing to cut DT some slack for now. The company also continues to receive solid credit ratings as shown below.

Credit rating Deutsche Telekom (Deutsche Telekom)

{kind=link}

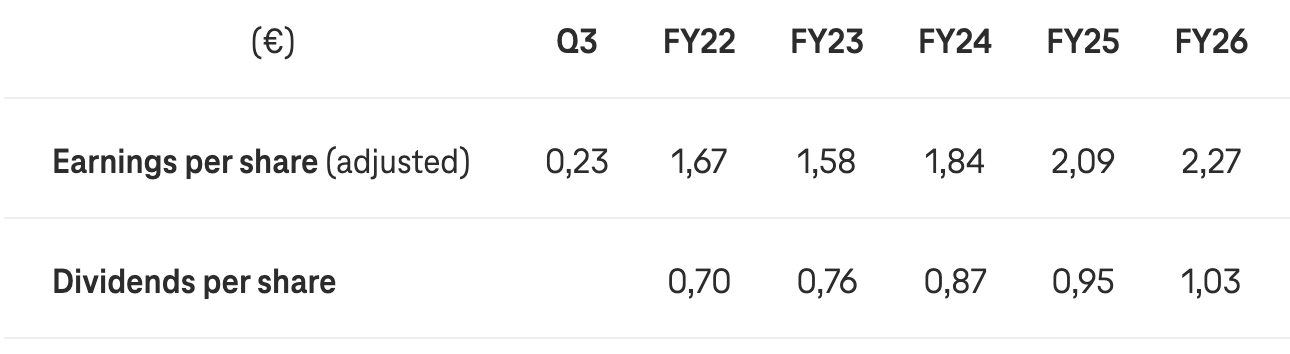

The company also offers a solid dividend yield as discussed before. The forward yield now stands at 3.32% based on a €0.70 payout. While this is a really solid yield, dividend growth has not been great over the last decade, while it has been upgrading at a solid pace over the last 2 years as part of its 4-year plan. DT is committed to paying 40% to 60% of its EPS to shareholders in the form of dividends and based on the analysts' EPS consensus, this results in the following dividend expectations, shown below. These expectations reflect a dividend growth CAGR of around 10%. Also, the dividend looks well covered and therefore safe for the following years. With the expectation of increased free cash flow over the coming years, this is increasingly the case. Of course, the dividend yield is not as strong as peers like Vodafone, Verizon, or AT&T, but I believe the better growth outlook also positions shareholders well for better dividend increases and share price growth. I view the dividend as solid, safe, and with plenty of growth potential.

Dividend and EPS outlook (Deutsche Telekom)

{kind=link}

Outlook & Valuation

For FY23, DT management has guided for a minor increase in revenue, coming from all segments but with increased growth in Europe. For guidance, management takes the midpoint of guidance by T-Mobile US to arrive at a conservative scenario. This results in an expected EBITDA of around €40.8 billion of which €13.9 billion will be coming from the US. DT expects to see 3% EBITDA growth for the German segment, a little over 5% for the US, and Europe to remain flat YoY. Capex should come in much lower compared to 2022 at just €16.8 billion due to a significant Capex decrease for the US segment. As a result, free cash flow is expected to come in much higher at above €16 billion compared to €11 billion in FY22. This should also result in EPS of €1.60 which is above FY22 EPS excluding the one of benefits.

I believe guidance from management is already very decent and considering the fact that management tends to guide way too conservatively, I expect to see the performance come in quite a bit higher. But how does this reflect in the current analyst guidance?

Analysts guide revenue of close to €116 billion, representing around 1% revenue growth. EBITDA growth is projected to come in at 4% and as I already mentioned, EPS is expected to come in a bit lower (5.3%) but this includes the one of benefits from the latest quarter. Excluding the one of benefits, EPS is projected to grow by 4.6% YoY.

I believe guidance by analysts is also too conservative and looks poised for upwards revisions after the first 6 months of the year. I expect DT to grow revenue by 2% this year and to see revenue of closer to €116 billion combined with EBITDA of at least above €41 billion. This should result in EPS growth of close to 6% or come in at €1.60. And even these estimates still feel conservative to me.

If we look at the period until 2026, analysts expect DT to grow revenue at a CAGR of 2.35% and EBITDA to grow at a faster 4.74%. Free cash flow is projected to grow at a CAGR of close to 20% and analysts project the net debt to decrease to just €82 billion by 2026 which should result in much better leverage. Finally, EPS is expected to see a growth CAGR of 8%. Combine this EPS growth with a solid dividend of above 3% and investors should be well-positioned to see solid returns of above 10% a year. In addition to this, I would not be surprised to see DT outperform the current 4-year consensus and see even better returns.

And this then brings me to the valuation, because just as a couple of months ago, the stock is still way too cheap, despite the share price increase. Based on its current share price of €21.19 on the German stock exchange, the company is valued at a forward P/E of 13x based on my estimates. Considering this company should be able to return over 10% per year based on current EPS estimates and dividends, I believe a P/E of 15 is warranted for a company this strong and resilient. This would result in a 12-month price target of €24 which should give investors an upside of 13% from its current share price. For DTEGY or DTEGF, this would result in a price target of approximately $25.

For comparison, 2 Wall Street analysts currently maintain a buy rating with a price target of $24.57, according to Seeking Alpha .

Conclusion

Deutsche Telekom AG continues to show a very impressive performance with it easily outperforming its own (conservative) guidance time after time again. I believe this telecommunications giant is best positioned compared to peers due to its solid business model, exposure to both Europe and the US, good management, and strong capital allocation. With the current EPS guidance from analysts until 2026, investors should see returns of at least 10% per year.

The company has shown impressive resiliency over the past year and has proven why it should be viewed as a cornerstone of your portfolio. The low volatility, inflation resistance, and consistency make this an excellent pick for any portfolio without many, if any, serious long-term risks. Part of this is due to its impressive pricing power, allowing it to offset most headwinds. The de-risking of the balance sheet should be an additional driver of investor attractiveness, driving up the valuation. Also, analysts project DT to have seen a peek Capex in 2022, in part due to the Sprint acquisition, and expect Capex to remain below €17 billion until 2026, compared to over €20 billion for FY22. This should be a solid driver of margins and EPS growth.

Based on my assumptions for FY23, I calculated a target price of €24 (or $25), leaving investors with a very decent upside potential of above 13% for the next 12 months, making this company an excellent buy at its current share price. I, therefore, maintain my rating and rate Deutsche Telekom AG a strong buy.

For further details see:

Deutsche Telekom AG: Investors Should Likely See Solid Returns