CA - Dollarama: Long-Term Compounder With Growth Ahead

2023-09-12 07:31:32 ET

Summary

- Dollarama's business model is strong, with significant barriers to entry and a wide range of affordable products, positioning it well in the Canadian market.

- The company has seen impressive financial performance, with high margins and over 600% share price return in the last decade.

- Dollarama's aggressive expansion strategy and ability to adapt to trends, such as e-commerce, contribute to its competitive advantage and potential for continued growth.

Investment Thesis

Our current investment thesis is:

- Dollarama Inc.'s ( DLMAF ) business model is strong, giving it an unrivaled position in Canada and sufficient barriers to entry to maintain its current trajectory. The company offers significant choice, an attractive price, and convenient access through footfall and e-commerce.

- Financial hardship, continued high store growth, and the optionality of LatAm growth give the business a good basis to maintain its current trajectory.

- Dollarama's margins are incredibly, substantially above many of its peers. This has allowed the business to reinvest and fund substantial shareholder returns, driving a >600% share price return.

- Dollarama's valuation is punchy but with no evidence of a slowdown and continued quarterly strength, we consider the stock a buy.

Company Description

Dollarama is a Canadian retail company headquartered in Montreal, Quebec. Founded in 1992, Dollarama has grown to become one of Canada's leading discount retailers. It operates a chain of retail stores that offer a wide range of consumer products, general merchandise, and everyday essentials, all priced at attractive dollar store rates. The company also owns a majority stake in Dollarcity, which operates in LatAm.

Share Price

Dollarama's share price performance has been magnificent, returning over 600% to shareholders in the last decade. This is substantially higher than the wider market and a reflection of the company's strong financial performance and lucrative shareholder returns.

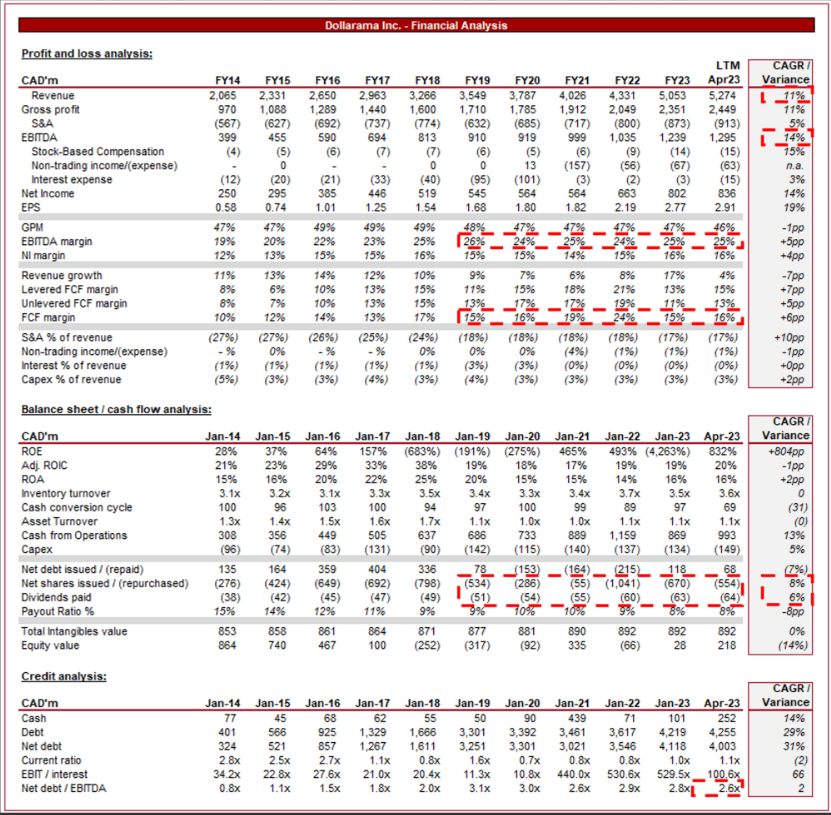

Financial Analysis

Dollarama Financials (Capital IQ)

{kind=link}

Presented above are Dollarama's financial results.

Revenue & Commercial Factors

Dollarama's revenue has grown extremely well, with a CAGR of 11% into the LTM. During this period, growth has been consistent, with no single fiscal year of growth below 6% (even during the pandemic).

Business Model

Dollarama's primary value proposition is offering a wide range of everyday products at extremely low prices and with the optionality of bulk. By maintaining a low fixed price point, it attracts price-conscious consumers looking for affordable alternatives to everyday items.

Dollarama's stores carry a diverse selection of products, including household goods, food and snacks, cleaning supplies, toys, seasonal items, health and beauty products, and more. This wide range caters to various customer needs, making it a one-stop shop for bargain shoppers. Dollarama's focus is on a particular demographic rather than specific items and so this broad product approach resonates well, allowing the company to increase its sales.

Dollarama stores are typically small and located in easily accessible areas, such as strip malls and urban centers. This format helps keep operating costs low and ensures convenient shopping for customers.

The company offers a significant number of private label brands, which is how prices are kept low, acknowledging that its demographic cares more about price than brands. Further, these brands often have higher profit margins than branded products, allowing Dollarama to maximize its profitability.

Dollarama maintains a highly efficient supply chain, which includes direct sourcing from manufacturers and distributors. This is a critical success factor for the business, as it allows Dollarama to keep procurement costs low and maintain consistent inventory levels.

Dollarama has pursued an aggressive expansion strategy, continually opening new stores across Canada. The company continues to reach underserved markets and increase its market presence. In the most recent quarter, Dollarama opened a net 21 new stores in Q1 (compared to 10 in the prior year). The company is targeting 2,000 stores by 2031, a further 500 from its current position.

Affordable Retail Industry

Dollarama faces competition from other value retailers, discount supermarkets, and e-commerce platforms. The company's substantial scale across Canada has reduced the impact of this, as illustrated by its impressive growth rate. We struggle to see its competitive position deteriorating in the medium term.

As online shopping continues to grow, driven by the benefits of convenience, Dollarama has invested in its e-commerce capabilities to remain relevant. This transition has been relatively successful and far better than many of its global peers, who have felt the business model does not translate well. For this reason, the risk has been broadly mitigated in our view, with Dollarama now benefiting from this trend by increasing its access to consumers.

Competitive Positioning

We consider the following factors to be key competitive advantages:

- Consumer Value - Dollarama's core value proposition of offering products at low prices resonates with cost-conscious consumers, especially during economic downturns.

- Convenience - The convenience of finding a wide array of products at a single location drives foot traffic to Dollarama stores.

- Private Label Success - Dollarama's private label brands offer cost-effective alternatives to national brands, contributing to higher profit margins.

- Store Expansion - Aggressive expansion into both urban and rural areas has allowed Dollarama to capture a larger market share and maintain a dominant position in Canada.

- Adaptation to Trends - Dollarama has shown its ability to adapt to changing industry dynamics successfully. For example, the need to increase prices and respond to the e-commerce trend.

Economic & External Consideration

Current economic conditions present an opportunity to broaden its current market size. With an extended period of high inflation, as well as the current elevated rates in Canada, many consumers are struggling with living costs. This has only been compounded by the rapid increase in home prices across major cities. This will inevitably lead to a rise in consumers "trading down" to more affordable retailers, positioning Dollarama well to capture this segment.

In its most recent quarter, Dollarama performed extremely well, illustrating this. The key takeaways are:

- Sales growth of +20.7%, with comparable store sales up +17.1%. This is an impressive performance and reflective of resilient demand and successful pricing action.

- EBITDA growth of +22.1%, illustrating margin accretion through its position revenue development.

Economic factors, including inflation and supply chain disruptions, have impacted the company's ability to maintain its low price points, contributing to the introduction of a new price structure (up to $5). This was announced in March '22 and will be rolled out across FY23 and FY24. Thus far, Dollarama's GPM has declined 1% but at an EBITDA and NIM level, this is not the case. For this reason, there is the potential for margin improvement following this strategic decision. Our expectation is for quarterly results to remain robust, although not necessarily at the growth rate achieved here.

What has the potential to restrict revenue growth is economic development, with GDP growth expected to be poor , particularly when compared to other developed nations. Canada's economy has grown well in the last 2 decades, which has supported Dollarama's financial performance.

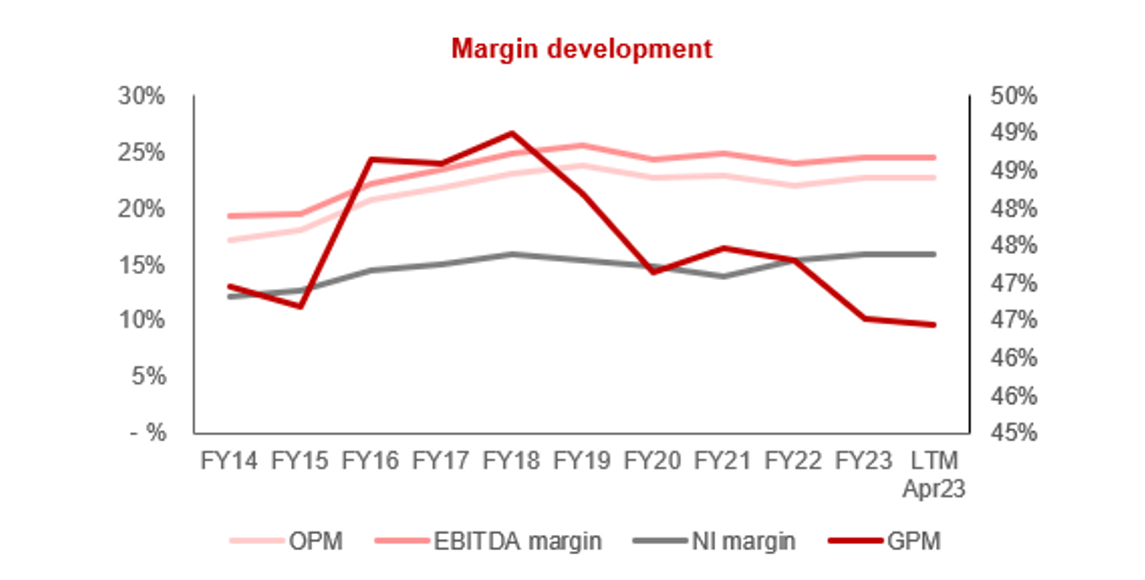

Margins

{kind=link}

Despite some variability in GPM, Dollarama's margins have broadly improved over the last decade, driven by operational improvements and scale benefits. Sustaining this trajectory is likely unrealistic but given the company's size and competitive positioning, we believe these levels are broadly maintainable.

Balance Sheet & Cash Flows

Dollarama's balance is incredibly clean and further illustrates the well-oiled machine that is this company. Inventory turnover has gradually improved, contributing to FCF gains in line with profitability. Further, debt usage is minimal due to cash generation, maximizing NIM.

This has allowed Dollarama to aggressively distribute to shareholders, with an 8% growth rate in net shares issues and a 6% rate in dividends. This has contributed to a 32% decline in diluted outstanding shares. All evidence points to this being sustainable.

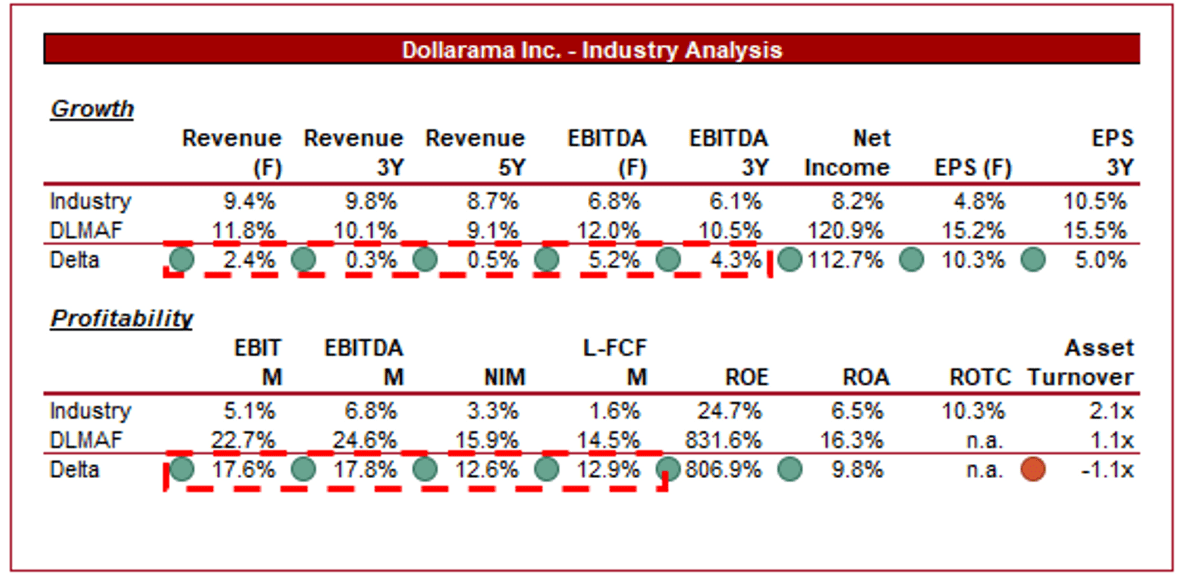

Industry Analysis

Hypermarkets and Super Centers Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Dollarama's growth and profitability to the average of its industry, defined as "Hypermarkets and Super Centers" as per Seeking Alpha's tool (10 companies).

Dollarama performs exceptionally well, with strong growth in profitability and a comparable revenue performance. Further, its margins are substantially higher than the industry average, illustrating its dominance over the industry in Canada relative to the higher competition in the US.

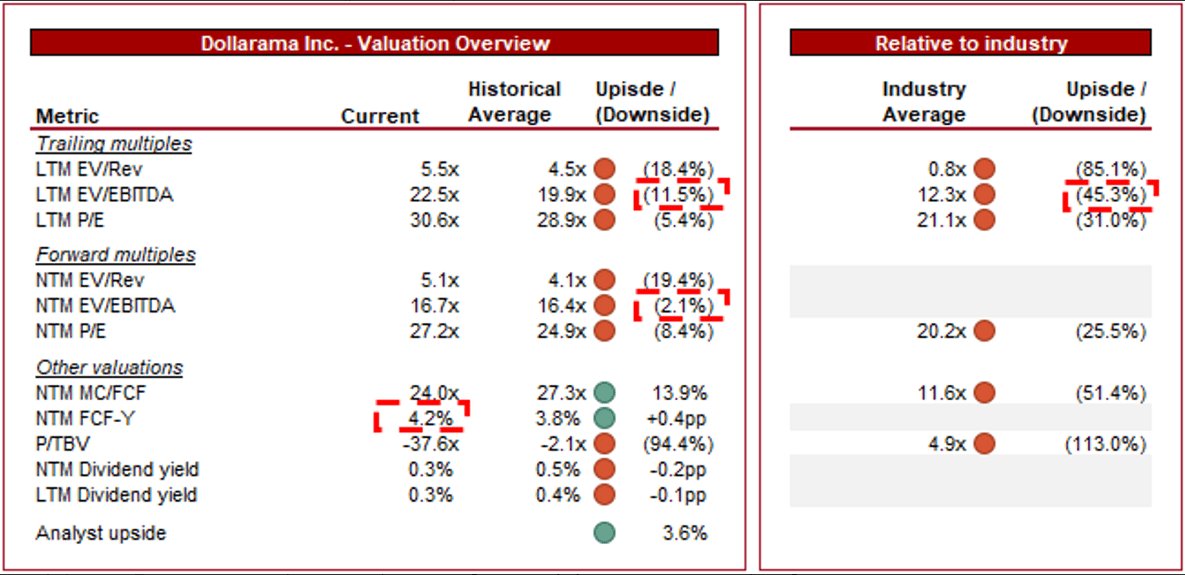

Valuation

{kind=link}

Dollarama is currently trading at 23x LTM EBITDA and 16x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is justifiable in our view, owing to the company's margin improvement, response to changes in industry dynamics, and its further scope for growth. The current premium feels slightly below fair value in our view, as illustrated by the above-average NTM FCF yield, which is now 4.2%.

Further, a premium to its peers is also reasonable, owing to its substantial FCF superiority and comparable growth. Long term, Dollarama is positioned to at least match growth (and maintain margins) given its competitive advantage in Canada and exposure to LatAm, even if the Canadian economy is unable to match the US in growth.

Broadly, we consider the company slightly undervalued, owing to the improvement in FCF yield.

Final Thoughts

Dollarama is a classic example of a boring business doing incredibly well. Its business model is not fancy but it is incredibly attractive to consumers. Its pricing structure, choice, and physical footfall/e-commerce platform position the company to be the perfect choice for millions of Canadians.

Underpinning this is strong execution from Management, responding to various trends, optimizing Dollarama's operations, and remaining focused on achieving growth. We see scope for a continuation of its current trajectory, with a growth rate of 6-9% appearing reasonable.

Dollarama is not cheap at a 45% premium to its peers but a deep dive of the business has shown this is reasonable. We consider the stock a long-term buy.

For further details see:

Dollarama: Long-Term Compounder With Growth Ahead