LMT - Dividend Growth: Lockheed Martin Is My Largest Investment For A Reason

2023-07-18 16:50:44 ET

Summary

- Lockheed Martin is a solid investment due to its strong dividends, shareholder benefits, and impressive quarterly results, including record-breaking orders and improved supply chains.

- The company's future growth is expected to be driven by rising demand for defense equipment and services, positive developments in its Aeronautics and Space segments, and high demand for advanced missiles.

- Despite temporary setbacks, LMT's strong cash flow, commitment to rewarding shareholders, and attractive valuation suggest significant long-term growth potential.

Introduction

Let's start this article with a disclaimer. The Lockheed Martin Corporation ( LMT ) is my largest investment. The company accounts for roughly 7% of my dividend growth portfolio. The aerospace and defense industry accounts for 20% of my total exposure.

While one could make the case that this creates a risk of bias, I would argue that the opposite is the case. Because of the size of my defense investments, it's important to be extra careful, which is why I frequently cover LMT, as well as the headwinds and tailwinds of the entire defense industry.

In this article, I'm not only going to reiterate why I'm so bullish on Lockheed Martin, but I will use its just-released earnings and general industry developments to explain what investors need to be aware of going forward.

Luckily, I get to confirm my bull case, as Lockheed reported stunning new orders, good margins, and improvements in its supply chains.

Given the attractive valuation, I remain a buyer of LMT shares in my own portfolio and most of the portfolios that I advise.

So, let's dive into the details!

LMT Is A Dividend Gem With Shareholder Benefits

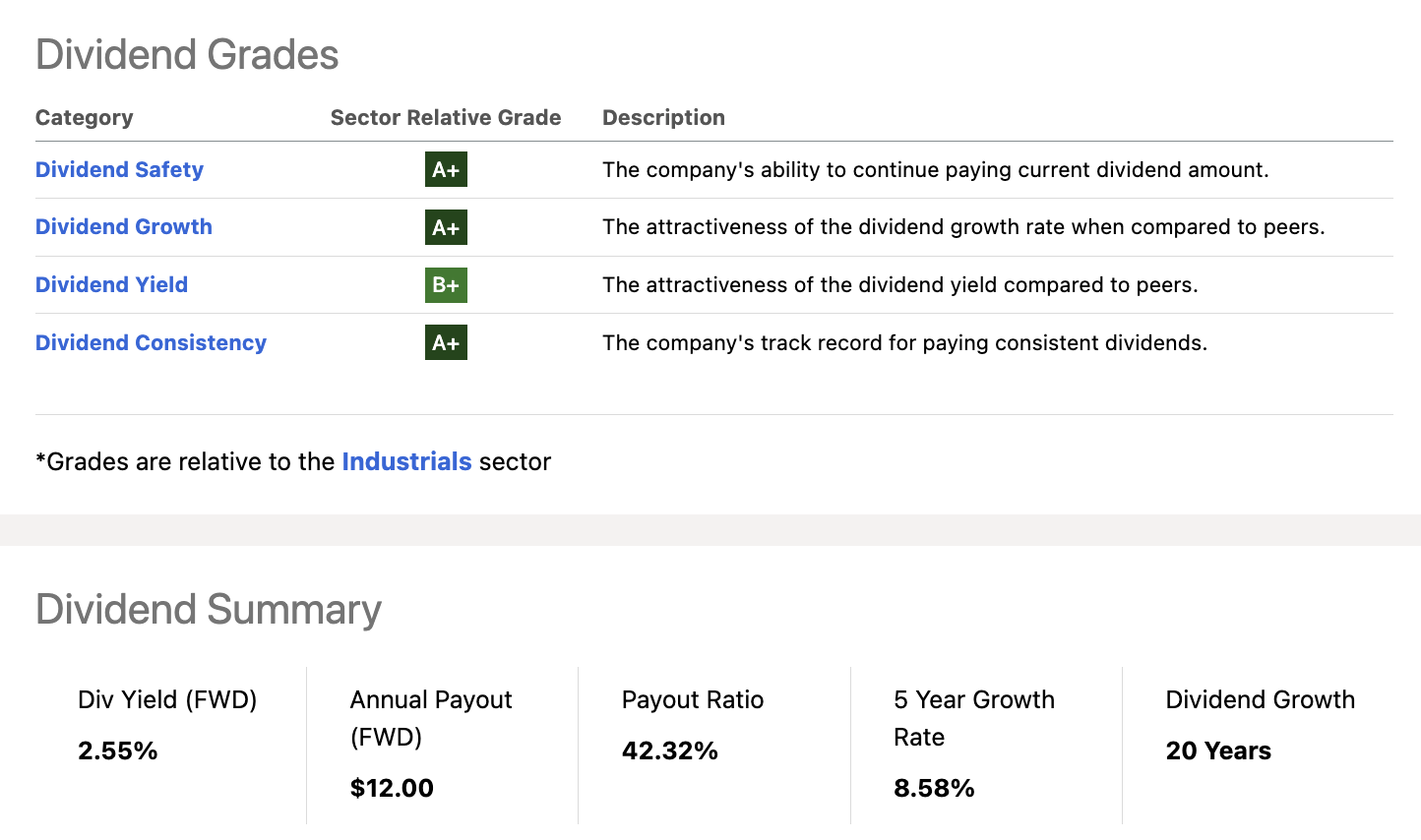

Before we get into the quarterly results and the bigger picture, I wanted to briefly highlight that the dividend is one of the main reasons why I added the stock to my dividend account.

Using Seeking Alpha's dividend scorecard, we see a lot of green. Please bear in mind that these are relative scores.

{kind=link}

- Lockheed currently yields 2.6%, which is roughly 110 basis points above the S&P 500 yield.

- The dividend is backed by a 42% payout ratio, which is healthy.

- Over the past five years, the average annual dividend growth rate was 8.6%.

- The company has hiked the dividend for 20 consecutive years. While it doesn't change much, the company could become a dividend aristocrat within five years.

During the past 10 years, LMT has bought back 21% of the total shares outstanding, which added tremendously to the per-share results, boosting its stock price and (indirect) shareholder value.

Thanks to these developments, LMT has outperformed the S&P 500 by a wide margin over the past 10 years - despite a series of issues like supply chain and budget issues that mainly occurred after the pandemic.

Having said that, I expect that LMT will continue to outperform the market, consistently grow its dividend, buy back shares, and maintain a low-volatility profile.

2022 Likely Was A Turning Point

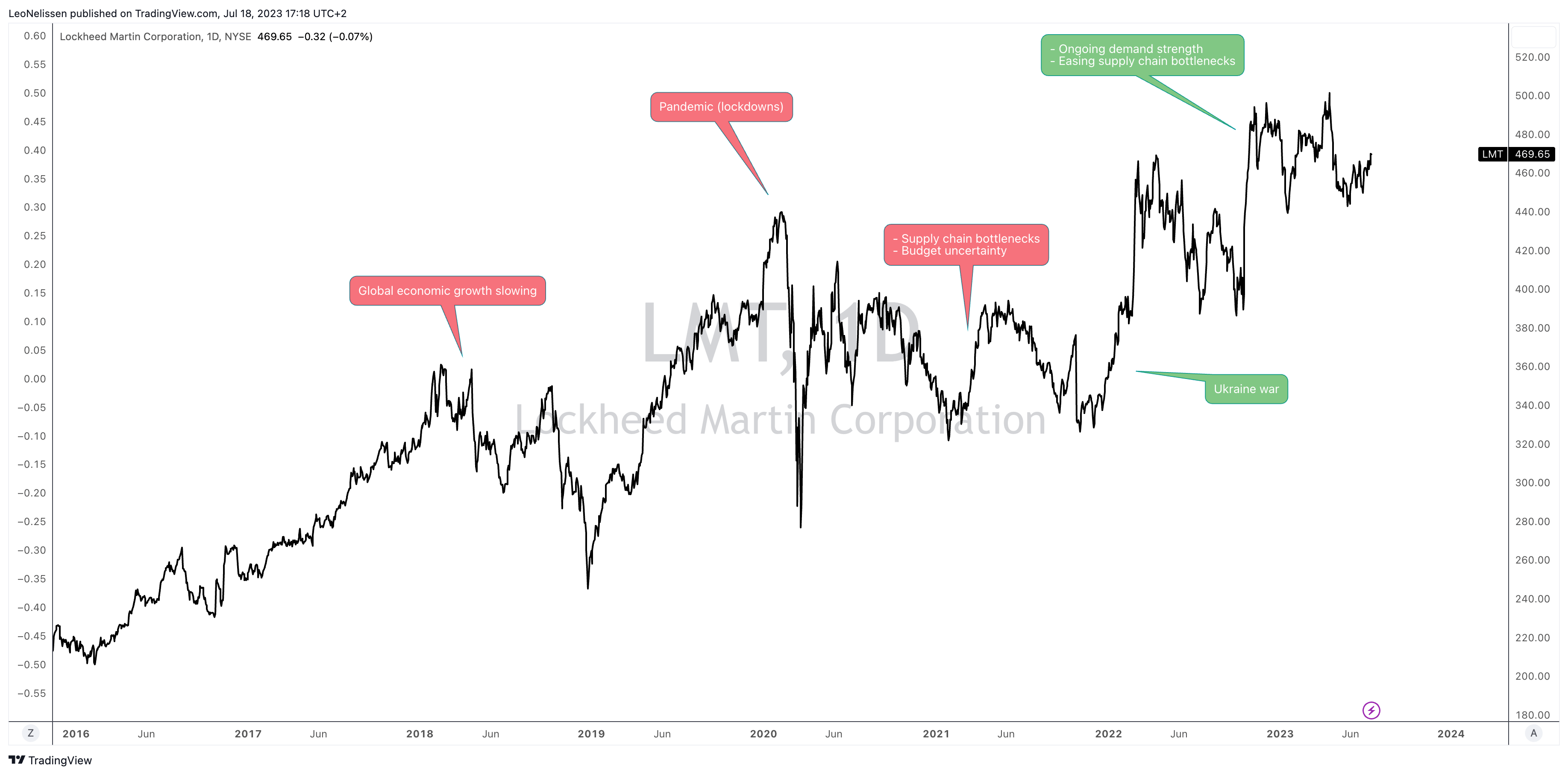

Shortly after the earnings release, I shared a chart on Twitter (the one below), which shows a number of forces that impacted the LMT stock price (my apologies for the small letter size).

Essentially, the stock didn't go anywhere between 2018 and 2022 (excluding dividends). In 2018, economic growth slowing hit the stock market. Once LMT started to gain momentum, the pandemic hit.

Although LMT has an anti-cyclical business without major commercial exposure, the supply chain troubles that followed did hurt the company a lot.

Shortages kept LMT and its peers from turning backlog into finished goods, while high inflation did a number on its margins. It also didn't help that there was a lot of uncertainty with regard to the defense budget.

TradingView (LMT)

{kind=link}

Having said that, my case is that LMT is now poised to continue its uptrend, as it's likely that 2022 marked the start of a sustainable uptrend driven by (among other factors):

- Rising demand for defense equipment and services.

- Rapidly easing supply chain bottlenecks.

The just-released earnings confirmed all of this.

When Everything Goes Right

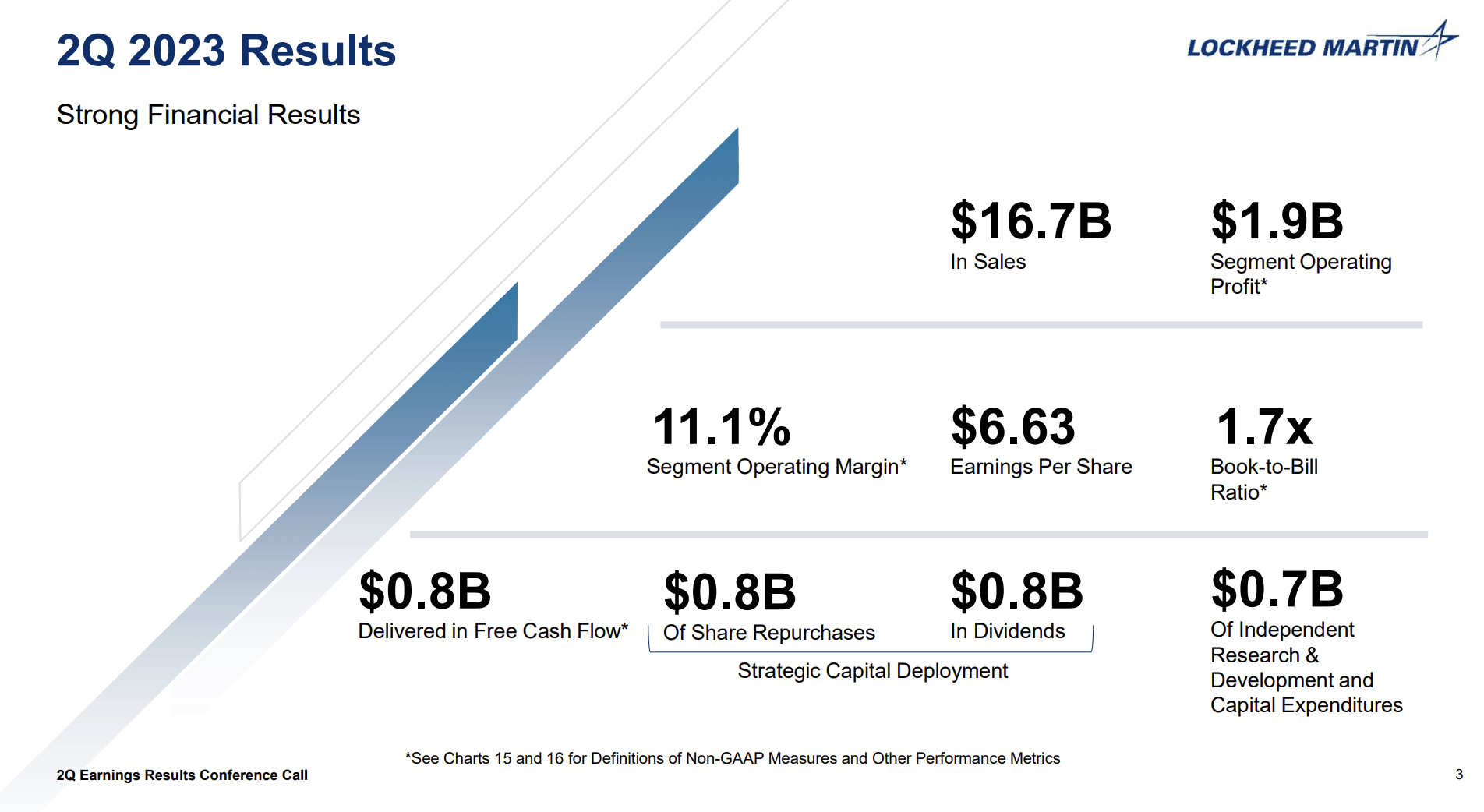

While the stock price didn't indicate it after the release, 2Q23 was a big success. The company generated $6.73 in EPS, which beat estimates by $0.28. This marks the fourth-consecutive time earnings came in higher than expected.

Seeking Alpha

Sales reached $16.7 billion, which is an 8% year-over-year increase, driven by double-digit growth in both Aeronautics and Space segments.

The company's backlog also hit a record level of $158 billion, indicating substantial demand and future sales visibility.

Not only did the backlog reach a record, but the company also reported a 1.7x book-to-bill ratio, which indicates that for every $1.00 in finished products, the company is getting $1.70 in new orders. This is proof of a much healthier demand environment and indicative of higher future growth.

{kind=link}

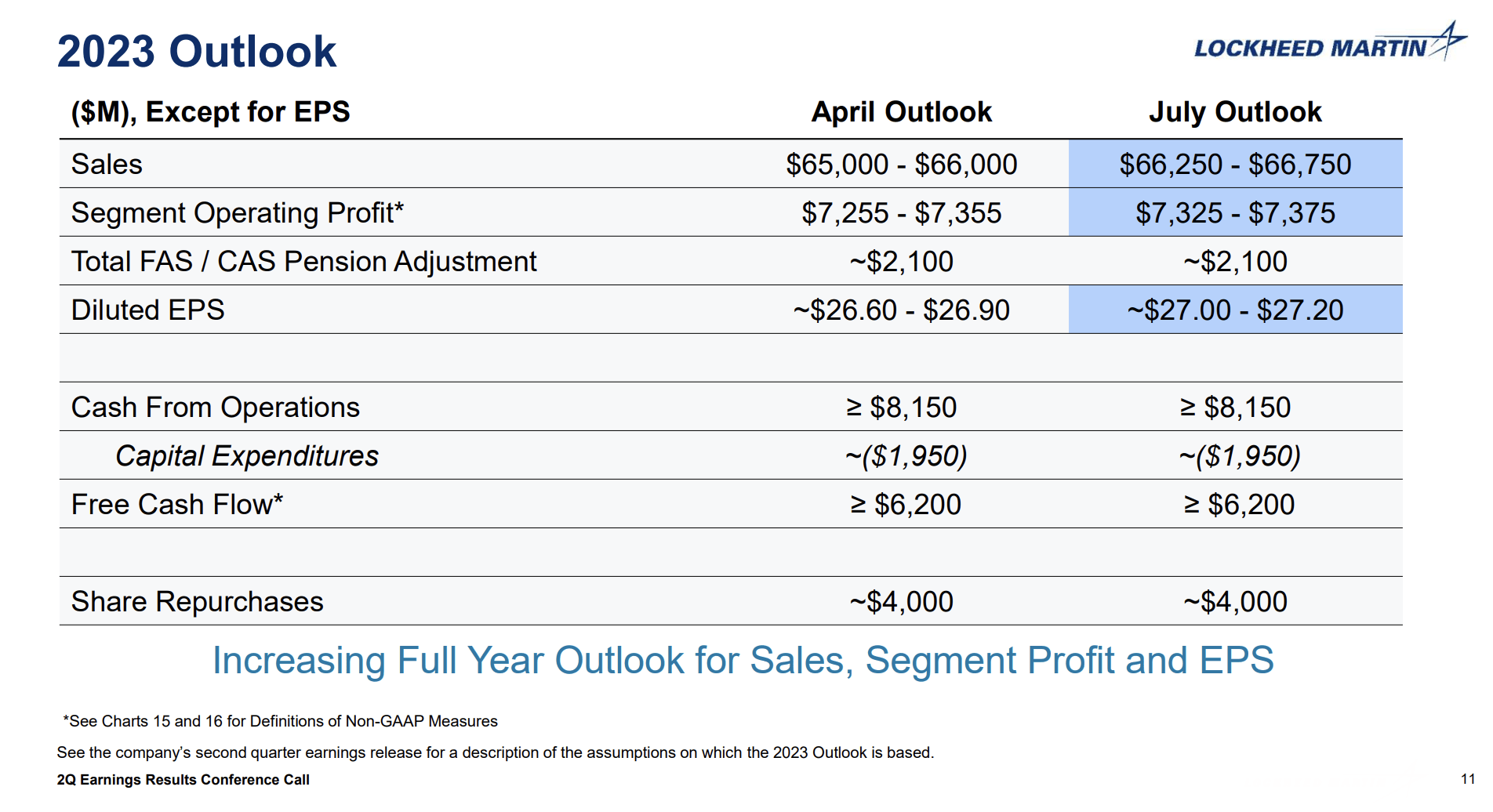

It also allowed the company to improve its guidance.

The company both raised and narrowed its full-year 2023 financial outlook due to the strong results in the first half of the year.

- For sales, the midpoint of the range was raised by $1 billion, resulting in a revised expectation of between $66.25 billion to $66.75 billion.

- The midpoint of the EPS range was also increased by $0.35, leading to a revised expectation of between $27 to $27.20 per share.

Essentially, LMT is confident in its ability to achieve these higher expectations and return to growth sooner than initially anticipated.

{kind=link}

Having said that, I want to highlight a few developments that explain why the company is so confident in its ability to return to growth sooner than expected.

For example, the outcome of the most recent debt ceiling negotiations preserved top-line defense spending at the president's budget request for FY2024. It also included stipulated defense budget growth in FY25 with the possibility of additional support through supplemental funding.

- The proposed FY24 defense budget incorporates funding for 83 F-35 aircraft, with supplemental funding to support munitions investment and ramp up production rates.

- The F-35 program continues to see strengthening customer demand both domestically and internationally. Notably, the Czech Republic has expressed interest in the aircraft, and Israel has decided to add 25 more F-35s, expanding their fleet by roughly 50%.

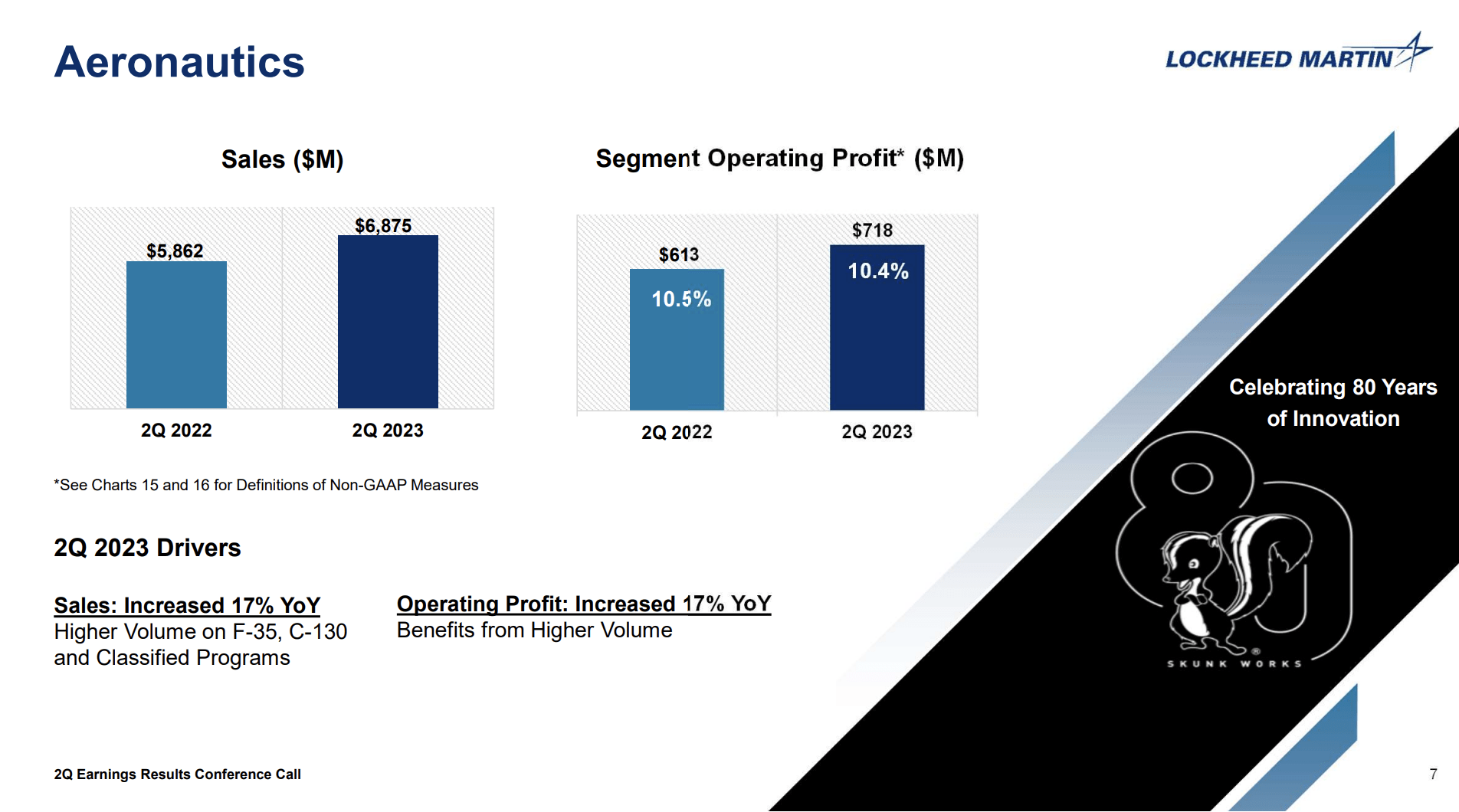

Lockheed expects to deliver 100 to 120 F-35 aircraft in 2023, and the supply chain and production system are on track to support the longer-term delivery outlook of 156 aircraft in 2025, which was not a certainty going into this year.

In general, the Aeronautics segment did very well, as sales improved by more than $1.0 billion, boosting operating profit to $718 million.

{kind=link}

Also, Skunk Works celebrated its 80th birthday. Skunk Works is currently partnering with NASA to develop and build the X-59, a prototype that aims to quiet supersonic booms and pave the way for supersonic commercial flights over land.

And speaking of anniversaries, Sikorsky, Lockheed Martin's rotorcraft helicopter division, celebrated its 100th anniversary. It continues to thrive globally, with achievements like the approval of foreign military sales to Norway and Spain for the MH-60 Romeo multi-mission helicopters.

Having said that, not only is the company benefiting from strong orders and easing supply chains in its Aeronautics segment, but it's also benefiting from strong demand for advanced missiles.

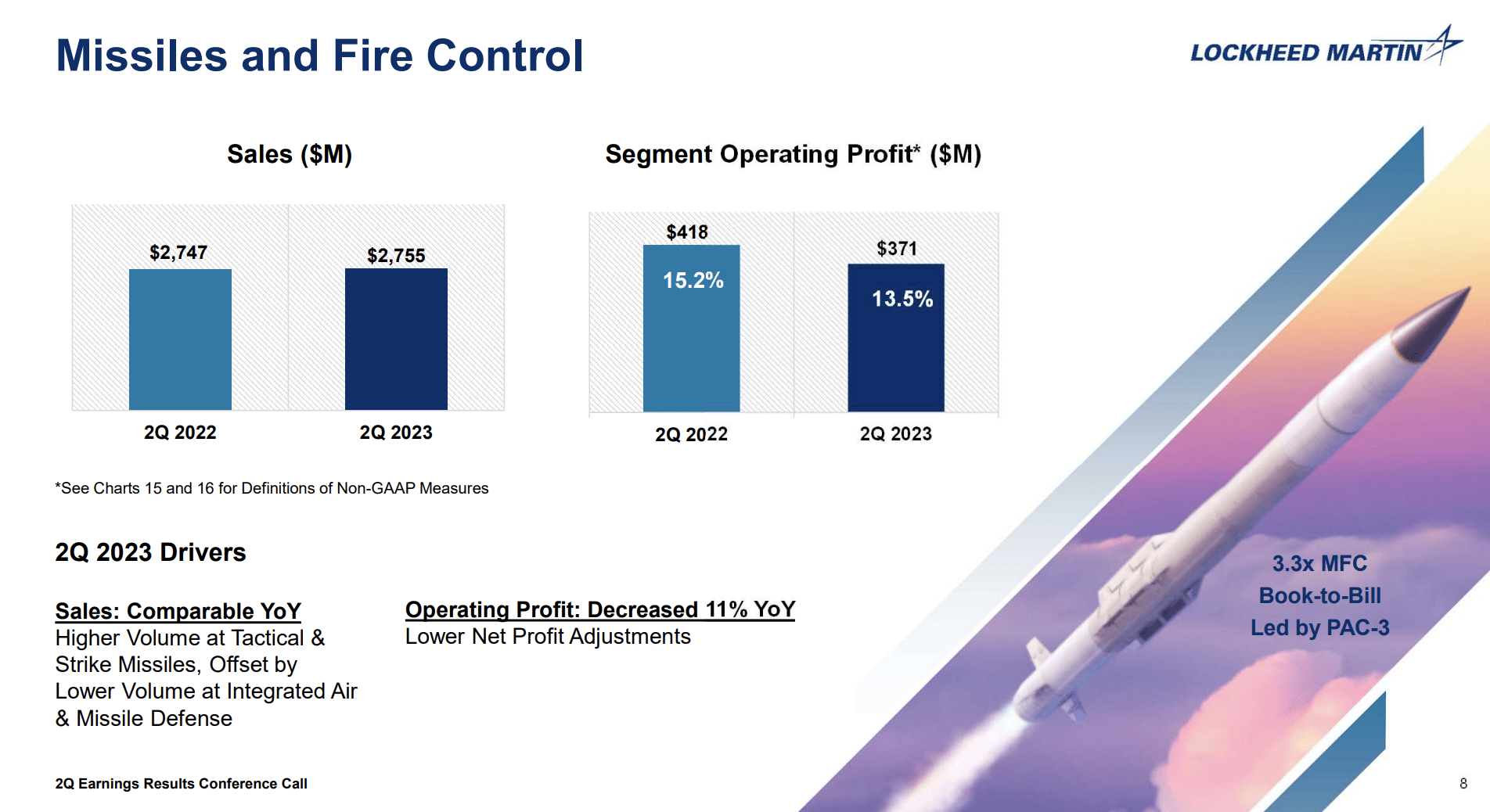

The Missiles and Fire Control segment saw higher sales volume on tactical strike missile programs but had to deal with lower volume within integrated air and missile defense.

Hence, segment operating profit and margins were down year-over-year, primarily due to lower net profit adjustments.

{kind=link}

However, we can ignore these numbers. Why? Because MFC managed to increase its backlog by $6.5 billion in the second quarter, driven by a record $9 billion of orders and a 3.3x book-to-bill ratio across key programs such as PAC-3, GMLRS, HIMARS, Javelin, and others.

In other words, the demand for advanced missiles is so high that demand is 2.3x higher than the company's ability to produce these missiles.

The reason for this is not what I had hoped for when I bought LMT a few years ago as the war in Ukraine requires a lot of missiles while NATO members are ramping up their own defense budgets. Because of high demand, the US is running out of ammo.

{kind=link}

As reported by the Wall Street Journal , Biden revealed in an interview with CNN that both Ukraine and the United States are running low on firepower. With Ukraine burning through 3,000 shells a day, the US Army plans to ramp up production to meet the demand, but concerns remain about America's ability to support a protracted war.

While Lockheed isn't necessarily the go-to place for standard artillery shells, the war in Ukraine is now requiring advanced missiles, as multiple nations are now supporting the delivery of long-range missiles.

So, not only were NATO nations already running behind their own defense plans, but now a lot of ammo will go to the war in Ukraine. Hence, I expect the demand for missiles to remain high on a prolonged basis.

And then if you look at the corpus of the Ukraine supplementals and what they're targeted for the overall amount has been $62 billion in 4 bills, the DoD we're going to Ukraine support. About 2/3 of that or $44 billion is for the purpose of restoring the presidential drawdown for the train of security assistance initiative, essentially, meaning the restocking of U.S. munitions. - James Taiclet, LMT CEO

Having said that, Lockheed also did very well in its Space segment.

{kind=link}

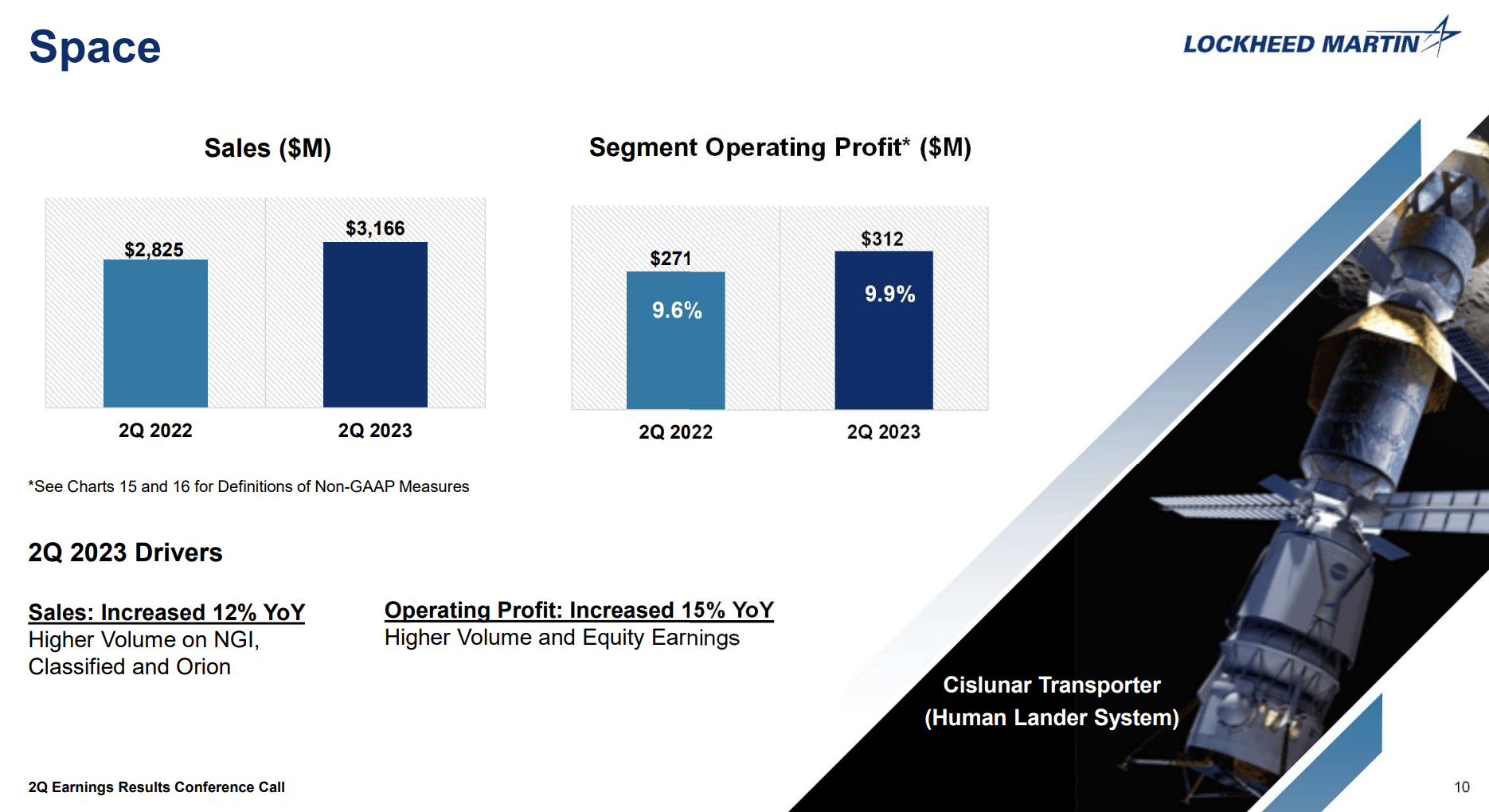

The Space business area witnessed a strong performance in the second quarter of 2023, with sales increasing by 12% year-over-year. This growth was driven by continued development activity on the next-gen Interceptor and classified programs, with additional upside from Orion.

Operating profit also increased by 15%, and margins improved by 30 basis points.

With all of this in mind, there was more good news for shareholders.

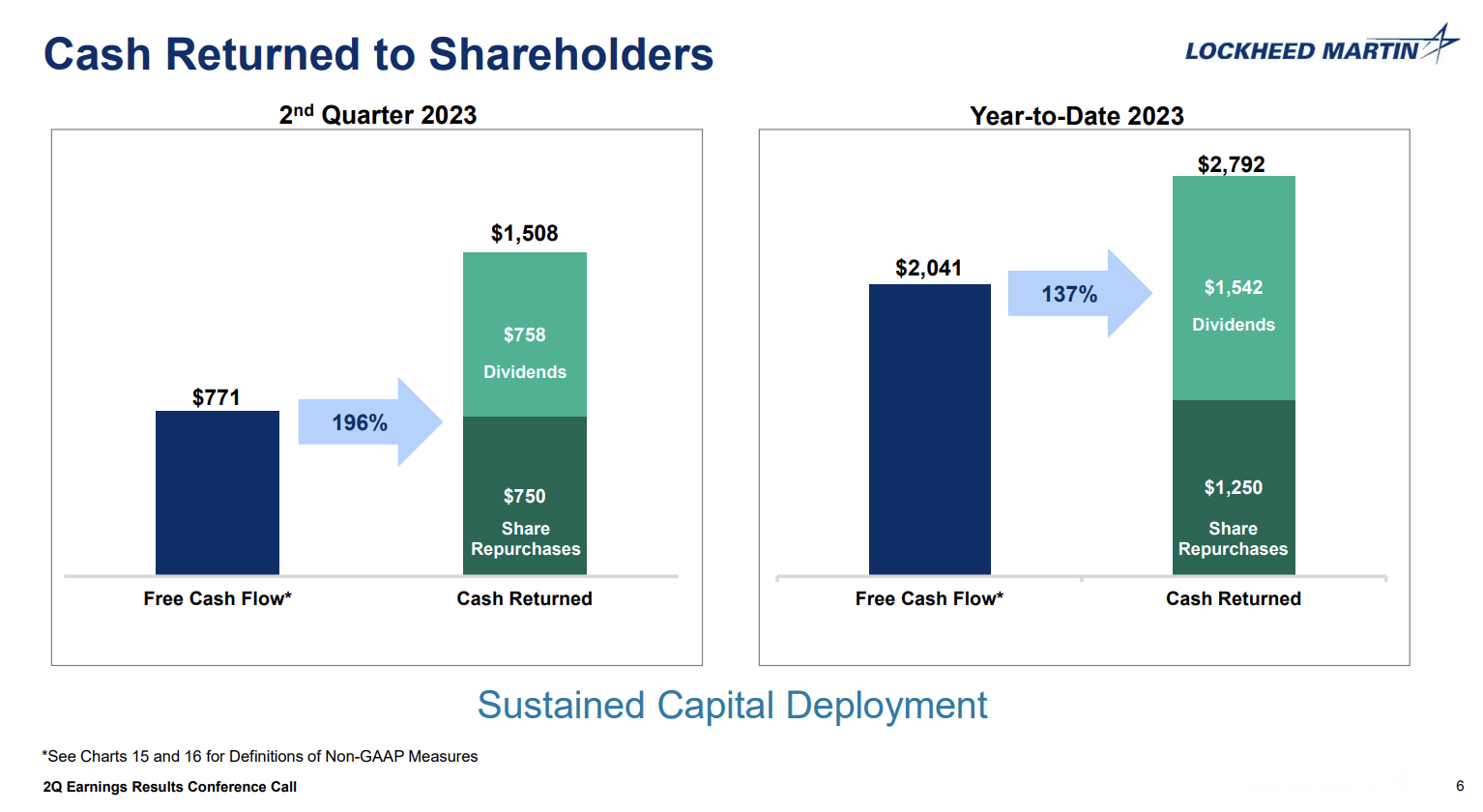

On the cash flow front, the company generated $771 million of free cash flow during the quarter, with roughly $330 million spent on capital expenditures.

It's worth noting that the free cash flow included $330 million of higher tax payments from the R&D capitalization legislation compared to the previous year, which is a temporary issue.

Despite this, the company remained committed to rewarding shareholders, as dividends and share repurchases exceeded free cash flow, totaling almost $2.8 billion or 137% of free cash flow for the first half of 2023.

Now, I know that some people will say that this isn't sustainable. However, note that free cash flow had a temporary setback and that growth is expected to accelerate. If the company wasn't confident, it wouldn't buy back more than $1.2 billion in stock.

{kind=link}

Additionally, the company issued $2 billion of debt across three tranches for a weighted coupon of 4.8%, mainly to provide flexibility and coverage during the debt ceiling negotiations.

The company enjoys an A- credit rating with a stable outlook.

Valuation

I believe that LMT shares are attractively valued. The company is trading at 13.4x NTM EBITDA and 17.8x 2024E free cash flow.

The company currently has a $509 consensus price target, which is 11% above the current price. I agree with that target.

Also, as I wrote in my prior article :

After that, I believe longer-term annual total returns will be somewhere between 7% and 10%, based on the company's comments and my view on the bigger picture.

Needless to say, LMT will remain my largest position. I will add shares on any meaningful correction as I believe LMT is one of the best ways to generate long-term wealth.

Takeaway

In conclusion, Lockheed Martin continues to impress as a dividend gem with significant shareholder benefits. The company's solid dividend scorecard, 20 consecutive years of dividend hikes, and substantial buybacks add to its allure.

The just-released earnings revealed impressive results, with record-breaking orders, good margins, and easing supply chain bottlenecks.

Lockheed's confidence in future growth is driven by rising demand for defense equipment and services and positive developments in its Aeronautics and Space segments.

Despite temporary setbacks in the Missiles and Fire Control segment, the high demand for advanced missiles indicates a promising future.

Moreover, LMT's strong cash flow and commitment to rewarding shareholders through dividends and buybacks further support its growth potential.

With an attractive valuation and a consensus price target suggesting an 11% upside, I remain highly optimistic about LMT's long-term prospects and will continue to view it as my top investment choice.

For further details see:

Dividend Growth: Lockheed Martin Is My Largest Investment For A Reason