RTX - Ducommun Aims For A Bigger Piece Of A Growth Pie

2023-09-14 07:00:00 ET

Summary

- Ducommun Incorporated provides engineering and manufacturing services for various industries, including aerospace and defense.

- Ducommun aims to achieve significant revenue growth and increase its EBITDA through restructuring, cost-cutting measures and accretive acquisitions.

- The company aims to expand its portfolio and extract more value from that portfolio.

The aerospace industry is a very interesting industry for investments. However, the industry currently does face various challenges next to the long-term opportunities. As a result, I am expanding my coverage deeper into the supply chain as the bigger aerospace companies might not always offer sufficient value in the near-term. In this report, I am adding Ducommun Incorporated ( DCO ) to my coverage.

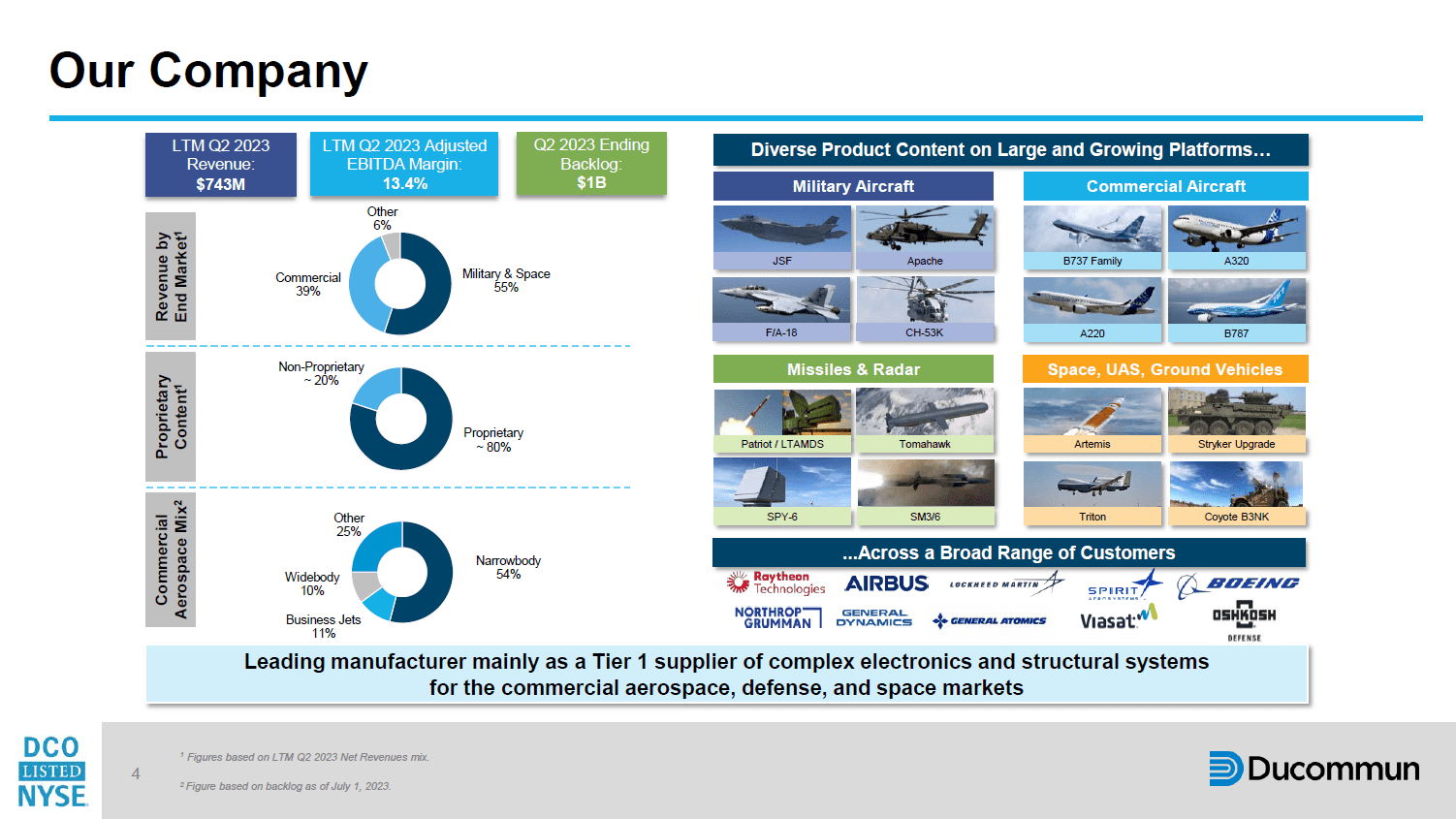

What Does Ducommun Do?

Ducommun Incorporated is a provider of engineering and manufacturing services for various products and applications used in the aerospace and defense, industrial, medical, and other industries. The Company offers value-added products and manufacturing solutions to its customers in its primary businesses of electronics, structures, and integrated solutions. It operates through two segments: Electronic Systems and Structural Systems .

The Electronic Systems segment designs, engineers and manufactures electronic and electromechanical products used in technology-driven markets, including aerospace and defense and industrial end-use markets. It has multiple product offerings in electronics manufacturing for diverse applications, such as complex cable assemblies and interconnect systems, printed circuit board assemblies, and lighting diversion systems.

The Structural Systems segment designs, engineers and manufactures various sizes of complex contoured aerostructure components and assemblies.

In April, the company completed the acquisition of BLR which provides aerodynamic systems that enhance the productivity, performance and safety of rotary- and fixed-wing aircraft on commercial and military platforms.

The Growth Drivers for Ducommun

{kind=link}

Ducommun has three end markets. The primary ones are commercial and defense with space being the smaller end market but with high growth opportunities. Within the commercial airplane market, the company is positioned well with exposure to the Boeing 737 MAX, Boeing 787, Airbus A220, Airbus A320neo and Airbus A330 leveraging its knowledge on titanium forming and aluminum forming and milling. All of these commercial airplane platforms are expected to see significant rate increases in the years to come which should generate higher revenues for Ducommun and better unit cost.

With the tailwind to defense spendings and the need for development of new capabilities in the areas of hypersonics, missile defense and unmanned aerial systems and counter unmanned aerial systems Ducommun can also expect revenues to increase in all defense categories.

Ducommun has a broad customer base, including Boeing ( BA ), Airbus ( EADSF ), Northrop Grumman ( NOC ), Lockheed Martin ( LMT ), General Dynamics ( GD ) and Raytheon Technologies ( RTX ).

{kind=link}

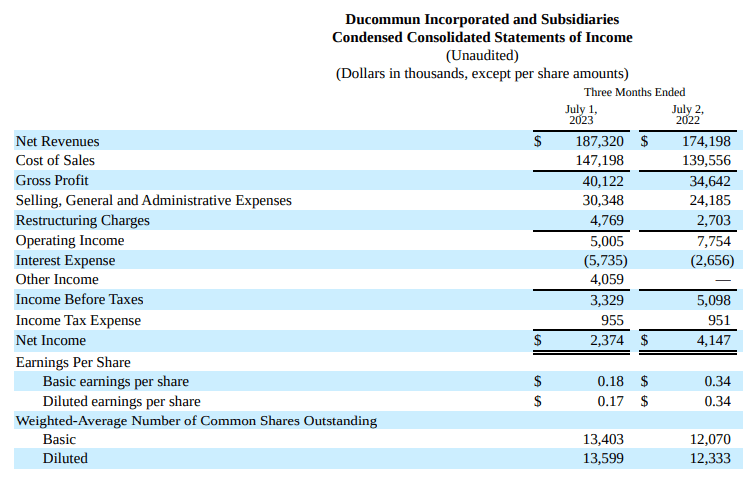

Revenues grew by 7.5% to $187.3 million, driven by $21.2 million higher revenues in commercial aerospace end markets due to higher production rates on big aircraft platforms, while military and space revenues declined $10.8 million due to lower build rates. Gross profits rose to $40.1 million marking a 21.4% gross margin up from 19.9% a year earlier.

The operating profits, however, declined due to higher selling, general and administrative expenses and restructuring charges while after-tax earnings declined from $4.15 million to $2.37 million driven by higher interest rates providing a headwind to the interest expenses partially offset by insurance recoveries recognized in other income related to business interruption and equipment damage due to a fire at a Mexico facility in 2020 and a smaller insurance recovery for a fire earlier this year.

These are the kind of income items that we want to adjust for as well as adjustments for restructuring and any cost in connection with the aforementioned fires. Adjusted EBITDA grew from $24.1 million to $26.1 million or around 8.3% with adjusted EBITDA margins of 13.9%.

So, on adjusted EBITDA basis the results did improve and showed EBITDA growth in excess of revenue growth.

Ducommun Executes Vision 2027

In 2022, Ducommun management approved a restructuring plan which should see the company grow its revenues by 35% to $950 million to $1 billion fully leveraging its titanium capabilities and supporting higher build rates in the commercial airplanes industry and higher demand in the defense industry. The revenue growth should be around 6 to 7 percent annually to achieve this goal. The H1 2023 revenues grew 9.1%, indicating that the company is slightly ahead of schedule.

Furthermore, the company wants to grow its EBITDA to 18% and from 13% in 2022. With little to no change in the adjusted EBITDA margin year-over-year, I would consider this to be the bigger challenges. To cut costs, the company has also expanded its manufacturing capacity in Guaymas, Mexico, which also fits in a near-shoring trend with a planned sale of the Monrovia facility in the used scheduled for the second half of the year. In the Engineering Products Portfolio, the company aims for a higher share of total revenue and more aftermarket revenues.

Is Ducommun Stock A Good Buy?

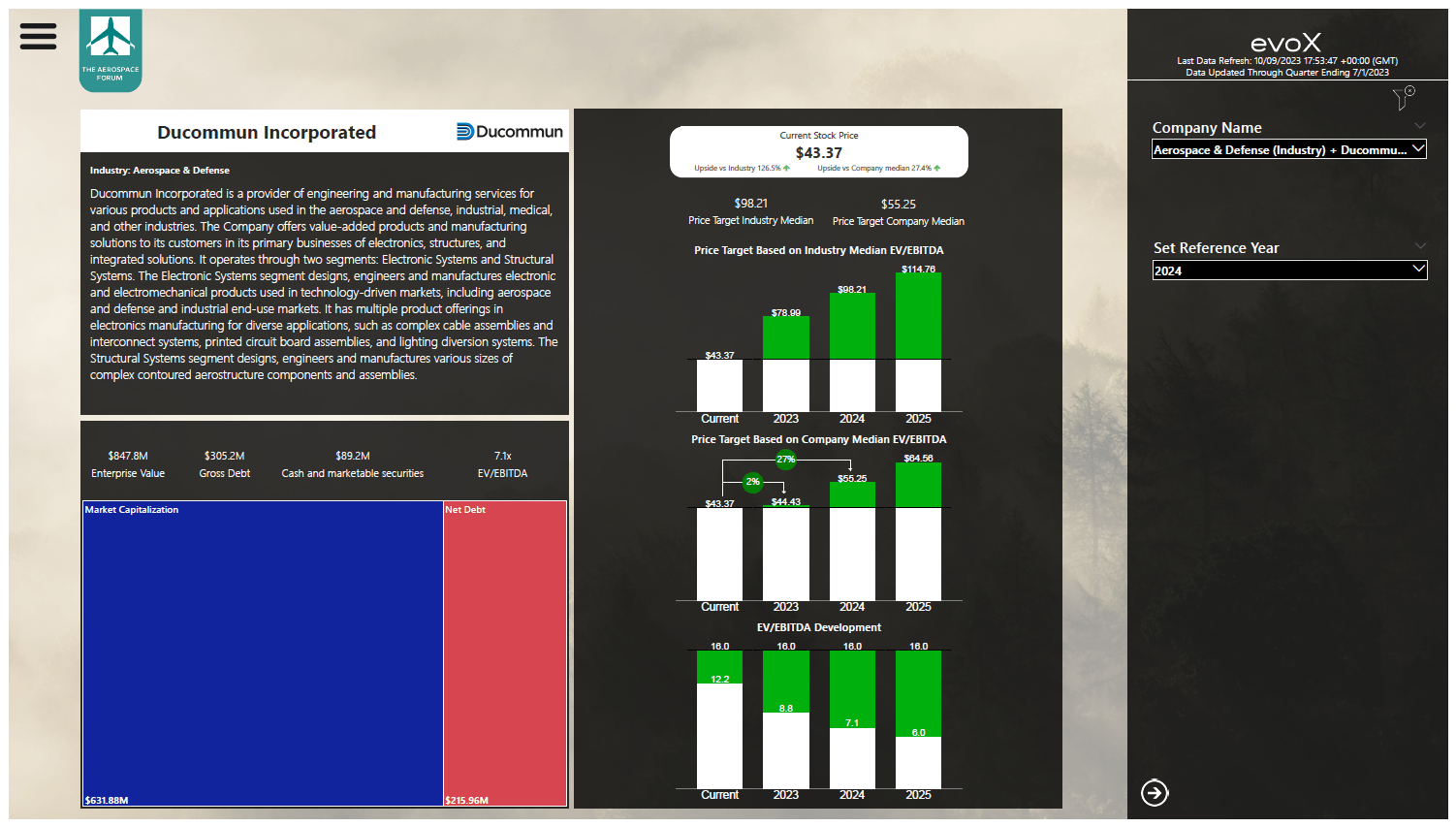

The big question of course is whether Ducommun stock is a good buy. In order to assess the appeal of the stock, I have entered the forward projections in my model. I have not entered any proceeds from the sale of the Monrovia facility, as we don’t know the gain on sale.

Stock price valuation for Ducommun using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

After entering the data in our stock price target model, we see that all bars are green, which visually already confirms a buy rating, perhaps even a strong buy rating, for the stock. Ducommun historically trades at a lower EV/EBITDA multiple compared to peers which I consider to be a positive since even when not valuing the company in line with peers there is upside. For 2023, that upside is rather limited, but I would also argue that 2024 is not far away at this point so looking at the 2024 upside is not premature. Furthermore, the gain on sale could be a big positive for the company that will drive some upside in 2023 and beyond. As a result, I mark shares of Ducommun a strong buy with a $55.25 price target representing 27% upside.

Conclusion: Vision 2027 Creates Value For Ducommun Shareholders

The most recent financial results are far from mind blowing, but Ducommun is working on achieving a bigger piece of a growing pie as there is growth in the commercial aerospace and defense industry which will result in more revenues for Ducommun and the company is also focusing on expanding its portfolio and aftermarket sales in both end markets while also growing the company via acquisitions. M&A activity always carries some execution risk, but Ducommun has shown in the past to be able to successfully integrate companies into its business. As a result, I consider the current Ducommun Incorporated price to be a nice entry point, as it carries a discount with respect to 2023 earnings and significant upside for 2024 and beyond.

For further details see:

Ducommun Aims For A Bigger Piece Of A Growth Pie