CA - Dividend At Risk: Sell Enbridge

Summary

- Enbridge's huge dividend yield looks like a trap; it’s now at risk of a cut.

- The company appears to be in a debt spiral, where it is forced to perpetually issue debt to maintain its dividend and meet short-term obligations.

- We'll analyze Enbridge's moat, normalized earnings, and investment prospects.

- In the decade ahead, I estimate total returns of 5% per annum, but is the risk worth the reward?

The Thesis

Dividend yields are great, but underneath every dividend yield is a real business, and you are the owner. Today, we're going to look beyond the dividend yield, deep into the financials of Enbridge Inc. ( ENB ). Hint : It's not looking great. I estimate that if Enbridge stock cuts its dividend, it can achieve total, long-term returns of 5% per annum.

Sell Enbridge

Enbridge is viewed by many as a safe dividend payer, with a consistent track record. You may look at Enbridge's pipeline business and think, "That seems like a consistent stream of cash flows." And, you'd be right, partially. The problem, of course, is Enbridge's free cash flow doesn't cover its dividend.

Below are Enbridge's yearly free cash flow numbers ( In bold ) and common and preferred dividends paid ( In Italics ):

| ||||||

| ||||||

|

Image created by author with data from Seeking Alpha (In Millions USD).

Combine this with the fact that Enbridge has very little available cash on its balance sheet and an overwhelming amount of short-term liabilities, and this puts the dividend at risk. So how is Enbridge paying its dividend anyway? Well, the company's increased its long-term debt almost 3-fold over the past ten years:

Noticed the big bump-up in debt from 2021 to 2022 (Roughly $7.5 billion)? That likely raised enough cash for Enbridge to keep paying you your dividend. Financing dividends with debt? Say it ain't so! Unfortunately, that appears to be the case.

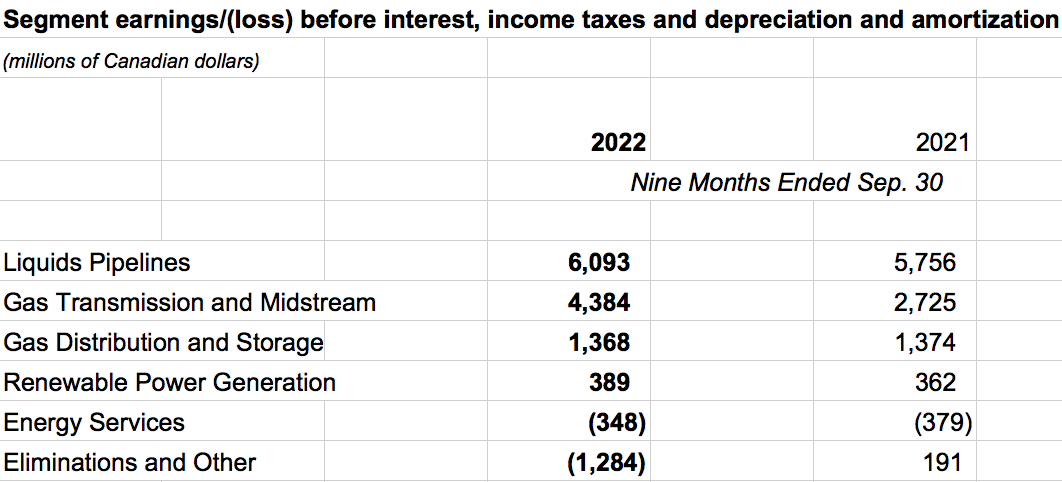

How Enbridge Makes Its Money

Before we continue, let's take a quick look at how Enbridge makes its money. Here's the company's segment results for 2022:

Enbridge's EBITDA By Segment (Created By Author With Data From Enbridge's 2022 10-Q)

{kind=link}

You can see that Enbridge has some renewable energy businesses. But, the company makes most of its cash from its pipelines and midstream operations.

Enbridge's Moat

I believe Enbridge's pipeline infrastructure is so large and essential at this point that the company has substantial pricing power. We've seen major railroad operations like Canadian National Railway ( CNR:CA ) and Union Pacific Corp. ( UNP ) pass on price hikes to customers and grow net income at a rate of 7% per annum over the past 30 years. Enbridge seems to have a similar "toll bridge" moat or durable competitive advantage.

Sailing On A Sea Of Debt

Enbridge has grown at an impressive rate, but its growth has been largely fueled by debt. Now, Enbridge is entering the precarious financial territory. The company's long-term debt and capital lease obligation is almost 9x larger than its operating income. As a rule of thumb, I like to see this number at less than 3x. Also, Enbridge's interest expense is about 40% of its operating income and rising. That's not a great margin of safety.

On top of all this, the company's working capital is negative $6 billion dollars USD, making it tough for Enbridge to service its short-term liabilities. The company also messes around with derivatives. In summary, as a student of accounting, I have concerns with Enbridge's financials.

Long-term Returns

Normalized Earnings

Enbridge's net income is abnormally low due to asset impairment charges . These come about from time to time, and essentially mean the company's assets are now worth less, on an accounting basis, than they were before. Luckily, the company has normalized its earnings for us in its recent press release , reporting adjusted earnings of $5.69 billion CAD. This translates to $4.27 billion USD or $2.11 per share for the New York listed stock.

My base-case scenario

My 2033 price target for Enbridge is $43 per share, implying returns of 5% per annum dividends reinvested. This is the result of growing $2.11 of adjusted EPS at 4.5% per annum and applying a 2033 terminal multiple of 13x.

- With extremely low unemployment in North America and an energy sector that's firing on all cylinders, Enbridge may be over-earning on an adjusted basis.

- I've assumed Enbridge will cut its dividend yield to 3.5% and pay down its debt. In my opinion, it's time for Enbridge to begin paying dividends with real cash flow and healthy dividend coverage.

- Because of the size of Enbridge's debt, it may be wise for management to sell some assets to improve balance sheet strength.

- While Enbridge has a strong position and little competition, it finds itself in a transitioning and plateauing industry. This partially offsets Enbridge's pricing power.

- Management's been investing in renewables, but so far, a lot of capital has been blown, as evidenced by the company's poor returns on invested capital.

In Conclusion

I have a sell rating on Enbridge Inc. A potential return of 5% per annum doesn't look too bad, but it implies an inflation-adjusted return of less than 2% per annum. And, that's assuming inflation reverts to its long-term average . Another thing to keep in mind is that I'm assuming Enbridge makes the responsible move of cutting the dividend. If management continues financing dividends with more and more debt, the future looks murky. Investors should be compensated for the risk that's at play here. In 2009, when credit markets froze, we saw what can happen to businesses with this amount of leverage. If you're looking to replace your dividend yield, I'm finding opportunities in international energy companies. For more on that, check out my articles:

You may also want to check out the pipeline infrastructure company Energy Transfer LP ( ET ), which has better dividend coverage (On a trailing basis) and a slightly stronger balance sheet.

Until next time, happy investing!

Note: This article analyzes New York listed stock ENB using U.S. dollar figures. The thesis, however, is nearly identical for ENB:CA.

For further details see:

Dividend At Risk: Sell Enbridge