SNBR - Don't Sleep On Sleep Number's Potential Earnings Recovery

2023-12-27 14:18:07 ET

Summary

- Sleep Number manufactures and sells beds at a high price point, including smart capabilities through a mobile app.

- The company has faced challenges with decreasing demand and supply chain issues, along with a likely weakly perceived new product line relaunch.

- Sleep Number has a number of initiatives to improve earnings, including closings of 40-50 stores, and supply chain & marketing spend optimization.

- A financial recovery isn't priced into the stock fully, as my DCF model estimates a good amount of upside despite the recent stock rally.

Sleep Number ( SNBR ) manufactures and sells mattresses, beddings, pillows, and beds. The company brands its offering as a Smart Bed, as the company has a mobile app for its bed. The app provides insights into sleep quality, health, as well as options to adjust the bed’s settings. As can be expected from the features, most of Sleep Number’s products are priced high with custom configurations for beds going up to five figures in price.

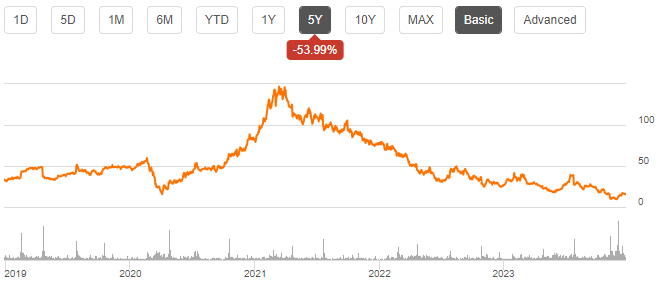

The company has struggled with decreasing demand after the pandemic’s positive effect subsided, as well as very significant supply chain issues deteriorating earnings. As a result, the stock has fallen nearly 90% from the 2021 high into the current level. More recently, the stock seems to have started a recovery, as the one-month return is 59% at the time of writing.

{kind=link}

Financial Hibernation After Constant Growth

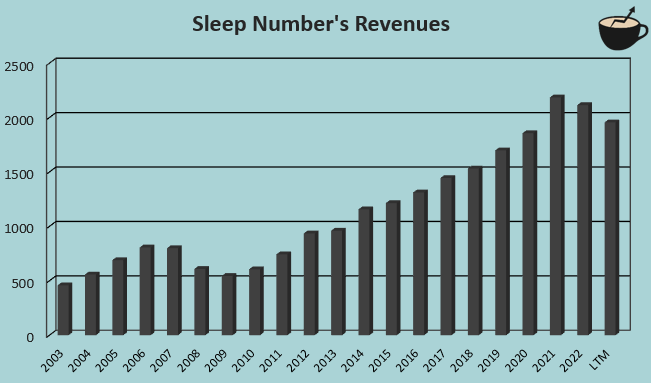

Zooming out from a weak recent financial performance, Sleep Number has been able to achieve constant growth. From 2003 to trailing figures as of Q3/2023, the company has achieved a revenue CAGR of 7.6% in mostly organic manner. The only reported annual revenue decreases are related to the great financial crisis from 2007 to 2009, and the current pandemic disruption along with a weaker consumer sentiment.

{kind=link}

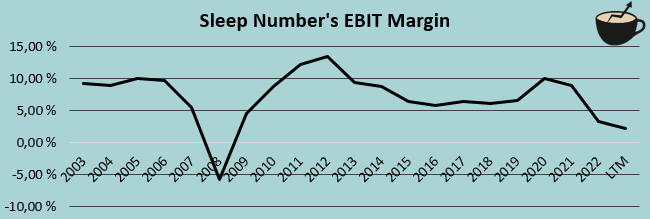

Although selling at a high price point, Sleep Number’s margins haven’t been very great due to a high amount of marketing costs – prior to the pandemic, Sleep Number achieved single-digit EBIT margins with a 2015-2019 average of 6.3%.

{kind=link}

As can be seen from the chart, the company has had recent troubles with the margin; the current trailing EBIT margin only stands at 2.2%. Sleep Number has faced significant challenges in supply chains in recent years. In addition, a currently lower amount of mattresses sold countrywide pushes down Sleep Number’s margins with negative operating leverage – in the company’s Q2 presentation , Sleep Number notes that as of trailing Q1/2023 figures, mattress unit sales are 14% below the 2019 level, down from 30.4 million to 26.3 million. With higher interest rates pushing up the company’s short-term borrowings’ costs, the bottom line is currently near zero. Further, in the Q3 earnings call , the company estimates that trailing unit sales have continued the decreasing trajectory into Q3, with a trailing unit sales level below 25 million units.

Challenges Aren’t Going Away Yet

Sleep Number’s Q3 results didn’t promise a better short- to medium-term performance yet – the company reported a revenue decrease of -12.6%, and an EBIT margin of 1.1% compared to a previous year margin of 2.3%. The sales were largely weak due to an abrupt change in demand in from August forward. In the Q&A of the Q3 earnings call, Peter Keith from Piper Sandler points out that the timing in demand change coincides with the relaunch of a new product line. The given answer from CEO Shelly Ibach relates mostly to Sleep Number’s change in messaging due to pressured consumer spending, but doesn’t seem to fully relate to the asked question; in my opinion, it seems like the launched product line was perceived weakly from customers.

To address the weaker demand, Sleep Number is closing down 40 to 50 stores by the end of 2024 and slowing down new store openings. The company anticipates around $50 million in cost savings from cost initiatives both through the store closings and reduction in headcount in corporate and R&D functions. I anticipate that the majority of cost savings are through closed stores – the savings won’t necessarily translate very well into the bottom row, as they will also result in lower sales. Sleep Number is also optimizing its marketing spend both for the long-term and to address the weaker demand.

The lower demand has hit Sleep Number in both sold units, and the gross margin. Prior to the pandemic, the company achieved a constant gross margin ranging from 60.6% to 63.8% between 2010 and 2019. Currently, the gross margin stands at 57.2%. I don’t see a reason that the gross margin will stay as low when the demand eventually recovers, and the company continues to optimize supply chains. Although the new product line relaunch seems to have had a weak demand, I believe that Sleep Number can recover with new line launches and the demand recovery, raising gross margins back close to the historical average.

Summing up, although the current financials are very weak, I don’t necessarily believe that investors should be worried about the long term. The currently depressed industry sales still seem like the main factor contributing to the financials, even with a likely weak perception of Sleep Number’s relaunch. The company anticipates a return to double-digit adjusted EBITDA margins in 2024, with the current trailing figure standing at 6.7%. Unless Sleep Number’s business is structurally impaired, I believe that an eventual recovery into historically average margins and stronger sales will happen.

Likely Earnings Recovery Still Seems Slept On

With currently turbulent sales and margins, the company’s trailing and forward P/E ratios don’t really provide context into the company’s valuation. To estimate a fair value for the stock, I constructed a discounted cash flow model as usual.

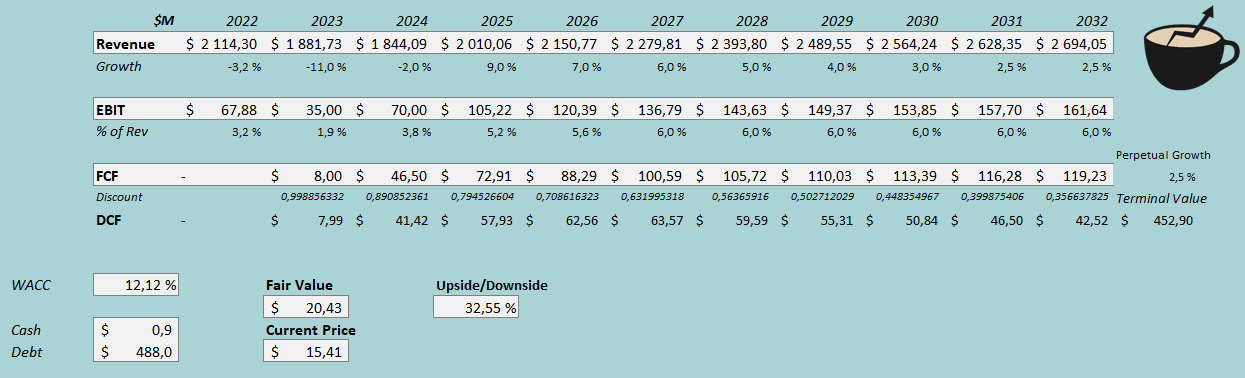

In the DCF model, I estimate a scenario where Sleep Number’s financials start to recover in 2024 and 2025 into historical averages, which I see as the most likely scenario. For 2024, I still estimate weak sales with a revenue decrease of -2% due to store closings along with a starting recovery in demand in the back half of the year. The 2025 growth estimate of 9% includes a recovery in demand, as well as some organic growth. The growth slows down in the following years into a perpetual growth rate of 2.5%, representing a revenue CAGR of 4.1% from 2023 to 2032. I believe that the estimated CAGR is still quite conservative, when comparing to the 2003-LTM CAGR of 7.6% and the weak figures estimated for 2023.

I believe that the margins should eventually recover as well due to a recovery in gross margins and some advantages from cost savings. From a weak 2023 EBIT margin estimate of 1.9%, I estimate Sleep Number to achieve improvements already in 2024 with the cost programs and some demand recovery, raising the EBIT margin to 3.8%. Afterwards, I estimate the EBIT margin to scale further into a sustained level 6.0%, near the level achieved prior to the pandemic. The company seems to have a good cash flow conversion with mostly minimal working capital changes excluding recent quarters, and a moderate level in capital expenditures .

With the mentioned estimates along with a cost of capital of 12.12%, the DCF model estimates Sleep Number’s fair value at $20.43, around 33% above the stock price at the time of writing. The stock seems to be valued only for a partial financial recovery, which is below my expectations for the financials providing a good risk-to-reward in my opinion even with the recent price rally.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the most recent reported quarter, Sleep Number had around $11 million in interest expenses. With the company’s current amount of short-term borrowings , Sleep Number’s annualized interest rate comes up to 8.98%. The company’s current amount of interest-bearing debt is quite large; I estimate the leveraged financing to continue with a high long-term debt-to-equity ratio of 50%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.88% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Sleep Number’s beta at a figure of 1.80 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 14.82% and a WACC of 12.12%.

Takeaway

Although the current financials can mostly only be discussed in a negative light, Sleep Number doesn’t seem like a bad investment due to the currently low pricing on the stock. I believe that the majority of current issues is caused by industry headwinds, and an eventual industry recovery will bring back Sleep Number’s financials into a more historical level. The main risk with the bullish thesis is a continuous weak perception of Sleep Number’s offering, as the relaunch in Q3 seems to be perceived weakly. Still, I don’t see the scenario very likely currently. In my opinion, the recent price rally still has room to continue sustainably, and I initiate a buy rating.

For further details see:

Don't Sleep On Sleep Number's Potential Earnings Recovery