DPZ - DPC Dash: Impressive Growth But Small Profits

2023-12-13 18:22:29 ET

Summary

- Domino's Pizza's master franchise in China, DPC Dash, has seen a 24% increase in its stock since its IPO debut in March at the Hong Kong Stock Exchange.

- Capitalising on China's fast growing food delivery market, the company has seen robust growth in H1 2023, expanded operating margins and even reported net profits.

- However, its market multiples are way ahead of its peers and its still small profits detract from its attractiveness.

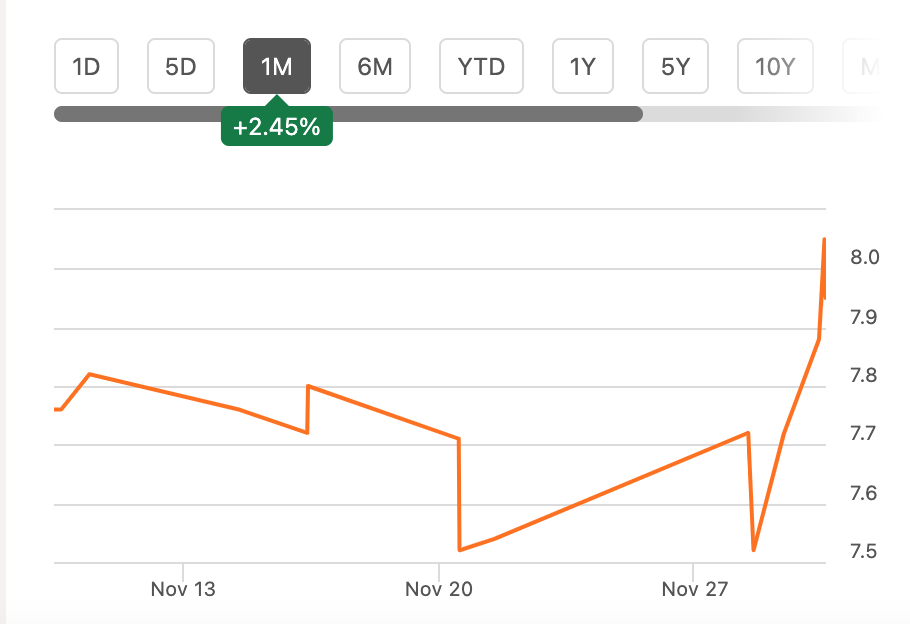

The Domino’s Pizza (DPZ) master franchise for mainland, DPC Dash Ltd (HK:1405, [[DPCDF]]) is a newbie at the stock markets. The initial public offering [IPO] debuted at the Hong Kong Stock Exchange in March and has been trading in the U.S. markets since early November. While the stock has seen just a 3% increase since the past month, the gains for the main listing are already notable at 24% since its first close in March.

{kind=link}

This is an encouraging place to start, and raises the question: can DPCDF stock continue to rise going forward?

The growing China market

Fundamentally, the company has a lot going for it. Domino’s Pizza dominates China's food service market, along with the likes of Starbucks ( SBUX ), McDonald’s ( MCD ), Yum China Holdings ( YUMC ), which operates brands like KFC, Pizza Hut and Taco Bell, as well as Restaurant Brands International (QSR), which runs Burger King along with other food joints.

The food service market is expected to see a healthy compounded annual growth rate [CAGR] of 7.4% over the next five years. But in the context of DPC Dash, the growth in the delivery segment is particularly significant, since 63.6% of its revenue in the first half of 2023 (H1 2023) was through the channel.

{kind=link}

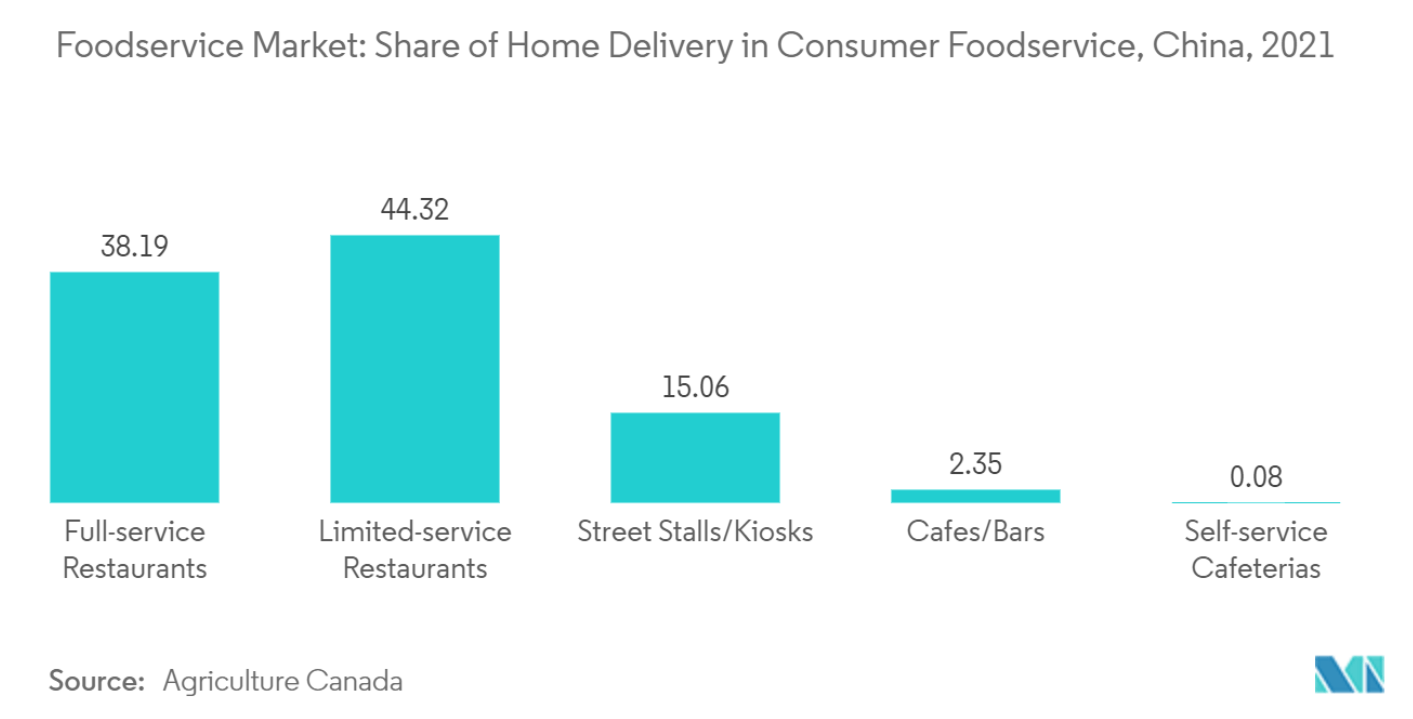

As it happens, research by Mordor Intelligence shows that it's the fastest growing segment in the food service market, enabled by supportive technologies like food delivery apps and growing urbanization. As of 2021, deliveries made up 38% of the market share even for full-service restaurants, though the share remains the highest for limited-service restaurants (see chart above), as would be expected. Over 2023-28, the segment is expected to see a CAGR of 9.6% , higher than that for the food service market as such.

Sales growth more than doubles

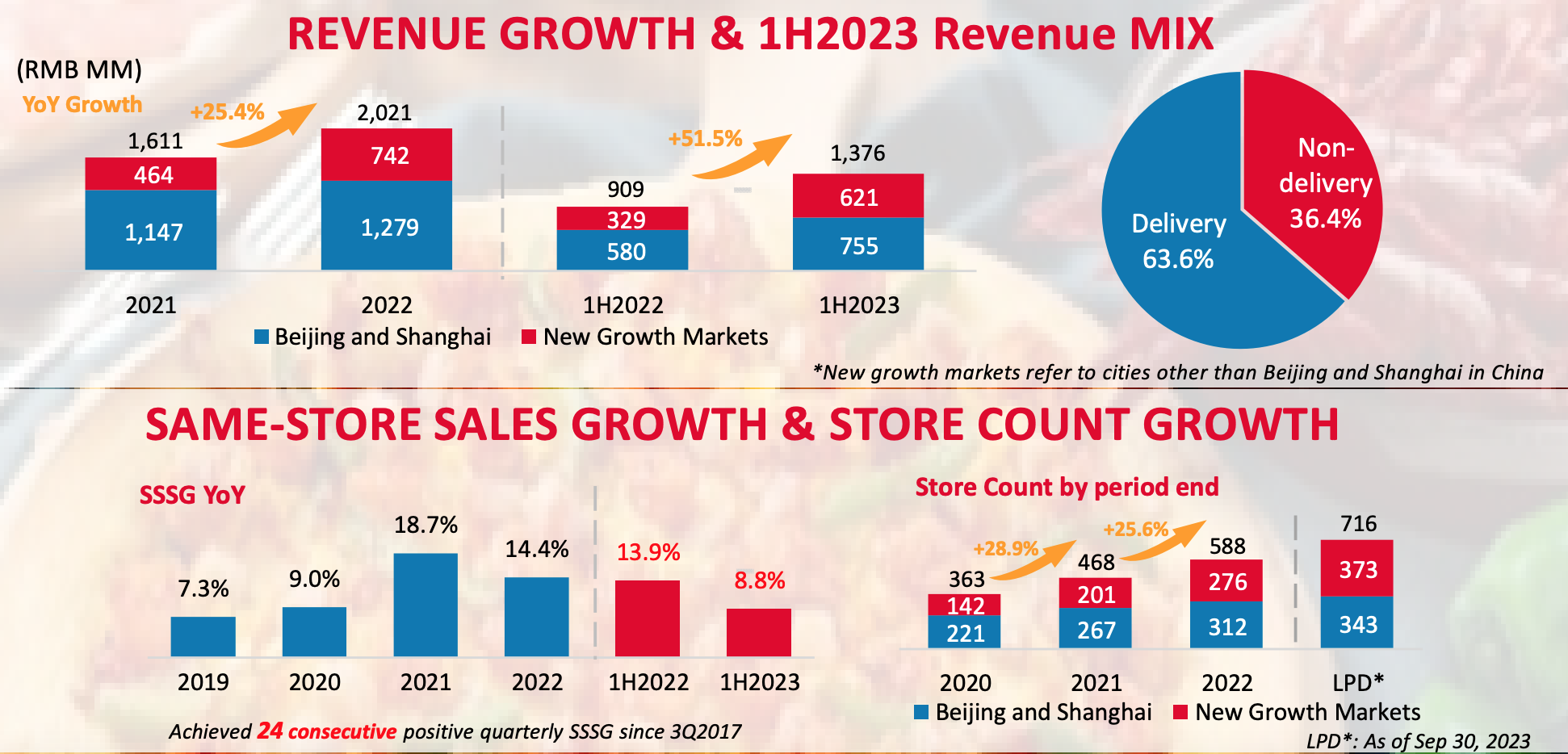

DPC Dash has seen a far bigger growth in delivery revenues so far this year, compared to that expected for the market. For H1 2023, the number came in at 30.2% year-on-year (YoY). Healthy as it is, growth in the non-delivery segment has been even bigger at 88.8%, which could be explained by pandemic-related caution during the base period, which made eating out less accessible.

Total revenues have seen a strong 51.5% growth, an improvement from the full year 2022 (see chart below). Interestingly, this is despite slower growth in the same sales stores in H1 2023 at 8.8% compared to 13.9% in H1 2022, indicating that revenues have been driven by store expansion.

{kind=link}

Becoming profitable

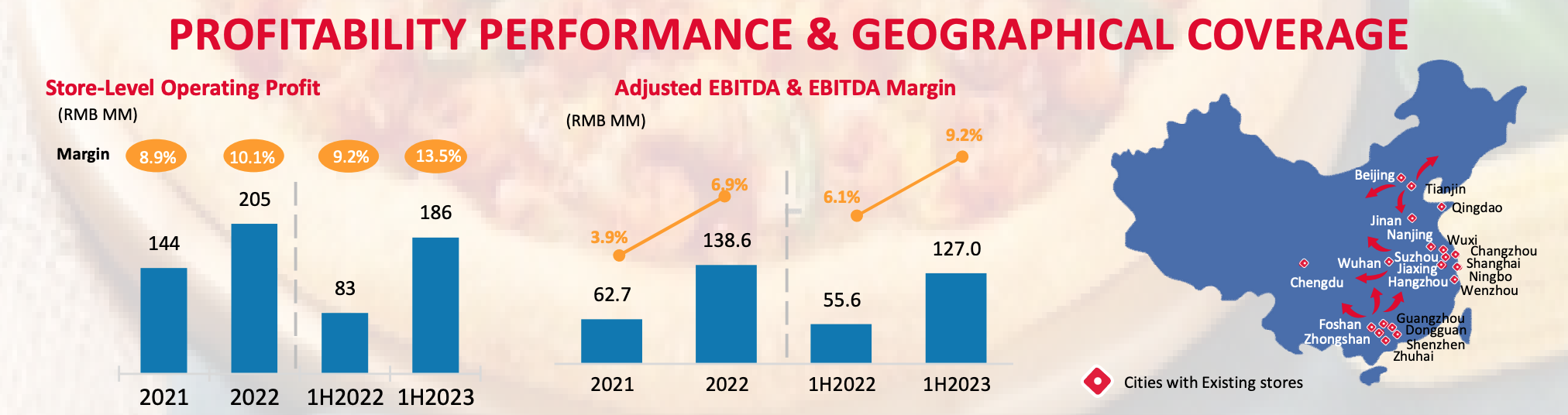

Profits are growing too. The company’s store-level operating profit more than doubled in H1 2023 (see chart below) and the margin has improved to 13.5%, higher than both that in H1 2022 and for the full year 2022. Similarly, EBITDA and adjusted EBITDA margins have improved as well.

{kind=link}

However, the key development regarding profits is that the company clocked net profits in H1 2023 after seeing a loss in H1 2022. The net profit margin (for profit attributable to shareholders) is still minuscule at 0.6%, but it’s still an improvement in trend.

The outlook

For the full year 2023, the company expects to continue expanding, with a target of 180 new stores after a net opening of 84 stores in H1 2023. It aims to add another 240 stores in 2024 as well.

Assuming that the revenue per store for the full year 2023 grows at the same rate of 14.5% as seen in H1 2023, DPC Dash would end the year with a revenue of RMB 3021 million or USD $423 million, representing a 49.5% growth in total revenues. If the trend continues into 2024 and the company's store openings go as targeted, DPC Dash will clock a revenue of RMB 4541 million or USD $635 million, a 50% YoY growth.

As far as profits go, if the net margin stays static at 0.6%, the net attributable profit would come in at RMB 19.2 million (USD $2.7 million) and RMB 28.9 million (USD $4 million) in 2023 and 2024 respectively.

It's of course possible that margins improve. However, since China is officially in deflation mode now, after flirting with the trend earlier in the year, I'm not sure if that can play out. Still, there's a possibility considering that PPI inflation softening even faster , so margin expansion can't be ruled out, though it remains to be seen.

The market multiples

Based on these estimates, DPCDF’s forward price-to-sale (P/S) for 2023 comes in at 2.3x, the same as the trailing twelve months [TTM] P/S. The company's multiples are higher than the ratios for the consumer discretionary sector at 0.88x and 0.89x respectively. This, of course, can be explained by the fact that the company is growing much faster than the sector. It has seen a 41.9% revenue increase on a TTM basis, compared to a 5.5% median growth for the sector.

Faster revenue growth is also an explanation for why DPCDF is trading at higher multiples than its closest peers. Consider YUMC, which has a forward ratio of 1.52x and a TTM ratio of 1.59x. Its TTM revenue growth is much smaller at 8.2% as well.

Similarly, Haidilao International (HDALF), which runs restaurants across China, has a forward ratio of 1.81x and a TTM P/S of 2.09x. It has an even smaller HDALF at just 1.6%.

At the same time, both YUMC and HDALF are profitable companies, and DPCDF hasn't yet reported a full year of profit. In fact, its small margin so far means that its forward P/E for 2023 is at a huge 368.1x compared with YUMC at 20.9x (the forward P/E for HDALF is unavailable).

What next?

On balance, it’s hard to make a case for DPC Dash just based on its stronger growth. Ultimately, its profits have to show an uptick. While it’s a good sign that the company has now become profitable, it remains to be seen if or how fast the profits grow. This is a particular concern in the China market in deflation.

From a medium to long-term perspective, the signs are encouraging, though. It has the franchise of a globally established brand, the market is firmly in its favor with the growing popularity of food delivery services, and its expansion is healthy as well. That it can make profits going forward is a good sign too.

But DPC Dash Ltd stock has run up since the IPO, and its market multiples don’t make a definite buy case for it. I’m going with a Hold rating on the DPC Dash stock.

For further details see:

DPC Dash: Impressive Growth But Small Profits