VZ - DISH Network: Cash Constrained But Having Amazon As Partner Is Useful

2023-05-30 05:58:58 ET

Summary

- As a mobile network operator building its own network, DISH's strategy to deploy 5G is not a conventional one.

- Here, its partnership approach with Amazon needs to be highlighted especially that now it may improve its Go-To-Market strategy.

- However, this is a cash-constrained company that has to respect a deadline in June.

- Given its history of spending capital, it deserves to be on your watchlist.

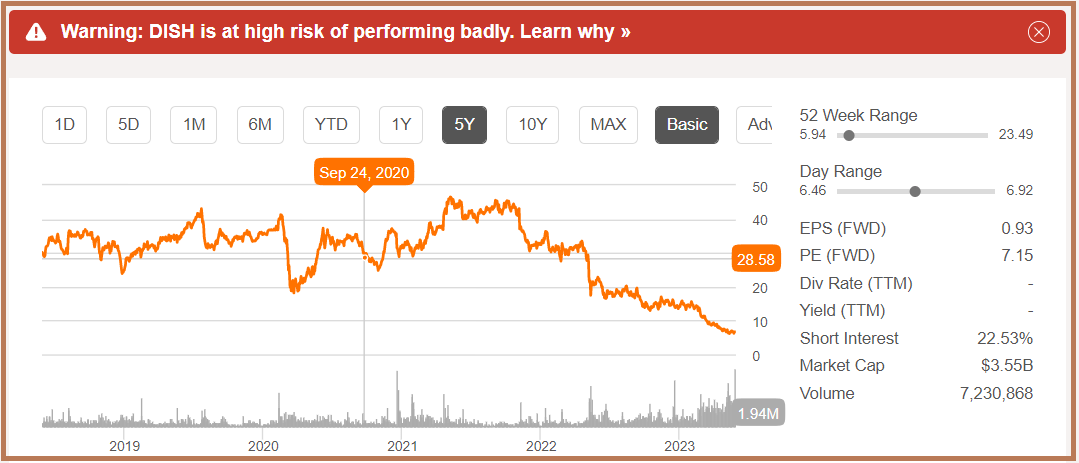

The last time I covered DISH Network ( DISH ) was in September 2020 when in sharp contrast with other U.S carriers, it had adopted a capital-light strategy to implement 5G. Thus, it partnered with Amazon’s (NASDAQ: AMZN ) AWS for hosting the underlying IT infrastructure and, now, there is a possibility of this partnership being extended to also cover product sales.

However, the market seems more focused on the company's finances and ability to deliver on time, with the stock falling from its mid-2021 high of $45 to trade at under $7. There are more downside risks as flagged in red below.

{kind=link}

DISH Performance (www.seekingalpha.com)

However, while the company's balance sheet is certainly tight in view of forthcoming expenses, the aim of this thesis is to also highlight the merits of the operator's disruptive strategy as a latecomer to the 5G arena already filled with strong competitors.

I start with how the nation’s fourth carrier and, by far, its smallest one too differentiates itself through partnering with the world’s largest public cloud provider.

How DISH Differentiates Itself

First, the deployment of the fifth-generation wireless network across the United States implies significant capital expenses. In addition to frequency spectrums which are auctioned at billions of dollars by the FCC, equipment is required for the core network installed in data centers and radio access atop towers.

Now, after purchasing frequency spectrum from T-Mobile (NASDAQ: TMUS ), and the 9 million customers of Boost Mobile in 2019, DISH had to build a 5G network to cover the majority of the nation by 2023. Unlike its peers which proceeded through the conventional way involving selecting a single source of supply like Ericsson (NASDAQ: ERIC ) for everything from hardware, software, and communications gear, DISH opted for several suppliers. These included Mavenir and Nokia ( NOK ) for software, antennae from Japan’s Fujitsu ( OTCPK:FJTSY ), and virtualization from VMware ( VMW ) just to name a few. The company also opted for Open RAN compared to more proprietary standards adopted by peers.

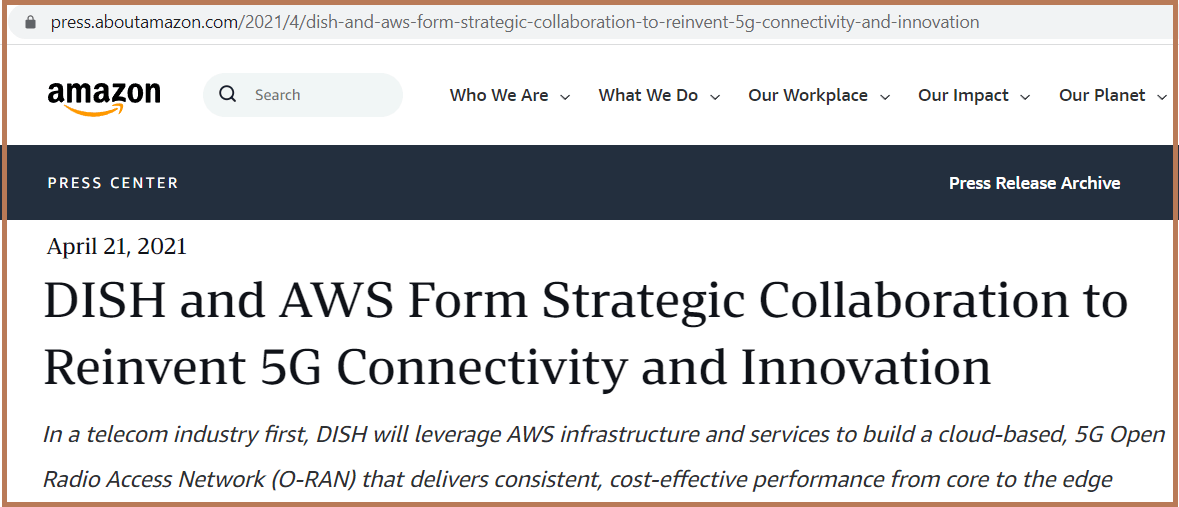

Furthermore, again in contrast with other operators, it did not buy container loads of servers for its data centers but opted for an Opex (operating expenditure) approach where you pay on a pay-per-use basis, namely through a partnership with AWS as illustrated below.

{kind=link}

press.aboutamazon.com

Therefore, far from being something "out of the blue", going through Amazon for selling represents a real possibility of the existing collaboration being extended, which this time could significantly improve DISH's go-to-market strategy.

Fast and Capital-Light Go-To-Market Strategy

The reason is first that selling subscription plans through Amazon's online shopping portal would give recognition to the DISH brand in a marketplace boasting nearly 38% of the U.S. eCommerce market share in June 2022, well ahead of eBay ( EBAY ) and Walmart ( WMT ). Furthermore, the giant online retailer has a vast network for DISH to sell 5G subscriptions.

This is somewhat analogous to the carrier outsourcing its marketing function while maintaining the network activation part. On the flip side, it will not necessarily obtain all the profits as some markup will go to Amazon (depending on the agreement made) but, in return, DISH does not have to spend money on marketing and sales, areas where competition remains tough. At the same time, the carrier stands more chances to abide by the FCC deadline as to the commercial availability of its product offerings.

Thinking aloud, financially constrained DISH is transiting from an MVNO (mobile virtual network operator) where it is essentially hitching a ride on top of T-Mobile’s and AT&T's ( T ) networks to becoming an MNO (mobile network operator). Here, since building its own infrastructure is capital-intensive, an Amazon deal may represent a much-needed lifeline somewhat similar to the IT infrastructure part.

In this respect, with cash and equivalents of only $2.5 billion and debt of around ten times more, the company’s balance sheet is flying close to the Sun since, after investing to achieve nationwide coverage, it still has to spend more money to enhance its network as it launches the commercial offers.

This may be the reason why investors' reaction was positive with the company gaining almost 19% premarket when the Amazon news broke out on May 25.

Focusing on Capex Usage Amid Challenges and the Deadline

In this respect, with lenders aware of the company’s current liabilities exceeding current assets, it becomes more difficult to obtain capital at reasonable costs, a problem which is exacerbated by the high prevailing interest rates, the result of the Fed's aggressively tightening monetary policy. Furthermore, with operating income margins of only 12% last year from its legacy businesses including satellite TV, and revenues having peaked in FY2021, it cannot rely on organic growth to generate enough cash.

Worst, as a late participant in the 5G game, it cannot count on a first-mover advantage but on the contrary, faces strong competition from AT&T, T-Mobile, and Verizon ( VZ ) throughout the United States. For this matter, its newly built network Boost Infinite network still has to support the iPhone which is currently proposed on a prepaid basis on Boost Mobile.

In these conditions, some may not have the stomach to invest, but, for those who are ready to take on the risks, I perform a comparison of the quarterly capex progression for the four carriers during the last three years.

As shown in the deep blue chart below, after peaking in 2022 due to the $7.3 billion spent on mid-band 3.45 GHz spectrum acquisition, DISH's capex has stayed much lower, at the $900 million level, which is at least four times less than its peers.

Tellingly, in case the company is able to achieve its June deadline to cover 70% of the population or 235 million people which is feasible according to its Executive Vice President for Network Development, this will be a meaningful achievement in terms of Capex to coverage ratio.

Now, as per the executive during the earnings call, investment should drop as the company attains its June milestone and subsequently, it will be more incremental expenses as DISH densifies or increases the quality of the coverage in regions where it is already present in preparation for commercial launch.

Do not Write off DISH Yet

They also add that expansion for the remaining 30% of markets will only continue in the late 2024 to 2025 time frame which gives the company some breathing space for the $1 billion of convertible notes becoming due on March 2024. As per the issuance details, it will settle its obligation either in shares, cash, or both. Now, given the liquidity conditions and the share price which is well below the $62.05 stock price at issuance, the most probable option will be a convert.

However, an even larger amount will be required for purchasing the 800 MHz spectrum from T-Mobile for about $3.6 billion, and in case DISH is not able to meet up with the deadline, it will incur a $72 million penalty. Add to this the $30 million of financial impact pertaining to the cybersecurity incident, and, you have two additional reasons for staying away from the stock.

Still, you cannot write off a company with $53.6 billion in total assets on its balance sheet, which exceeds overall liabilities of $34.9 billion. Noteworthily, these assets include the $34 billion of spectrum purchased at auctions and whose value has appreciated. In this respect, possessing more frequencies helps carriers deliver a better user experience through higher upload and download speeds, and as competition grows tougher the three other operators are likely to look for these, thereby providing DISH with an opportunity to monetize unused assets.

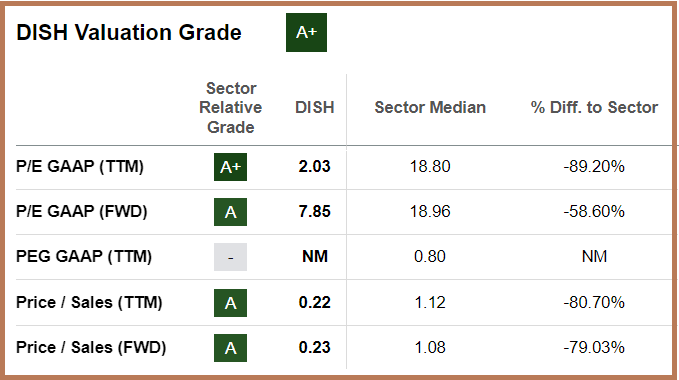

Continuing on a positive note, after seeing its value being eroded, the company has a valuation grade of A+ implying that its Price-to-Sales and Price-to-Earnings multiples are now lower than the sector median by more than 70% on average as pictured below.

{kind=link}

Valuation Grades (www.seekingalpha.com)

Also, this remains a profitable company with a profitability grade of B .

However, low valuations and profitability alone are not sufficient for DISH to be on your watchlist and the reason for my "hold" position. My main rationale is the possibility of the operator covering 70% of the country to meet the regulatory mid-June deadline, and doing so while incurring four times fewer capital expenses than its peer (above Capex chart). This should be due to its differentiated strategy encompassing the Amazon collaboration which circumvents the need to purchase certain equipment. Now, just think of the possibilities in case this collaboration is extended to product sales as the company starts monetizing its greenfield network.

Finally, the May 25 price action may have been ephemeral since the upside was not sustained, but, as per the old saying, "there is no smoke without fire". Therefore, there must have been some concrete talks between Amazon and DISH, and given their partnership history, we can't eliminate the possibility of a deal, something positive for the operator. On the other hand, investors also need to price in the downside risks in case penalties are inflicted if it is not able to deliver on time, and this is precisely the reason why you may want to see a corporate update on the 70% coverage before investing.

For further details see:

DISH Network: Cash Constrained But Having Amazon As Partner Is Useful