CA - Dream Residential: Outperforming The Entire U.S. Residential REIT Sector

2023-03-22 13:10:32 ET

Summary

- This residential REIT began its operations in 2022.

- It has taken the market time to warm up to it, but we saw the potential.

- We were bullish in 2022 and that has not changed.

- The fantastic appreciation to date should temper your expectations.

We debuted our coverage of Dream Residential REIT ( DRR.U:CA ) in October of last year. It had only had its IPO earlier in the year and received a frigid welcome from the market. With a low debt to asset ratio, no refinancings in the next couple of years, higher yield than its peers, and a good management team, it had us intrigued. The market valued it at half its NAV. We liked the REIT's chances and said.

If it even trades a bit higher from its current 12X AFFO to 14X AFFO or the cap rate gap closes, we get to a price of $8.40. That combined with its yield and the expectation of a reduction in cap rate, makes it a good buy for any portfolio.

Source: Want A Residential REIT With A 6% Yield? Dream On

It has been a bumpy ride, but investors of this REIT have done alright since then. It has outperformed its strong Canadian peers like Boardwalk REIT ( BEI.UN:CA ), ( BOWFF ) and Canadian Apartment REIT ( CAR.UN:CA ), ( CDPYF ). DRR has also absolutely clobbered the US peer group. Equity Residential ( EQR ) lagged DRR by almost 39% and AvalonBay Communities ( AVB ) fell short by 36%. The same chart had this residential REIT bring up the rear back in October.

In October, the market was bestowing the fledgling an 8% implied capitalization rate [cap rate] versus the 4.9% calculated by the REIT. This was harsher than the treatment meted out to its more experienced peers like Boardwalk and Mid-America. With Q4 results, DRR increased its weighted average cap rate to 5.22%.

{kind=link}

Despite the solid appreciation in the units, the stock still trades with an implied cap rate of close to 7%. Next, we briefly reintroduce DRR to the uninitiated, review the recent numbers and provide our updated outlook for this REIT.

The REIT

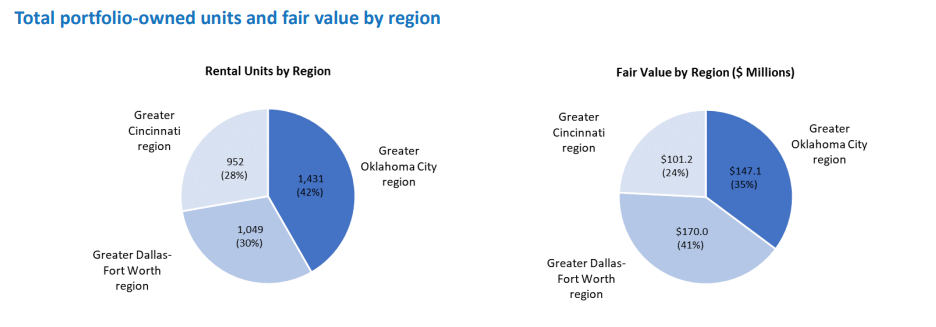

DRR has a portfolio of 16 garden-style properties, comprising 3,432 units and located across the Sunbelt and Midwest regions of the US.

{kind=link}

Garden-style properties comprise low rise multifamily buildings with access to considerable green space.

{kind=link}

It has comfortably enjoyed occupancy rates in the 90s since inception last year, with the most recent data coming in over 95%. With an average term to maturity of 5.6 years, DRR does not have any refinancings to deal with until 2025 and nor does it have any variable rate debt. The weighted average interest rate on its mortgages, all of which are secured, was 3.95% at the end of 2022. At December 31, 2022, its debt to asset ratio was under 30% and interest coverage was 2.7X.

{kind=link}

DRR pays a monthly distribution of $0.035/unit, which at the current price of $8.75 makes this residential REIT yield 4.8%. While decent and still a leader amongst its peers, it is lower than the 6% we were getting last October.

Q4 Results

DRR closed out 2022 with a 1.8% increase in average monthly rent compared to the previous quarter. Occupancy bumped up to 95.5% and leasing spreads were up over 8%. The REIT kept inflation effects under control as net operating income (NOI) margins expanded slightly in the fourth quarter. The FFO for the short year was $0.40/unit. The focus for 2022 was on the development front. DRR completed 109 renovations during the quarter across properties. One of the key advantages of its renovations was the big bump up in rents. On average, it is getting about 30% higher rents for renovated suites. Now, even the non-renovated suites are in high demand and expiring leases bumped 15% higher. Nonetheless, the capex is paying off and the plan is to complete renovations for about 400 units in 2023.

Valuation

DRR trades at about 13X FFO for 2023. This compares to a relatively expensive peer group trading near 18X. That per group multiple is generally too high and lands most of our ratings in the hold or sell category . But Dream's ultra-low multiple combined with low debt makes this one of the rare attractive values in apartment/residential space. Unlike its peer group, DRR remains insulated from interest rate risk for two more years. Overall, DRR's 7% implied cap rate with multiple additional favorable qualities, makes it the best value in this area.

Verdict

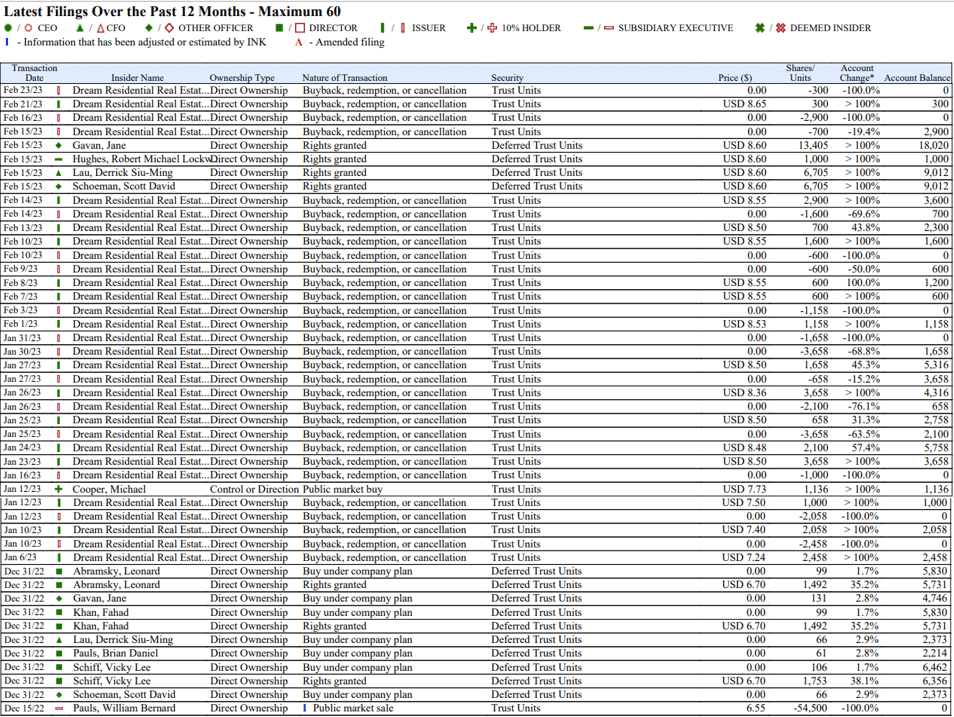

If you had to pick a residential REIT today, DRR is definitely one that should grab your attention. Previously, insiders had purchased a lot of DRR units.

Insider Ink

Currently that has slowed with only one public market buy in recent times. The REIT did start buying back its units subsequent to the year end and that adds a bit of confidence to the situation.

{kind=link}

It has the approval to buy back close to a million units for a period of one year. As of February 23, over 25,000 units had been bought back under this program. The steady execution alongside NAV accretive buybacks underscores the potential for the year ahead. The key risk is of course a widespread market meltdown which could derail even the most bullish thesis. We still think DRR merits a look, even with that risk in mind. We are maintaining our buy rating with a $9.50 price target for 2023.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Dream Residential: Outperforming The Entire U.S. Residential REIT Sector