MSFT - Don't Sleep On Akamai's AI Potential

2023-07-05 15:01:44 ET

Summary

- Akamai's stock has reversed its losses from earlier this year after delivering impressive first quarter results, supported by an improved roadmap for its growth strategy in security and compute.

- Yet, management remains conservative on the company's AI prospects, despite the mission-critical role Akamai solutions will play in the development, deployment and usage of related technologies.

- While management has remained tight-lipped on how Akamai Connected Cloud plans to incorporate AI, the company is well-positioned to monetize from related opportunities.

- Akamai remains a potential AI play on our watchlist, as relevant developments across the security, compute, and delivery businesses could catalyze an upward valuation re-rate for the stock, buoyed also by a solid balance sheet and self-sufficient, cash flow positive operations.

Akamai's stock (AKAM) has rallied more than 25% since bottoming in mid-March after management's decision earlier this year to double-down on compute investments for 2023 raised concerns over the potential neglect of opportunities in security, which taken together would drive an imbalance to its risk profile. Yet, Akamai's robust beat and raise for the first quarter reported in May has propped up investor confidence in the stock so far, with management also providing greater clarity on the company's strategic roadmap for scaling its security, content delivery network ("CDN") and compute businesses going forward.

Specifically, first quarter results and management's guidance for the current quarter and full year 2023 provided confidence in Akamai's value proposition as it deepens its foray within the increasingly competitive cloud-computing industry. Meanwhile, Akamai's recent acquisition of Neosec , which specializes in "API detection and response… based on data and behavioural analytics", underscores continued discipline in opportunistic M&A activities focused on complementary assets to its existing leadership in web security (e.g. web application firewall; application and API security; bot management solutions), which would reinforce the company's commitment to restoring reacceleration in the segment. Its CDN business is also benefiting from normalizing demand trends following an abrupt post-pandemic economic slowdown, among other favourable industry trends.

While execution risks remain on how these clarified strategies will play out, the improved visibility on Akamai's growth and margin expansion roadmap, alongside first quarter outperformance have lifted sentiment in the stock nonetheless. Yet, we think there remains conservatism in the market over Akamai's prospects in capitalizing on emerging incremental generative AI opportunities across security, compute and CDN. Looking ahead, we expect consistent delivery of positive progress on the company's long-term growth roadmap for its security, CDN and compute businesses, alongside a deepening reach into the emerging generative AI growth frontier, to be value accretive factors capable of narrowing the stock's valuation discount at current levels relative to peers exhibiting a similar fundamental profile.

Generative AI in Security

Despite deceleration in Akamai's security revenues in recent quarters, dragged down primarily by softness in demand for its enterprise-focused solutions, the segment currently generates the bulk of the company's consolidated sales at a 44% share mix.

Specifically, Akamai's ability to gain share in enterprise security with its Zero Trust portfolio of solutions - including Zero Trust Network Access ("ZTNA"), multi-factor authentication ("MFA") to replace traditional virtual private networks ("VPN"), micro-segmentation to replace legacy network firewalls, and Secure Web Gateway ("SWG") to offer protection "against malware and phishing attacks" - remains lacking. Yet, management remains optimistic that the continued integration of Guardicore - a security firm, specialized in micro-segmentation, which Akamai had acquired in late 2021 - will become a core differentiating factor for improving the company's capture of opportunities stemming from enterprise security. In the meantime, its foray in web security continues to gain market share, bolstered by Akamai's recent acquisition of Neosec which is expected to expand its growth opportunities in the burgeoning market for API security:

Last year saw a record number of web app and API attacks more than double the number in 2021. The rapid rise in API attacks is becoming a critical challenge for enterprises across all verticals and with IDC and Gartner now projecting the API security market to exceed $1 billion by 2027.

While Akamai's security business has been experiencing slowing growth in recent quarters, underperforming an industry that has remained a relatively resilient corner in software amid macro-driven uncertainties in the enterprise IT spending environment, management has recently reiterated optimism that the first quarter represented a "trough in growth" for the segment, with expectations for reacceleration going forward. This is in line with management's full year guidance for security revenue to expand by a low double-digit percentage exiting 2023, albeit still being far from growth in the 20% range observed just a year ago.

We expect the continued integration of AI capabilities across its security portfolio to bolster the segment's growth prospects ahead of favourable secular trends. For instance, Neosec's API security platform "leverages AI-based behavioural analytics" to drive detection, analysis, and identification of vulnerabilities, ensuring the delivery of timely and cost-efficient defense against cybersecurity attacks for customers. The optimized cost and performance advantages enabled by the integration of AI capabilities via Neosec are expected to further Akamai's market leadership in the provision of application and API security solutions, and better take advantage of secular demands in the industry. Specifically, accelerating digitization efforts across the industry mean increased exposure to the use of APIs, applications, and other cloud-based solutions vulnerable to elevated cybersecurity threats. And this underscores why security is a key component of the API management cycle as identified by research firm Gartner:

Full life cycle API management software enables organizations to discover, design, develop, manage and secure APIs…The number of APIs within organizations is growing rapidly in IT departments and lines of business. APIs form the connection points between platforms and ecosystems. Every connected mobile app, every website and every application deployed on a cloud service uses APIs…The full life cycle API management market grew by 26.7% in 2021, to $2.7 billion, despite a challenging year. It remained the third-fastest growing segment of the application infrastructure and middleware market…Gartner expects this market to continue to register strong double-digit growth for at least the next five years.

Source: Gartner

In addition to incremental market share gains, the rapid adoption of generative AI technologies is also expected to drive incremental demand for cybersecurity solutions, bolstering tailwinds for the industry. Specifically, the budding subfield of AI is expected to "make attacks more sophisticated" and simplify the process for hackers to breach cybersecurity guardrails. More than 60% of organizations have been subject to a "ransomware attack in the past 18 months", encouraging more than 38% of global corporations to identify cybersecurity improvement as a top investment priority. The bullish demand environment is expected to drive the global cybersecurity market into a $300+ billion opportunity over the next five years, representing expansion at a compounded annual growth rate of 14.5%, marking strong tailwinds for Akamai's increasing prominence in API security and emerging strength in enterprise security.

Generative AI in Compute

Generative AI also represents an incremental tailwind for Akamai's aspirations to gain share in the cloud-computing market, despite its late entry. Recall that the company has been doubling down on its compute strategy in recent quarters. Instead of competing directly against hyperscalers like Amazon's AWS ( AMZN ), Microsoft's Azure ( MSFT ), and Alphabet's Google Cloud Platform / GCP ( GOOG / GOOGL ), Akamai aims to be a supplementary cloud vendor for "workloads with less need for up-the-stack functionality", while offering competitive pricing as a differentiated value proposition. We believe this strategy is expected to bode favourably for Akamai amid growing optimization and multi-cloud adoption trends in the industry.

Specifically, cloud spend optimization has become a top priority for enterprise end markets, which makes Akamai's competitive pricing structure a key appeal to existing and prospective customers. The company is able to leverage existing infrastructure shared by its security and CDN businesses to drive its compute operations, effectively realizing cost savings that can be passed on to customers. One of these cost benefit areas is on egress fees. While companies are typically charged hefty egress fees on transferring large amounts of data, Akamai's expansive server and points of presence ("PoPs") footprint can reduce related spending for its compute customers. With more than 4,000 PoPs and 350,000 servers worldwide , Akamai's compute capacity enables data to "sit as close to the end user as possible", making it less expensive for customers.

Akamai intends to offer the world's most distributed platform placing compute, storage, databases and other cloud services closer to end users and enterprise data centers.

And by focusing on hosting less complex workloads, Akamai positions itself well for growing enterprise adoption of multi-cloud strategies. In a recent sentiment check survey performed by RBC Capital Markets, close to 90% of corporations that have begun their respective transitions to the cloud have indicated the use of "multiple public cloud providers", while more than half are using "three or more". While leading hyperscalers like AWS and Azure are typically the preferred primary public cloud vendors for enterprises of all sizes, late entrants and niche players - like Akamai - with a differentiated value proposition stand to benefit from growing enterprise adoption of multi-cloud strategies, given benefits that include "risk mitigation, reliability/redundancy, multi-function availability, and most importantly, cost-efficiencies".

In addition to tailwinds stemming from the shift in enterprise cloud strategies, the advent of generative AI is also expected to drive incremental cloud TAM, bolstering prospects for Akamai's compute ambitions ahead. Specifically, generative AI is expected to expand the TAM for cloud-computing by driving incremental demand for compute capacity to facilitate both the development and training of large language models, as well as the deployment of related applications.

And Akamai's continued build out of the Linode data centers to enhance its "enterprise-grade" solution offered through Akamai Connected Cloud will be critical to ensuring the company's adequate capture of incremental demand tailwinds from generative AI, multi-cloud and optimization trends, and drive accelerated growth.

…we are looking to leverage the Linode cloud computing services for enterprise customers by building new enterprise-grade core and distributed sites and connecting them to the Akamai backbone, which we believe will give Akamai an advantage over its bigger cloud rivals".

Source: Akamai 2022 10-K Filing

Recall that the Linode cloud computing platform was acquired by Akamai last year to complement its efforts in making compute a key growth frontier for the company. Akamai is currently aiming to "double the number of Linode data centers, targeting three next quarter, [and become] enterprise-ready by the middle of 2024".

Akamai Connected Cloud links Linode's 11 core data centers with Akamai's 4,100 edge computing locations. In addition, we're in the process of building out 14 more core enterprise scale data centers with at least 3 expected to come online in the next few months.

This is expected to further bolster growth prospects in the business going forward, in line with management's expectations for "approximately $0.5 billion in revenue from Compute in 2023", accelerating from the implied run-rate observed during the first quarter. And over the longer-term, an expanded enterprise-grade compute footprint is expected to drive "greater scale and lower cost for enterprise workloads", reinforcing Akamai's value proposition for its cloud strategy.

Generative AI in CDN

Although security has overtaken CDN as Akamai's core revenue generator, the latter remains a key business for the company. Despite declines observed over the past year, driven primarily by uncertainties in the IT spending environment amid macroeconomic weakness and in part "because of the war in Ukraine", the CDN business remains a profit driver for the company due to its expansive scale, which is key to sustaining growth investments in the security and compute businesses. And management expects improvements through the remainder of the year, with cautious optimism for the business to exit 2023 flat from the prior year given favourable trends observed in recent months - including "stronger traffic growth" and "vendor consolidation".

Specifically, Akamai is observing normalizing traffic levels with "more people streaming, gaming, and downloading software as well as 4K becoming more prevalent". This is expected to improve utilization of its expanding global network of server PoPs, especially as Akamai bolsters its market-leading share in servicing the gaming, media and entertainment, and e-commerce verticals, which are amongst the most popular cohorts of CDN usage.

But we do think we can be very competitive for certain kinds of applications, particularly in the verticals where we do a lot of business, the media vertical, entertainment obviously, video, gaming, commerce. And that's because those customers, they know us, they like us, they use us for the delivery and security.

Meanwhile, surging generative AI interest is expected to become a core immediate- to longer-term tailwind for CDN traffic trends. For instance, ChatGPT became the fastest growing online platform, acquiring 100 million monthly active users and more than 10 million daily queries on average during its first two months of availability to the general public. Considering the massive amounts of data needed to facilitate generative AI applications (e.g. ChatGPT), and the pervasive surge in usage of related technologies worldwide in recent months, CDNs have become more important than ever before to minimize potential delays in getting content up on user screens.

Specifically, CDN plays a mission-critical role in reducing latency in web data consumption by essentially serving as "secondary servers" spread across different locations from the "origin server" to keep content closer to the end-user, and "improve site rendering speed and performance".

To minimize the distance between the visitors and your website's server, a CDN stores a cached version of its content in multiple geographical locations (a.k.a., points of presence, or PoPs). Each PoP contains a number of caching servers responsible for content delivery to visitors within its proximity.

Source: imperva.com

Recall that Akamai has more than 4,000 server PoPs worldwide. And with the figure still expanding, the company is well-positioned to capitalize on incremental CDN growth opportunities stemming from the burgeoning interest in generative AI - not just in enterprise settings but also across mass market consumption of related technologies.

The CDN business is also coming off of tough PY comps where macro-driven weakness observed over the prior year lapped with accelerating usage during the pandemic era, which is expected to drive sustainable improvements to growth rates going forward. Akamai has also observed a meaningful extent of "vendor consolidation" in the CDN industry in recent quarters, which would benefit the company given its market leading reliability and competitive unit economics. Historically, CDN customers have had "four or five [vendors] that can get to be pretty expensive". As optimization trends continue to spread across enterprise digitization roadmaps, Akamai is well-positioned to benefit.

Fundamental Analysis

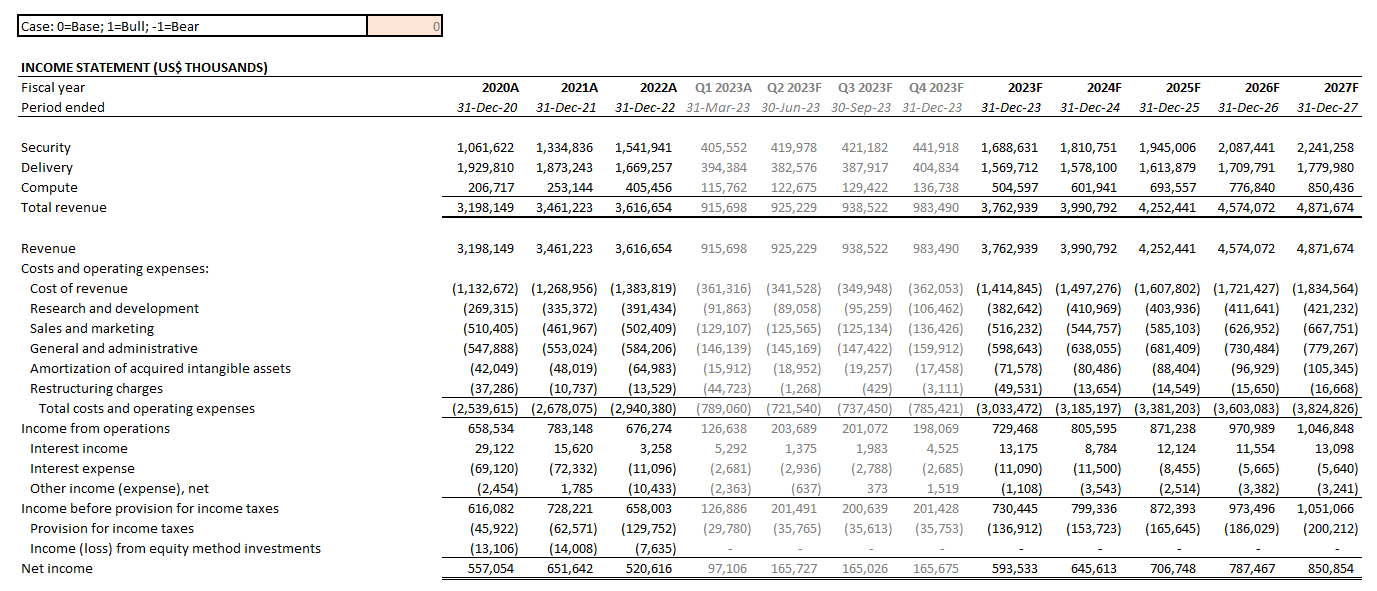

Considering the foregoing analysis on the current demand environment for each of Akamai's core compute, security and CDN business, as well as other operating considerations such as the improved go-to-market roadmap for compute and security and easing PY comps for the cyclical CDN business, the company remains on track towards management's guidance offered for the current period and full year 2023. The incremental boost of demand ensuing from the advent of generative AI is expected to further reinforce Akamai's prospects of achieving the 2% y/y to 4% y/y growth target for 2Q23 and 3% y/y to 5% y/y growth target for full year 2023, considering the mission-critical role of compute, security and CDN solutions in enabling the development, deployment and usage of AI technologies.

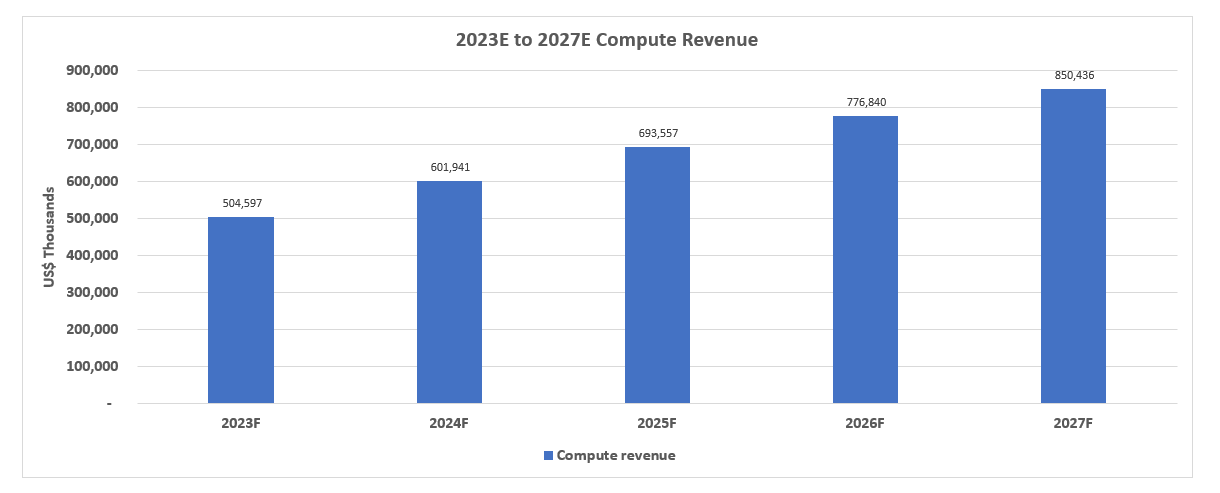

We expect Akamai's compute segment to remain a key beneficiary of incremental demand for cloud services stemming from burgeoning interest in generative AI. The segment is expected to expand by 16% y/y in the current quarter towards $122.7 million, and 24% y/y for full year 2023 to $504.6 million, in line with management's full year target for at least $0.5 billion in compute sales. And considering Akamai's increasing investments in building out its compute capacity to adequately capture longer-term secular opportunities in the industry, buoyed by its strategic focus on servicing less complex workloads stemming from multi-cloud adoption tailwinds, the segment is expected to expand at a low double-digit percentage CAGR through 2027 and grow its share of the company's revenue mix towards the high-teens range from the current low-teens range. This is expected to improve the emerging growth segment's scale, and contribute favourably to Akamai's longer-term margin expansion efforts back towards the 30%+ range.

{kind=link}

{kind=link}

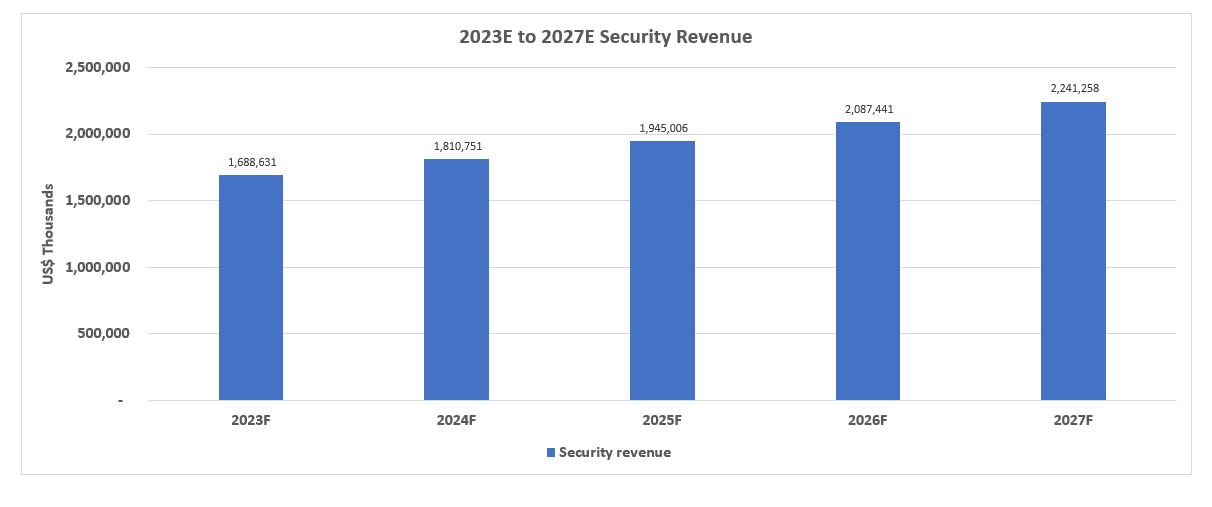

On the security front, we expect modest sequential acceleration through the year, helped primarily by strong demand in the API security market bolstered by both AI tailwinds and synergies from Akamai's integration of Neosec, offset by relatively softer reacceleration in enterprise security. This is in line with Akamai being still in early stages of integrating Guardicore and ramping up its foray in enterprise security, albeit positive signs backed by strong bookings growth during the first quarter, whereas its integration of Neosec would complement existing company expertise in API and web security. We forecast security revenue to expand by 10% for full year 2023 towards $1.7 billion. This is line with management's guidance for improvements from 6% y/y growth during the first quarter towards low double-digit y/y growth exiting 2023. And over the longer-term, the segment is expected to expand at a 6% CAGR through 2027, considering the niche security market and specific verticals (e.g. media) Akamai serves compared to its higher growth security software peers like Cloudflare ( NET ). The segment is expected to remain the biggest share of Akamai's revenue mix as the company continues to focus on security opportunities over the longer-term, alongside compute, as its legacy core CDN business matures.

{kind=link}

{kind=link}

As CDN comes off of acute cyclical headwinds observed in the prior year, supported by improved traffic trends exiting the first quarter with anticipated incremental demand stemming from AI interest, as well as a leadership advantage in capturing tailwinds from end-market vendor consolidation trends, and softer PY comps driven by the onset of macro-driven demand challenges at the time, the segment's revenue declines are expected to improve through the year. Specifically, CDN revenues are expected to decline 8% y/y during the second quarter, and exit 2023 in low single-digit declines, bringing full year 2023 contraction of the business at 6%. This is in line with management's cautious optimism about exiting the year flat in the CDN business, as traffic growth improvements are not yet at pre-pandemic levels:

Rudy Kessinger

…Anything in particular in the quarter that would give you hope that delivery maybe you could potentially turn that back to a, I don't know, say, a flat or maybe only a 3%-5% decline in business as opposed to a 10%-ish decline in business as we've seen over the last few quarters?

Ed McGowan

…I think if we get back to kind of pre-pandemic levels, that's certainly going to help…So the double-digit declines, I wouldn't expect that certainly next quarter or the quarter after that. And in Q4 is always the toughest quarter to call, but things will get -- should get a little bit better from a year-over-year compare standpoint. But in terms of getting to sort of flat or even plus or minus a point, you're going to need to see stronger traffic growth than what we're seeing now.

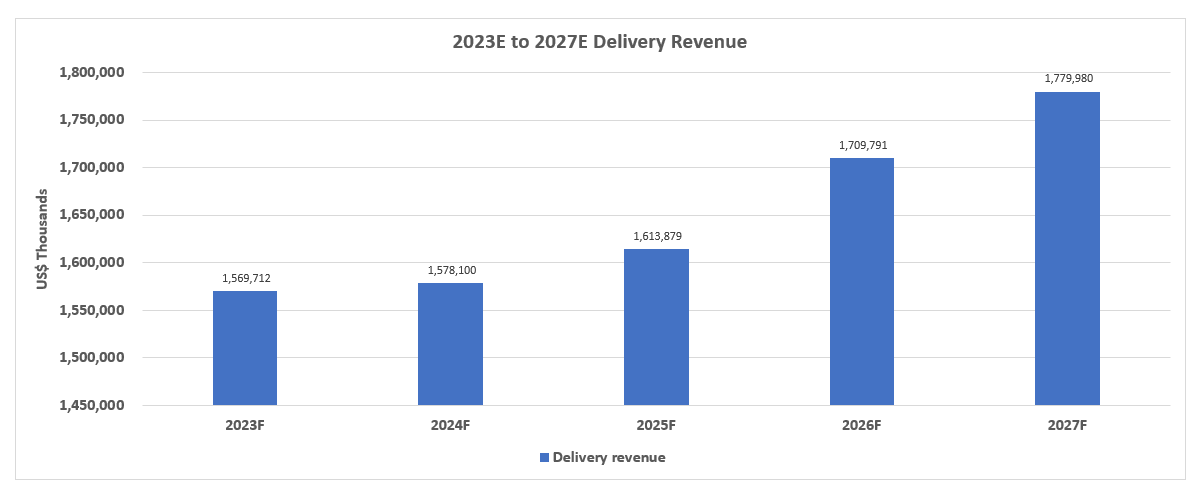

And over the longer-term, as market share gains in the delivery business restores traffic stability observed during the pre-pandemic days, the segment is expected to expand at a 3% CAGR through 2027 towards annual revenue of $1.8 billion. While the burst of interest in generative AI and related web applications could further catalyse TAM expansion and growth for the segment, we focus on near-term expectations for progress in the recovery of CDN traffic towards pre-pandemic levels, helped by additional momentum in the nascent technology trend, before turning more constructive on what lies beyond.

{kind=link}

{kind=link}

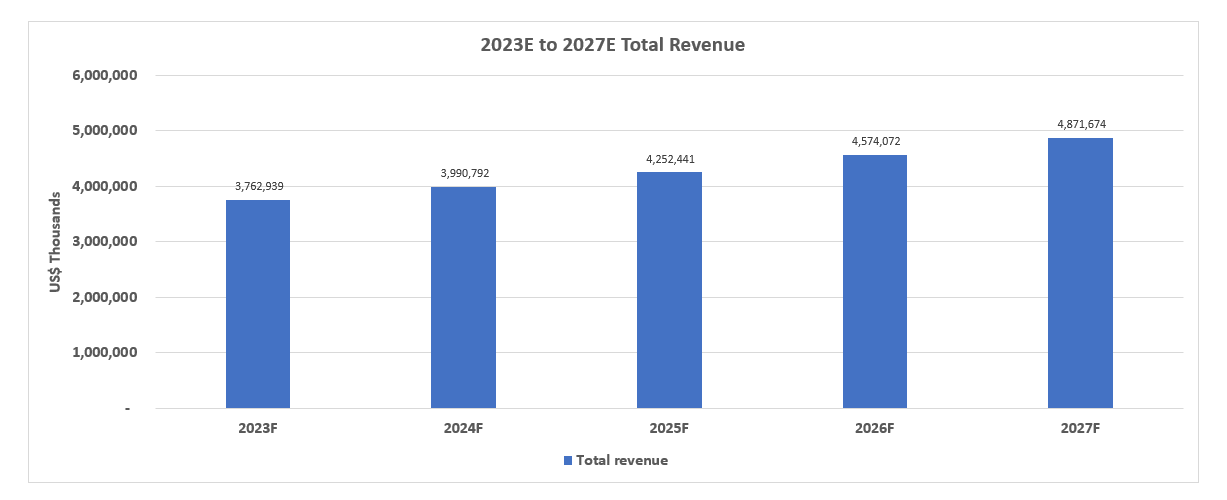

Taken together, we expect consolidated revenue to expand by 4% y/y towards $3.76 billion for full year 2023, which nears the midpoint of management's guidance. And over the longer-term, reacceleration would depend primarily on progress in ramping up market share gains in enterprise security via Guardicore integration to complement robust growth in API security. The ramp up of new compute capacity from the ongoing build out of Linode data centers will also be critical in driving revenue reacceleration at Akamai.

{kind=link}

{kind=link}

We expect the five-year CAGR to stay modest at 5% based on the foregoing segment analysis, with prospects for double-digit growth in the longer-term should generative AI tailwinds become more constructive at Akamai (e.g. announcements of generative AI-specific offerings, in addition from benefitting indirectly from accelerating AI interest). While Akamai's three core business groups are well-positioned to benefit from incremental demand given their mission-critical roles in facilitating the development, deployment, and absorption of AI services, management has yet to pull the lever on direct integration of related technologies across its portfolio of offerings, which could favourably alter the respective segments' growth potential.

Meanwhile, regarding considerations over Akamai's bottom-line, management's ambitions to bring gross margins back towards the 30% range will depend on the continued ramp up of growth investments - particularly in compute, which would improve utilization of existing server and other infrastructure shared across security and delivery. In the meantime, savings resulting from headcount reductions of approximately 3% earlier this year are expected to drive margin upsides in the "$40 million range" on an annualized basis, which management expects Akamai to "get about three quarters of the benefit of" through the remainder of 2023. As a result, we expect GAAP operating margins to improve from the teens back towards the 20% range exiting 2023, with further expansion driven by acceleration in core growth businesses over the longer-term.

{kind=link}

Akamai_-_Forecasted_Financial_Information.pdf

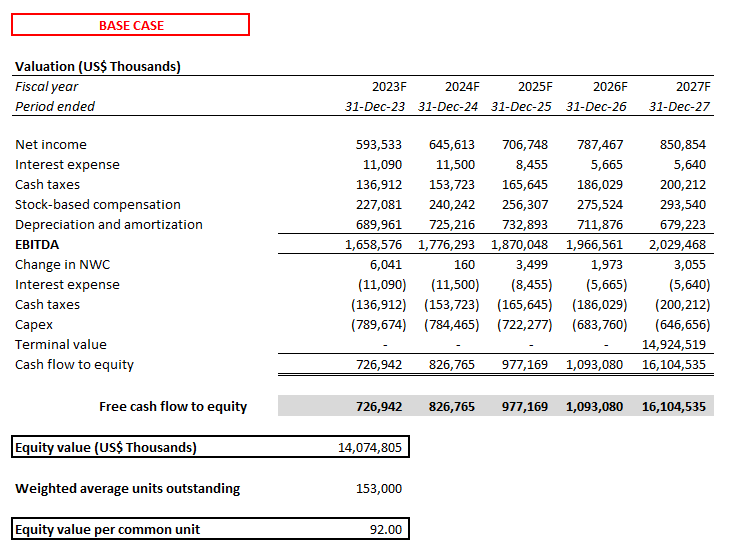

Valuation Analysis

{kind=link}

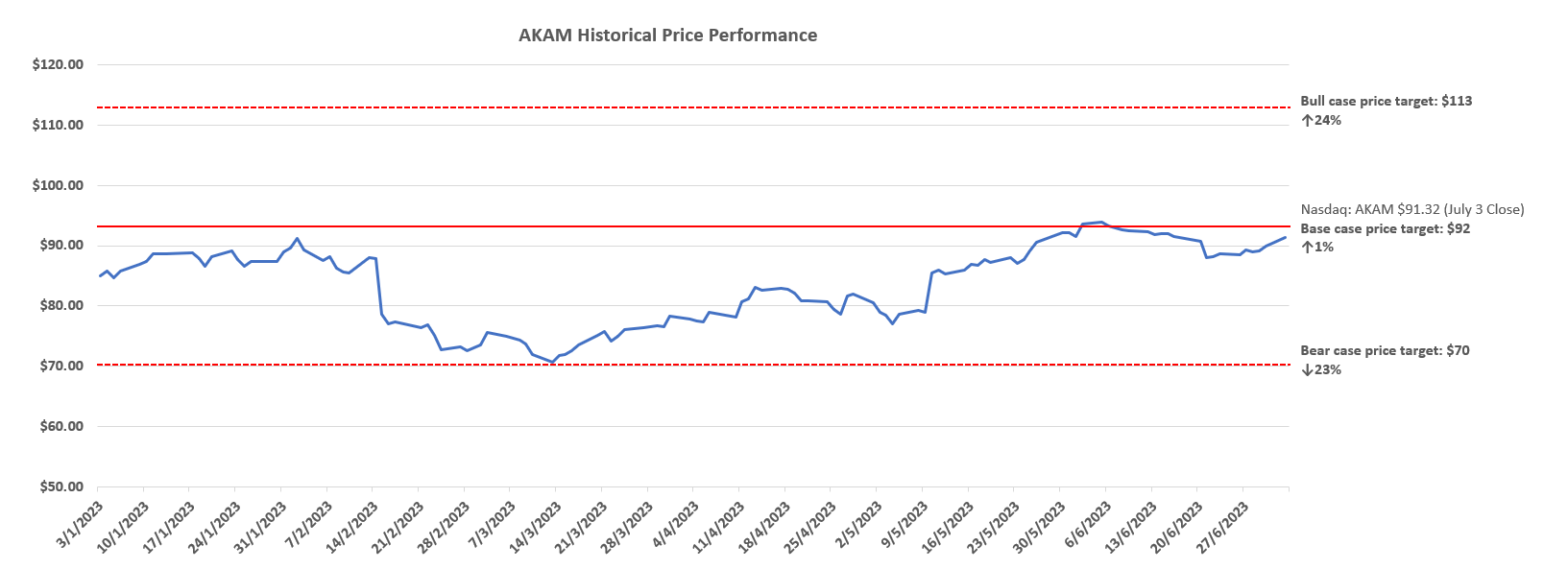

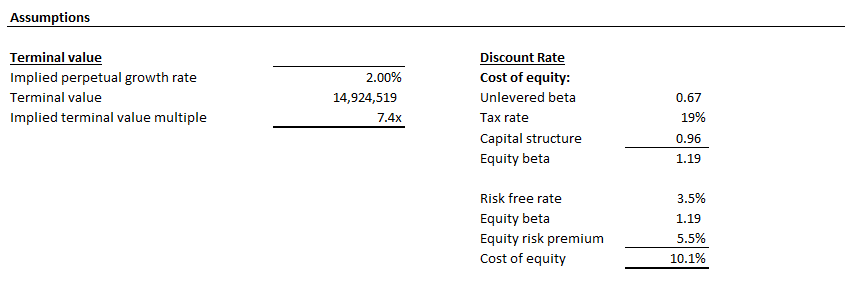

Based on the discounted cash flow ("DCF") analysis on projected cash flows taken in conjunction with our base case fundamental forecast for Akamai, with the application of a 10% WACC in line with the company's capital structure and risk profile, the stock's current price at about $91 apiece (July 3 close) implies a perpetual growth rate of about 2%.

The rate implies maturity in the low-growth tech name, and has likely yet to price in anticipated incremental growth stemming from AI-driven demand for security, compute and content delivery solutions, let alone additional opportunities should management pull the AI lever by integrating related technologies across its portfolio of offerings. But the stock at currently levels fairly reflects execution risks facing Akamai's ramp up of its growth businesses, namely security and compute, considering lingering macro sensitivities alongside competitive headwinds. This is also consistent with management's cautiously optimistic growth guidance for full year 2023 in the mid-single-digit range, reflecting a lack of conviction for a more constructive path towards double digit growth over the longer-term as targeted per last year's Analyst Day presentation.

{kind=link}

{kind=link}

Admittedly, management has given little airtime for AI, taking a conservative approach on Akamai's potential near-term benefits from burgeoning interest in the nascent technology. AI and related terms were only mentioned twice during Akamai's first quarter earnings call, referring briefly to Neosec's incorporation of AI in security analytics and indirect benefits of the emerging tech trend for Akamai Connected Cloud. While the stock's tepid valuation at current levels likely reflects market's digestion of the setback observed in Akamai's fundamental growth due to worse-than-expected macro challenges, compared to the optimistic double-digit three- to five-year CAGR guidance offered during last year's Analyst Day presentation , burgeoning interest in AI and ensuing TAM expansion across security, compute and content delivery could be the lifeline for restoring said optimism.

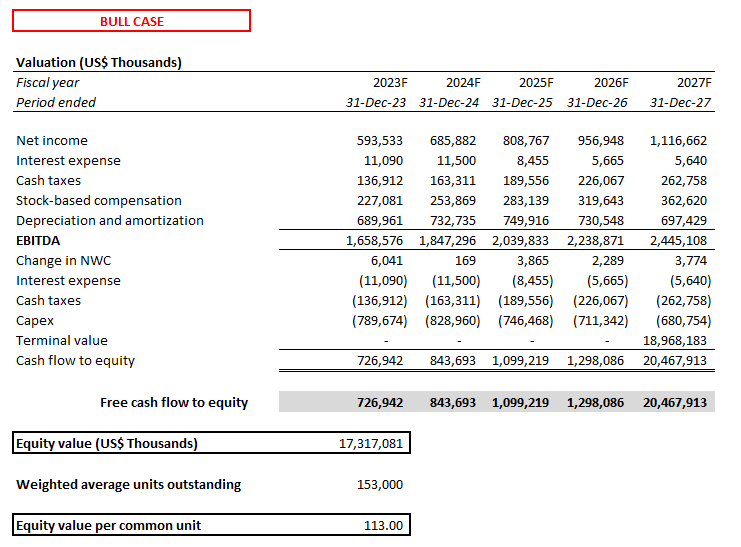

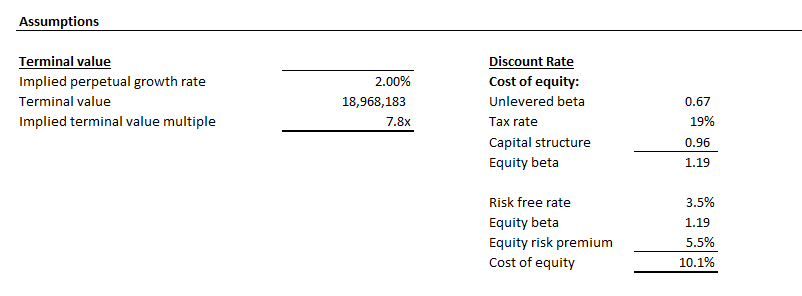

In the upside scenario, we estimate a 10% CAGR for total revenue through 2027, consisting of 25% CAGR for compute sales, 9% CAGR for security, and 3% CAGR for delivery sales, supported by constructive monetization of impending generative AI trends, while holding the cost structure constant from the base case. Under the DCF valuation approach, we are also keeping the base case perpetual growth rate of 2% and WACC of 10% unchanged, yielding a bull case price target of $113.

{kind=link}

{kind=link}

{kind=link}

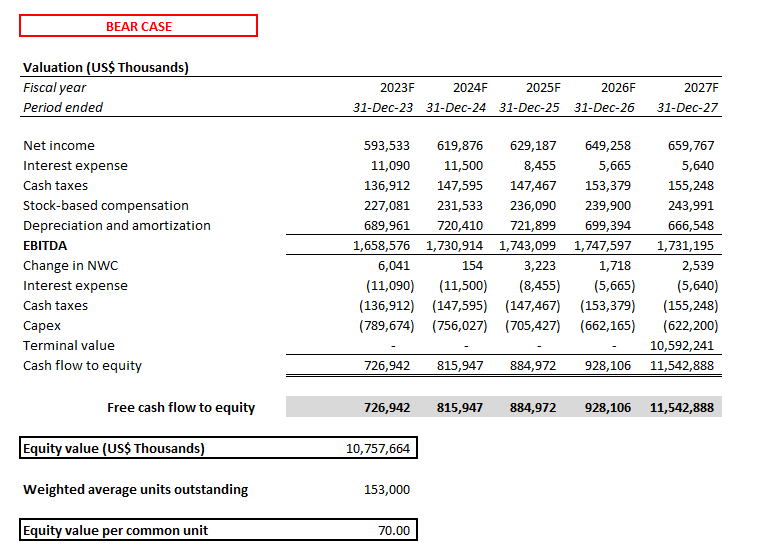

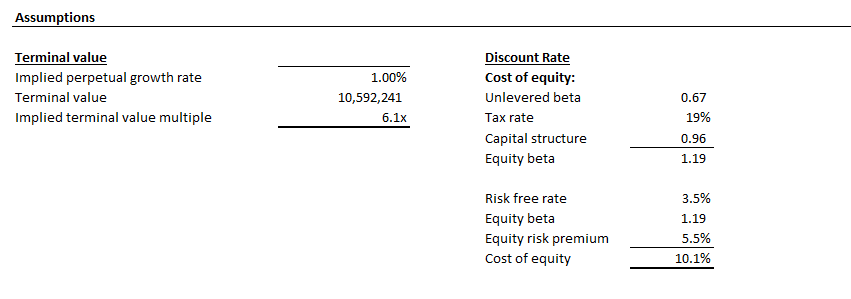

In the downside scenario, we estimate a nominal 1% CAGR for total revenue through 2027, consisting of modest security and compute sales expansion in the mid-single-digit range CAGR, and continued declines in delivery sales. This reflects continued market share losses in CDN, alongside less optimistic expansion for Akamai's key growth segments, security and compute. The bear case price is $70, applying a 1% perpetual growth rate to the DCF analysis, in line with assumptions for weaker growth prospects going forward, while holding the 10% WACC unchanged from the base case.

{kind=link}

{kind=link}

{kind=link}

The Bottom Line

We believe Akamai's forays in security, compute and content delivery are well-positioned to further monetize generative AI opportunities ahead, which has yet to become a consensus view given the stock's modest valuation at current levels relative to its software peers that have been more engaged in taking advantage of incremental demand stemming from the ancient technology. Admittedly, the stock at current levels continues to reflect execution risks to Akamai's growth aspirations in security and compute, despite a clarified roadmap on how it will offer a differentiated value proposition to overcome competition.

However, we remain optimistic in incremental pent-up value driven by generative AI-driven demand that has yet to be priced into the stock, with further upside potential should Akamai decide to incorporate generative AI technologies more directly across its portfolio of Akamai Connected Cloud solutions offered, as management had briefly mentioned during the first quarter earnings call:

We're working with customers in e-commerce, travel, hospitality, software as a service, media and entertainment to improve their ability to personalize experiences monetize content, accelerate data processing, facilitate collaboration, simplify management, improve performance and reduce costs, in some cases, by large amounts. And we're having early discussions about potentially leveraging Akamai Connected Cloud for AI inference engines. Each of these use cases plays to Akamai's advantage in terms of numbers of POPs, global reach performance and cost.

Looking ahead, we will continue to focus on potential generative AI tailwinds at Akamai, which could be additive to its forward prospects as the company propels forward with growth investments in security and compute. Burgeoning interest in the ancient technology, and Akamai's potential integration of related solutions to its portfolio over the longer-term could catalyse a new bullish narrative and unlock further upside to the stock from current levels.

For further details see:

Don't Sleep On Akamai's AI Potential