CA - Dream Office: A Dividend Cut Is Necessary To Preserve Value

2023-09-05 05:33:17 ET

Summary

- Dream Office's Q2-2023 results reflect the risks of the substantial issuer buyback and stresses in the office sector.

- Occupancy levels have remained steady, but tenant retention ratio is low, and interest coverage ratio has fallen.

- Despite leasing activity and commitments, the company may need to consider a dividend cut to preserve its NAV.

On our last coverage of Dream Office REIT ( D.UN:CA ), (DRETF), we went over the risks of the substantial issuer buyback, coupled with the current stresses in the office sector. We left with a relatively negative note and felt that even the 8% implied cap rate did not warrant a firm buy rating. With the Q2-2023 results out and the company metrics now reflecting the substantial issuer bid, we thought it would make sense to put out why we felt the best move would be a dividend cut.

The Big Picture

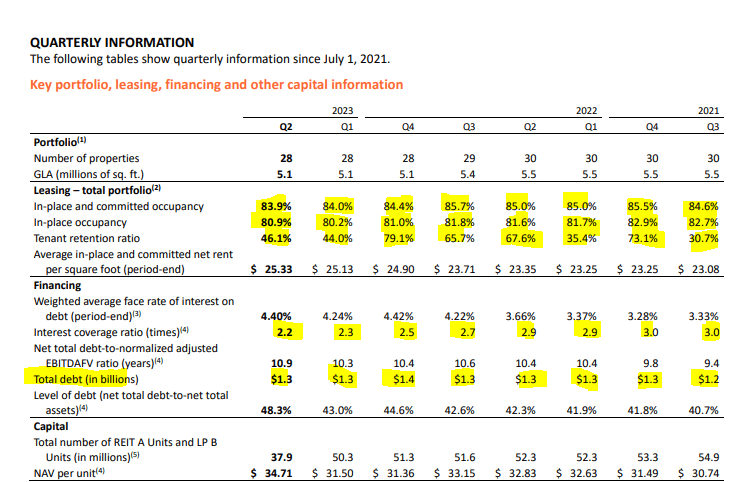

For the point we want to make, only one picture from the company financial statements is enough to hit home. We have highlighted a few things below but every single figure there is relevant. So let's get to it.

Dream Office Q2-2023 Financials

{kind=link}

In place and committed, occupancy was down a smidge again from 84.0% to 83.9%. This is a small drop and overall the company has held occupancy levels pretty steady since Q3-2021. This is despite a tenant retention ratio which has been on the low side in most quarters. So Dream Office has managed to fill vacant spaces about as fast as they can. This is still not the best outcome relative to retaining their existing tenants. The best customer you have is the one already in place. The second best customer/tenant is one you are trying to recruit and costs tons in leasing commissions and usually a lot in tenant improvements.

Through this turmoil, their interest coverage ratio has fallen from 3.0X to 2.2X. A lot of that is rising interest rates. That you can see in the same picture above, moving from 3.33% to 4.4%. But the REIT still deserves scolding for that. They could have locked in slightly higher rates for a lot longer in the era of ZIRP (zero interest rate policy) but did not. But that is not all that happened. Total debt and net debt to total assets are also up in the same period. Debt to adjusted EBITDA is up 1.5 turns. These latter numbers have been going up as Dream is directing excess cash flow towards unit buybacks. Total outstanding units are down from almost 55 million to just a shade under 38 million.

Q2-2023

The results were in line with expectations, with funds from operations ((FFO)) coming in at 35 cents a share. On a quarterly basis, FFO peaked in Q3-2021 at 42 cents and has been steadily moving lower despite some massive buybacks. In some ways this likely could be the short term trough as the full impact of the lowered unit count will flow through Q3-2023.

Leasing activity was healthy and the REIT has secured commitments that exceed the natural lease expirations during 2023. The strategy of adding value to existing buildings by leasing premium restaurants continues for Dream Office and a new one was launched this quarter.

During Q2 2023, we successfully completed the launch of premium restaurant Daphne in the ground floor retail space at 67 Richmond Street alongside our joint venture partner, INK Entertainment. Since the beginning of 2022, as part of our strategy to pursue premium retail offerings at our properties, we have completed 52,000 square feet of restaurant leases in the downtown core at weighted average initial net rents of $54.44 per square foot, or 24.8% higher than the weighted average prior net rents on the same space, escalating to an average net rent of approximately $70.00 per square foot over the terms of the leases with a weighted average lease term of 14.1 years. For certain restaurant leases, the Trust has revenue participation rights over and above the contractual net rents.

Source: Dream Office Q2-2023 Financials

Another validation of the management strategy came post Q2-2023 when the REIT leased an entire building.

Subsequent to Q2 2023, we secured a commitment at 366 Bay Street for a lease for the entire building with a global financial institution that has been attracted by the location of the asset, as well as the successful completion of our redevelopment and decarbonization program at the building. The lease is expected to have a term of 15 years for approximately 40,000 square feet with initial net rents of $38.00 per square foot, escalating to $50.00 per square foot over the term of the lease. The full building fixturing and fitout is expected to commence in Q4 2023 on redevelopment project completion with lease commencement scheduled for Q4 2024.

Source: Dream Office Q2-2023 Financials

This is a small building (remember Dream Office's total GLA is 5.1 million square feet), but positive feedback from the market nonetheless.

Outlook

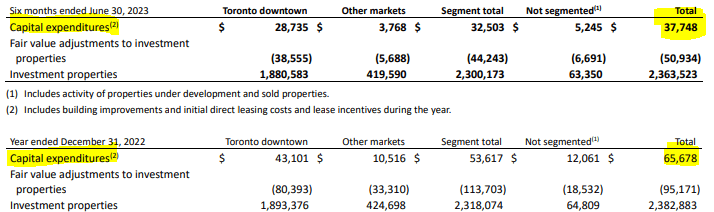

It is going to be a long slog improving office occupancies. While some trends in work from home are reversing, vacancies remain too high to give landlords any bargaining power. One key metric here is the relative ratios of FFO to capital expenditures. Note how the FFO has dropped from last year to this year.

Dream Office Q2-2023 Financials

{kind=link}

Now compare the capital expenditures in the first 6 months of this year, versus the total for last year.

Dream Office Q2-2023 Financials

{kind=link}

Even without comparing last year, capital expenditures this year have exceeded FFO. FFO is before dividends. So this gets to the core of our problem today. With a weighted average debt maturity of 2.9 years and capital expenditures exceeding FFO, how much in dividends do you want the REIT to pay?

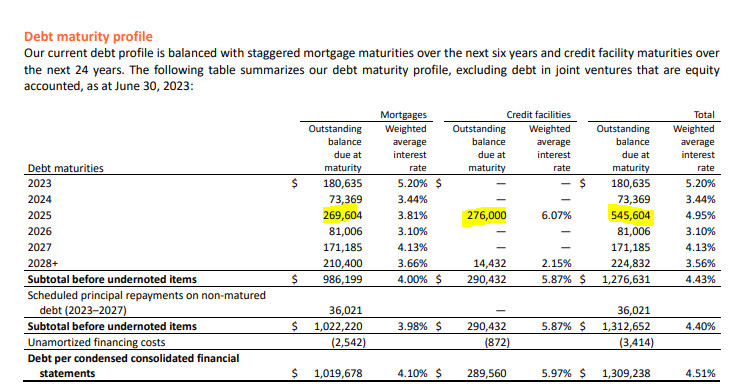

One could argue that there might be a rebound soon and that should fix all the problems. We think a rebound is possible and certainly some analysts think FFO trough is right at our doorsteps. But even the most optimistic (as in lowest) estimates for capex into 2024 and 2025 will make dividends+ capex to be higher than FFO. We are going into a refinancing flood in 2025. There is half a billion plus to refinance.

Dream Office Q2-2023 Financials

{kind=link}

FFO this year, which again is before dividends and capex, will be close to $55 million. So we think a proactive measure here is to baton down the hatches and focus on preserving the NAV that the company clearly believes in.

Verdict

Dream Office has cut its dividends in the past. The current situation is about as stressful as the 2016 fallout from low oil prices. Back then, Dream Office was completely leveraged to Calgary office buildings and the downturn was monumental. It made the correct decision to get rid of that space, even at a big loss and cut the dividend. As it turned out, Calgary office has still not found a bottom on occupancy 7 years later. Good call.

Here, the NAV stands at almost 2.5X the current price. We can say with some confidence that almost no one outside of management believes that $34.71 number. Even Dream Unlimited Corp. ( DRM:CA ) tendered in almost all the units it owns via Dream Asset Management in the substantial issuer bid. So, if the REIT wants any chance of getting the price anywhere in the postal code of that NAV, it needs to take the refinancing stress off its plate. We would argue that the dividend cut would also make it appear less desperate to tenants pushing for a deal. After all, the REIT's refinancing needs in two years are public knowledge, and having a more liquid balance sheet will definitely help. Based on all the information, Dream Office now has a "High" level of danger of a dividend cut on our proprietary Kenny Loggins Scale.

Author's Scale

This rating signifies a 33-50% probability of dividend cut in the next 12 months. We continue to rate the stock as a "hold" as we think NAV is higher than the current stock price but not enough to offer a good margin of safety.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Dream Office: A Dividend Cut Is Necessary To Preserve Value