CA - Dexterra Group: Why Buy Into The Revenue Growth

2023-07-18 08:23:24 ET

Summary

- Dexterra Group will likely achieve its $1 billion revenue and $100 million EBITDA target.

- We discuss the $2 billion revenue goal.

- The dividend, stock buybacks, and margin expansion are assessed.

Dexterra Group (HZNOF) is a Canadian-based company that provides services for facilities. It has five brands that are driving its 2023 business plan. Since posting quarterly results in May, shares are trading at the upper end of its trading range and near a 52-week-high. Markets bid shares higher after the company posted revenue and adjusted EBITDA growth.

Revenue Growth in Q1/2023

In the first quarter, Dexterra posted an increase in revenue. Acquisitions in 2022 are the primary driver of higher revenue. In addition, the firm benefited from contract wins.

{kind=link}

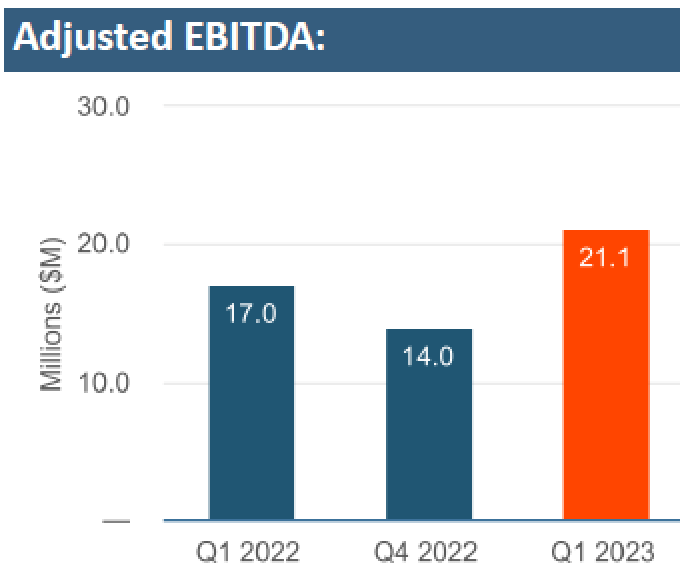

Profitability increased when the company demonstrated it could make accretive acquisitions. It rationalized its contracts, improved execution, and managed inflationary costs. As a result, adjusted EBITDA increased Y/Y:

{kind=link}

Dexterra also benefited from favorable comparisons. In the Dana food service unit, Covid restrictions hurt results in the previous period. Customers resumed their business-as-usual patterns, with educational contracts rebounding to normal capacity levels.

The company said that it expects its acquisitions will add around $130 million in revenue this year. With effective inflation management, shareholders may forecast margins rising above the 6.4% reported in Q1.

Addressable Market Expansion

Dexterra Group's acquisition of VCI Controls will expand the total addressable market. It adds to the firm's building and automation control capabilities. Clients are focusing more on ESG initiatives. Expect demand for energy efficiency solutions and the need to reduce carbon footprint to boost Dexterra's revenue.

In the latter half of the year, sales momentum in the Integrated Facility Management segment will accelerate. The company won several new contracts recently in the educational sector. While margins will expand naturally, Dexterra will increase profitability by exploring acquisition targets in late 2023 or in 2024.

In the energy services sector, the contract fulfillment with LNG will increase occupancy levels for Crossroads Lodge .

Due to the demand for wildfire support in Alberta, Dexterra will have tailwinds from higher forestry activity, including tree planting. In the Workforce Accommodations, Forestry, and Energy Services ("WAFES") segment, revenue increased by 13% to $129.6 million . The unit will need demand from the mining and energy sector to sustain that revenue growth. Dexterra said that it has new sales opportunities for mining projects in Ontario and Quebec. This will offset the scheduled completion of projects like Coastal GasLink, set for this year.

Opportunities

Dexterra is a worthwhile speculative dividend income position. It is targeting a conversion of EBITDA to free cash flow of 50% in 2023. It expects this FCF will easily cover its dividend payments, which costs $22 million annually. At a 26-cent a-share dividend, the stock yields 6.17% based on a $4.20 closing price.

The company has a stock buyback authorization of up to 1.3 million shares. This helps support the share price. It decreases the chance of an unforeseen stock dip. Management believes the stock trades at a large discount to its real value. Using its FCF to reduce the stock count will benefit shareholders.

Dexterra has a lofty, near-term revenue goal of $1 billion and $100 million in EBITDA. After posting $268.1 million in quarterly revenue, it is not far from the former goal. In addition, the EBITDA target is easily achievable. From there, organic growth and acquisitions could drive the business toward a $2 billion revenue target.

Dexterra is counting on the VCI acquisition to account for its market growth. Markets are closely watching management's ability to build its capability around VCI. In the next quarterly report, watch out for the company reporting that operating margins expanded. It will need to raise its profit forecast for the year to win investor confidence.

Dexterra will also update its shareholders on the pipeline growth. The business is still rebounding from the end of Covid restrictions. It needs to post a strong win rate for new contracts. This would demonstrate that management has the capability to grow profits amid a competitive environment.

Risks

Dexterra's debt increased from $94.0 million in Q4/2022 to $110.6 million. This rose due to the higher working capital investment needs from business expansion and the payment for the VCI acquisition. The firm ended the quarter with $78.1 million available from its credit facility.

Your Takeaway

Dexterra is on the cusp of breaking out. Investors are waiting for the company to announce contracts that will add meaningfully to its revenue growth. The firm took provisions in prior quarters to cover additional project costs. Those efforts should pay off in future quarters. As the company signs new contracts, investors will want to see profit margins expand.

For further details see:

Dexterra Group: Why Buy Into The Revenue Growth