LMT - Dividend Delight: Lockheed Martin Rides High On Favorable Winds

2023-06-21 08:00:00 ET

Summary

- LMT is my largest dividend investment, accounting for 7%+ of my portfolio. Its consistent shareholder value is my main reason for investing.

- Everything is in LMT's favor, with eased supply chains, funded defense programs, and successful investments in next-gen defense.

- LMT is confident in its position in light of the new defense budget (proposal), expecting growth to resume in 2024.

- Solid orders and positive signs in the space segment contribute to LMT's growth trajectory.

Introduction

Lockheed Martin ( LMT ) is my largest dividend investment. The company accounts for slightly more than 7% of my portfolio value, as I have aggressively added to the company in the past three years. Thanks to the headwinds the company faced after the pandemic, I was able to buy a few major corrections that allowed me to build a significant stake in LMT - relatively speaking.

My decision to buy was never based on any potential wars in the future, but on the company's ability to deliver consistent shareholder value.

Not only does LMT come with a decent dividend yield of 2.6%, but it is also now finally in a position where everything goes in its favor. Supply chains are easing, major defense programs are getting the funding they require, and investments in next-gen defense areas are starting to pay off.

In this article, I'll walk you through my thoughts as we assess the company's tailwinds, what we can expect in terms of long-term total returns, and what this means for the risk/reward.

So, let's get to it!

Everything Goes In Lockheed's Favor

Slightly more than 20% of my portfolio consists of four major defense contractors. That decision was never based on future wars, but on the simple fact that innovation in defense industries keeps us from dealing with major wars in the first place.

While we're currently dealing with the war in Ukraine, I believe that advanced technologies and partnerships are the reasons why this war won't likely go beyond Ukraine. For example, Poland is armed to the teeth, and most nations in that area are NATO members.

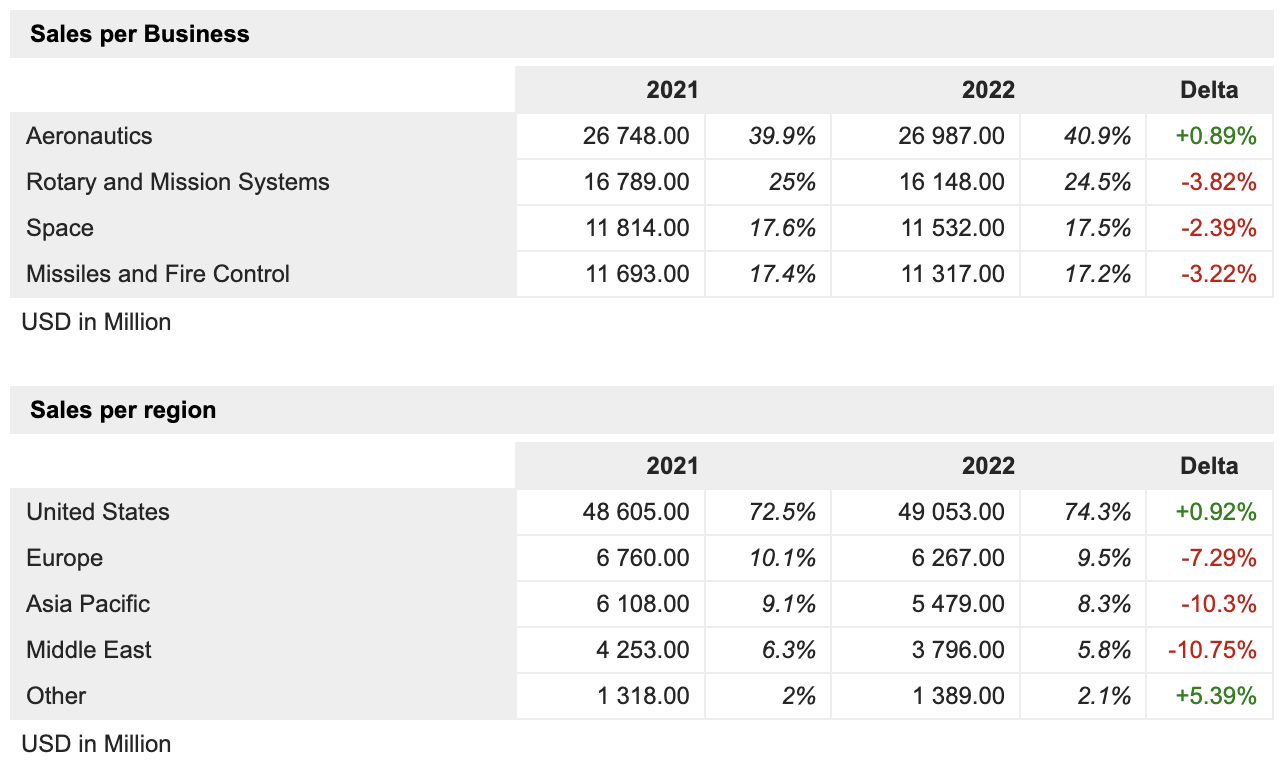

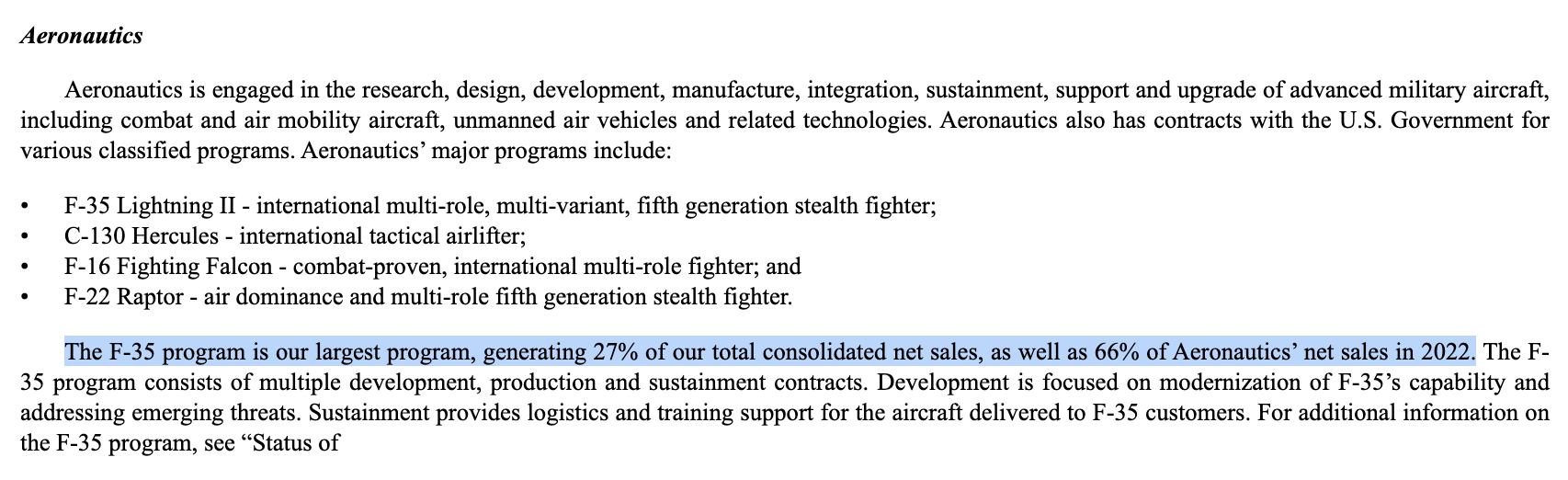

With that said, Lockheed is the cornerstone of NATO defense forces. Not only does it produce a wide range of products in its four segments, Aeronautics, Rotary and Mission Systems, Space, and Missiles and Fire Control, but it's also the main producer of the F-35, C-130 Hercules, F-16, and the mighty F-22, which is now in maintenance mode only.

{kind=link}

MarketScreener

However, one thing that is a risk is the fact that the F-35 program accounts for 26% of the company's total sales. It's a subdued risk, but potential issues in the future could have a major impact on its sales. I don't expect that, but not mentioning it would be wrong.

{kind=link}

Lockheed Martin 2022 10-K

With that said, during the recent Bernstein Annual Strategic Decisions Conference , the company commented on all key issues that were on my radar.

For example, the company expressed confidence in its position in relation to the Biden budget. CEO Taiclet stated that the initial budget provides sufficient funding for programs like the F-35 and munitions, aligning with the company's growth assumptions.

The 2024 budget looks favorable for Lockheed Martin, and even in the face of political discussions surrounding the debt ceiling, the defense sector is expected to generate 3% growth for two years.

While budget growth is not as high as some might have expected, we're seeing that companies with high-tech exposure are benefiting even from smaller budget increases because of targeted spending. The headline/article below is a good example of targeted spending.

{kind=link}

DefenseOne

In light of these developments, Lockheed expects growth to resume in 2024, supported by a solid backlog and a positive budget outlook. The company's backlog grew by 11% in 2022, and even excluding certain special items, it still experienced 5% growth.

The second quarter of this year (so far) has seen solid orders, particularly in the munitions sector. According to LMT, these orders provide multiple years of requirements, supporting the anticipated growth in programs like PAC-3, GMLRS, and HIMARS.

Additionally, Lockheed Martin's space backlogs are showing positive signs.

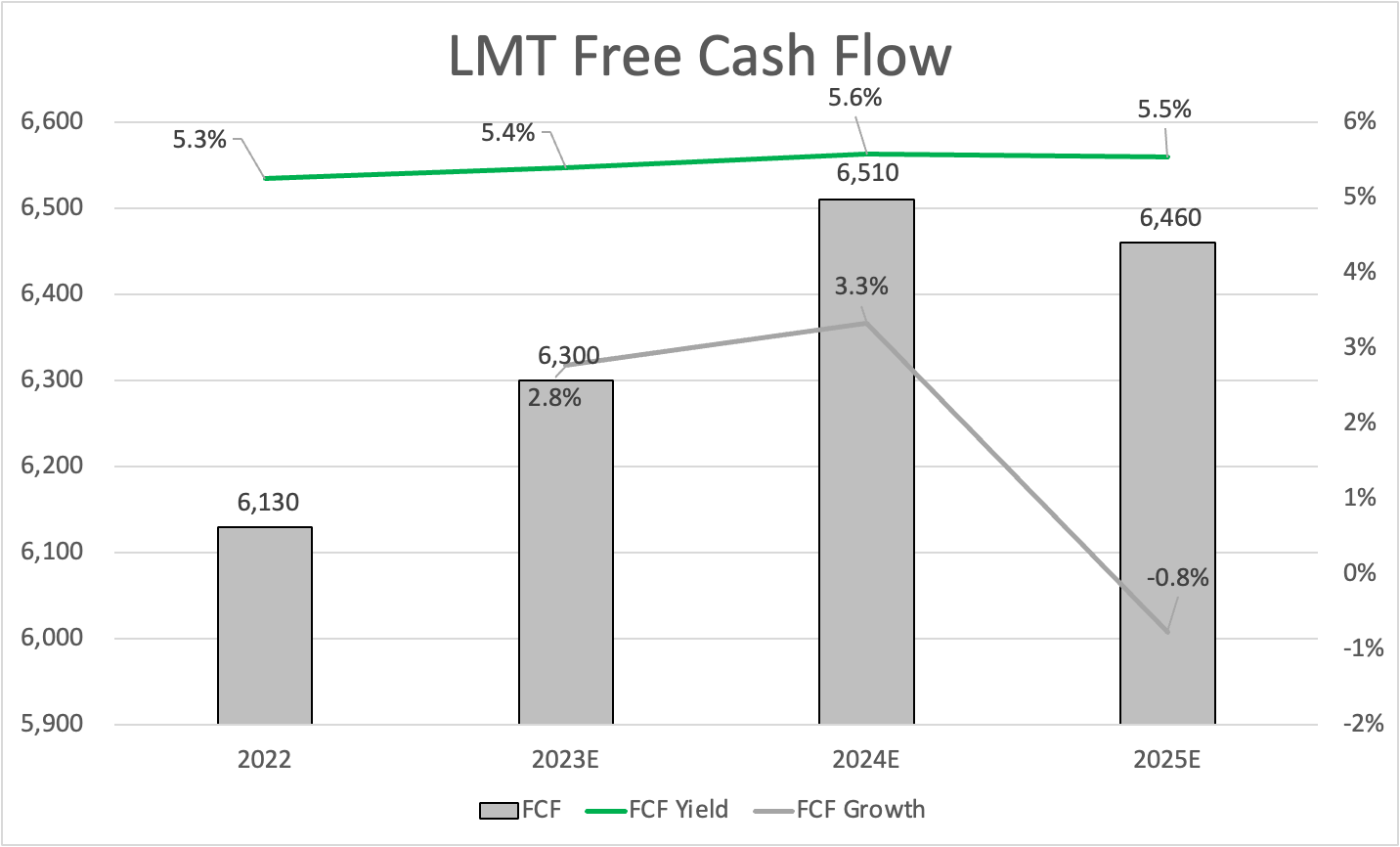

Based on these comments and looking at the chart below, we see that LMT had trouble growing since the pandemic.

Now, free cash flow is expected to grow again, which confirms the company's comments and ongoing trends when it comes to orders and operations. Please note that the graph below is based on consensus estimates, not company guidance.

{kind=link}

Leo Nelissen

Growth is not only supported by strong demand but also smooth operations in the mighty F-35 program. CEO Taiclet mentioned that the current production plan for 156 aircraft looks solid for the near term.

The potential for expanding production capacity is a separate decision that will depend on government interest.

However, Lockheed Martin believes it can sustain the current production rate with the current interest in the aircraft.

In terms of overall growth rates for the F-35 program, Taiclet highlighted the expected 6% compound annual growth rate in sustainment, which would contribute to low single-digit growth for the entire program.

The company remains committed to reducing sustainment costs per flight hour while increasing activity levels, which is something that would certainly please the crowd on Capitol Hill.

Adding to that, the F-16 program, which initially started in the 1970s, is gaining momentum. The cheaper alternative to the F-35 (I know it's not as good as the F-35) benefits from war-related uncertainties.

According to Lockheed, one aircraft has been delivered to Bahrain, with a backlog of 127 aircraft and an additional 20 expected to be added by the end of the year. The production rate is projected to reach three aircraft per month by the end of 2024 and a steady state rate of four by the end of 2025.

Further orders are dependent on the approval of the US Government, which includes potential sales to Turkey.

This brings me to Ukraine. Ukraine is now in talks to potentially get F-16 jets, in addition to a wide range of other weapons to support the ongoing counter-offensive.

{kind=link}

EuroAsian Times

According to Lockheed, its growth trajectory has seen a significant improvement due to additional funding to Ukraine.

As that sounds obvious, let me elaborate on that. For example, the programs like GMLRS, HIMARS, and PAC-3 (they are all advanced missiles) are expected to generate substantial growth until at least 2027 with estimated added revenues of $6 billion.

Beyond 2027, the potential for an additional $4 billion exists, resulting in a considerable growth outlook of approximately $10 billion over ten years.

Furthermore, the company is growing beyond replenishing NATO inventories.

In addition to new investments in hypersonics (super-fast rockets that are hard to intercept), it is seeing tremendous growth in an increasingly important business: space.

Lockheed Martin's space segment, now an $11 billion business, consists of national security and civil commercial space.

The national security space includes strategic missile defense and is transitioning from legacy programs to new ones. Legacy programs such as SBIRS and OPIR are cycling down. Excluding their impact, the national security space business was up 9% last year.

What does all of this mean for shareholders?

Shareholder Value & Valuation

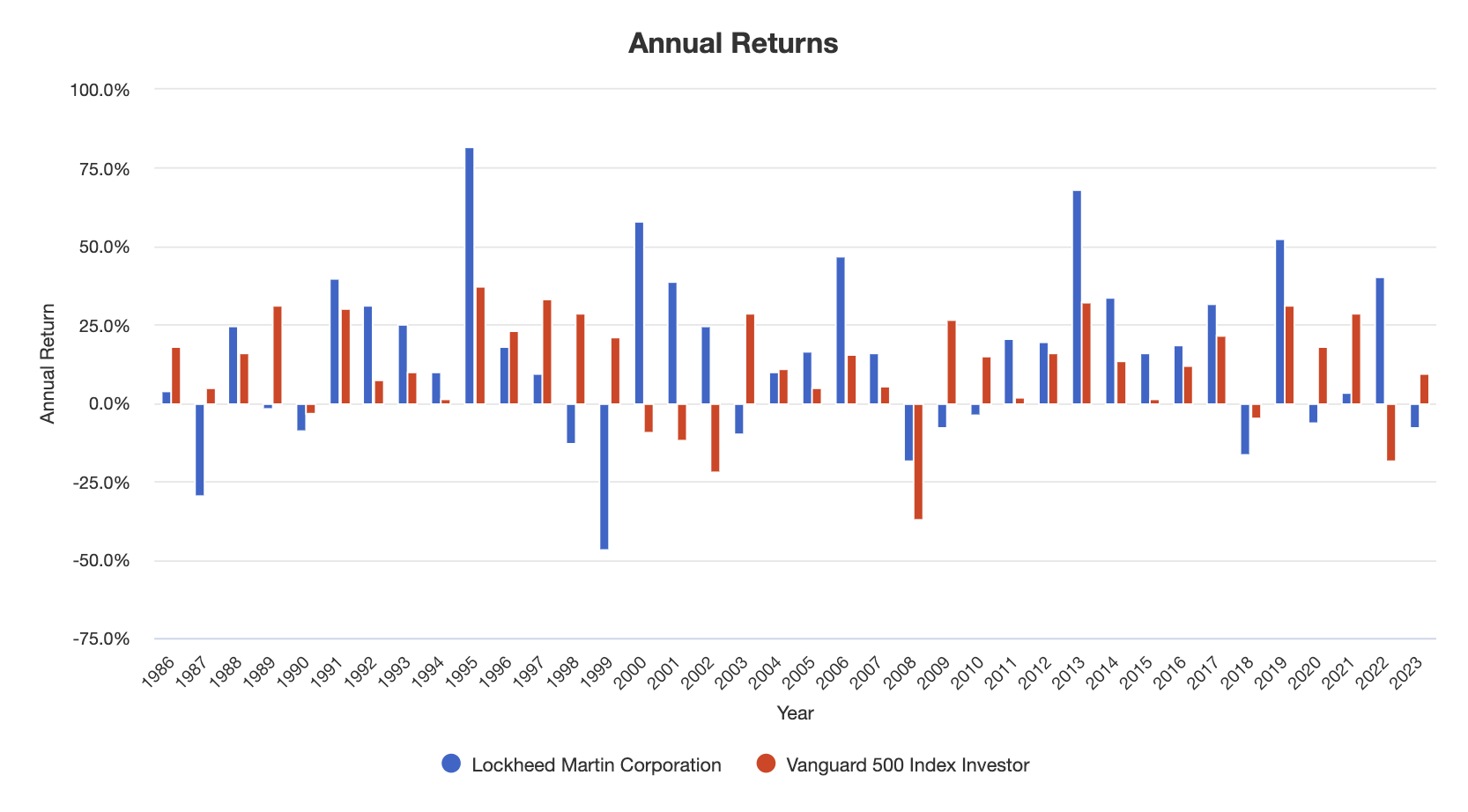

For many decades, LMT has been the source of conservative dividend income and capital gains for investors. Since 1986, LMT shares have returned 12.5% per year. The S&P 500 has returned 10.6% during this period.

While LMT isn't outperforming the market every year - especially not when it struggled with COVID-related issues - it is a source of stability during recessions. After all, its income is anti-cyclical. If anything, recessions tend to boost defense spending, as it's an easy way to stimulate the manufacturing sector due to the complex of tens of thousands of suppliers.

{kind=link}

Portfolio Visualizer

Consistent capital gains came with consistent dividend growth. Lockheed, which currently yields 2.6%, has hiked its dividend by 8.6% per year over the past five years (on average). The payout ratio stands at 42%, which means that we can expect mid-single-digit dividend growth going forward.

In this case, it also helps that LMT has a healthy balance sheet. Its 2024E net leverage ratio is 1.4x EBITDA, which comes with an A- credit rating.

This means that the company can prioritize shareholders over debtholders.

Furthermore, using the free cash flow chart in this article, the company has a >5% free cash flow yield, which is expected to rise towards 6%. This indicates high dividend coverage and room for further hikes.

Adding to that, Lockheed Martin targets low-single-digit growth in absolute free cash flow and mid-single-digit growth in free cash flow per share - boosted by buybacks.

The company aims to achieve a total shareholder return of 7-8% over the next three to four years, considering share repurchases and dividends.

While this doesn't come with any guarantees, I think it's a reasonable assumption based on the bigger story. Also, as an LMT shareholder, I am satisfied with this outlook.

Valuation-wise, we're dealing with a price-to-free cash flow ratio of slightly above 18x. The forward EBITDA multiple is at 13.1, which is a fair valuation as well.

The current consensus price target is $506, which is 10% above the current price. I agree with that and believe the stock will work its way to that price over the next 12 months. After that, I believe longer-term annual total returns will be somewhere between 7% and 10%, based on the company's comments and my view on the bigger picture.

FINVIZ

With all of this in mind, here's my takeaway.

Pros & Cons

Pros:

- Consistent shareholder value and dividend income.

- Stable performance during recessions.

- Strong position in the defense industry.

- Favorable budget outlook and funding for key programs.

- Growing backlog and solid orders.

- Commitment to cost reduction and sustainment.

- Healthy financials and dividend growth potential.

Cons:

- Risks associated with the F-35 program's impact on sales.

- Dependency on government contracts and defense spending.

Takeaway

As a long-term investor in Lockheed Martin, I am confident in the company's ability to deliver consistent shareholder value. With favorable market conditions, easing supply chains, and increased funding for defense programs, Lockheed is poised for growth.

While there is a subdued risk associated with the size of the F-35 program, the company's solid backlog and positive budget outlook provide reassurance. The potential for expanding production capacity and the growing momentum of the F-16 program further contribute to Lockheed's positive trajectory.

Additionally, investments in hypersonics and the space segment offer new avenues for growth.

As a shareholder, I value the company's commitment to dividend growth, supported by a healthy balance sheet and strong free cash flow.

Looking ahead, I anticipate annual total returns of 7% to 10% and believe the stock will reach the consensus price target of $506 in the next 12 months.

Overall, Lockheed Martin remains a stable investment with attractive long-term potential.

For further details see:

Dividend Delight: Lockheed Martin Rides High On Favorable Winds