NVDA - Digital Realty: A Rising 'AI' Tide Lifts All Ships

2023-06-13 07:00:00 ET

Summary

- At iREIT™ we recognize that the rapid growth of data generation fueled by AI has transformed how data is stored, processed, managed, and transferred.

- Within the REIT sector, we see strong potential with the increasing demand for computing power across data centers.

- I’m piling back into Digital Realty Trust stock, recognizing that there’s a tremendous opportunity to capitalize on what I consider to be one of the best business models on the planet.

This article was published at iREIT™ on Alpha on Sunday June 11, 2023.

In a recent Seeking Alpha article , I explained that,

“...the artificial intelligence ("A.I.") craze that took over markets last week was crazy to see…and essentially represented a microcosm of what’s been going on with the broader markets throughout 2023 thus far.

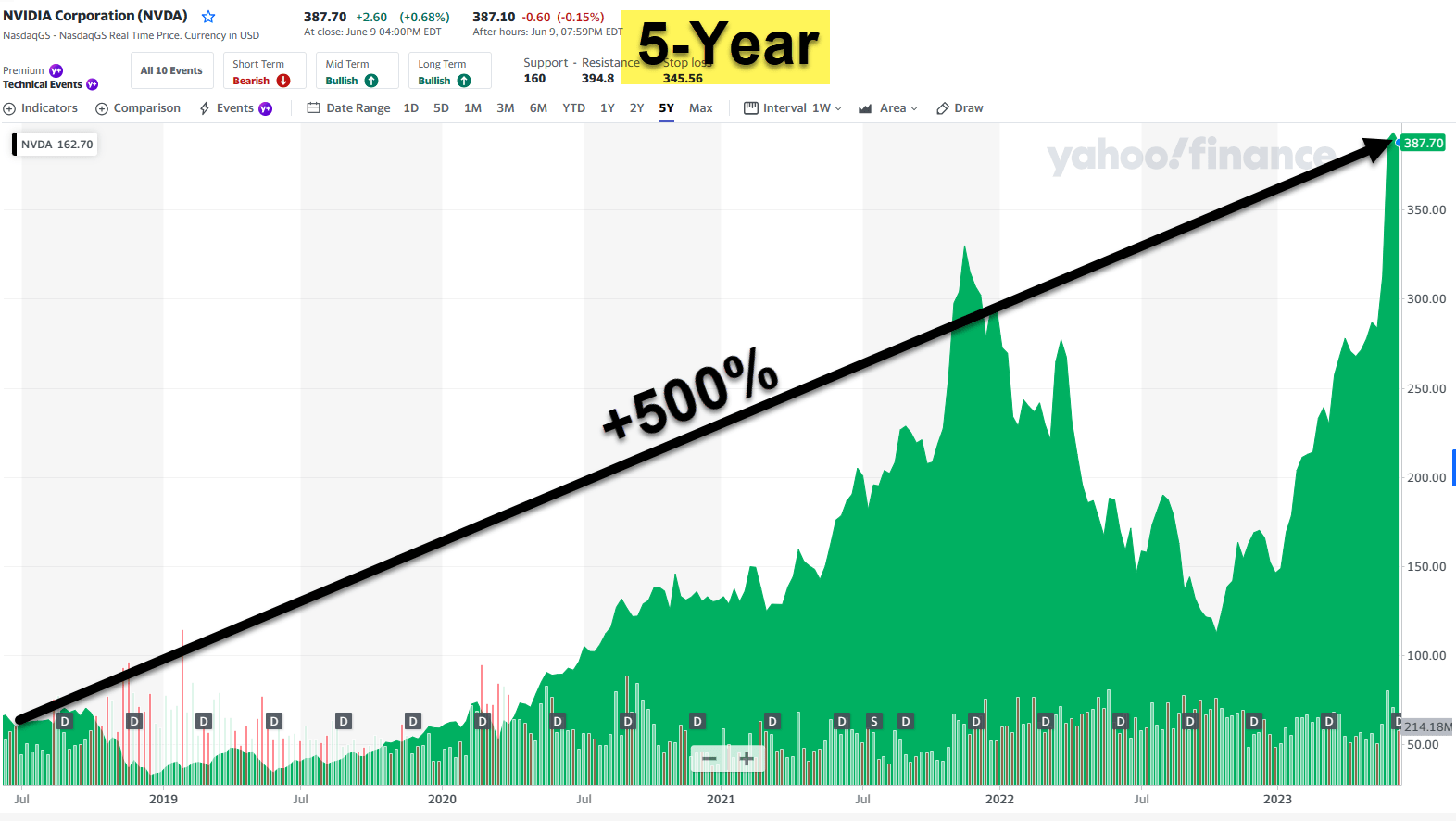

We saw Nvidia Corporation ( NVDA ) post earnings which blew away analyst estimates, causing that stock to spike by approximately 26.5%.”

{kind=link}

I pointed out in that same article that Nvidia is:

“a speculative growth stock that pays a paltry dividend, so it’s not really something that I’m interested in owning at this point in my life. However, a couple of the analysts on my team who own shares and cover the stock closely told me that NVDA’s report was a thing of beauty.”

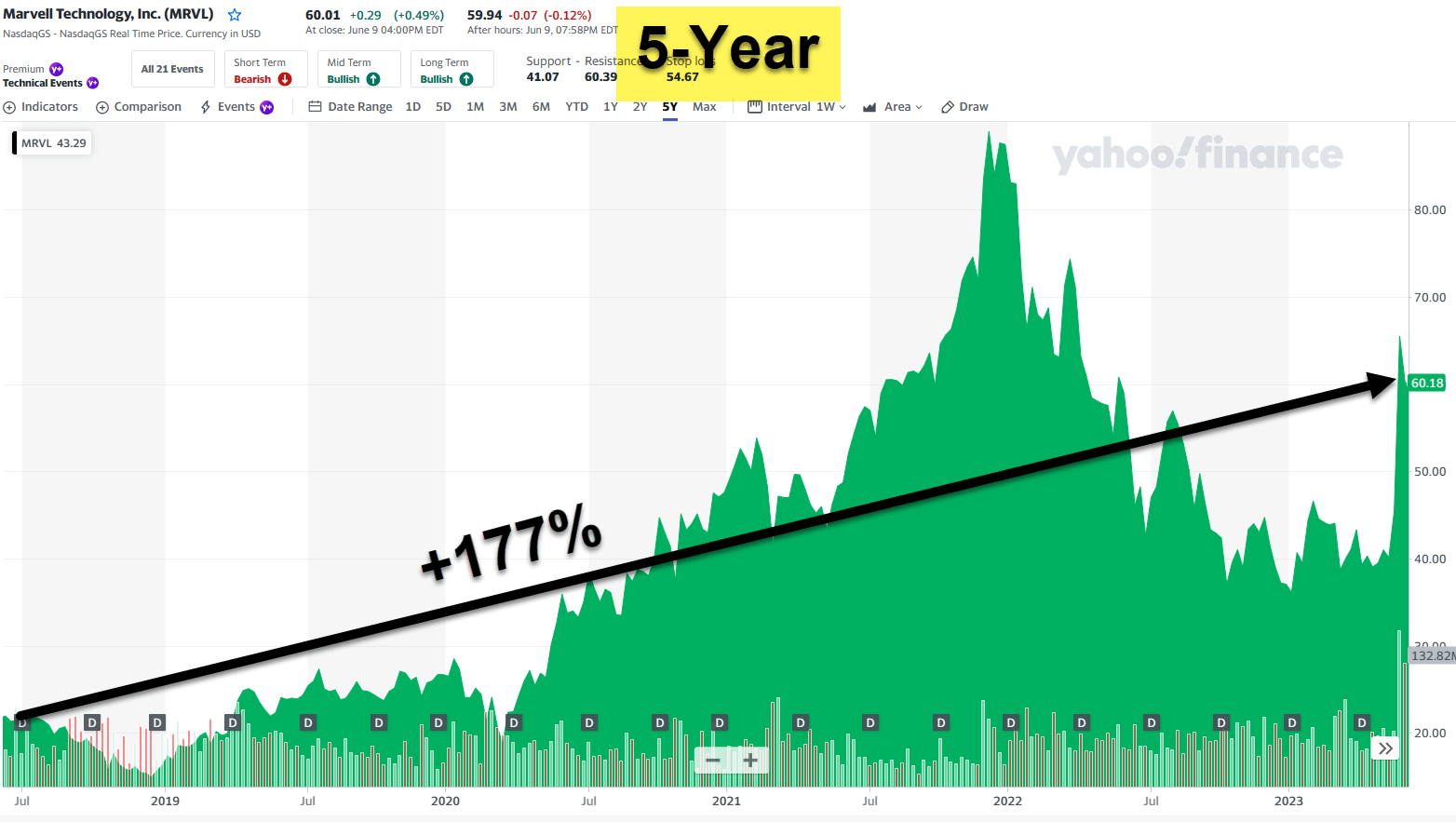

I also pointed out that Marvell Technology, Inc. ( MRVL ) similarly jumped 44.65% the preceding week, pushing its year-to-date gains up to 82.02%.

“Once again, A.I. was the driving force here, with its management team calling for its A.I.-related growth to be in the triple digits during its fiscal 2024.”

{kind=link}

Given all the AI buzz, it is certainly tempting to jump on the train with names like Microsoft ( MSFT ), Alphabet ( GOOG , GOOGL ), Meta Platforms ( META ), SAP SE ( SAP ), and Taiwan Semiconductor ( TSM ).

In full disclosure, I actually do own TSM thanks to my fellow contributor Chuck Walston’s work . We recommend the company in August 2022, and shares are up over 32% year-to-date.

{kind=link}

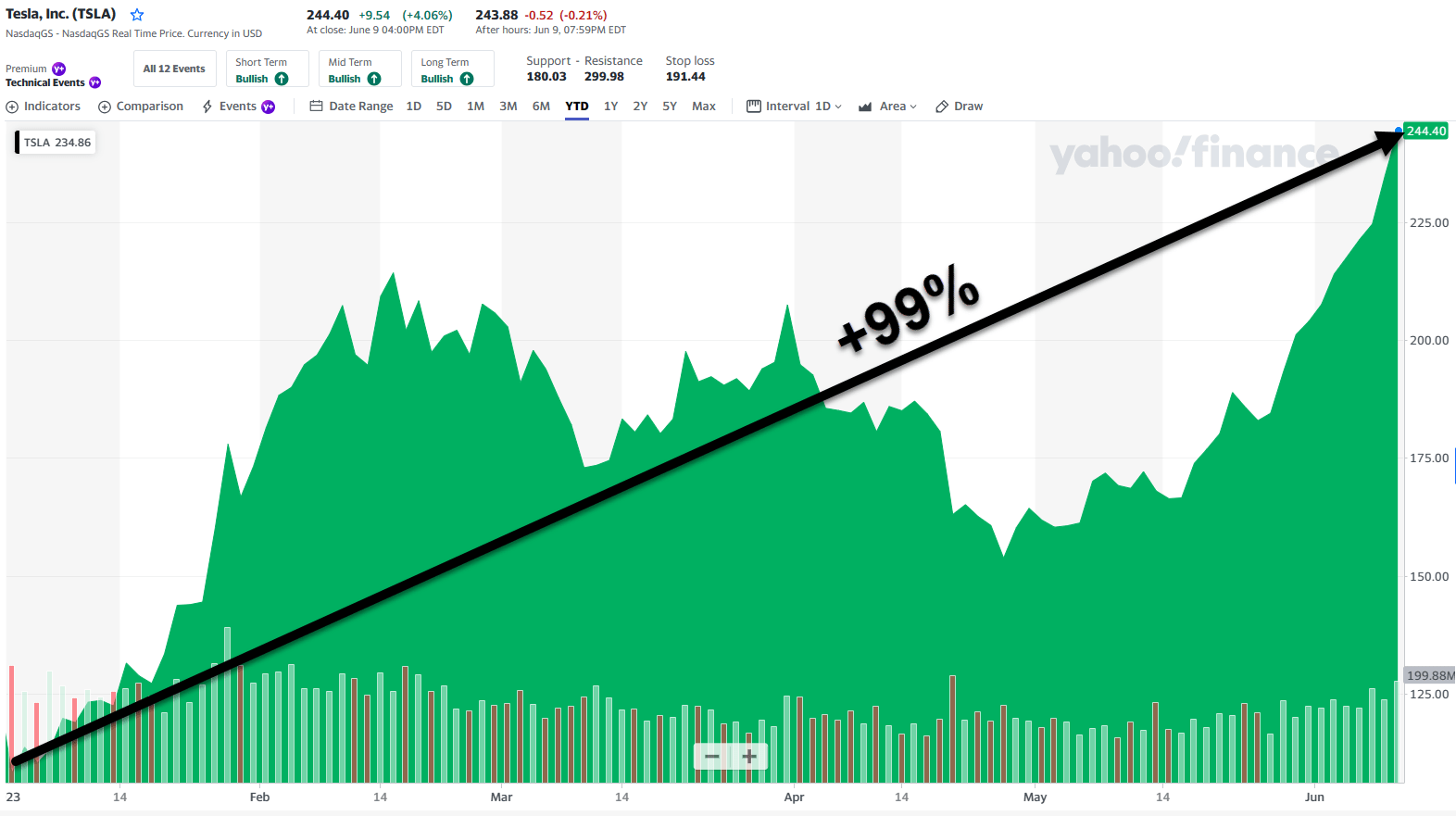

The other big tech name in my portfolio is Tesla, Inc. ( TSLA ) in which I decided to put chips on the table after reading fellow Dividend King’s contributor Dividend Sensei’s article last December.

In the article, he wrote that “Tesla, Inc. is one of the fastest growing companies on earth, with 27% earnings growth and 30% free cash flow growth.”

{kind=link}

Owning these tech names has certainly enabled me to generate outsized returns in 2023. More recently I joined the Advisory Board of nROAD , whose mission is to become a domain-led, unstructured content processing and insights generation company.

At iREIT™ we recognize that the rapid growth of data generation fueled by AI has transformed how data is stored, processed, managed, and transferred. And within the real estate investment trust ("REIT") sector, we see strong potential with the increasing demand for computing power across data centers.

To meet demand generated by AI, data centers are evolving and adapting their design, power infrastructure, and cooling equipment in various unique ways. Here’s the definition of a data center, as defined by Chat GPT:

A data center REIT is a type of Real Estate Investment Trust ('REIT') that specializes in owning and operating data center properties. Data centers are facilities that house computer systems, servers, network equipment, and other infrastructure necessary for storing, processing, and distributing large amounts of digital data.

Data center REITs acquire, develop, and lease data center properties to technology companies, cloud service providers, telecommunications companies, and other organizations that require robust data storage and processing capabilities. These properties typically have advanced cooling, power supply, and security systems to ensure the reliable and secure operation of the data center infrastructure.

Investing in data center REITs provides individuals with an opportunity to participate in the growing demand for digital data storage and processing. With the increasing reliance on cloud computing, big data analytics, streaming services, and the Internet of Things (IoT), the need for data centers has expanded significantly.

Digital Realty Trust, Inc.

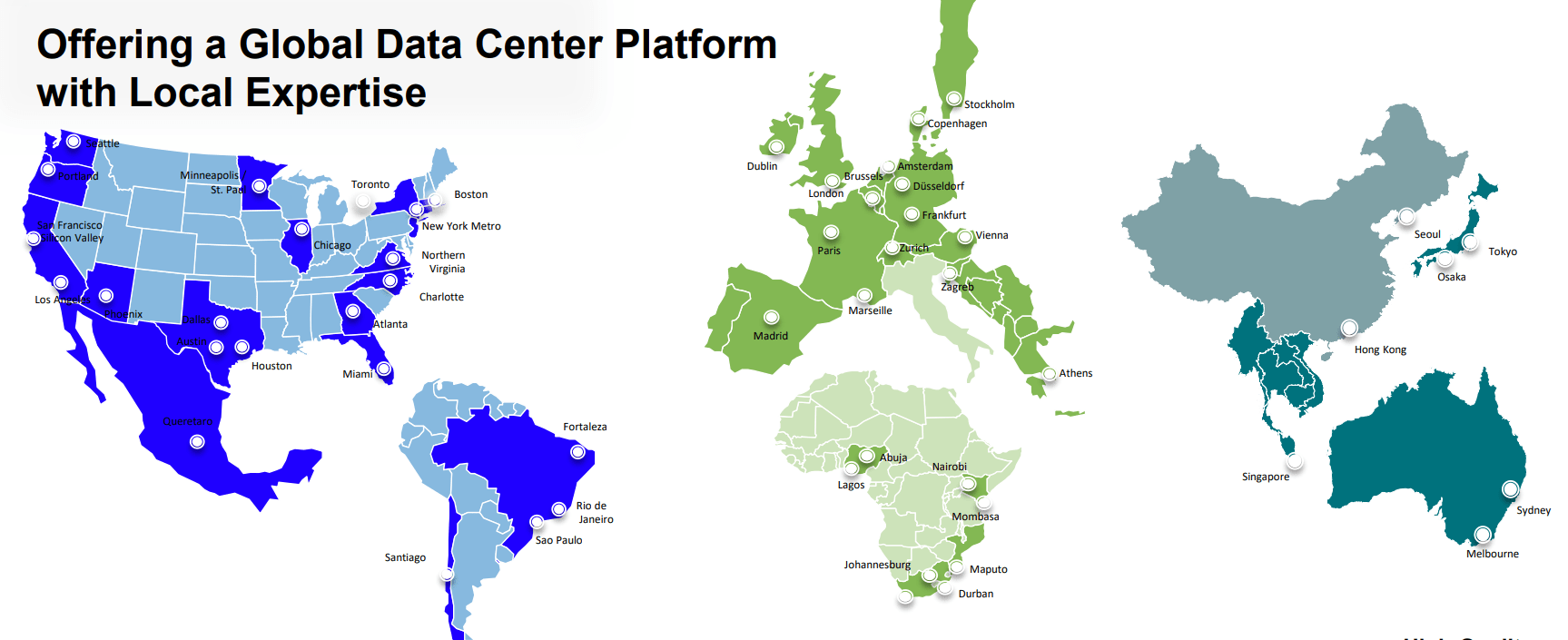

Digital Realty (DLR) is the largest owner-operator of data center capacity, digital infrastructure, spanning six continents, north of 50 metropolitan areas, supporting 5,000 plus customers worldwide, with a full spectrum of capabilities from enterprise-oriented hybrid, IT, co-location interconnection to the multiple megawatt dedicated data halls for hyperscale customers.

The global footprint includes over 310+ data centers across 25+ countries, and over 50+ metros. The data center platform has over 4,000+ customers including over 1,500+ enterprises, 1,300+ network service providers and over 1,100 cloud and IT providers.

{kind=link}

Here’s a breakdown of Digital Realty’s geographic diversification:

- North America 55%

- EMA 29%

- APAC 10%

- Latin America 6%.

Here’s a breakdown of Digital Realty’s customer type:

- Cloud 39%

- Content 13%

- Financial 12%

- Enterprise 9%

- Network 16%

- IT 12%.

Digital Realty owns most (87%) of its locations and leases (13%) the balance.

As viewed below, you can see that Digital has been very active in the M&A space:

{kind=link}

Data centers provide vast computing resources and storage, enabling AI to process massive datasets for training and inference. Digital realty is positioned to increase market share within the AI sector as explained by the company’s CEO (last week at REITWeek , emphasis added)"

“There is AI in our 300 plus data centers in terms of workloads, but it is a minority of the true sense of what AI is today and whereas could be in the future. And I'm seeing small minority.

The lion's share of not only our installed base, but our leasing activity, our new logos over the last several quarters, I would say, has not been AI oriented. It's the growth of the cloud. It's going to move from on-prem to off-prem. It's edge activities. We are, I would say, infancy may be an overestimation of where AI is as a category …

Certainly more training oriented. And I think that the definition of training and what training is today for artificial intelligence and what it will be in the future is going to obviously evolve. Only way I could think about this, I don't see how this is not a rising tide lifting all ships in the data center because this AI will live in the data center is my belief.

And we have a very big role to play. ..I think we're going to have a place to play in supporting the growth of AI . And what we're trying to do is navigate it to do that in the most value-add to the end customers' deployments to create a more sustainable business model around it.”

{kind=link}

The Balance Sheet

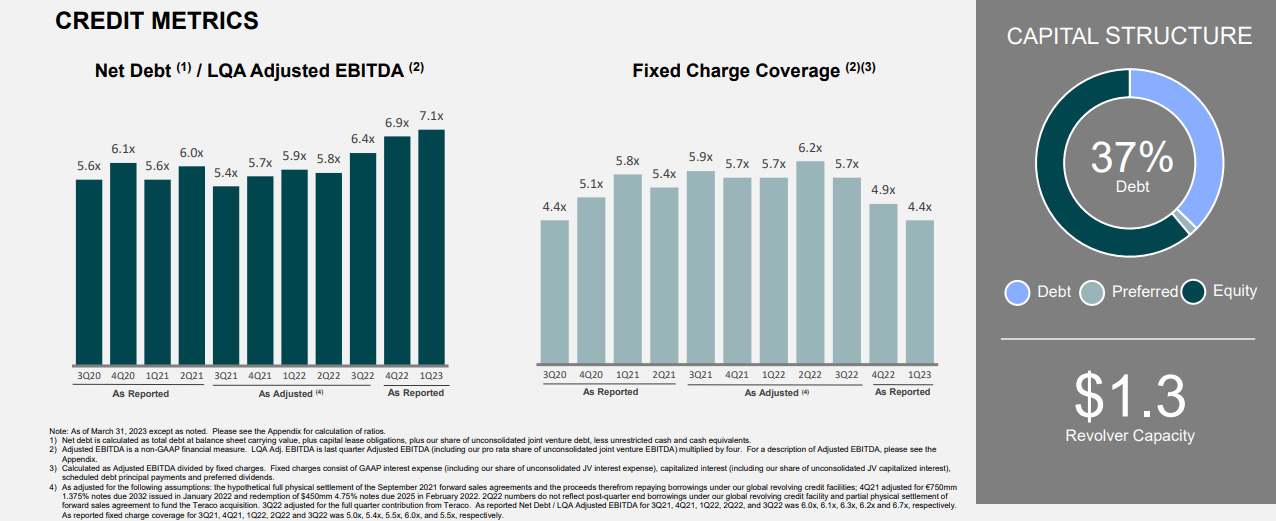

There is no argument that Digital Realty has seen intense capital headwinds in 2023 related to the company’s asset disposition plans and cost of debt that has more than doubled in 12 months. In Q1-23 , the company reported leverage of 7.1x and fixed charge coverage of 4.4x.

In January 2023, the company completed a $740 million 2-year term loan with an initial maturity date at March 31, 2025, plus a 1-year extension option and an effective rate of 5.6%. The company said that it “intends to reduce leverage toward the long-term target over the course of 2023.”

{kind=link}

To make that happen the company has been on aggressive asset recycling plan that includes JVs. The target is to recycle around $2 billion this year and to move leverage back towards 6x.

Last week (at REITWeek), Digital announced additional sales - this time it was a non-core data center in Texas in which the REIT realized around $150M of net proceeds from the sale of its 100% interest in the property.

The property, which was originally acquired in 2012 and leased as a powered shell facility, was sold at a 4.4% cap rate based on projected 2023 NOI, and generated a capital gain of ~$88M.

Separately, the company said it has raised some $1.1B of gross proceeds from the sale of ~11M shares issued under its at-the-market program, including 3.5M shares to be issued pursuant to forward sales agreements. Proceeds from the asset sale and ATM issuance are expected to be used to pay down debt and to fund ongoing and future investment activity.

As of Q1-23, Digital’s weighted average debt maturity was ~5 years with a weighted average coupon of 2.8%. Approximately 82% of debt was non-U.S. dollar-denominated, reflecting the growth of the global platform. Over 80% of net debt is fixed rate and 97% of debt is unsecured, providing ample flexibility for capital recycling.

{kind=link}

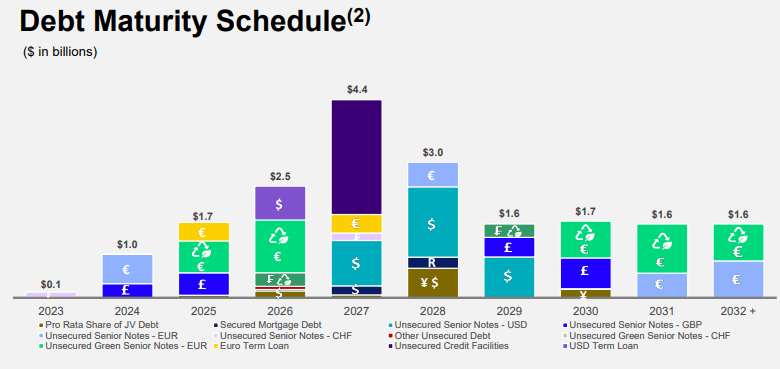

As you can see, Digital has minimal near-term debt maturities with only $100 million maturing in 2023, together with a well-laddered maturity schedule. The company is rated BBB by S&P with a negative outlook. Keep in mind that in 2013 S&P also gave the company a negative outlook that was later revised to neutral.

The asset sales should give the company breathing room and the price discovery has been very positive. As CEO, Andrew (Andy) Power, further explained last week:

“We laid out as part of our $2 billion funding plan that we initially laid out at the beginning of the year about $500 million of that is non-core dispositions...

…we are making progress with multiple parties and multiple projects, and I don't think we going to have to wait all too long for the next incremental data point to come to fruition here.”

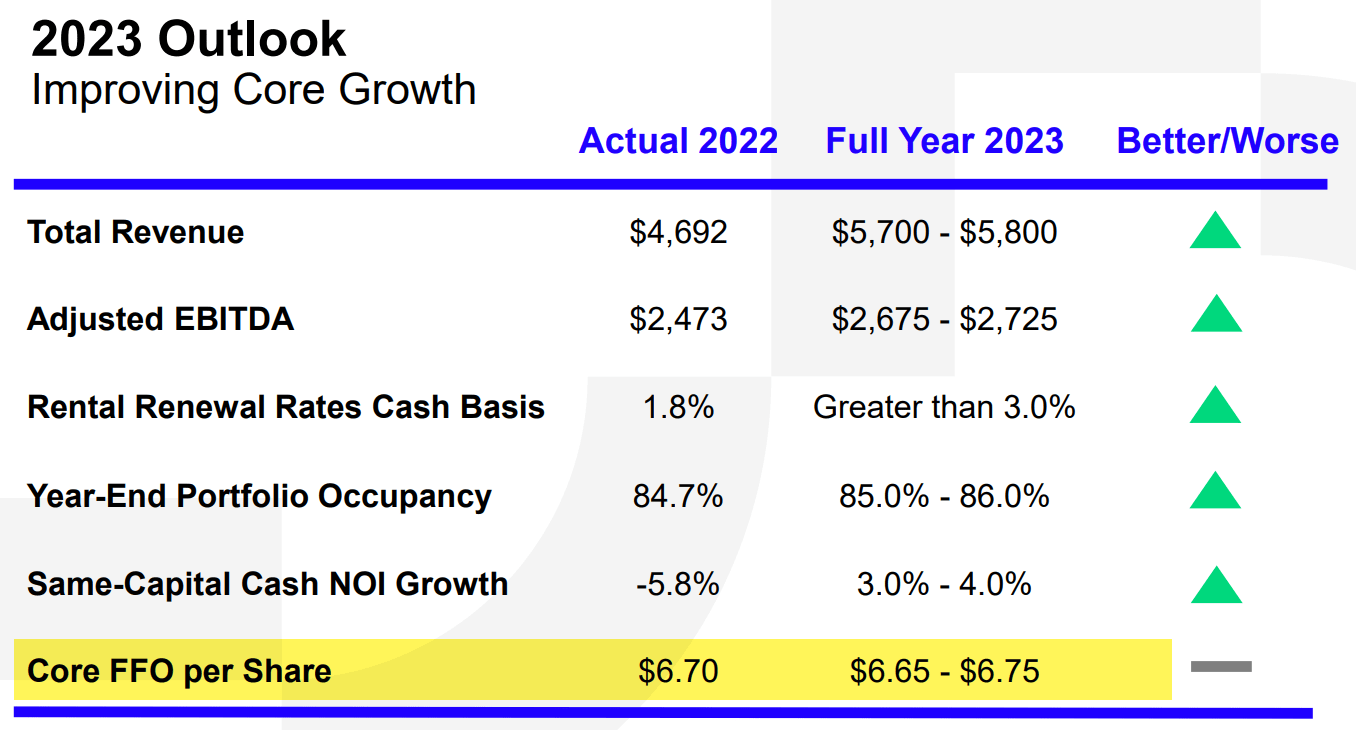

In terms of earnings growth, Digital reported Q1-23 core FFO (funds from operations) of $1.66 per share, $0.01 better versus prior quarter and a $0.01 light relative to 2022. On a constant currency basis, core FFO was $1.69 per share relative to the $1.67 reported in Q1-22. As viewed below, the company has guided $6.65 to 6.75 Core FFO per Share for 2023 (midpoint of $6.70).

{kind=link}

Is The Dividend at Risk?

As viewed below, Digital Realty has maintained an impressive track record of dividend increases for 17 years in a row. To accomplish that, the company has maintained a conservative payout ratio:

{kind=link}

At REITWeek last week, research analyst Jon Petersen asked a rapid-fire question: “Is there any risk to the dividend?”

The CEO, Andrew (Andy) Power, responded,

“The story with the dividend that those a little bit less familiar with REIT tax, so we have -- when we sell assets - either outright or joint ventures, we typically have capital gains because we build things to high returns and sell them at lower cap rates than those returns.

In order to retain that capital, the dividend essentially absorbs that return, otherwise, we have to pay a special dividend. So, if we believe that we're going to be successful in the non-core dispositions or the JVs that I mentioned, we should be keeping the dividend where it is to absorb that gain and retain that capital.

So, we believe we're going to execute on these joint ventures not in core assets, like I said. So hence, right, I do not see the risk of dividend based on that fact pattern.”

To put it in simple terms…

- DLR forecasts ~$2.7 billion in EBITD A in 2023 (see above 2023 Outlook chart).

- DLR’s development spend (cap ex) is ~$2.4 billion in 2023.

- DLR’s maintenance cap ex (i.e. batteries, roof replace, etc.) is $250 million .

- DLR’s interest income for 2023 is $400 million .

- DLR’s dividend is ~$1.5 billion ($4.88 per share) in 2023.

- The combination of 2, 3, 4, and 5 is $4.55 billion in 2023.

So, before development (which includes cap ex), Digital earns $2.7 billion and will pay out interest ($400 mm), maintenance cap ex ($250 mm), and dividends ($1.5 billion). That leaves $550 million for development ($2.4 billion).

As Andy Powers explained last week,

“…while as much as I do not love issuing equity at this current stock price, we thought it was a prudent course to not put the enterprise at risk and raise some capital to essentially be able to maintain the optionality and ability to execute on those investment opportunities.”

In other words, Digital has two important levers to use to fund the development pipeline:

- issue equity (which every REIT does to grow, including Prologis ( PLD ), Realty Income ( O ), Agree Realty ( ADC ), etc.) or

- recycle assets (which it’s doing currently).

Keep in mind, Digital does not need to develop whatsoever to cover the dividend. However, the data center giant has a long history of development success as the company targets (year one) yields of 9% to 15%.

Importantly, the development pipeline is 55% pre-leased , and 83% pre-leased in North America (thanks in large part to the big hyper-scalers). In certain markets (Dallas, Portland, and Toronto) the pipeline is 100% pre-leased.

To put this in more simple terms, the $2.4 development business generates attractive returns for investors, and in fact, this is the growth engine that has powered the business model since inception.

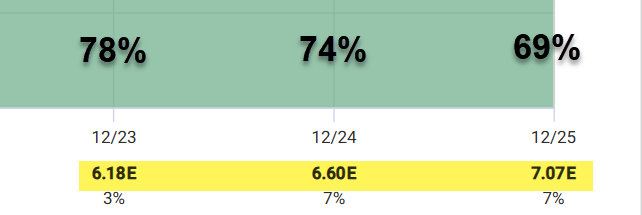

Using AFFO (adjusted FFO) per share analyst estimates (below) for 2023, Digital’s payout ratio appears safe (I used the current dividend per share of $4.88 for all periods). I see no risk of a dividend cut and I believe the company will stay on track to become a Dividend Aristocrat in a few more years.

{kind=link}

Management

Another risk to consider here is management and board turnover.

The CEO, Andy Powers, is fairly new to the CEO role. He was promoted to CEO last December after previously serving as president and CFO, after former CEO William Stein departed from his role and resigned from the Board of Directors. I met Andy last week at REITWeek and listed to his presentation. Here’s his bio:

Andrew (Andy) Power Bio

Andrew (Andy) Power is the Chief Executive Officer and a member of the Board of Directors of Digital Realty. Andy also has served as Digital Realty’s President since 2021 and as Chief Financial Officer since 2015, with responsibility for global portfolio operations, technology development and innovation, service provider and enterprise customer solutions, asset management and information technology, as well as the company’s financial functions across its global platform.

Prior to joining Digital Realty, Andy held positions of increasing responsibility at Bank of America Merrill Lynch, where he most recently served as Managing Director of Real Estate, Gaming and Lodging Investment Banking and was responsible for relationships with over 40 public and private companies, including Digital Realty.

Prior to Bank of America Merrill Lynch, Andy was employed by Citigroup, where he held similar positions. During his career, he has managed the execution of over $30 billion of public and private capital raises, including the largest REIT IPO to date, and more than $19 billion of merger and acquisition transactions.

Andy was part of the lead underwriting team that advised Digital Realty on its initial public offering in 2004 and served as a lead manager on nearly every subsequent public capital raise.

Andy also serves on the Board of Directors of Americold Realty Trust ( COLD ), where he is a member of the audit committee and investment committee. He received a Bachelor of Science degree in Analytical Finance from Wake Forest University.

Also, Digital has a new Chief Revenue Officer, Colin McLean, who previously served senior leadership roles including Senior Vice President, Global Accounts, and leader of the Global Sales Operations and Partnerships & Alliances efforts. He has over 25 years of sales and operational experience.

DLR Website

Also, long-term board member Laurence Chapman resigned last week, after serving on Digital’s board for 19 years. In a letter addressed to Chair Mary Hogan Preusse, Chapman raised concerns about the behavior of another member of the board, Mark Patterson.

Chapman also said his replacement as chairman of the board in a May 2022 board meeting "failed to follow a typical governance process." He said the topic of selecting a new chair wasn't on the board agenda, and that a subset of directors decided it was time for a change while at a hotel bar.

{kind=link}

Interesting to see that former CEO, Bill Stein, who was terminated without cause last year, used to work with Chapman in the '80s at Westinghouse Electric. Chapman was already set to depart last week and opted to resign a few days early, citing disagreements over certain governance practices.

As far as I’m concerned, the Board did a great job refreshing candidates. Chapman offered no new perspective, especially as it relates to the global initiatives of Digital Realty.

As you can see below, Digital now has a highly diverse Board that includes a Meta V.P. , a former Director of the US Air Force’s Intelligence Surveillance , Reconnaissance and Cyber Effects enterprise, a CEO Quanergy Systems, a provider of smart sensing solutions, a graduate of the U.S. Military Academy at West Point , a Board member of Dish Network ( DISH ), and former Managing Director and the Head of Real Estate Global Principal Investments at Merrill Lynch .

DLR Website

Another risk ( or opportunity ) worth mentioning -

Cyxtera Technologies, Inc. ( CYXT ) is Digital Realty’s 12th largest tenant (1.7% of annualized rent) and its Chapter 11 filing, while not completely unexpected, adds a potential headwind to Digital Realty’s core FFO growth recovery.

At this point, the financial impact is unclear, but an exit scenario would weigh on earnings, albeit potentially muted longer term by the ability to raise below-market rents.

CYXT has received a commitment for $200 million in new financing and noted its intention to pay vendors and suppliers in full under normal terms for goods and services provided on or after the filing date. However, any unpaid debts for goods/services provided prior to the filing will be subject to the Chapter 11 process.

CYXT leases 15 data centers from DLR including in Chicago, New Jersey, Silicon Valley, Frankfurt, and Singapore, many of which are critical to CYXT. However, CYXT filed bankruptcy in the U.S., which means that 20% of rent is not impacted from the non-U.S. assets (BK exposure is just 1.3%).

CYXT was forced into BK because of its enhanced floating rate risk which increased expenses by ~$50 million. We view this as an opportunity for Digital because CYXT’s tenants (in DLR’s buildings) pay 2x more rent, which means CYXT is making EBITDA from Digital’s buildings.

This could be an interesting opportunity for Digital to acquire CYXT’s asset light business model out of bankruptcy.

I’ll keep you updated on that front…

Valuation

I saved the best for last, which of course means I’m referring to valuation…

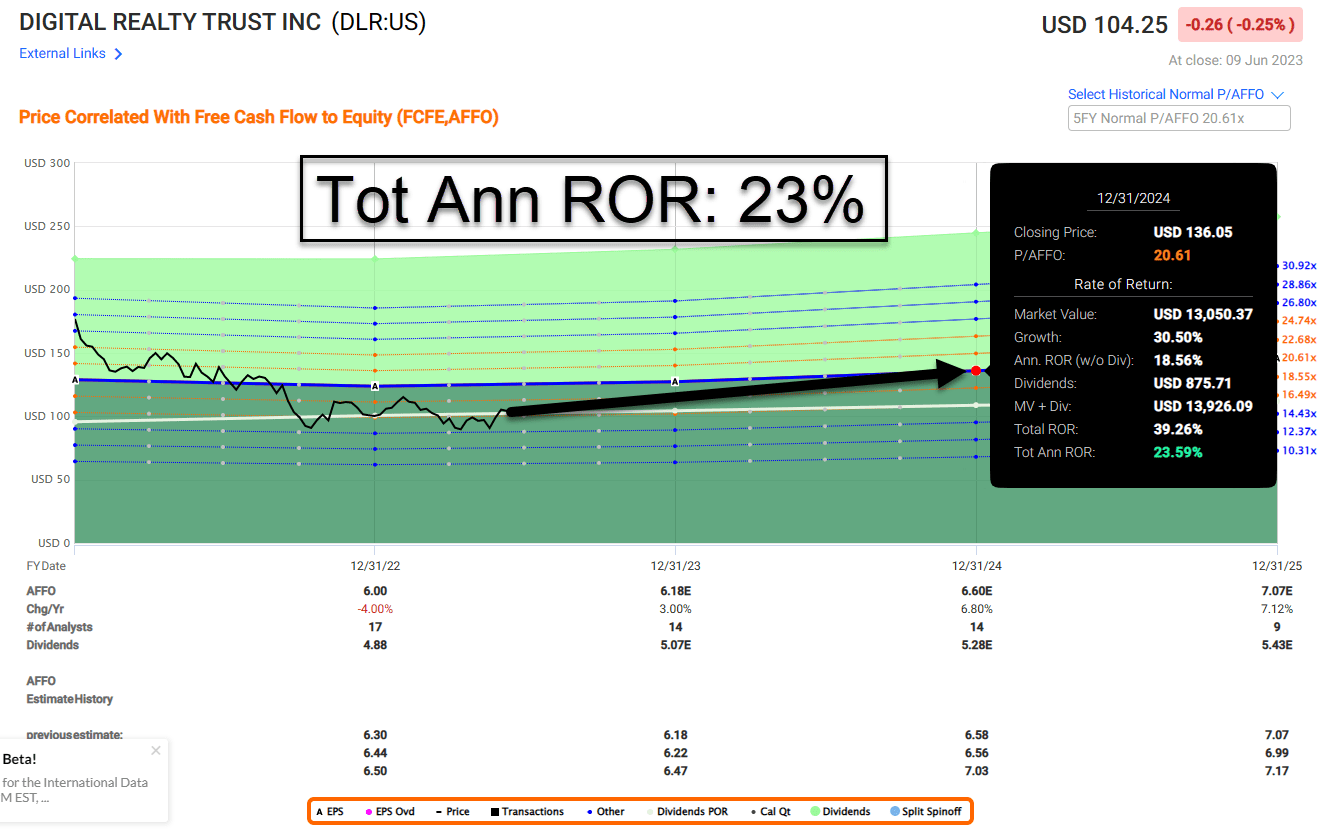

As seen below, Digital is trading a $104.25 per share with a P/AFFO multiple of 17.2x, compared with a normal P/AFFO of 20.0x. The AFFO equity yield is 5.8% (compared with the development yields of ~10%).

FAST Graphs

I like using FAST Graphs to highlight value while also comparing historical growth trends:

{kind=link}

As you can see, Digital’s valuation in these periods:

- 2007-2013: 19.9x

- 2013-2019: 18.2x

- 2020-2021: 24.0x

- Current: 17.2x.

Analysts are forecasting growth as follows:

- 2023: 2%

- 2024: 7%

- 2025: 7%.

Shares are now yielding 4.7%, and assuming analyst estimates are correct (17 analysts by the way), we believe shares could return 23% annually over the next 2 years.

{kind=link}

Digital has affirmed its full year adjusted EBITDA guidance of $2.7 billion at the midpoint and the company has made meaningful progress on fundamentals during the last quarter, including cash and GAAP re-leasing spreads over 3%, same-capital cash NOI growth of 3% to 4% and year-end portfolio occupancy between 85% and 86%.

As CEO Powers pointed out last week, AI demand is in its infancy and the opportunity is significant and at a minimum should help further support pricing.

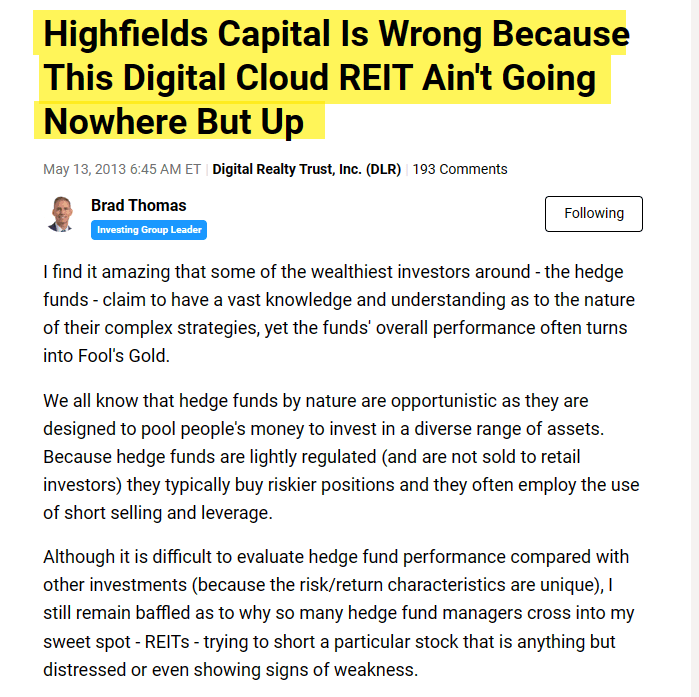

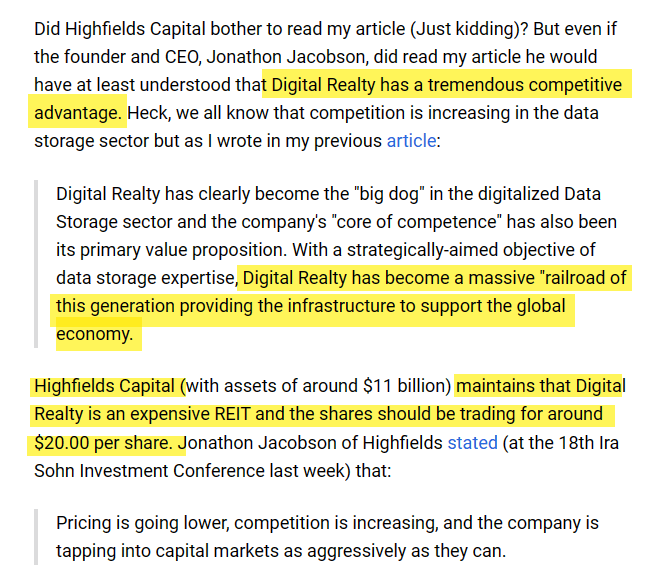

Finally, I want to point out an article I wrote back over 10 years ago (May 2013):

{kind=link}

Read more below:

{kind=link}

Well, my friends, history does not repeat itself, but it does rhyme…

I’m piling back into Digital Realty, recognizing that there’s a tremendous opportunity to capitalize on what I consider to be one of the best business models on the planet.

I don’t think anyone can argue with the demand side of the equation (you’re reading my article right now that’s housed in a data center) and in terms of supply, I’m happy to throw more capital at the company to support the growth pipeline (average 10% return on capital).

I also have confidence in the leadership, including the CEO and the diverse (and highly experienced) Board of Directors.

As always, thank you for reading and commenting and Happy SWAN Investing!

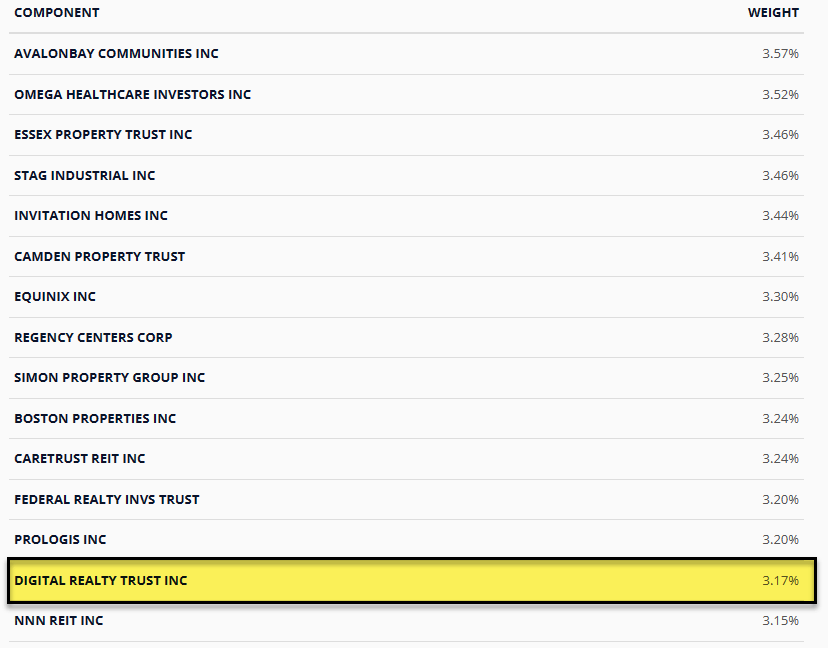

Note: Digital Realty and Equinix ( EQIX ) are constituents in the iREIT-MarketVector ™ Quality REIT Index that provides exposure to high quality U.S. listed common and preferred equity securities of REITs while ensuring sector diversification.

{kind=link}

For further details see:

Digital Realty: A Rising 'AI' Tide Lifts All Ships