ET - DPG: Fine Fund High Premium

Summary

- DPG has continued to push into a higher premium after breaking into premium territory in 2021 for the first time since its inception.

- The fund's distribution has been steady, and although the NAV rate is elevated, I wouldn't expect a cut.

- The underlying portfolio holdings seem perfectly fine, but due to a higher premium, it remains a hold at this level.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 9th, 2023.

Duff & Phelps Utility and Infrastructure Fund ( DPG ) caught the premium bug a couple of years ago and hasn't been able to shake it. Perhaps, it's been hanging out with its sister fund for too long, DNP Select Income Fund Inc. ( DNP ).

YCharts

The fund's underlying portfolio is all sorts of things that I love to invest in: infrastructure that includes a heavy emphasis on utilities, some midstreams and a dash of other infrastructure plays such as toll roads and rail. It is the premium that makes me weary of adding or considering it at this time. Other funds can add similar exposure for a better valuation.

However, we can still update the fund for those who continue to hold the name. We have an annual report to look at distribution coverage, and we can see what changes the portfolio has made since our last visit. Since our last update on this fund, the share price has decreased. On a total return basis, however, investors were given positive results.

DPG Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 1.62

- Premium: 11.51%

- Distribution Yield: 10.25%

- Expense Ratio: 1.62%

- Leverage: 29.44

- Managed Assets: $662 million

- Structure: Perpetual

The investment objective for DPG is "to seek total return, resulting primarily from (i) a high level of current income, with an emphasis on providing tax-advantaged dividend income, and (ii) growth in current income, and secondarily from capital appreciation."

They intend to meet this objective by "investing primarily in equities of domestic and foreign utilities and infrastructure providers. The Fund's investment strategies endeavor to take advantage of the income and growth characteristics of equities in these industries."

The fund's total expense ratio comes to 2.51% when including the leverage expenses. As interest rates have been rising, their borrowing costs have also been rising. However, they took down leverage slightly in the last fiscal year . Secured borrowings went from $170 million to $155 million.

Their mandatory redeemable preferred shares stayed flat at $40 million year-over-year. The preferred here are floating rates, so they aren't sheltering the fund from the higher costs. It is based on 3-month LIBOR plus 1.95%. At the end of October 31st, 2022, the rate came to 5.69%. That's a massive leap from the weighted daily average rate of 3.16%, which itself was also elevated due to rapidly rising interest rates.

Their borrowings through the credit agreement aren't much better, but they ended the fiscal year at a rate of 3.975%, averaging 1.88%.

All that being said, with interest rates continuing to rise, leverage has only become even more expensive.

Performance - Strong Investments, Too Expensive

To continue on the topic of leverage for a bit, utilities are seen as a natural casualty of higher interest rates. Debt becomes more expensive, and investors who find utilities attractive are generally income investors who can now get ~4% rates from risk-free U.S. Treasuries.

However, DPG noted an important point in its last annual report: most utility debt is long-term and fixed. Too bad DPG didn't take a page from their underlying portfolio position playbook and fix their interest rates too. In this discussion, they also noted that the rising costs could be recovered with a bit of lag.

There has been increased concern recently about the earnings risk to utilities from refinancing variable rate, short-term debt at higher interest rates. It is important to note that the vast majority of utility company debt is fixed and long-term. Additionally, regulated utilities can generally recover rising interest expense through customer rates, though there can be a lag in recovery depending on the timing of rate cases. The bigger risk is at the unregulated operations of utilities' parent companies, where debt costs are not recoverable through regulatory mechanisms.

So the higher interest rates aren't impacting these investments on the debt side of the equation. We certainly saw the utility sector doing what it does best in 2022, too. That was being the defensive plays they naturally are, and investors kept utilities flat for a year when everything else was down despite these concerns. That's also helped keep DPG stable over the last year, with similarly flat results. That was except for the fund's share price results.

YCharts

With an outperforming share price above the underlying portfolio performance, that's how we end up with a premium. A premium that was already elevated by now near all-time high record valuations.

YCharts

As I mentioned, some other funds with similar but not completely the same exposure could provide better values at this time. That could include Cohen & Steers Infrastructure Fund ( UTF ) and Reaves Utility Income Fund ( UTG ). These funds offer different approaches but are as close to what you could get to as 'peers' in the CEF world full of niche funds.

Over the longer term, one might notice how much DPG has underperformed against these peers and its sister too.

YCharts

However, I'm somewhat willing to defend these results as the longer term isn't particularly relevant. They changed their name and investment policy at the end of 2019 . The results since then have been more encouraging. Here are the results from January 1st, 2020, up to today.

YCharts

Distribution - Elevated But No Cut Expected

A similarity between DPG and DNP is consistent distribution. However, DPG's history is much shorter than DNP's history. DPG also pays quarterly rather than DNP.

{kind=link}

With that being said, CEFs can pay out what they want for as long as they want until NAV goes to $0. In this case, the fund's distribution rate comes to 10.25%. That's certainly attractive, but with a hefty premium, the NAV rate is actually 11.43%. That's how much the fund has to earn to cover its distribution.

That alone, we know, is an elevated level relative to what one might be able to expect over the longer term. Despite that, Duff & Phelps, if DNP is any indication, isn't into cutting their distributions.

{kind=link}

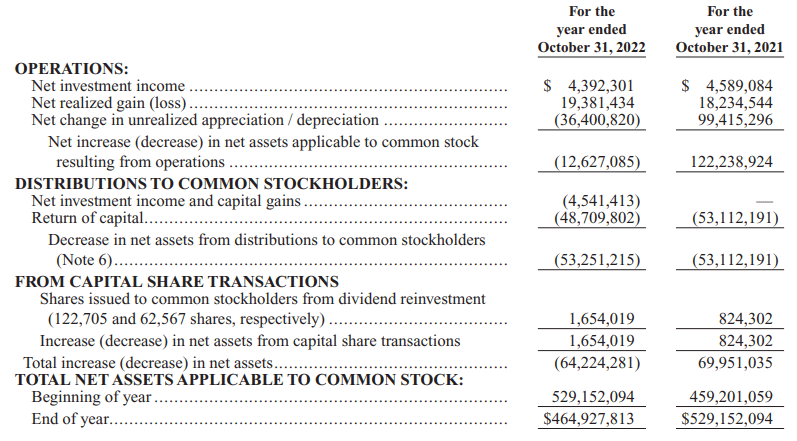

NII coverage came to 8.25%, and we know that with higher leverage costs, this should go down going forward. The decline could be negated to some degree by higher dividends in the portfolio, as most utility companies raise their dividends annually.

Additionally, the fund carries energy names that pay out return of capital. That is subtracted to come up with the total investment income. Therefore, if we add that back in, we can get net distribution coverage or distributable cash flow.

{kind=link}

That would take coverage up to nearly 25%. A much better coverage, but most equity CEFs will require significant capital gains.

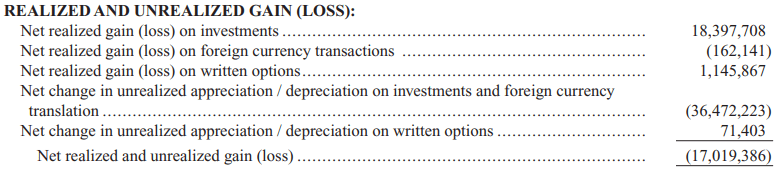

Although the fund hadn't declined as much as the broader market, the realized gains and unrealized gains combined still meant a decline in assets. Some of these realized gains came from their option writing strategy. That can be replicated in a flat or down year.

{kind=link}

This all suggests that the fund didn't cover its distribution in the last year, which can become a problem if it happens year after year.

For tax purposes, that also means we have seen some destructive return of capital in the fund despite collecting ROC distributions on its underlying holding. Here's the 2022 tax information they provided.

{kind=link}

DPG's Portfolio

The fund is fairly active; it consistently has a portfolio turnover of around 50%. That being said, the fund doesn't appear to change drastically in how it is positioned.

Overall, the fund is positioned the heaviest in the utility sector. This is followed by midstream exposure and then infrastructure. Within the midstream exposure, several of the names are MLPs. Cash is a minimal position, as it should be for a fund.

DPG Sector Exposure (Duff & Phelps)

For geographic exposure, the fund carries the highest weighting to U.S. This has traditionally been the case. It had even increased its weighting since our prior coverage, when it showed a 65.4% weighting. This doesn't make it much of a global fund, which is what they pivoted away from in 2019.

DPG Geographic Allocation (Duff & Phelps)

With global positioning, this has put some exposure to different currencies. Although not to an overly large extent.

DPG Currency Exposure (Duff & Phelps)

Looking at the top holdings, we see a hefty allocation of nearly 40%. The top holding of NextEra Energy ( NEE ) represents 7.5% alone.

DPG Top Holdings (Duff & Phelps)

NEE also is one of the names that has continued to be in DPG for years, as it was previously its largest exposure. In fact, NEE is in just about every utility/infrastructure fund that I cover in some allocation. This has been for a good reason, as historically, the results and growth from NEE have been quite impressive. However, these sorts of results have also made it quite a pricey utility name to consider.

Energy Transfer ( ET ) is another popular name in infrastructure and energy funds, which I run into commonly. It's an MLP that had cut its distribution previously but has been working to ramp it back up. They're now paying the same amount as they were prior to the cut. The unit price has been heading in the right direction but has been much slower to recover.

YCharts

The third-largest position is Atlas Arteria Ltd ( MAQAF ). This is where we start to get a bit more interesting as it's a global toll road name based out of Australia. These shares do not trade on a U.S. exchange. However, this is a name that still provides distributions and a higher yield to DPG and its shareholders. That being said, it's also variable, as is common with companies outside of the U.S.

{kind=link}

Conclusion

DPG has an interesting portfolio of infrastructure plays but continues to trade at a premium. In fact, the premium has increased to a level where it's near an all-time high premium. That keeps it at a hold rating, and investors could consider waiting for a better entry.

For further details see:

DPG: Fine Fund, High Premium